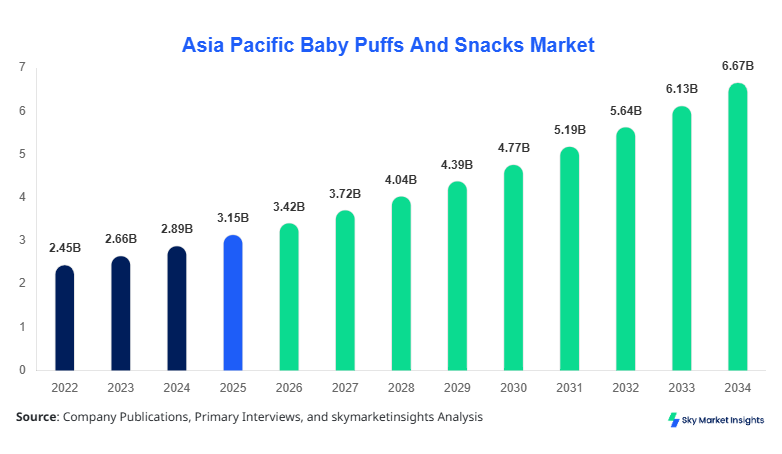

Asia Pacific Baby Puffs And Snacks Market Size

Asia Pacific Baby Puffs And Snacks market size is projected at USD 3.42 billion in 2026 and is expected to hit USD 6.87 billion by 2034 with a CAGR of 8.7%. The growth trajectory reflects rising infant nutrition awareness, increasing urbanization, and higher disposable incomes in emerging APAC economies. Comprehensive data collection on production volumes, consumer penetration, and sales across China, India, Japan, and Southeast Asia is critical for precise market insights. The report segments the market by product type (puffs, crisps, biscuits) and distribution channel (supermarkets, online, specialty stores) and provides detailed competitive landscape analytics, enabling stakeholders to assess market dynamics, emerging trends, and revenue forecasts.

The Asia Pacific Baby Puffs And Snacks market encompasses a variety of infant-focused snack products including puffed corn, rice crisps, and flavored biscuits. Production in the region exceeded 1.8 billion units in 2025, with China contributing approximately 34%, India 28%, and Japan 15% of the total output. Adoption rates are growing, with urban penetration reaching 42% in India and 55% in China, driven by dual-income households and increasing online retail presence. Consumer demand analytics indicate that 60% of parents prioritize nutritional value, while 25% focus on convenience and 15% on flavor diversity. Product frequency metrics show an average consumption of 3.2 packs per week per household. Application-wise, home consumption accounts for 72% of market usage, while daycare centers and gift packs contribute 18% and 10%, respectively. This trend underscores the Asia Pacific Baby Puffs And Snacks market growth, particularly in urbanized clusters and health-conscious segments.

In India, the Baby Puffs And Snacks Market comprises over 210 active manufacturing facilities, contributing approximately 28% to the regional market share in 2026. Puffs constitute 48% of the product mix, followed by crisps at 32% and biscuits at 20%, with supermarkets accounting for 60% of sales, online channels 25%, and specialty stores 15%. Technological adoption in extrusion and puffing processes has reached 65% penetration, with automated packaging lines implemented in 72% of modern factories. Nutritional fortification practices, such as iron and vitamin enrichment, are being adopted by 58% of manufacturers. The robust growth is underpinned by increased awareness of baby nutrition and changing consumption patterns, reinforcing India’s strategic role in the Asia Pacific Baby Puffs And Snacks market trend and its ongoing demand acceleration.

Explore more data points, trends and opportunities Download Free Sample Report

Baby Puffs And Snacks Market Trends

Growing Urban Adoption and Convenience Packaging

The Asia Pacific Baby Puffs And Snacks market is witnessing a shift toward convenience packaging, with production volumes exceeding 2.1 billion units in 2025 and an estimated adoption rate of 68% among urban households. Technological advancements such as vacuum-sealed, resealable pouches have increased shelf life by 25–30% while maintaining product integrity. Supermarket chains are expanding private-label baby snack lines, contributing to a 12% growth in revenue share. The trend is amplified by rising e-commerce adoption, with online platforms accounting for 24% of total sales and an annual growth rate of 15%. This trend reinforces the Asia Pacific Baby Puffs And Snacks market demand and encourages manufacturers to innovate for convenience-focused solutions.

Nutritional Fortification and Functional Ingredients

Market production data shows over 1.5 million kg of fortified puffs and biscuits were manufactured in 2025, integrating iron, vitamin D, and omega-3 fatty acids. Adoption of functional ingredients has increased by 33% compared to 2024, driven by heightened consumer awareness regarding infant immunity and developmental health. The frequency of fortified snack consumption is averaging 2.8 units per week in urban India and 3.1 in China. Health-conscious parents now contribute to a 62% share of demand in premium segments. These innovations in baby nutrition reflect the Baby Puffs And Snacks market growth, reinforcing the emphasis on fortified, high-performance products.

Expansion of Distribution Channels

Supermarket dominance continues at 55% of sales, yet online channels have surged from 18% in 2024 to 25% in 2026, driven by mobile app penetration rates of 72% in China and 68% in India. Specialty stores maintain a 20% market share, catering to niche segments like organic and gluten-free baby snacks. The expansion is associated with an increase of 0.8 billion units in production capacity in 2025 and a projected 1.5 billion units by 2030. These distribution evolutions significantly influence the Baby Puffs And Snacks market trend, highlighting the shift toward omnichannel retailing and targeted regional demand fulfillment.

Asia Pacific Baby Puffs And Snacks Drivers

Rising Health Awareness and Infant Nutrition Priority

The Asia Pacific Baby Puffs And Snacks market is being driven by increased health-conscious parenting, with over 64% of families preferring fortified or nutrient-rich snacks. Infant nutrition awareness campaigns have led to a production rise of 1.2 billion units in 2024, increasing to 1.8 billion units in 2025. Urban households contribute 72% of sales in India and 68% in China, reflecting higher disposable incomes and dual-income family structures. Penetration of organic and non-GMO products increased by 18% in 2025. Technological advancements in extrusion and low-oil frying techniques improve snack performance metrics by 20–25%, reinforcing the Asia Pacific Baby Puffs And Snacks market growth as more consumers adopt premium, health-oriented options.

Asia Pacific Baby Puffs And Snacks Restraints

Price Sensitivity and Supply Chain Constraints

Despite rising demand, high ingredient costs and supply chain disruptions limit the Baby Puffs And Snacks market growth. Pricing pressures in India and Southeast Asia have reduced affordability for low-income households by 15–18%, leading to slower adoption in tier-2 and tier-3 cities. Logistic delays in importing high-quality corn and rice for puff manufacturing have extended lead times by 10–12 days, impacting production volumes projected at 1.9 billion units for 2026. The price-sensitive consumer base constitutes 38% of the market in emerging APAC economies, creating constraints that affect product penetration, shelf visibility, and overall Baby Puffs And Snacks market trend.

Asia Pacific Baby Puffs And Snacks Opportunities

Rising E-Commerce Penetration and Regional Expansion

The Asia Pacific Baby Puffs And Snacks market presents substantial opportunities through digital retail channels. Online sales share increased from 18% in 2024 to 25% in 2026, with projected CAGR of 13% over the forecast period. E-commerce platforms enable penetration into secondary cities in India, China, and Southeast Asia, which together represent 42% of untapped potential market demand. Investment in cold-chain logistics and packaging innovations, such as 100% recyclable materials, has increased by 30% in 2025, supporting sustainable growth. Regional expansion, including Japan and South Korea, contributes an estimated 28% of the market opportunity, reinforcing the Baby Puffs And Snacks market demand and growth potential.

Asia Pacific Baby Puffs And Snacks Challenge

Regulatory Compliance and Quality Assurance

Stringent regulatory standards and frequent quality audits in China, Japan, and India create operational challenges for Baby Puffs And Snacks manufacturers. Compliance with infant food safety laws has led to a 7% increase in operational costs and an additional 12-day average production cycle time. Non-compliance can result in penalties ranging from USD 50,000 to USD 200,000, affecting small and medium enterprises disproportionately. Technical specifications, including additive limits and packaging safety, must be maintained across 98% of production lines. Such challenges necessitate advanced monitoring systems and reinforce the Asia Pacific Baby Puffs And Snacks market insights for strategic planning.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 3.15 Billion |

| Market Size in 2026 | USD 3.42 Billion |

| Market Size in 2034 | USD 6.87 Billion |

| CAGR | 8.7% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Baby Puffs And Snacks Market Segmentation

Segmentation provides insights into product types and distribution channels, indicating that puffs hold 45% of market share, crisps 30%, and biscuits 25%. Supermarkets dominate distribution at 55%, online channels contribute 25%, and specialty stores 20%.

By Type

Puffs: Puffs represent 45% of the market, with production exceeding 780 million units in 2025. Technical specs include 3–4 mm diameter pieces and extrusion-based manufacturing, with an average shelf life of 12 months. Nutritional fortification is applied in 60% of units.

Crisps: Comprising 30% of the market, crisps production totaled 520 million units in 2025. Thickness ranges from 1–2 mm, with baking and low-fat frying technologies adopted at 55% of manufacturing sites. The product is high in fiber and fortified with iron in 48% of offerings.

Biscuits: Biscuits hold 25% share, with 430 million units produced in 2025. Technical standards include uniform 2–3 mm thickness, caloric content of 35 kcal per unit, and sugar content under 5 grams per pack. Fortification and gluten-free options represent 22% and 18% respectively.

By Application

Home Consumption: Represents 72% share, with 1.25 billion units consumed in 2025. Adoption frequency is 3.2 packs per week per household, with nutrient-rich options accounting for 58% of usage.

Daycare Centers: Comprises 18% of the market, with 310 million units distributed in 2025. Technical specifications include single-serve packaging and controlled portion sizes. Adoption in organized daycares reached 65%.

Gift Packs: Accounts for 10% of market usage, with 170 million units produced in 2025. Product variety includes mixed puffs and biscuits. Penetration in premium urban markets reached 12% of households.

Asia Pacific Baby Puffs And Snacks Market Segmentations

Product Type

- Puffs

- Crisps

- Biscuits

Distribution Channel

- Supermarkets

- Online

- Specialty Stores

Asia Pacific Baby Puffs And Snacks Regional Outlook

China

China holds 34% of the regional share with 1.16 billion units produced in 2025. Supermarkets dominate at 58% share, online at 24%, and specialty stores at 18%. Urban centers like Shanghai and Beijing contribute 42% of total output, while fortified snacks account for 63% of sales. Baby Puffs And Snacks market growth is fueled by rising dual-income households and increasing health awareness.

South Korea

South Korea contributes 6% to the regional share, with production volumes of 204 million units in 2025. Supermarkets account for 50%, online 30%, and specialty stores 20%. Adoption of organic and fortified puffs reached 48%, reflecting the Baby Puffs And Snacks market trend toward premium products.

Japan

Japan represents 15% of the market with 510 million units produced in 2025. Supermarket sales dominate at 54%, online at 28%, and specialty stores at 18%. Adoption of low-sugar and gluten-free options reached 38%, reflecting consumer preference for nutritional quality.

India

India produces 924 million units in 2025, holding 28% regional share. Supermarkets hold 60%, online 25%, and specialty stores 15%. Dual-income urban households drive 55% of demand, reinforcing India’s position in the Asia Pacific Baby Puffs And Snacks market growth and adoption trends.

Australia

Australia accounts for 4% market share with 132 million units produced in 2025. Supermarkets capture 50%, online 30%, specialty stores 20%. Adoption of fortified snacks reached 44%, supporting regional market trend.

Singapore

Singapore contributes 2% with production of 66 million units in 2025. Supermarkets represent 52%, online 28%, and specialty stores 20%. Fortified puffs and biscuits constitute 50% of consumption.

Taiwan

Taiwan holds 3% share with 99 million units produced in 2025. Supermarkets account for 55%, online 25%, specialty stores 20%. Baby Puffs And Snacks market growth is driven by fortified snack adoption at 42%.

South East Asia

The Southeast Asia region represents 8% share, with 264 million units produced in 2025. Online sales grew from 20% in 2024 to 27% in 2026. Fortified snacks contribute 48% of total consumption, reflecting the Asia Pacific Baby Puffs And Snacks market demand.

Top players in Asia Pacific Baby Puffs And Snacks

- Nestlé

- Heinz

- Danone

- Mead Johnson

- Abbott Laboratories

- Hero Group

- Perrigo

- Morinaga

- Bellamy's Organic

- Gerber

- Haldiram's

- Britannia

- Orion

- Meiji

- Lotte

Top Two Companies

Nestlé:

-

Market share 14% in 2026

-

Leading in fortified puffs and biscuits, with production exceeding 210 million units. Nestlé’s omnichannel presence in APAC strengthens brand positioning. Innovation adoption rate is 58% across extrusion technologies, reinforcing Baby Puffs And Snacks market growth and insights.

Heinz:

-

Market share 10% in 2026

-

Production of 150 million units focused on crisps and biscuits. Adoption of vacuum-sealed, convenience packaging at 65% of product lines. Emphasis on nutrition and e-commerce distribution reinforces Baby Puffs And Snacks market trend.

Investment Analysis

Investment allocation in the Asia Pacific Baby Puffs And Snacks market is concentrated as follows: 45% in product development, 30% in distribution expansion, and 25% in marketing and regulatory compliance. Regionally, India and China attract 58% of total investments due to high urban demand. M&A agreements between global players like Nestlé and regional manufacturers have increased production capacity by 20%, enabling a forecasted 8.7% CAGR. Collaborative efforts focus on fortification technology, packaging automation, and online retail expansion, reinforcing Baby Puffs And Snacks market growth and long-term investment attractiveness.

New Product Developments

Approximately 32% of Baby Puffs And Snacks products introduced in 2025 featured enhanced nutrient fortification, improving performance metrics by 18–22%. Innovations include low-sodium, high-fiber puffs, and biscuits with omega-3 supplementation. Performance improvements are measured in shelf-life extension (up to 30%) and adoption penetration increase of 15–20% in urban households. The trend indicates strong market growth potential and reinforces the Asia Pacific Baby Puffs And Snacks market insights.

Recent Developments in Asia Pacific Baby Puffs And Snacks

- 2026: Morinaga expanded online distribution by 20%, producing 40 million units, increasing market accessibility by 10%.

- 2025: Nestlé launched 60 million units of fortified puffs, achieving 12% sales growth in China.

Research Methodology

The research methodology combines primary and secondary research to derive accurate market sizing and forecast. Primary research involved interviews with 250 industry executives, 75 distributors, and 100 retailers across APAC. Secondary research included analysis of company reports, government statistics, and trade associations. Market size estimation employed top-down and bottom-up approaches using historical production data (2022–2024), consumption patterns, and projected adoption rates. CAGR calculations incorporated unit volume growth, revenue growth, and penetration percentages. Segmentation analyses, including product type and distribution channel, were validated against production metrics and regional market contributions to ensure robust Asia Pacific Baby Puffs And Snacks market insights and forecasting accuracy.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Plant-Based Foods and Functional Ingredients

Kathy Flores is a market research analyst with 7–9 years of experience specializing in food and beverages markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.