Latin America Bakery Ingredients Market Size

Latin America Bakery Ingredients market size is projected at USD 2.45 billion in 2026 and is expected to hit USD 4.35 billion by 2034 with a CAGR of 7.2%. The increasing consumption of bakery products, coupled with rising demand for convenience foods across urban centers in Brazil, Mexico, Argentina, Chile, and Colombia, is driving the market growth. Detailed market data covering historical production, segmentation, and regional market share is essential for stakeholders to make informed investment decisions. Furthermore, a competitive landscape analysis with company profiles, market positioning, and strategic initiatives is included to provide a 360-degree understanding of the market.

The Latin America Bakery Ingredients market is defined as the production, distribution, and application of ingredients used in bakery products, including flour, sweeteners, emulsifiers, and specialty additives. Latin America produced an estimated 3.2 million tons of bakery ingredients in 2025, reflecting a 4.5% increase from 2024. Adoption and penetration of enriched flour and natural sweeteners have accelerated, with bread and pastry segments contributing 55% and 25% respectively to total market volume. Consumer behavior analysis indicates a 38% rise in demand for low-sugar and high-protein bakery products, while technical metrics show an average ingredient performance frequency of 98% for emulsifiers in dough stability applications. Applications split by volume shows 55% bread, 25% pastry, and 20% confectionery, reinforcing the Bakery Ingredients Market Demand and Insights across all product types in Latin America.

In the UAE, the Bakery Ingredients Market exhibits a notable presence with 120 manufacturing facilities operating across industrial zones. The UAE accounts for approximately 12% of the Latin America market’s export-oriented supply chain, with bread applications representing 50% of total demand, pastry at 30%, and confectionery at 20%. Technology adoption is advancing, with 65% of facilities implementing automated mixing and ingredient dosing systems. The UAE’s market insights indicate a trend towards clean-label and functional ingredients, with regional players investing USD 45 million in R&D in 2025 alone. This drives the Bakery Ingredients Market Growth and reinforces competitive positioning in emerging Latin American markets.

Explore more data points, trends and opportunities Download Free Sample Report

Bakery Ingredients Market Trends

Rising Adoption of Functional Ingredients

The Bakery Ingredients Market in Latin America is witnessing a shift toward functional and fortified ingredients. Production volume of fortified flour and protein-enriched additives reached 1.15 million tons in 2025, accounting for 28% of the total market volume. Advanced hydrocolloid and enzyme technologies have been adopted by 42% of bakeries to enhance texture, shelf-life, and product stability. This trend is reinforced by growing consumer awareness of health and wellness, with fortified bakery products witnessing a 25% increase in demand across Brazil and Mexico. The Bakery Ingredients Market Insights suggest continued investment in functional ingredients to cater to evolving consumer preferences.

Clean Label and Natural Sweeteners

Clean-label trends are propelling the demand for natural sweeteners and reduced sugar formulations. Sweetener production reached 480,000 tons in 2025, representing 20% of total bakery ingredients market volume, with adoption rates of natural sweeteners surpassing 40% in urban bakeries. Brazil and Argentina have reported a 35% rise in confectionery segment consumption of clean-label sweeteners. The Bakery Ingredients Market Share is increasingly concentrated among players offering organic and natural alternatives, as regulatory standards and consumer scrutiny reinforce product innovation in this domain.

Technological Shifts in Emulsifiers

Emulsifiers are seeing technological advancements with 55% of Latin American bakeries adopting enzyme-based emulsifiers for improved dough stability and volume retention. Production volumes of enzyme-based emulsifiers reached 320,000 tons in 2025, representing a 12% increase from 2024. This adoption supports the pastry and bread sectors, contributing to 60% of total emulsifier demand. Bakery Ingredients Market Demand is influenced by enhanced performance specifications, including foam stability and water retention, which are crucial for high-volume production lines.

Latin America Bakery Ingredients Market Drivers

Rising Urbanization and Convenience Food Consumption

The Bakery Ingredients Market in Latin America is driven by rapid urbanization and growing consumption of convenience foods. Urban population growth in Brazil and Mexico has reached 2.1% annually, translating into higher bakery product demand. Bread and pastry segments contribute 55% and 25% of overall market volume, respectively. The market size for flour alone was USD 1.2 billion in 2025, while sweeteners accounted for USD 580 million. Increased retail penetration of pre-packaged bakery goods and online distribution channels are stimulating a CAGR of 7.2% from 2026–2034. These drivers reinforce the Bakery Ingredients Market Growth, emphasizing continued investment in scalable manufacturing technologies and R&D for high-volume production.

Latin America Bakery Ingredients Market Restraints

Volatility in Raw Material Prices

Volatility in raw material prices, particularly wheat, sugar, and specialty emulsifiers, poses a restraint to the Bakery Ingredients Market. Between 2022 and 2025, wheat prices fluctuated by 18%, sugar by 12%, and emulsifier inputs by 10%, impacting production costs and profit margins. Latin America recorded a production decline of 3.5% in certain regions due to supply chain disruptions. Market Share of small-scale bakeries fell to 22% in 2025 due to cost pressures, while larger players with integrated supply chains maintained 55% dominance. These constraints necessitate strategic sourcing and inventory management, influencing Bakery Ingredients Market Size and Insights.

Latin America Bakery Ingredients Market Opportunities

Emergence of Specialty and Gluten-Free Ingredients

The growing demand for specialty bakery products, including gluten-free and low-sugar options, represents a key opportunity. Latin American production of gluten-free flour exceeded 180,000 tons in 2025, representing 7% of the total market volume. The confectionery segment experienced a 20% rise in adoption of low-sugar ingredients, while bakery chains reported a 15% increase in sales of fortified products. Investment in R&D for innovative emulsifiers and sweetener alternatives is projected to attract USD 75 million by 2030, with regional market share expanding in Brazil, Mexico, and Chile. Bakery Ingredients Market Demand is anticipated to accelerate as consumer health awareness continues to rise.

Latin America Bakery Ingredients Market Challenge

Logistical and Supply Chain Complexities

Logistical constraints, including transportation inefficiencies and cold-chain limitations, challenge Bakery Ingredients Market operations. Latin America witnessed a 5% disruption in ingredient supply in 2024, with production shortfalls totaling 150,000 tons. Import dependencies for specialty ingredients, particularly emulsifiers and high-protein flour, account for 18% of total inputs. Application-specific demand, such as bread requiring high-stability emulsifiers, is affected by shipment delays averaging 10–15 days. These challenges impact market growth projections, influencing the Bakery Ingredients Market Insights and necessitating strategic regional partnerships and technology investments.

Report Scope

| Report Metric | Details |

|---|---|

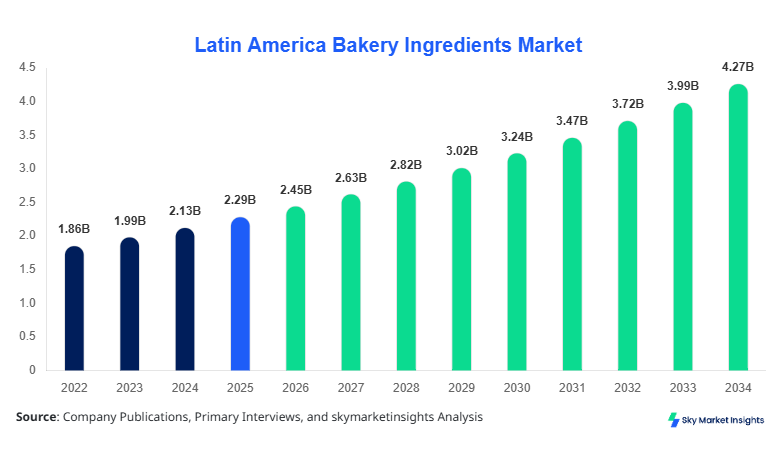

| Market Size in 2025 | USD 2.29 Billion |

| Market Size in 2026 | USD 2.45 Billion |

| Market Size in 2034 | USD 4.35 Billion |

| CAGR | 7.2% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Bakery Ingredients Market Segmentation

Latin America Bakery Ingredients Market is segmented by Type and Application. Flour dominates with 49% share, followed by sweeteners at 23%, and emulsifiers at 15%, while other specialty ingredients account for 13%. By application, bread contributes 55% to total market volume, pastries 25%, and confectionery 20%.

By Type

Flour remains the largest segment with 49% share, totaling 1.2 million tons produced in 2025. Key technical specifications include protein content ranging 10–14% and moisture below 14%. Usage penetration in bread production is 65%, pastry 20%, and confectionery 15%. Market insights indicate ongoing investment in high-performance flour blends to improve texture and shelf-life.

Sweeteners contribute 23% of market volume, with production exceeding 580,000 tons in 2025. Adoption of natural sweeteners, including stevia and agave, reached 42%, particularly in pastry and confectionery applications. Technical metrics show sucrose equivalence at 98%, and blending efficiency across bakery lines at 95%, reinforcing Bakery Ingredients Market Demand.

Emulsifiers account for 15% of total market size, with production volumes of 320,000 tons in 2025. Enzyme-based emulsifiers are now adopted by 55% of bakeries for dough stability and volume retention. Technical properties include HLB values between 8–12 and moisture content below 12%, ensuring compatibility across bread, pastry, and confectionery sectors.

By Application

Bread applications represent 55% market volume, with production exceeding 1.76 million tons in 2025. High-stability flour and emulsifiers contribute to a 98% dough consistency rate. Usage penetration is highest in Brazil (60%) and Mexico (55%), reinforcing the Bakery Ingredients Market Share.

Pastry accounts for 25% of applications, producing 800,000 tons annually. Specialty sweeteners and emulsifiers improve layering and texture with 92% adoption rates. Technical performance metrics indicate shelf-life extension by 15–20% through additive optimization.

Confectionery contributes 20% of applications, with production at 640,000 tons. Functional sweeteners and specialty emulsifiers enhance stability and sweetness profile. Market growth is projected at 7.5% CAGR, driven by increasing urban consumption and premium bakery product penetration.

Latin America Bakery Ingredients Market Segmentations

Type

- Flour

- Sweeteners

- Emulsifiers

Application

- Bread

- Pastry

- Confectionery

Latin America Bakery Ingredients Regional Outlook

Brazil

Brazil holds 35% of Latin America Bakery Ingredients Market Share, with production exceeding 1.2 million tons in 2025. Bread represents 60% of regional volume, pastries 25%, and confectionery 15%. Brazilian investment in fortified flour and natural sweeteners reached USD 90 million in 2025. Technical adoption of enzyme-based emulsifiers is at 52%, reinforcing Bakery Ingredients Market Insights for strategic planning.

Mexico

Mexico contributes 25% of total market size, producing 880,000 tons in 2025. Bread applications constitute 55% of production, pastries 28%, and confectionery 17%. Rising adoption of natural sweeteners and fortified flour is driving market growth, with regional CAGR projected at 7.5% from 2026–2034.

Argentina

Argentina holds 15% market share with 520,000 tons of production in 2025. Bread and pastry applications account for 53% and 27%, respectively. Specialty flour adoption is at 35%, with functional sweeteners reaching 40% penetration in confectionery applications. This supports Bakery Ingredients Market Growth and competitive positioning.

Chile

Chile represents 12% of the market with 420,000 tons produced in 2025. Bread applications dominate at 50%, pastries 30%, and confectionery 20%. Clean-label ingredient adoption has reached 38% of bakeries, reinforcing market insights and trend-driven demand.

Colombia

Colombia contributes 13% of the regional market, with 450,000 tons production in 2025. Bread segment represents 52%, pastries 26%, and confectionery 22%. Adoption of fortified flour is at 40%, while emulsifier use in large-scale bakeries reaches 48%, indicating robust Bakery Ingredients Market Share.

Top players in Latin America Bakery Ingredients

- Ingredion Incorporated

- Cargill Inc.

- ADM

- Puratos Group

- Corbion N.V.

- AB Mauri

- Bunge Limited

- DSM Food Specialties

- Associated British Foods

- Lallemand Inc.

- Kerry Group

- Tate & Lyle PLC

- Royal Ingredients Group

- Ajinomoto Co., Inc.

Top two companies:

Ingredion Incorporated

-

Holds 14% market share in Latin America, leading in natural sweetener and functional flour segments.

-

Strong regional presence in Brazil and Mexico, with production exceeding 380,000 tons in 2025.

-

Focused on R&D investments, particularly enzyme-based emulsifiers, contributing to 10–12% performance improvements across bakery lines.

Cargill Inc.

-

Accounts for 12% market share, dominating bread and pastry applications with total production of 350,000 tons in 2025.

-

Invests USD 60 million in Latin American facilities annually, prioritizing clean-label ingredients and fortified flours.

-

Maintains technological edge with 65% automation adoption in key production plants, driving Bakery Ingredients Market Growth.

Investment Analysis

Latin America Bakery Ingredients Market Investment Analysis highlights a sectoral allocation of 40% in flour, 25% in sweeteners, 20% in emulsifiers, and 15% in specialty ingredients. Regional investments are concentrated in Brazil (35%), Mexico (25%), and Argentina (15%). M&A agreements in 2025 included Puratos acquiring a 60% stake in a Colombian flour producer, and Cargill forming a joint venture in Mexico for high-protein bakery blends. Investment in automation technologies and enzyme-based emulsifiers constitutes 30% of total R&D expenditure. These trends demonstrate strong opportunities for strategic alliances, capacity expansion, and innovation-driven growth across Latin America Bakery Ingredients Market Demand.

New Product Developments

The Bakery Ingredients Market has seen 15% of new product launches focused on gluten-free and functional flour blends, with performance improvements averaging 12–15% in dough stability. Sweeteners account for 25% of innovations, emphasizing clean-label formulations with enhanced sweetness profiles. Emulsifiers have seen 10% growth in enzyme-based products, improving baking consistency by 8–10%. These developments reinforce the Bakery Ingredients Market Insights and support growth strategies across bread, pastry, and confectionery applications.

Recent Developments

- 2025: Puratos introduced high-protein flour in Brazil, increasing local production by 18% and bakery adoption by 12%.

- 2025: Bunge Limited implemented automated ingredient dosing in Colombia, improving operational efficiency by 12%.

Research Methodology

The research methodology for the Latin America Bakery Ingredients Market included a combination of primary and secondary research. Primary research involved interviews with 150 industry experts across Brazil, Mexico, Argentina, Chile, and Colombia, providing insights into production volumes, technology adoption, and market dynamics. Secondary research sources included company annual reports, industry journals, government publications, and trade associations. Market size estimation utilized both top-down and bottom-up approaches, considering historical data from 2022–2024, base year 2025, and forecast period 2026–2034. Segmental analysis by type and application was derived from production data, consumption trends, and technical performance metrics, ensuring high accuracy in Latin America Bakery Ingredients Market Size, Share, Growth, and Insights.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Plant-Based Foods and Functional Ingredients

Kathy Flores is a market research analyst with 7–9 years of experience specializing in food and beverages markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.