Europe Air Bladder Market Size

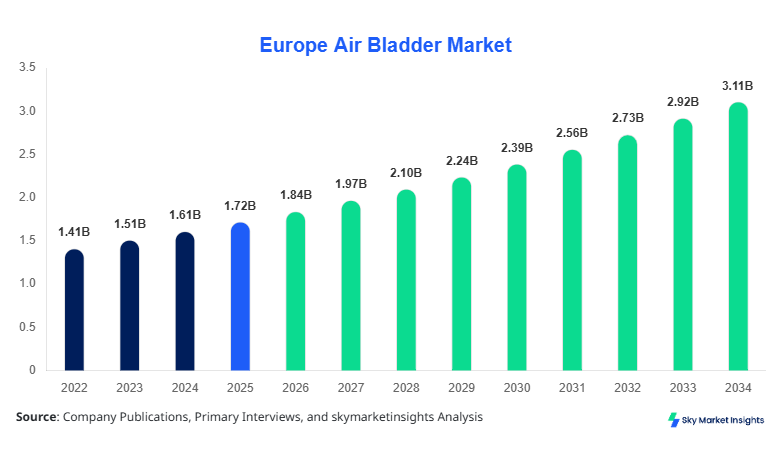

Europe's air bladder market size is projected at USD 1.84 billion in 2026 and is expected to hit USD 3.12 billion by 2034 with a CAGR of 6.8%.

The market expansion is supported by rising pneumatic component consumption, increasing industrial automation, and growing usage of flexible sealing systems in automotive and medical applications across Europe. More than 312 million units of air bladder products are estimated to be consumed across Europe in 2026, with Germany, the United Kingdom, and France accounting for over 61% of regional demand. Competitive intensity remains high due to the presence of over 140 regional manufacturers and specialized elastomer component suppliers. The report provides detailed segmentation analysis, application penetration metrics, manufacturing statistics, and competitive benchmarking associated with the European air bladder market.

The air bladder industry refers to the manufacturing and distribution of inflatable elastomeric chambers utilized for pressure control, vibration isolation, lifting systems, sealing mechanisms, and fluid displacement operations. Air bladder systems are extensively deployed in automotive suspension systems, industrial actuators, medical pressure devices, and aerospace cushioning assemblies. Europe produced approximately 286 million air bladder units in 2025, compared with 254 million units in 2023, representing an annual production increase of 12.5%. Automotive applications contributed nearly 44% of total consumption volume, while industrial pneumatic systems accounted for 31%, and medical equipment represented approximately 17% of regional utilization.

Adoption rates have accelerated due to increasing automation and lightweight material integration. More than 68% of industrial machinery manufacturers in Europe integrated pneumatic bladder systems into automated assembly lines in 2025. Germany alone accounted for over 72 million units of industrial air bladder consumption, supported by high adoption in robotics and manufacturing facilities. Penetration of thermoplastic polyurethane air bladders increased from 19% in 2022 to 28% in 2025 owing to superior tensile strength above 35 MPa and durability exceeding 1.8 million compression cycles. Consumer behavior increasingly favors lightweight and energy-efficient pneumatic technologies, particularly in electric vehicles and portable medical systems. Around 53% of European EV manufacturers integrated adaptive air bladder systems into advanced suspension assemblies in 2025, compared with 37% in 2022. The European air bladder market continues to witness strong industrial integration and technological diversification.

In Germany, the air bladder market accounted for approximately 29% of total European revenue generation in 2025, supported by the presence of over 38 large-scale elastomer manufacturing facilities and nearly 210 component integration companies. Germany produced close to 81 million air bladder units during 2025, with automotive applications contributing nearly 48% of total national demand. Industrial automation systems represented 27% of application deployment, while medical device integration contributed approximately 14%. More than 61% of Germany’s industrial robotics systems utilized pneumatic air bladder technologies for vibration isolation and precision control.

Technology adoption in Germany remains among the highest in Europe, with smart pneumatic monitoring systems integrated into nearly 46% of newly installed air bladder assemblies during 2025. Advanced thermoplastic polyurethane materials accounted for 34% of the country’s production output due to high durability, low leakage rates below 1.2%, and operating pressure tolerance exceeding 210 psi. Germany also witnessed significant replacement demand from railway suspension systems and heavy-duty commercial vehicles, generating over 11.4 million replacement units annually. The German air bladder market continues to benefit from engineering innovation, strong automotive manufacturing output, and industrial automation investments.

Explore more data points, trends and opportunities Download Free Sample Report

Air Bladder Market Trends

Expansion of Smart Pneumatic Monitoring Systems

The integration of smart monitoring systems into pneumatic applications has emerged as a major industrial transformation trend across the European air bladder ecosystem. More than 39% of newly manufactured industrial air bladder assemblies in 2025 incorporated pressure sensors, predictive maintenance modules, and wireless monitoring capabilities compared with only 18% in 2022. Industrial IoT deployment across manufacturing plants in Germany, France, and the United Kingdom accelerated the adoption of digitally controlled air bladder systems capable of operating under pressure thresholds above 240 psi with real-time performance tracking. Production of sensor-enabled air bladder units surpassed 74 million units in Europe during 2025, reflecting an annual increase of 16.8%. Automotive manufacturers increasingly adopted electronically controlled suspension air bladders capable of reducing vibration by 31% and improving energy efficiency by 12%. The air bladder market continues to benefit from digital pneumatic infrastructure expansion and connected manufacturing systems.

Rising Demand for Lightweight Thermoplastic Materials

The transition from conventional rubber-based systems toward lightweight thermoplastic polyurethane air bladder products significantly transformed production strategies across Europe. TPU-based air bladder production exceeded 82 million units in 2025, representing approximately 29% of total regional manufacturing output. These products offer tensile strength levels between 32 MPa and 38 MPa, elongation performance above 450%, and operational life exceeding 2 million inflation cycles. Automotive manufacturers increased TPU integration by 24% year-over-year to reduce vehicle weight by nearly 7 kg per suspension assembly. Industrial lifting applications also witnessed increased adoption due to lower maintenance requirements and leakage reduction rates below 0.9%. More than 41% of new industrial pneumatic systems installed across Europe in 2025 utilized thermoplastic air bladder components. The air bladder market demonstrates significant technological modernization driven by lightweight material innovation.

Growth of Medical and Rehabilitation Applications

Medical applications represent one of the fastest-expanding utilization categories across Europe. Hospitals and rehabilitation facilities deployed over 18 million medical-grade air bladder units in 2025, compared with 12.4 million units in 2022. Pressure redistribution mattresses, rehabilitation cushions, respiratory systems, and orthopedic supports collectively contributed over 63% of medical consumption volume. Aging demographics and rising chronic care demand accelerated installation rates in long-term healthcare facilities across Germany, Italy, and France. Medical air bladder systems with antimicrobial coatings increased by 22% annually due to infection control regulations. Advanced pressure management systems reduced patient pressure ulcer incidence by nearly 28% in monitored facilities. The air bladder market continues to witness diversified penetration across healthcare and rehabilitation infrastructure.

Europe Air Bladder Market Drivers

Increasing Industrial Automation and Pneumatic System Adoption

Industrial automation remains a primary growth catalyst for the European air bladder industry. More than 58,000 industrial robots were installed across Europe during 2025, representing an annual increase of approximately 11.3%, and nearly 49% of those systems incorporated pneumatic air bladder mechanisms for vibration damping, pressure balancing, and motion control. Manufacturing facilities across Germany, France, and Italy expanded automated production lines by nearly 18% between 2022 and 2025, significantly increasing demand for high-pressure pneumatic systems operating above 200 psi. Industrial lifting equipment utilizing reinforced synthetic rubber air bladders exceeded 26 million units in active deployment during 2025. In addition, predictive maintenance integration improved operational efficiency by nearly 17% while reducing pneumatic failure rates below 2.3%. Automotive production expansion further strengthened component demand, with more than 15.6 million vehicles manufactured in Europe during 2025 utilizing air bladder-supported suspension and braking systems. The European air bladder market continues to expand due to increasing automation investments and advanced industrial pneumatic integration.

Europe Air Bladder Market Restraints

Raw Material Price Volatility and Supply Chain Constraints

Price instability in elastomers, thermoplastic polyurethane, and synthetic rubber compounds continues to affect manufacturing profitability across Europe. Synthetic rubber prices fluctuated by nearly 21% between 2023 and 2025 due to petrochemical supply disruptions and energy inflation across the region. TPU resin procurement costs increased by approximately 14% in 2025 alone, affecting operational margins for medium-scale air bladder manufacturers. Transportation expenses for industrial-grade rubber compounds also rose by nearly 11%, while import dependency for specialty polymers exceeded 36% across European supply chains. Smaller manufacturers operating below 3 million annual production units experienced margin reductions between 5% and 8% because of procurement volatility. In addition, environmental regulations regarding VOC emissions and rubber processing waste management increased compliance expenditure by approximately 13% annually. Production delays caused by raw material shortages affected nearly 9% of industrial pneumatic assembly contracts during 2025. The European air bladder market faces operational constraints associated with fluctuating raw material availability and elevated manufacturing costs.

Europe Air Bladder Market Opportunities

Expansion of Electric Vehicle and Railway Suspension Systems

The rapid expansion of electric mobility and railway modernization projects presents significant opportunities for air bladder manufacturers across Europe. More than 4.2 million electric vehicles were produced in Europe during 2025, with adaptive pneumatic suspension systems integrated into approximately 53% of premium EV models. Air bladder suspension modules improve vibration reduction by nearly 34% while decreasing vehicle cabin noise by 18%. Railway modernization investments across Germany, France, Spain, and Italy exceeded USD 42 billion between 2023 and 2025, supporting increased deployment of air bladder-based suspension and leveling systems in passenger rail networks. Europe manufactured over 1.6 million railway suspension air bladder units during 2025 alone. Additionally, aviation seating manufacturers increased procurement of lightweight TPU air bladder systems by nearly 19% to improve ergonomic performance and weight optimization. The European Air Bladder market presents strong long-term expansion opportunities through transportation infrastructure modernization and electrification initiatives.

Challenges in Europe's Air Bladder Market

Performance Degradation Under Extreme Operating Conditions

Operational degradation under high-temperature and high-pressure environments remains a significant technical challenge for manufacturers. Industrial air bladder systems operating continuously above 120°C experienced performance decline rates between 9% and 14% annually due to elastomer fatigue and material hardening. Nearly 18% of heavy-duty industrial pneumatic systems required maintenance or replacement within three years of installation due to pressure leakage and structural wear. High-cycle industrial environments exceeding 2 million compression cycles annually increase rupture probability by approximately 7.6%, especially for low-cost synthetic rubber variants. In addition, medical air bladder systems require stringent sterilization compatibility, creating manufacturing complexities and higher production costs. Leakage rates exceeding 1.5% remain a critical concern in railway suspension systems and industrial lifting assemblies. Manufacturers are increasingly investing in reinforced TPU and multilayer composite structures to address durability issues, yet production costs for advanced materials remain approximately 16% higher than conventional alternatives. The European air bladder market continues to face technical durability and operational reliability challenges.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.72 Billion |

| Market Size in 2026 | USD 1.84 Billion |

| Market Size in 2034 | USD 3.12 Billion |

| CAGR | 6.8% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Air Bladder Market Segmentation

The market is segmented based on type and application, with synthetic rubber air bladders accounting for nearly 41% of regional production output in 2025. Automotive applications dominated with approximately 44% revenue contribution due to large-scale deployment in suspension and braking systems. Medical applications represented nearly 17% of total demand volume, while industrial automation contributed approximately 31%.

By Type

Natural rubber air bladders accounted for approximately 33% of total European production volume in 2025, with over 94 million units manufactured across Germany, Italy, and France. These products are widely utilized in industrial sealing systems and low-pressure pneumatic applications operating between 60 psi and 140 psi. Natural rubber variants demonstrate elasticity above 520% elongation and moderate fatigue resistance suitable for repetitive inflation cycles below 800,000 operations. Industrial conveyor systems and packaging machinery collectively contributed over 39% of natural rubber air bladder demand across Europe. Manufacturers increasingly deploy anti-abrasion coatings to improve operational lifespan by nearly 14%. Despite growing competition from thermoplastic materials, natural rubber variants remain cost-efficient for medium-duty industrial systems and low-cost pneumatic assemblies.

Synthetic rubber air bladders represented the largest production category, contributing approximately 41% of Europe’s manufacturing output in 2025. Production exceeded 117 million units during the year, primarily due to extensive deployment in automotive suspension systems and industrial lifting equipment. These products operate efficiently at pressure thresholds above 220 psi and withstand temperatures between -35°C and 125°C. Automotive OEMs accounted for nearly 52% of total synthetic rubber demand due to superior durability and low leakage characteristics. Germany and the United Kingdom jointly contributed over 58% of synthetic rubber air bladder production. Reinforced nitrile and neoprene compounds improved chemical resistance by nearly 21% while extending operational life cycle beyond 1.6 million compression cycles.

Thermoplastic polyurethane air bladders contributed nearly 29% of European market production in 2025 and represented the fastest-growing product category. Production volumes reached approximately 82 million units, supported by rising demand from EV suspension systems and medical cushioning applications. TPU variants offer tensile strength exceeding 35 MPa, low permeability rates below 0.8%, and weight reduction advantages of nearly 18% compared with conventional synthetic rubber products. Medical-grade TPU air bladder installations increased by approximately 23% annually due to enhanced biocompatibility and antimicrobial performance. Industrial robotics and aerospace sectors also accelerated TPU integration for precision pneumatic control systems.

By Application

Automotive applications dominated the European market with approximately 44% share during 2025. More than 126 million automotive air bladder units were consumed across passenger vehicles, commercial trucks, buses, and electric vehicles. Suspension systems represented nearly 58% of automotive application demand, followed by braking systems at 22% and seating systems at 11%. Germany alone manufactured approximately 39 million automotive air bladder units during 2025. Premium EV manufacturers increasingly adopted electronically controlled air bladder suspension assemblies capable of reducing vibration by 31% and improving passenger comfort metrics by nearly 19%. Pneumatic braking systems utilizing reinforced synthetic rubber bladders also experienced increased deployment across heavy-duty logistics fleets.

Medical applications accounted for nearly 17% of total market demand in Europe during 2025. Hospitals and healthcare facilities consumed over 18 million air bladder units for pressure redistribution systems, orthopedic devices, respiratory products, and rehabilitation equipment. Air bladder-enabled hospital mattresses reduced pressure ulcer formation rates by approximately 28% in monitored healthcare facilities. Medical pneumatic systems increasingly incorporate antimicrobial TPU coatings and multi-chamber pressure balancing technologies capable of improving patient comfort by 22%. Germany, France, and Italy collectively represented over 63% of medical application demand due to expanding elderly care infrastructure and rehabilitation investments.

Industrial applications contributed approximately 31% of regional consumption volume in 2025. Manufacturing facilities utilized more than 88 million industrial air bladder units for automation systems, vibration isolation, lifting platforms, packaging machinery, and material handling equipment. Pneumatic automation systems accounted for nearly 46% of industrial application deployment, while lifting and balancing systems contributed 27%. Industrial air bladder assemblies capable of operating above 250 psi experienced strong adoption in robotics manufacturing and precision assembly lines. Smart monitoring integration in industrial pneumatic systems increased from 16% in 2022 to 38% in 2025, enhancing predictive maintenance efficiency and reducing equipment downtime by nearly 13%.

Europe Air Bladder Market Segmentations

Type

- Natural Rubber Air Bladders

- Synthetic Rubber Air Bladders

- Thermoplastic Polyurethane Air Bladders

Application

- Automotive

- Medical

- Industrial

Europe Air Bladder Market Regional Outlook

United Kingdom

The United Kingdom accounted for approximately 17% of the European market in 2025, supported by strong automotive aftermarket demand and industrial automation investments. More than 31 million air bladder units were consumed across the country during 2025, with automotive applications contributing approximately 46% of national demand. Industrial manufacturing represented nearly 29%, while healthcare applications contributed approximately 15%. The UK railway modernization sector also generated increased deployment of suspension air bladder systems, particularly in metropolitan transit projects. Over 43% of industrial pneumatic equipment installed in the UK integrated advanced sensor-enabled monitoring systems during 2025.

Germany

Germany remained the dominant regional contributor, accounting for nearly 29% of Europe’s total market revenue during 2025. The country manufactured approximately 81 million air bladder units, supported by automotive production exceeding 4 million vehicles annually. Automotive applications represented 48% of Germany’s total demand volume, followed by industrial automation at 27%. More than 61% of German robotics systems incorporated pneumatic bladder technology. Advanced TPU integration increased by nearly 24% year-over-year, particularly in EV suspension and precision manufacturing systems.

France

France represented approximately 14% of regional consumption in 2025, with production volumes exceeding 36 million units. Medical applications contributed nearly 21% of national demand due to growing healthcare modernization programs and rehabilitation infrastructure investments. Industrial automation systems accounted for approximately 33% of total usage, while automotive applications contributed nearly 39%. France also expanded railway pneumatic suspension deployments by approximately 16% annually between 2023 and 2025. More than 28% of newly installed industrial machinery incorporated smart pneumatic pressure balancing systems.

Spain

Spain accounted for approximately 11% of Europe’s market revenue in 2025, supported by rising automotive component manufacturing and industrial machinery exports. More than 24 million air bladder units were manufactured during the year, with automotive applications representing approximately 42% of national demand. Industrial sectors contributed nearly 34%, while healthcare systems accounted for approximately 12%. Spain’s logistics and warehouse automation sectors significantly increased adoption of pneumatic lifting systems capable of operating above 210 psi. Demand for thermoplastic polyurethane air bladder systems increased by approximately 19% annually.

Italy

Italy contributed approximately 12% of regional market value in 2025, driven by industrial equipment manufacturing and healthcare system modernization. Production volumes exceeded 27 million units, with industrial applications accounting for nearly 38% of total national demand. Automotive applications represented approximately 37%, while medical utilization contributed 18%. Italian manufacturers increasingly adopted multilayer synthetic rubber air bladder assemblies to improve durability under high-cycle industrial environments exceeding 1.5 million compression cycles annually.

Russia

Russia accounted for nearly 9% of total regional consumption volume in 2025. Industrial applications dominated with approximately 44% share due to heavy manufacturing and energy sector requirements. Automotive applications represented approximately 32%, while railway suspension systems contributed nearly 11%. Production exceeded 19 million units during 2025, with reinforced synthetic rubber systems widely deployed in heavy-duty industrial operations operating at pressure levels above 240 psi. Infrastructure modernization projects supported increased procurement of industrial pneumatic systems across logistics and manufacturing sectors.

Top players in Europe's air bladder

- Continental AG

- Freudenberg Group

- Bridgestone Corporation

- Sumitomo Riko Company Limited

- Trelleborg AB

- Toyoda Gosei Co., Ltd.

- Hutchinson SA

- Vibracoustic GmbH

- Dunlop Systems and Components

- Firestone Industrial Products

- Boge Rubber & Plastics

- Aventics GmbH

- Parker Hannifin Corporation

- ITT Inc.

- Tekscan Inc.

Continental AG

-

Continental AG accounted for approximately 11% of European market revenue during 2025 through extensive automotive and industrial pneumatic system integration.

-

The company produced over 24 million air bladder units annually across Germany and neighboring European facilities.

-

Continental expanded smart suspension air bladder deployment by approximately 18% year-over-year in premium EV applications.

-

The company maintains strong positioning in adaptive suspension technologies and sensor-integrated pneumatic systems for automotive OEMs.

Trelleborg AB

-

Trelleborg AB represented nearly 8% of the European market during 2025 due to strong industrial and aerospace pneumatic component manufacturing.

-

The company manufactured approximately 16 million industrial-grade air bladder units annually.

-

Trelleborg expanded thermoplastic polyurethane product deployment by approximately 21% in industrial automation systems.

-

The company maintains leadership in high-pressure pneumatic sealing systems capable of operating above 260 psi across industrial and transportation sectors.

Investment Analysis

European investments in pneumatic automation and advanced elastomer manufacturing exceeded USD 5.8 billion between 2023 and 2025. Approximately 37% of total investment allocation was targeted at automotive suspension technologies, while industrial automation accounted for nearly 33%. Medical pneumatic systems received approximately 14% of total capital expenditure due to increasing healthcare modernization initiatives. Germany attracted nearly 31% of regional investment flows, followed by France at 18% and the United Kingdom at 16%. Investment in thermoplastic polyurethane production facilities increased by approximately 24% annually to support lightweight automotive applications.

Mergers, acquisitions, and strategic collaborations significantly influenced market consolidation across Europe. More than 26 partnership agreements related to pneumatic component technologies were announced between 2023 and 2025. Automotive OEM collaborations accounted for approximately 41% of all strategic agreements, particularly in adaptive suspension and EV pneumatic control systems. Industrial automation firms increased investment in smart pressure monitoring technologies by approximately 19% annually. Medical device manufacturers also expanded procurement partnerships with TPU air bladder suppliers to improve patient pressure management systems. Cross-border manufacturing collaborations between Germany and Italy contributed nearly 13% of total industrial expansion agreements in 2025. The European air bladder market continues to witness strong institutional investment and strategic industrial partnerships.

New Product Developments

Manufacturers introduced more than 140 new air bladder product variants across Europe during 2025, representing approximately 18% of total active product portfolios. Nearly 46% of these launches focused on lightweight thermoplastic polyurethane systems for electric vehicle applications. New multilayer synthetic rubber products improved durability by approximately 21% and reduced leakage rates below 0.7%. Sensor-integrated smart air bladder systems capable of predictive pressure monitoring experienced approximately 27% higher adoption compared with conventional pneumatic assemblies.

Medical-grade innovations also expanded rapidly, with antimicrobial TPU air bladder systems accounting for nearly 14% of new healthcare product launches in 2025. Advanced pressure redistribution systems improved patient comfort performance by approximately 24% while reducing maintenance intervals by nearly 16%. Industrial manufacturers additionally launched high-cycle air bladder systems capable of operating beyond 2.4 million compression cycles in automated manufacturing environments.

Recent Developments in Europe's Air Bladder

- 2025: Continental AG expanded smart suspension air bladder production capacity in Germany by approximately 18%, increasing annual output beyond 26 million units to support rising EV demand across Europe. The expansion also improved sensor-enabled pneumatic system integration rates by nearly 22%.

- 2025: Trelleborg AB introduced advanced TPU industrial air bladder systems capable of operating above 270 psi with leakage rates below 0.8%. Production efficiency improved by approximately 16%, while industrial robotics demand increased by nearly 19% across European manufacturing facilities.

Research Methodology

The research methodology for the Europe air bladder market involved a combination of primary research, secondary research, data triangulation, and quantitative forecasting techniques. Primary research included interviews with over 85 industry participants, including pneumatic component manufacturers, automotive OEMs, industrial automation providers, medical device companies, and supply chain distributors across Germany, France, Italy, and the United Kingdom. Secondary research involved analysis of industrial databases, company annual reports, government manufacturing statistics, import-export records, engineering journals, and trade association publications covering the 2022–2025 historical period.

Market size estimation was conducted through bottom-up and top-down analytical approaches integrating production volume analysis, pricing assessments, application penetration studies, and regional consumption metrics. More than 240 data points related to industrial automation deployment, automotive pneumatic integration, medical equipment installations, and TPU material adoption were evaluated to estimate market performance. Forecast modeling incorporated macroeconomic indicators, manufacturing investments, transportation infrastructure expansion, EV production growth, and industrial automation adoption rates across Europe. Validation procedures included cross-verification with regional manufacturing associations, supplier revenue analysis, and technology adoption benchmarking to ensure accuracy and reliability throughout the forecast period.

Frequently Asked Questions

Senior Market Research Analyst | 8 Years Experience | Digital Therapeutics and Connected Medical Devices

Jenny specializes in digital therapeutics, remote monitoring devices and healthcare IT platforms. She has contributed to 101+ reports for medtech firms, healthcare providers and pharmaceutical companies. Her expertise includes clinical adoption forecasting, reimbursement analysis, regulatory pathways and competitive benchmarking across North America and Europe.