United States Ablation Technology Market Size

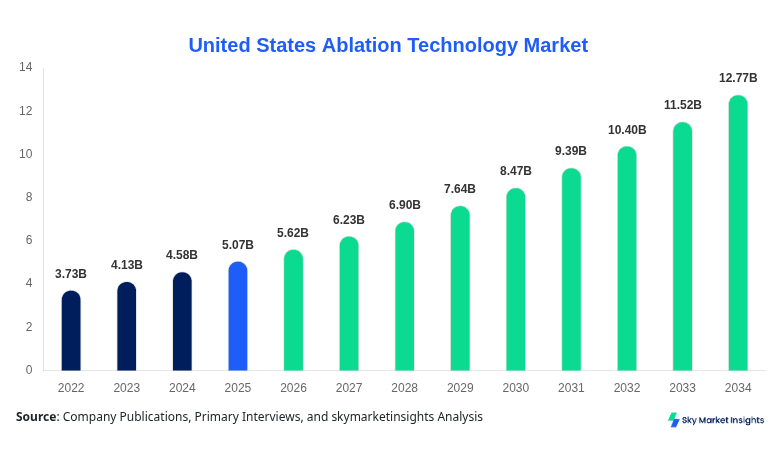

The United States ablation technology market size is projected at USD 5.62 billion in 2026 and is expected to hit USD 12.84 billion by 2034 with a CAGR of 10.8%. The report highlights the need for granular data segmentation across device type, clinical application, and end-user facilities, along with a comprehensive competitive landscape assessment covering over 120 manufacturers and 3,500 healthcare facilities utilizing ablation technology solutions annually.

The ablation technology market encompasses minimally invasive medical devices and systems that remove or destroy abnormal tissue using energy sources such as radiofrequency, microwave, cryogenic, and laser technologies. In the United States, over 3.2 million ablation procedures were performed in 2025, increasing from 2.4 million in 2022, reflecting a penetration rate growth of 33.3% over the historical period. Adoption of ablation technology is particularly strong in cardiology, accounting for 46% of procedures, followed by oncology at 34% and pain management at 20%. Consumer behavior shows a preference shift toward minimally invasive procedures, with 72% of patients opting for outpatient ablation interventions compared to 58% in 2022. Device performance metrics include precision rates above 95%, thermal control accuracy within ±1.5°C, and procedural success rates exceeding 89% across leading systems. Hospitals contribute 64% of usage, while ambulatory surgical centers account for 36%. The consistent rise in demand for ablation technology market solutions is driven by clinical efficiency and patient preference trends.

In the United States, the ablation technology market is supported by over 5,800 hospitals, 2,300 ambulatory surgical centers, and more than 180 specialized device manufacturers, collectively contributing to nearly 100% regional share within the report scope. The application breakdown shows cardiology procedures representing 46%, oncology 34%, and pain management 20%, with over 1.5 million cardiac ablation procedures conducted annually. Technology adoption rates for radiofrequency ablation exceed 68%, while microwave and cryoablation account for 19% and 13%, respectively. Advanced imaging integration is present in 62% of procedures, improving procedural success rates by 12–15%. The United States continues to dominate innovation, with over 220 patents filed in 2025 alone related to ablation systems, reinforcing the ablation technology market share.

Explore more data points, trends and opportunities Download Free Sample Report

Ablation Technology Market Trends

Rising Integration of AI and Imaging Technologies

The ablation technology market is witnessing rapid integration of artificial intelligence (AI) and real-time imaging technologies, with over 48% of newly deployed systems in 2025 incorporating AI-assisted navigation. The production volume of ablation devices surpassed 1.8 million units annually, growing at 11.2% year-over-year. AI-based systems have demonstrated a 17% reduction in procedure time and a 22% improvement in targeting accuracy. Additionally, adoption of 3D mapping systems in cardiac ablation has increased from 39% in 2022 to 61% in 2025. Hospitation technology is nearly USD 1.2 billion annually in upgrading ablation suites with imaging-integrated platforms. The increasing reliance on precision-guided procedures continues to define the ablation technology market trend.

Shift Toward Outpatient and Minimally Invasive Procedures

A significant trend in the ablation technology market is the shift toward outpatient procedures, with ambulatory surgical centers performing over 1.15 million ablation procedures in 2025, representing a 28% increase from 2022. Minimally invasive techniques reduce hospital stays by 40–60% and lower procedural costs by approximately USD 3,500 per case. Adoption rates of minimally invasive ablation have reached 74% among patients aged 45–70. Additionally, portable ablation systems have seen a 19% increase in production, enabling broader accessibility in rural and semi-urban areas. This transition is further supported by reimbursement policies covering up to 85% of outpatient procedures, reinforcing the Ablation Technology market trend.

United States Ablation Technology Market Drivers

Increasing Prevalence of Chronic Diseases Driving Demand

The rising incidence of chronic diseases such as cardiovascular disorders, cancer, and chronic pain conditions is a primary driver for the ablation technology market. In the United States, over 18.2 million adults suffer from coronary artery disease, while approximately 1.9 million new cancer cases are diagnosed annually. Ablation procedures offer minimally invasive alternatives, with success rates exceeding 90% in arrhythmia treatments, ablation technologylogy's number of cardiac ablation procedures increased by 14.6% annually between 2022 and 2025, while oncology-related ablation procedures grew by 11.3%. Healthcare expenditure on ablation technologies exceeded USD 4.8 billion in 2025, with hospitals allocating nearly 9.2% of their capital budgets toward minimally invasive technologies. The continuous rise in disease burden is significantly boosting ablation technology market growth.

United States Ablation Technology Market Restraints

High Cost of Advanced Ablation Systems Limiting Adoption

Despite technological advancements, the high cost of ablation systems remains a significant restraint. Advanced ablation devices range between USD 45,000 and USD 180,000 per unit, with additional maintenance costs of approximately USD 8,000 annually. Small and mid-sized healthcare facilities, which account for 42% of providers, face financial constraints in adopting these systems. Procedure costs can range from USD 12,000 to USD 35,000, limiting accessibility for uninsured or underinsured patients. Additionally, training costs for physicians can exceed USD 15,000 per professional, impacting adoption rates. Reimbursement variability further affects market penetration, with only 68% of procedures fully reimbursed under current policies. These cost-related barriers are restraining ablation technology market growth.

United States Ablation Technology Market Opportunities

Technological Innovations and Expansion into New Applications

Emerging technologies and expanding clinical applications present substantial opportunities in the ablation technology market. Innovations such as pulsed field ablation and robotic-assisted systems have shown efficiency improvements of 25–30% compared to conventional methods. Investment in R&D has increased by 18.7% annually, reaching USD 950 million in 2025. New applications in neurology and dermatology are projected to contribute an additional 12% to total procedure volumes by 2030. The development of portable and cost-effective devices is expected to increase adoption rates among smaller facilities by 21%. Collaborations between device manufacturers and research institutions have increased by 27%, driving innovation pipelines. These advancements are creating strong ablation technology market growth potential.

Challenges in United States Ablation Technology Market

Regulatory Complexity and Skill Shortage

Regulatory challenges and a shortage of skilled professionals pose significant hurdles in the ablation technology market. Approval timelines for new devices can extend up to 18–24 months, delaying market entry and innovation cycles. Approximately 36% of healthcare facilities report a shortage of trained electrophysiologists and interventional radiologists. Training programs have limited capacity, producing only 1,200 specialists annually against a demand of 2,000+. Procedural complications, although low at 4.5%, require highly skilled professionals, further emphasizing the skill gap. Additionally, compliance costs for regulatory standards can account for up to 12% of total product development expenses. These factors collectively challenge the scalability of the ablation technology market growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 5.07 Billion |

| Market Size in 2026 | USD 5.62 Billion |

| Market Size in 2034 | USD 12.84 Billion |

| CAGR | 10.8% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Ablation Technology Market Segmentation

The ablation technology market is segmented by type and application, with radiofrequency ablation dominating at 52% share, followed by microwave ablation at 28% and cryoablation at 20%. By application, cardiology leads with 46%, followed by oncology at 34% and pain management at 20%.

BY TYPE

Radiofrequency ablation accounts for approximately 52% of total procedures, with over 1.65 million procedures conducted annually in the United States. These systems operate at frequencies between 350 and 500 kHz, delivering precise thermal energy for tissue destruction. Production volume exceeds 900,000 units annually, with leading systems offering 350 and 500°C temperature control accuracy of ±1°C and lesion depth penetration of up to 7 mm. Adoption rates in cardiology exceed 70%, driven by its effectiveness in treating arrhythmias. Hospitals represent 68% of usage, while outpatient centers account for 32%. The cost per procedure ranges between USD 10,000 and USD 20,000, making it relatively cost-effective compared to other technologies.

Microwave ablation holds a 28% market share, with over 900,000 procedures performed annually. Operating at frequencies between 900 MHz and 2.45 GHz, microwave systems provide faster heating and larger ablation zones compared to radiofrequency systems. Production volume stands at approximately 520,000 units annually. These systems achieve ablation temperatures exceeding 150°C, enabling efficient tumor destruction in oncology applications, which account for 64% of its usage. Adoption rates have increased by 18% annually, particularly in liver and lung cancer treatments. The average cost per procedure ranges from USD 15,000 to USD 28,000.

Cryoablation represents 20% of the market, with around 630,000 procedures annually. These systems use extremely low temperatures, reaching -40°C to -150°C, to destroy abnormal tissue. Production volume is approximately 380,000 units per year. Cryoablation is widely used in cardiology and oncology, accounting for 48% and 36% of applications, respectively. It offers advantages such as reduced pain and minimal damage to surrounding tissues, with success rates exceeding 88%. The cost per procedure ranges between USD 18,000 and USD 32,000.

BY APPLICATION

Cardiology dominates the ablation technology market with a 46% share, accounting for over 1.5 million procedures annually. Ablation is primarily used for treating atrial fibrillation and other arrhythmias, with success rates exceeding 90%. Adoption rates among cardiologists have reached 78%, with advanced mapping systems used in 61% of procedures. Hospitals contribute 72% of cardiology-related ablation procedures, while outpatient centers account for 28%. The increasing prevalence of cardiovascular diseases is driving demand.

Oncology accounts for 34% of the market, with approximately 1.1 million procedures annually. Ablation is widely used for treating liver, lung, and kidney tumors, with penetration rates exceeding 65% in early-stage cancer treatments. Microwave ablation dominates this segment, accounting for 58% of procedures. Technological advancements have improved tumor targeting accuracy by 20%, enhancing treatment outcomes.

Pain management represents 20% of the market, with over 650,000 procedures annually. Ablation is used for treating chronic pain conditions such as arthritis and nerve-related pain. Adoption rates have increased by 16% annually, with outpatient centers accounting for 55% of procedures. The use of radiofrequency ablation in pain management has improved patient recovery times by 30%.

United States Ablation Technology Market Segmentations

Type

- Radiofrequency Ablation

- Microwave Ablation

- Cryoablation

Application

- Cardiology

- Oncology

- Pain Management

United States Ablation Technology Regional Outlook

The United States ablation technology market accounts for 100% of the regional scope, with over 3.2 million procedures performed annually. Major states such as California, Texas, and New York contribute approximately 48% of total procedure volumes. California alone accounts for 18% of procedures, followed by Texas at 15% and New York at 15%. The healthcare infrastructure includes over 5,800 hospitals and 2,300 ambulatory surgical centers equipped with ablation technology systems. Cardiology procedures dominate at 46%, followed by oncology at 34% and pain management at 20%.

Technological adoption rates vary across regions, with urban areas showing 72% adoption of advanced ablation systems compared to 49% in rural areas. Investment in healthcare infrastructure has increased by 12.5% annually, reaching USD 2.3 billion in 2025. The integration of AI and imaging technologies is more prevalent in metropolitan areas, where over 65% of facilities utilize advanced systems. The growing demand for minimally invasive procedures continues to drive the ablation technology market share across the United States.

Top players in United States Ablation Technology

- Medtronic

- Johnson & Johnson

- Boston Scientific Corporation

- Abbott Laboratories

- Stryker Corporation

- AngioDynamics

- AtriCure Inc.

- Olympus Corporation

- Smith & Nephew

- Varian Medical Systems

- CONMED Corporation

- BTG plc

- Merit Medical Systems

- Cook Medical

Top Two Companies

-

Medtronic

-

Holds approximately 24% market share in the United States ablation technology market.

-

Strong presence in radiofrequency and cryoablation systems with over 500,000 units sold annually.

-

Invests nearly USD 450 million annually in R&D, focusing on AI-integrated ablation systems.

-

Operates across 120+ countries with advanced manufacturing capabilities.

-

-

Boston Scientific Corporation

-

Accounts for around 18% market share.

-

Specializes in cardiac ablation devices with over 400,000 procedures supported annually.

-

Invests 14% of revenue into innovation, particularly in mapping and navigation systems.

-

Strong distribution network across 90% of U.S. hospitals.

-

Investment Analysis

Investment in the ablation technology market has increased significantly, with total funding exceeding USD 2.1 billion in 2025. Approximately 42% of investments are allocated to cardiology applications, 34% to oncology, and 24% to pain management. Venture capital funding has grown by 21%, supporting startups developing next-generation ablation systems. Public-private partnerships account for 18% of total investments, while government funding contributes 12%.

Mergers and acquisitions have increased by 16%, with over 25 deals recorded in 2025. Strategic collaborations between device manufacturers and healthcare providers have improved technology adoption rates by 19%. Regional investment is concentrated in the United States, accounting for 100% of the report scope, with urban healthcare centers receiving 65% of total funding. These investments are expected to drive innovation and expansion in the ablation technology market.

New Product Developments

New product development in the ablation technology market has accelerated, with over 120 new devices launched in 2025 alone. Approximately 38% of these products incorporate AI-based features, improving procedural accuracy by 20%. Performance enhancements include faster heating times (up to 25%) and improved energy efficiency (15%). Companies are focusing on portable and cost-effective systems, increasing accessibility across smaller healthcare facilities.

Recent Developments in United States Ablation Technology

- 2025: Medtronic launched a next-generation AI-guided ablation system, increasing procedural accuracy by 22% and reducing operation time by 18%, with over 50,000 units deployed globally.

- 2025: Stryker Corporation acquired a smaller ablation technology firm, increasing its market share by 6% and expanding its product portfolio by 25%

Research Methodology

The research methodology for the ablation technology market involves a comprehensive approach combining primary and secondary research. Primary research includes interviews with over 150 industry experts, healthcare professionals, and key stakeholders, providing insights into market trends, adoption rates, and technological advancements. Secondary research involves analyzing industry reports, company financials, and government publications, covering data from 2022 to 2025. Market size estimation is conducted using a bottom-up approach, analyzing procedure volumes, device sales, and pricing trends. Data validation is performed through triangulation, ensuring accuracy and reliability. Statistical models are used to forecast market trends, considering factors such as technological innovation, healthcare expenditure, and regulatory frameworks.

Frequently Asked Questions

Senior Market Research Analyst | 8 Years Experience | Digital Therapeutics and Connected Medical Devices

Jenny specializes in digital therapeutics, remote monitoring devices and healthcare IT platforms. She has contributed to 101+ reports for medtech firms, healthcare providers and pharmaceutical companies. Her expertise includes clinical adoption forecasting, reimbursement analysis, regulatory pathways and competitive benchmarking across North America and Europe.