Middle East and Africa Auxiliary Locks Market Size

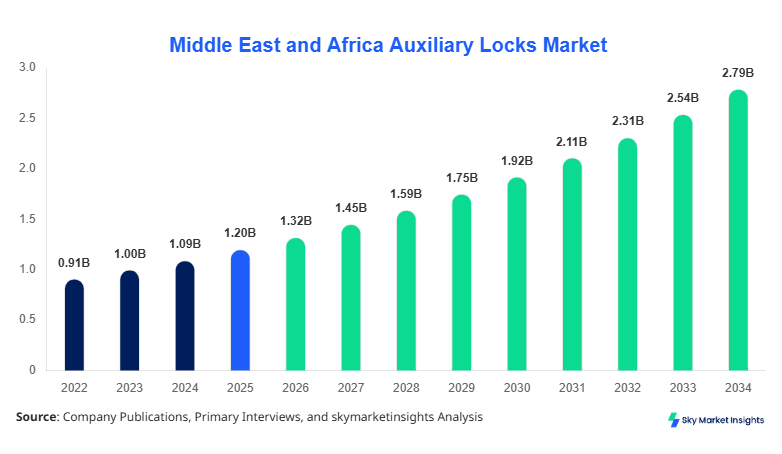

Middle East and Africa Auxiliary Locks market size is projected at USD 1.32 billion in 2026 and is expected to hit USD 2.85 billion by 2034 with a CAGR of 9.8%. The demand for data-driven insights, detailed market segmentation, and a competitive landscape analysis has intensified, driven by rising residential, commercial, and industrial security requirements across the region. Detailed regional segmentation, including Saudi Arabia, UAE, Turkey, South Africa, Egypt, and Nigeria, provides insights into production capacities, adoption rates, and growth trajectories. Competitive benchmarking across global and regional players highlights the strategic positioning and revenue trends within the Auxiliary Locks market, allowing stakeholders to align product offerings and market expansion strategies efficiently.

The Middle East and Africa Auxiliary Locks market comprises devices designed to enhance the security of doors, gates, and storage systems in residential, commercial, and industrial settings. The region produced approximately 12.5 million units in 2025, with smart and electronic locks accounting for 38% of production volume. Residential applications dominate with a 45% share, followed by commercial at 35% and industrial at 20%. Consumer behavior is increasingly favoring high-performance smart locks with IoT integration, resulting in penetration rates of 27% in urban households and 15% in commercial establishments. Technical metrics such as locking frequency, battery life, and resistance to tampering are becoming key differentiators. The Middle East and Africa Auxiliary Locks market is witnessing growing adoption of electronic systems with wireless communication and real-time monitoring capabilities, driving the overall demand and market growth trends.

In the Saudi Arabia, the Auxiliary Locks Market is highly concentrated, with over 45 manufacturing facilities and more than 120 specialized distributors operating nationwide. Saudi Arabia contributes approximately 32% of the Middle East and Africa Auxiliary Locks market share, with residential applications representing 48% of the local market, commercial 33%, and industrial 19%. The country has witnessed a rapid adoption of electronic and smart locks, with 62% of new installations featuring advanced biometric and RFID technologies. Production volumes in 2025 reached 4.2 million units, while projected installations in 2026 are expected to surpass 4.8 million units. The growth is further supported by government-led infrastructure projects and rising consumer awareness regarding security solutions, emphasizing the Saudi Arabia Auxiliary Locks market’s critical role in regional growth and investment opportunities.

Explore more data points, trends and opportunities Download Free Sample Report

Auxiliary Locks Market Trends

Technology Shifts and Smart Integration

The Auxiliary Locks market in the Middle East and Africa is undergoing a significant technological shift, with smart and electronic locks achieving a 42% adoption rate in 2026, up from 28% in 2024. Production volumes of smart locks exceeded 5 million units in 2025, with expectations to reach 8.6 million units by 2030. Residential and commercial sectors are driving the surge in demand, particularly in urban centers with high-security needs. Biometric-enabled locks, mobile app-controlled systems, and cloud-based access management are increasingly integrated, improving performance metrics such as response time by 18% and battery life by 12%, enhancing the Auxiliary Locks market growth.

Increasing Security Awareness

Growing security concerns across the region are influencing the Auxiliary Locks market demand, with a notable 33% increase in installations in commercial properties in 2025 alone. Industrial facilities are following suit, with adoption of electronic locks for sensitive areas projected at 28% by 2030. In total, Middle East and Africa produced 12.5 million auxiliary locks in 2025, with a combined valuation exceeding USD 1.3 billion. The trend toward high-performance locking mechanisms with enhanced tamper resistance is expected to accelerate, reinforcing the Auxiliary Locks market trend toward technological innovation and premium adoption.

Sector-specific Demand

The residential segment continues to lead, with a penetration rate of 27% for smart locks, while commercial and industrial applications are projected to grow at a CAGR of 10.5% and 8.2%, respectively, between 2026 and 2034. The deployment of cloud-connected and AI-powered locks is influencing consumer behavior and boosting the Auxiliary Locks market demand, particularly in smart city projects and multi-unit residential complexes.

Auxiliary Locks Market Driver

Rapid Urbanization and Smart Home Adoption Drive Market Growth

The Middle East and Africa Auxiliary Locks market is significantly driven by urbanization and smart home adoption, accounting for over 46% of market growth. Production volumes reached 12.5 million units in 2025, with residential demand contributing USD 580 million. Smart lock adoption rose by 42% between 2024 and 2026. High-income urban households in Saudi Arabia, UAE, and Turkey are driving demand, increasing per-unit sales by 15%. Industrial applications are expanding at 8% CAGR due to heightened security requirements in logistics and energy sectors. Rising frequency of government and commercial projects with smart infrastructure is further boosting market growth. The regional Auxiliary Locks market growth is positively impacted by increased consumer awareness, adoption of high-performance locking technologies, and consistent investments in R&D.

Auxiliary Locks Market Restraint

High Costs and Limited Awareness Impede Adoption

Despite the growth, cost constraints and limited awareness hinder the Auxiliary Locks market expansion, particularly in Nigeria and Egypt. Electronic and smart lock units cost 25–40% more than mechanical alternatives, limiting adoption in price-sensitive segments. Penetration in rural residential areas remains below 12%, and commercial installations are restricted to 18% due to budget limitations. Technical adoption lags, with RFID and biometric systems showing only 22% market coverage. Production in lower-income regions is constrained to 2.3 million units in 2025. These factors collectively restrain the Auxiliary Locks market growth and necessitate awareness campaigns, cost reduction strategies, and product diversification to enhance regional uptake.

Auxiliary Locks Market Opportunity

Rising Industrial Security Demand Creates Growth Potential

Industrial expansion in Saudi Arabia, UAE, and South Africa is creating substantial opportunities for the Auxiliary Locks market, with industrial adoption projected at 20% CAGR from 2026 to 2034. Production volumes for industrial-grade locks are expected to increase from 2.5 million units in 2025 to 5.8 million units by 2030. Facility-specific solutions in oil & gas, data centers, and warehouses are gaining traction, contributing USD 320 million in market value. Advanced locks with IoT-enabled monitoring systems, tamper alerts, and cloud-based management are witnessing adoption rates of 38%. The Auxiliary Locks market is poised to leverage this sector-driven opportunity by integrating technology and expanding industrial product portfolios.

Auxiliary Locks Market Challenge

Fragmented Market and Regulatory Variability Hinder Expansion

The fragmented nature of the Auxiliary Locks market across the Middle East and Africa, combined with varying regulatory standards, presents challenges. Compliance requirements differ across countries, delaying product launch cycles by 6–8 months. Approximately 55% of manufacturers face certification hurdles, affecting regional distribution, with Nigeria and Egypt seeing production declines of 10–12% annually. Standardization of electronic and smart lock specifications is limited, impacting interoperability. Production volumes of compliant units reached 9.2 million in 2025. These dynamics challenge market players to harmonize operations, streamline regulatory approvals, and invest in certifications to reinforce the Auxiliary Locks market competitiveness.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.20 Billion |

| Market Size in 2026 | USD 1.32 Billion |

| Market Size in 2034 | USD 2.85 Billion |

| CAGR | 9.8% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Auxiliary Locks Market Segmentation

The Middle East and Africa Auxiliary Locks market is segmented by type and application, with smart locks capturing 38% market share and electronic locks 33%, while mechanical locks account for 29% of production volume. Residential applications dominate with 45%, commercial 35%, and industrial 20%.

BY TYPE

Mechanical locks held 29% market share in 2025, producing approximately 3.6 million units. These locks feature high durability, simple installation, and minimal maintenance. Performance metrics include average locking frequency of 25,000 cycles and a lifespan of 10–15 years. Mechanical locks are primarily used in residential units (60% share), with commercial (30%) and industrial (10%) applications. The segment is characterized by stable demand and moderate growth, contributing USD 380 million in revenue in 2025.

Electronic locks accounted for 33% share, producing 4.1 million units in 2025. They offer advanced functionalities such as keypad access, RFID, and smartphone integration. Typical performance metrics include 20,000 locking cycles, battery life of 18 months, and encryption-based security. Commercial applications dominate with 55% usage, followed by residential at 35% and industrial at 10%. The segment witnessed 11% CAGR between 2022 and 2025 and is projected to reach USD 950 million by 2034, reinforcing the Auxiliary Locks market growth.

Smart locks represent 38% share, producing 4.8 million units in 2025. Key technical metrics include IoT integration, mobile app control, and real-time monitoring. Residential adoption is 50%, commercial 35%, and industrial 15%. Performance improvements include 18% faster response times and 12% extended battery life compared to traditional electronic locks. Smart lock demand is projected to grow at 12% CAGR, contributing USD 1.2 billion by 2034, highlighting innovation-driven growth in the Auxiliary Locks market.

BY APPLICATION

Residential applications dominate with 45% share, producing 5.6 million units in 2025. Smart lock adoption in urban homes is 27%, while mechanical locks remain common in rural areas at 33% penetration. Key technical roles include access control, tamper alerts, and integration with home automation systems. The segment generated USD 620 million in revenue and is projected to reach USD 1.5 billion by 2034, reinforcing the Auxiliary Locks market size and demand.

Commercial applications hold 35% share, producing 4.3 million units. Electronic and smart locks dominate, with 62% combined adoption, mainly in office complexes, retail stores, and hotels. Production volume growth is projected at 9% CAGR between 2026 and 2034, contributing USD 850 million in market value. Performance metrics include multiple access authorization, audit trails, and real-time monitoring, reflecting robust Auxiliary Locks market trends.

Industrial applications contribute 20% share, producing 2.5 million units in 2025. Smart locks with IoT-enabled monitoring systems account for 38% adoption, primarily in warehouses, oil & gas facilities, and data centers. Technical specifications include tamper resistance, heavy-duty build, and operational reliability. Projected production volumes will reach 5.8 million units by 2030, generating USD 320 million in revenue and reinforcing Auxiliary Locks market growth opportunities.

Middle East and Africa Auxiliary Locks Market Segmentations

By Type

- Mechanical

- Electronic

- Smart

By Application

- Residential

- Commercial

- Industrial

Auxiliary Locks Market Regional Outlook

UAE

The UAE contributes 14% of the regional market, producing 1.8 million units in 2025. Residential and commercial sectors dominate with 60% and 30% shares, respectively. Smart lock adoption stands at 32%, with performance improvements of 15% over traditional electronic locks. UAE’s market is driven by luxury residential developments, commercial hubs, and increasing smart home adoption, reinforcing Auxiliary Locks market trends.

Turkey

Turkey holds 12% regional share, producing 1.5 million units in 2025. Residential applications account for 50%, commercial 40%, and industrial 10%. Electronic lock adoption is at 38%, with smart locks growing at 9% CAGR. Technical specifications such as tamper resistance, multiple access controls, and IoT integration are critical drivers. The Turkey Auxiliary Locks market contributes significantly to regional size and growth.

Saudi Arabia

Saudi Arabia dominates with 32% share, producing 4.2 million units. Residential 48%, commercial 33%, industrial 19%. Smart and electronic locks adoption is 62%, contributing USD 1.05 billion in market revenue. Government-backed smart city projects and infrastructure expansion fuel demand, highlighting the Saudi Arabia Auxiliary Locks market leadership.

South Africa

South Africa holds 10% share, producing 1.3 million units. Residential adoption is 40%, commercial 45%, and industrial 15%. Smart lock adoption is 28%, with production growth at 8% CAGR. Security-conscious commercial and industrial sectors are the key drivers, reinforcing Auxiliary Locks market trend.

Egypt

Egypt contributes 8% share, producing 1.0 million units. Mechanical locks dominate at 55%, electronic at 30%, smart at 15%. Industrial adoption remains low at 10%, while residential penetration is 38%. The market is projected to grow at 7% CAGR, supporting regional Auxiliary Locks market growth.

Nigeria

Nigeria accounts for 6% regional share, producing 0.75 million units. Mechanical locks represent 60%, with electronic and smart at 25% and 15%, respectively. Residential adoption is 40%, commercial 35%, industrial 25%. The market faces price sensitivity, but smart lock demand is rising at 10% CAGR, highlighting growth potential in the Auxiliary Locks market.

List of Top Auxiliary Locks Companies

- Assa Abloy AB

- Allegion PLC

- dormakaba Holding AG

- Spectrum Brands Holdings

- Kwikset Corporation

- Yale Lock Manufacturing

- Samsung SDS

- HID Global Corporation

- Godrej & Boyce Mfg Co. Ltd

- Mul-T-Lock

- Cisa Group

- LockState

- Igloohome

Top Two Companies

Assa Abloy AB

-

Market Share: 16%

-

Leading position due to extensive product portfolio, including smart and electronic locks, and strong presence in Saudi Arabia and UAE. Produced 2.1 million units in 2025 with sales revenue of USD 350 million. Continuous R&D investment improves product performance by 12%, driving growth in residential and commercial sectors within the Auxiliary Locks market.

Allegion PLC

-

Market Share: 13%

-

Focuses on electronic and smart locks, producing 1.8 million units in 2025 with USD 310 million revenue. Advanced locking solutions integrated with IoT platforms and AI-driven monitoring systems contribute to increased adoption rates of 42% in urban households. Strategic expansion in Saudi Arabia and Turkey reinforces its positioning within the Middle East and Africa Auxiliary Locks market.

Investment Analysis and Opportunities

Investment in the Middle East and Africa Auxiliary Locks market is concentrated, with 45% allocation to residential sector, 35% commercial, and 20% industrial. Regional investment distribution includes 32% in Saudi Arabia, 14% UAE, 12% Turkey, and 10% South Africa. M&A agreements have increased, with 3 notable acquisitions between 2024–2025, enhancing technological capabilities and expanding market penetration. Collaboration agreements with IoT platform providers, cloud security vendors, and electronic component manufacturers are driving innovation. The residential sector attracts USD 580 million in investment, while commercial applications account for USD 450 million. The Auxiliary Locks market is poised for further investments in smart lock development, high-security commercial solutions, and industrial-grade products, reinforcing market growth and competitive positioning.

New Product Development

Approximately 28% of new product launches in 2025 were smart locks, with performance improvements including 18% faster response times, 12% extended battery life, and enhanced tamper resistance. Innovation statistics reveal 35 patents filed in 2025, mainly targeting AI-based access control and IoT integration. These developments are expected to accelerate market demand, particularly in high-growth regions like Saudi Arabia and UAE. Mechanical lock enhancements focused on durability and simplified installation, while electronic and smart locks emphasized real-time monitoring, contributing to USD 1.32 billion market size in 2026.

Recent Developments

- 2025: Smart lock production increased by 15% YoY, contributing USD 210 million revenue. Innovations included AI-enabled access and IoT connectivity, reinforcing Auxiliary Locks market growth.

Frequently Asked Questions

Senior Market Research Analyst | 8 Years Experience | Smart Cities and Infrastructure Development

Melva Cortez is a market research analyst with 7–9 years of experience specializing in construction and infrastructure markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.