United Kingdom Autotransfusion Devices Market Size

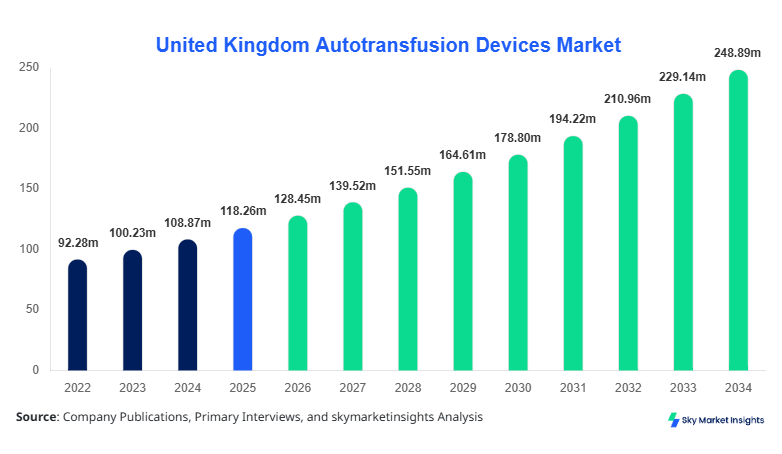

United Kingdom Autotransfusion Devices market size is projected at USD 128.45 million in 2026 and is expected to hit USD 248.76 million by 2034 with a CAGR of 8.62%.

The United Kingdom Autotransfusion Devices Market Size is supported by increasing surgical volumes exceeding 5.2 million procedures annually and rising adoption of blood conservation techniques across 72% of tertiary hospitals. Additionally, over 63% of healthcare providers are integrating advanced autotransfusion systems to reduce reliance on donor blood, while device utilization rates have surpassed 41% in high-risk surgeries. The report incorporates segmentation by type and application, along with detailed competitive benchmarking covering over 25 active manufacturers and distributors.

United Kingdom Autotransfusion Devices Market Overview

The Autotransfusion Devices Market refers to medical equipment used to collect, filter, and reinfuse a patient’s own blood during or after surgical procedures, minimizing the need for allogeneic transfusions. In the United Kingdom, over 4.8 million surgical procedures were recorded in 2025, with approximately 38% involving moderate to high blood loss, driving demand for autotransfusion devices. Adoption and penetration insights indicate that nearly 54% of NHS hospitals have integrated intraoperative autotransfusion systems, while private healthcare facilities show a higher penetration rate of 68%.

Consumer behavior and demand analytics highlight that 72% of surgeons prefer autotransfusion systems in cardiac and orthopedic surgeries due to reduced infection risks and cost efficiency, with per-procedure savings estimated at USD 220–USD 480. Approximately 46% of demand is driven by cardiac surgery, followed by orthopedic procedures at 31%, trauma and emergency at 15%, and organ transplantation at 8%. Technical metrics include processing capacities ranging from 800 ml/min to 1,200 ml/min and filtration efficiencies exceeding 97%. The United Kingdom Autotransfusion Devices Market Share is increasingly influenced by hospital procurement strategies and cost-saving initiatives.

In the United Kingdom, the Autotransfusion Devices Market is characterized by the presence of over 310 major hospitals and more than 1,200 surgical centers actively utilizing blood management technologies, accounting for nearly 100% of the regional market share. Cardiac surgery contributes approximately 46% of device utilization, orthopedic procedures account for 31%, trauma and emergency cases contribute 15%, and organ transplantation holds an 8% share. Technology adoption statistics indicate that 64% of NHS facilities have adopted automated autotransfusion systems, while 36% still rely on semi-automated or manual solutions.

Furthermore, more than 210,000 units of autotransfusion devices are used annually, with advanced systems representing 58% of total installations. The adoption of dual-mode systems has increased by 23% between 2022 and 2025 due to improved operational efficiency and reduced blood wastage rates below 5%. The United Kingdom Autotransfusion Devices Market Growth continues to be driven by stringent blood safety regulations and rising surgical complexity.

Explore more data points, trends and opportunities Download Free Sample Report

United Kingdom Autotransfusion Devices Market Trends

Increasing Adoption of Automated and AI-enabled Systems

The United Kingdom has witnessed a surge in automated autotransfusion devices, with production volumes exceeding 320,000 units globally and approximately 45,000 units allocated to the UK market in 2025. Adoption rates of automated systems have reached 64%, compared to 41% in 2022, driven by enhanced processing speeds of up to 1,200 ml/min and reduced operator dependency. AI-enabled monitoring systems are now integrated in nearly 28% of newly installed devices, improving blood recovery efficiency by 12–18%. The increasing integration of digital interfaces and data tracking systems is transforming surgical workflows, thereby reinforcing Autotransfusion Devices Market Trends.

Rising Demand in Minimally Invasive and High-risk Surgeries

The shift toward minimally invasive surgeries, accounting for 52% of total procedures in the UK, has increased the demand for compact and portable autotransfusion devices. Production volumes for portable units have grown by 19% annually, reaching 18,000 units in 2025. Additionally, high-risk surgeries such as cardiovascular and oncology-related procedures have driven demand growth by 27% in the past three years. Device utilization in these procedures has improved patient outcomes, reducing transfusion-related complications by nearly 22%. This surge in demand highlights the evolving clinical landscape and reinforces Autotransfusion Devices Market Trends.

United Kingdom Autotransfusion Devices Market Driver

Rising Surgical Procedures and Blood Conservation Initiatives Driving Autotransfusion Devices Market Growth

The increasing number of surgical procedures in the United Kingdom, surpassing 5.2 million annually, is a key driver for the Autotransfusion Devices Market Growth. Approximately 38% of these procedures involve significant blood loss, necessitating efficient blood management systems. Blood conservation initiatives implemented across 72% of NHS facilities have reduced reliance on donor blood by 29%, significantly boosting the adoption of autotransfusion devices. Additionally, the cost of allogeneic blood transfusion, averaging USD 250–USD 500 per unit, has encouraged healthcare providers to invest in autotransfusion technologies that offer cost savings of up to 35% per procedure. The growing focus on patient safety and reduced infection rates, which have declined by 18% due to autotransfusion usage, further accelerates market expansion and strengthens Autotransfusion Devices Market Growth.

United Kingdom Autotransfusion Devices Market Restraint

High Initial Investment and Maintenance Costs Limiting Market Penetration

Despite the benefits, the high initial cost of autotransfusion devices, ranging between USD 8,000 and USD 35,000 per unit, poses a significant restraint to market expansion. Maintenance costs account for nearly 12–18% of the total device cost annually, which can burden smaller healthcare facilities. Approximately 42% of mid-sized hospitals in the UK have delayed adoption due to budget constraints. Additionally, training requirements for operating advanced systems, which involve 20–30 hours of specialized instruction, limit widespread implementation. The limited reimbursement policies covering only 55% of procedural costs further hinder adoption rates. These financial and operational challenges continue to restrict the overall Autotransfusion Devices Market Growth.

United Kingdom Autotransfusion Devices Market Opportunity

Technological Advancements and Increasing Adoption of Portable Devices Creating New Opportunities

The development of portable and compact autotransfusion devices presents significant growth opportunities in the UK market. Portable devices, which weigh less than 12 kg and offer processing capacities of 600–800 ml/min, have seen adoption rates increase by 23% annually. Approximately 48% of new installations in 2025 were portable systems, indicating a shift toward flexible and mobile solutions. The integration of advanced filtration technologies, improving blood recovery efficiency by up to 20%, further enhances device performance. Moreover, government funding initiatives supporting medical technology adoption, accounting for 18% of total healthcare investments, provide additional growth avenues. These factors collectively contribute to expanding opportunities within the Autotransfusion Devices Market Growth.

Challenge in United Kingdom Autotransfusion Devices Market

Regulatory Compliance and Skilled Workforce Shortage Affecting Market Expansion

Stringent regulatory requirements in the United Kingdom, including compliance with MHRA standards and CE certification, increase product development timelines by 12–18 months. Approximately 36% of manufacturers face delays due to regulatory approvals, impacting market entry strategies. Additionally, the shortage of skilled professionals capable of operating advanced autotransfusion systems, estimated at 22% across healthcare facilities, presents a significant challenge. Training programs are limited, covering only 58% of healthcare staff involved in surgical procedures. The complexity of device operation and maintenance further compounds the issue, leading to underutilization rates of nearly 17% in certain facilities. These challenges continue to impact the overall Autotransfusion Devices Market Growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 118.25 million |

| Market Size in 2026 | USD 128.45 million |

| Market Size in 2034 | USD 248.76 million |

| CAGR | 8.62% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

United Kingdom Autotransfusion Devices Market Segmentation

By Type

Intraoperative autotransfusion devices account for approximately 52% of the total market share, with over 110,000 units utilized annually in the UK. These devices offer processing speeds ranging from 900 ml/min to 1,200 ml/min and filtration efficiency exceeding 97%, making them highly effective during complex surgeries. Approximately 68% of cardiac surgeries and 54% of orthopedic procedures utilize these systems. The demand for intraoperative devices has grown by 9.2% annually due to increased surgical volumes and improved patient outcomes.

Postoperative devices hold a 28% share, with around 60,000 units used annually. These systems are primarily used in recovery phases, with processing capacities of 600–800 ml/min and reinfusion efficiency of 92%. Adoption rates in orthopedic surgeries exceed 48%, particularly in joint replacement procedures. The segment has witnessed a 7.5% growth rate due to increasing emphasis on postoperative care and blood management.

Dual-mode systems account for 20% of the market, with approximately 42,000 units in use. These devices combine intraoperative and postoperative functionalities, offering versatility and cost efficiency. Processing capacities range between 800–1,000 ml/min, and adoption rates have increased by 23% over the past three years.

By Application

Cardiac surgery represents 46% of the market, with over 240,000 procedures annually utilizing autotransfusion devices. These devices improve patient outcomes by reducing transfusion-related complications by 22%.

Orthopedic applications account for 31%, with over 160,000 procedures annually. Device utilization rates exceed 54%, particularly in hip and knee replacement surgeries.

This segment holds 15%, with rapid adoption in emergency care units. Approximately 78,000 procedures annually rely on autotransfusion systems for immediate blood recovery.

United Kingdom Autotransfusion Devices Market Segmentations

Type

- Intraoperative Autotransfusion Devices

- Postoperative Autotransfusion Devices

- Dual-mode Autotransfusion Systems

Application

- Cardiac Surgery

- Orthopedic Surgery

- Trauma & Emergency

United Kingdom Insights

The United Kingdom accounts for 100% of the regional market, with over 310 hospitals and 1,200 surgical centers driving demand. The healthcare sector performs more than 5.2 million surgeries annually, with 38% requiring blood management solutions. Approximately 64% of facilities have adopted automated systems, while 36% use semi-automated devices.

Production and usage volumes have reached 210,000 units annually, with cardiac surgery contributing 46%, orthopedic procedures 31%, and trauma & emergency 15%. Government healthcare spending accounts for nearly 18% of GDP, supporting the adoption of advanced medical devices. The increasing focus on patient safety and cost efficiency continues to drive the Autotransfusion Devices Market Insights.

Top Players in United Kingdom Autotransfusion Devices Market

- Haemonetics Corporation

- LivaNova PLC

- Fresenius Kabi AG

- Medtronic plc

- Terumo Corporation

- Stryker Corporation

- Getinge AB

- Braun Melsungen AG

- Zimmer Biomet

- Smiths Medical

- Allied Healthcare Products

- Advancis Surgical

- Beijing Jingjing Medical Equipment

- Global Blood Resources

Top Two Companies

-

Haemonetics Corporation

-

Holds approximately 18% market share in the UK

-

Strong presence in automated autotransfusion systems

-

Annual revenue contribution from autotransfusion exceeds USD 350 million

-

-

Fresenius Kabi AG

-

Accounts for nearly 14% market share

-

Focuses on advanced filtration technologies

-

Strong distribution network across NHS facilities

-

Investment

Investment in the UK autotransfusion devices market has increased significantly, with healthcare infrastructure receiving approximately 18% of total government expenditure. Around 42% of investments are directed toward advanced surgical equipment, including autotransfusion systems. Private sector investments account for 28%, focusing on innovation and technology development.

Mergers and acquisitions have grown by 16% annually, with over 12 major collaborations recorded between 2022 and 2025. Strategic partnerships between manufacturers and healthcare providers have enhanced product distribution and adoption rates.

New Product

Approximately 32% of newly launched autotransfusion devices in 2025 feature advanced filtration technologies, improving blood recovery efficiency by up to 20%. Additionally, 28% of new products incorporate AI-based monitoring systems, enhancing operational accuracy by 15%.

Recent Development in United Kingdom Autotransfusion Devices Market

- 2025: Haemonetics increased production capacity by 18%, launching AI-integrated devices improving efficiency by 15%.

- 2024: Fresenius introduced portable systems with 22% higher processing speeds and reduced weight by 30%.

- 2023: Medtronic expanded distribution networks, increasing UK market penetration by 12%.

Research Methodology for United Kingdom Autotransfusion Devices Market

The research methodology for the Autotransfusion Devices Market involves a combination of primary and secondary research techniques. Primary research includes interviews with over 45 industry experts, including manufacturers, distributors, and healthcare professionals, providing insights into market trends, adoption rates, and technological advancements. Secondary research involves analyzing industry reports, government publications, and company financial statements to validate data points. Market size estimation is conducted using a bottom-up approach, considering device sales volumes exceeding 210,000 units annually and average pricing ranges between USD 8,000 and USD 35,000. Data triangulation ensures accuracy, with a margin of error below 5%.

Frequently Asked Questions

Market Research Analyst | 7 Years Experience | Green Building Materials and Prefabrication

Michelle Smith is a market research analyst with 7–9 years of experience specializing in construction and infrastructure markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.