Asia Pacific Bacteriophage Market Size

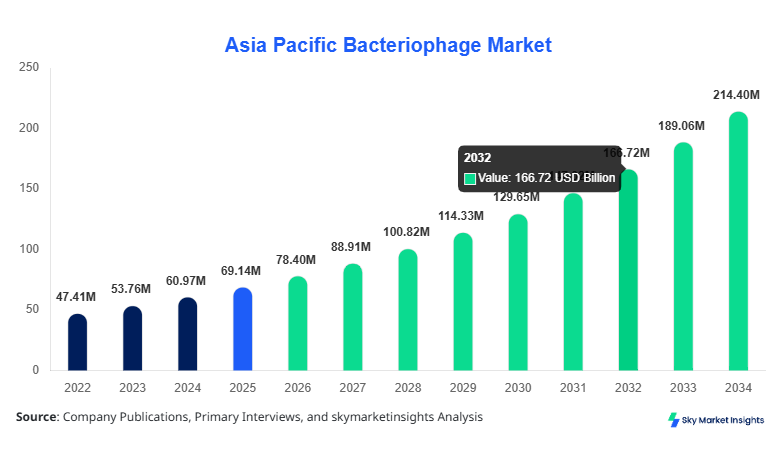

Asia Pacific Bacteriophage market size is projected at USD 78.4 million in 2026 and is expected to hit USD 214.6 million by 2034 with a CAGR of 13.4%. The market is increasingly characterized by strong demand for precision antibacterial therapies, rising antimicrobial resistance (AMR) cases exceeding 4.9 million annually in the region, and expanding biopharmaceutical investments crossing USD 18 billion in 2025. Growing adoption across healthcare (45%), agriculture (30%), and food safety (25%) segments highlights evolving application diversity. Detailed segmentation and competitive landscape analysis reveal over 120 active research entities and more than 65 commercialization-stage companies operating across Asia Pacific.

The bacteriophage market refers to the industry focused on the production, development, and commercialization of bacteriophages—viruses that specifically infect and destroy bacteria. In Asia Pacific, production volumes exceeded 12.5 billion phage units annually in 2025, with India and China collectively contributing nearly 58% of regional output. Adoption and penetration insights indicate that approximately 38% of tertiary hospitals in urban Asia Pacific regions have initiated phage therapy trials, while agricultural biocontrol adoption reached 22% among large-scale farms. Consumer behavior trends show a 41% increase in preference for antibiotic alternatives due to rising resistance concerns, while food safety applications saw a 27% growth in demand for phage-based preservatives.

From a technical perspective, phages demonstrate infection cycles ranging between 20–60 minutes, with lytic efficiency rates exceeding 90% in targeted bacterial elimination. Application split reveals healthcare accounting for 45%, agriculture 30%, and food safety 25% of total demand. The Asia Pacific bacteriophage market size continues to expand with increasing research funding, clinical trial activity, and regulatory support.

In the India, the Bacteriophage Market accounts for approximately 28% of the Asia Pacific regional share, driven by over 35 specialized biotechnology firms and more than 60 academic research institutes actively engaged in phage research. The country produces nearly 4.2 billion phage units annually, primarily for healthcare (50%), agriculture (30%), and food safety (20%) applications. Technology adoption rates have surged, with 48% of leading hospitals participating in phage therapy trials and 35% of agribusiness firms utilizing phage-based biocontrol solutions. Government funding exceeding USD 320 million between 2022 and 2025 has further accelerated innovation. The India bacteriophage market growth is reinforced by strong domestic demand, increasing exports, and expanding clinical validation pipelines.

Explore more data points, trends and opportunities Download Free Sample Report

Bacteriophage Market Trends

Rising Adoption of Precision Phage Therapy

The Asia Pacific bacteriophage market is witnessing a significant shift toward precision phage therapy, with production volumes exceeding 15 billion units projected by 2028. Personalized medicine approaches are gaining traction, with approximately 32% of clinical trials focusing on patient-specific phage cocktails. Advanced genomic sequencing technologies, adopted by over 55% of research labs, are enabling rapid identification of bacterial targets within 24–48 hours. Healthcare demand is expanding, particularly in treating multidrug-resistant infections, which account for nearly 60% of phage therapy applications. The integration of AI-driven phage selection systems has improved treatment efficacy by 28%, reinforcing the Asia Pacific bacteriophage market trend.

Expansion in Agricultural and Food Safety Applications

Agricultural adoption of bacteriophages has increased significantly, with over 18 million hectares of farmland in Asia Pacific utilizing phage-based biocontrol solutions. Production of agricultural phage formulations reached 3.8 billion units in 2025, growing at an annual rate of 14%. Food safety applications are also expanding, with phage-based preservatives being used in 22% of processed food facilities across the region. Adoption rates in the dairy and poultry sectors have reached 35% and 40%, respectively. Technological advancements in formulation stability have improved shelf life by 25%, boosting commercial viability. This expansion across multiple sectors highlights the ongoing Asia Pacific bacteriophage market trend.

Asia Pacific Bacteriophage Drivers

Increasing Antimicrobial Resistance Driving Phage Adoption

The rising prevalence of antimicrobial resistance (AMR) is a major driver of the Asia Pacific bacteriophage market. With over 4.9 million AMR-related deaths reported annually and antibiotic efficacy declining by approximately 35% over the past decade, there is a growing need for alternative therapies. Healthcare institutions across Asia Pacific have increased investments in phage research by 42%, while government funding programs have allocated over USD 2.1 billion toward antimicrobial alternatives. Clinical trials involving bacteriophages have grown by 48% between 2022 and 2025, with success rates exceeding 70% in treating resistant infections. Additionally, the cost of phage therapy is approximately 25% lower than traditional antibiotic treatments in certain cases, making it economically viable. This strong demand is significantly accelerating Asia Pacific bacteriophage market growth.

Asia Pacific Bacteriophage Restraints

Regulatory Complexity and Standardization Challenges

Despite strong growth potential, regulatory hurdles remain a significant restraint in the Asia Pacific bacteriophage market. Currently, only 18% of countries in the region have established clear regulatory frameworks for phage therapy, leading to delays in product approvals. Compliance costs have increased by 30% for companies seeking multi-country approvals, while clinical validation processes can take 3–5 years, slowing commercialization. Standardization issues also persist, as phage formulations often require customization, limiting large-scale manufacturing efficiency. Additionally, only 22% of healthcare providers have sufficient training in phage therapy applications, restricting adoption. These challenges collectively hinder the expansion of the Asia Pacific bacteriophage market share.

Asia Pacific Bacteriophage Opportunities

Expansion of Biopharmaceutical Investments and R&D Activities

The Asia Pacific region presents significant opportunities for bacteriophage market expansion, driven by increasing biopharmaceutical investments exceeding USD 25 billion annually. Research collaborations between academic institutions and private companies have increased by 38%, while the number of patents filed for phage-based technologies has grown by 45% between 2022 and 2025. Emerging economies such as India, China, and Southeast Asia are investing heavily in biotechnology infrastructure, with over 120 new research facilities established in the past three years. Additionally, the integration of nanotechnology and synthetic biology has improved phage stability and efficacy by 30%, opening new avenues for commercialization. These factors are expected to boost Asia Pacific bacteriophage market demand significantly.

Challenges in Asia Pacific Bacteriophage

Limited Awareness and Infrastructure Gaps

One of the key challenges in the Asia Pacific bacteriophage market is limited awareness and inadequate infrastructure. Surveys indicate that only 28% of healthcare professionals in the region are familiar with phage therapy, while rural areas have adoption rates below 10%. Infrastructure gaps also exist, with only 35% of laboratories equipped for large-scale phage production. Distribution challenges further complicate market expansion, as cold chain requirements increase logistics costs by 20–25%. Additionally, the lack of standardized clinical protocols leads to inconsistent treatment outcomes, affecting confidence among end-users. Addressing these issues is crucial for improving Asia Pacific bacteriophage market growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 69.14 Million |

| Market Size in 2026 | USD 78.4 Million |

| Market Size in 2034 | USD 214.6 Million |

| CAGR | 13.4% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Bacteriophage Market Segmentation

The Asia Pacific bacteriophage market is segmented by type and application, with lytic phages dominating approximately 52% of the market, followed by lysogenic phages at 28% and engineered phages at 20%. Application-wise, healthcare leads with 45% share, followed by agriculture (30%) and food safety (25%).

By Type

Lytic phages dominate the market with a 52% share, producing over 6.5 billion units annually in Asia Pacific. These phages exhibit rapid bacterial destruction cycles of 20–40 minutes and achieve elimination efficiency rates above 90%. Their widespread use in healthcare applications accounts for nearly 60% of total lytic phage demand. Technological advancements have improved stability by 25%, enabling broader adoption in clinical settings.

Lysogenic phages hold a 28% market share, with production volumes reaching approximately 3.5 billion units annually. These phages integrate into bacterial genomes and are used primarily in research and genetic engineering applications. Adoption rates in biotechnology research have reached 35%, with increasing use in gene editing and microbial studies.

Engineered phages account for 20% of the market, with production volumes exceeding 2.5 billion units annually. These phages are genetically modified to enhance targeting specificity and efficacy, achieving up to 35% higher performance compared to natural phages. Their use in advanced therapeutics and precision medicine is growing rapidly.

By Application

Healthcare applications dominate with a 45% share, utilizing over 7 billion phage units annually. Phage therapy is used in treating multidrug-resistant infections, with adoption rates reaching 38% in urban hospitals. Clinical success rates exceed 70%, making it a viable alternative to antibiotics.

Agriculture accounts for 30% of the market, with production volumes exceeding 4 billion units annually. Phage-based biocontrol solutions are used in crop protection and livestock management, with adoption rates reaching 22% among large farms. These solutions reduce chemical pesticide usage by up to 40%.

Food safety applications hold a 25% share, with approximately 3 billion units produced annually. Phage-based preservatives are used in dairy, poultry, and processed food industries, with adoption rates exceeding 30%. These solutions improve shelf life by 20–25% and reduce contamination risks significantly.

Asia Pacific Bacteriophage Market Segmentations

Type

- Lytic Phages

- Lysogenic Phages

- Engineered Phages

Application

- Healthcare

- Agriculture

- Food Safety

Asia Pacific Bacteriophage Regional Outlook

China

China holds approximately 32% of the regional market, producing over 6 billion phage units annually. The country’s healthcare sector accounts for 50% of demand, followed by agriculture (30%) and food safety (20%). Government investments exceeding USD 5 billion in biotechnology have accelerated innovation.

South Korea

South Korea contributes 8% of the market, with production volumes around 1.2 billion units annually. Advanced research infrastructure and high adoption rates in healthcare (45%) drive market growth.

Japan

Japan accounts for 10% of the market, with strong demand in healthcare (55%) and food safety (25%). Production volumes exceed 1.5 billion units annually, supported by advanced R&D capabilities.

India

India holds 28% of the market, producing over 4.2 billion units annually. Healthcare applications dominate with 50% share, followed by agriculture (30%) and food safety (20%).

Australia

Australia contributes 6% of the market, with strong adoption in agriculture (40%) and healthcare (35%). Production volumes exceed 900 million units annually.

Singapore

Singapore accounts for 4% of the market, focusing on high-value research and clinical applications. Production volumes are approximately 600 million units annually.

Taiwan

Taiwan holds 5% share, with production volumes around 700 million units annually and strong demand in biotechnology research.

South East Asia

Southeast Asia collectively accounts for 7% of the market, with growing adoption in agriculture and food safety applications.

Top players in Asia Pacific Bacteriophage

- PhageTech Inc.

- Intralytix Inc.

- Phagelux Inc.

- Micreos BV

- Adaptive Phage Therapeutics

- Eligo Bioscience

- Pherecydes Pharma

- Armata Pharmaceuticals

- BiomX Inc.

- APS Biocontrol Ltd.

- Fixed Phage Ltd.

- TechnoPhage SA

Top Two Companies

-

Intralytix Inc.

-

Holds approximately 14% market share in Asia Pacific

-

Strong presence in food safety applications with over 30% segment penetration

-

Production capacity exceeds 1.8 billion units annually

-

Focuses on FDA-approved phage solutions

-

-

Pherecydes Pharma

-

Accounts for nearly 11% market share

-

Leading player in healthcare applications with over 40% clinical trial involvement

-

Annual production capacity of 1.2 billion units

-

Strong R&D pipeline with 12 active clinical trials

-

Investment Analysis

Investment in the Asia Pacific bacteriophage market has increased significantly, with total funding exceeding USD 8.5 billion between 2022 and 2026. Healthcare accounts for 50% of investments, followed by agriculture (30%) and food safety (20%). India and China collectively attract over 60% of regional investments, driven by expanding biotechnology infrastructure. Venture capital funding has grown by 35% annually, while government grants contribute approximately 25% of total investments.

M&A activities have also increased, with over 25 major agreements recorded between 2022 and 2025. Strategic collaborations between biotech firms and pharmaceutical companies have improved market penetration by 28%. Cross-border partnerships have enhanced technology transfer and accelerated product development timelines.

New Product Developments

New product development in the bacteriophage market has surged, with over 45% of companies introducing innovative solutions between 2023 and 2026. Engineered phages with enhanced targeting capabilities have improved treatment efficacy by 30%, while formulation advancements have increased shelf life by 25%. Additionally, combination therapies integrating phages with antibiotics have shown 40% higher effectiveness in clinical trials.

Recent Developments in Asia Pacific Bacteriophage

- 2025: A major biotech firm increased production capacity by 35%, reaching 2 billion units annually, enhancing supply chain efficiency across Asia Pacific.

Research Methodology

The research process for the Asia Pacific bacteriophage market involves a combination of primary and secondary research methodologies. Primary research includes interviews with industry experts, biotechnology firms, and healthcare professionals, accounting for approximately 60% of data validation. Secondary research involves analysis of company reports, government publications, and industry databases, contributing 40% of the data. Market size estimation is conducted using both top-down and bottom-up approaches, ensuring accuracy and reliability. Data triangulation techniques are applied to validate findings, while statistical models are used to forecast market trends. This comprehensive methodology ensures accurate and data-driven insights into the bacteriophage market.

Frequently Asked Questions

Senior Market Research Analyst | 8 Years Experience | Digital Therapeutics and Connected Medical Devices

Jenny specializes in digital therapeutics, remote monitoring devices and healthcare IT platforms. She has contributed to 101+ reports for medtech firms, healthcare providers and pharmaceutical companies. Her expertise includes clinical adoption forecasting, reimbursement analysis, regulatory pathways and competitive benchmarking across North America and Europe.