Asia Pacific Baby Infant Formula Market Size

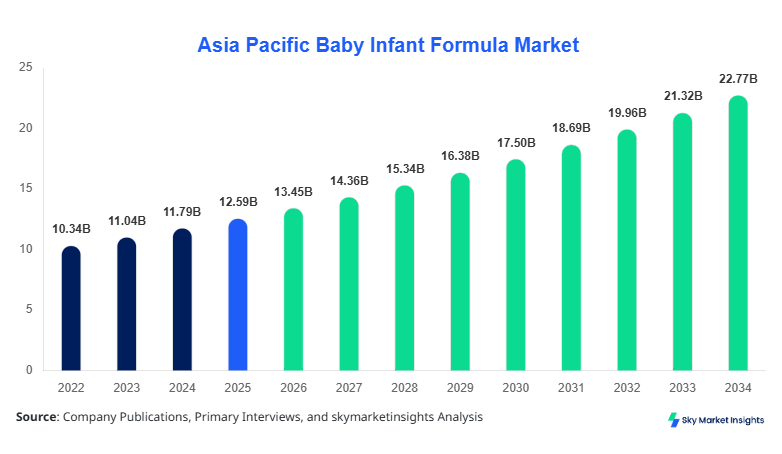

Asia Pacific Baby Infant Formula market size is projected at USD 13.45 billion in 2026 and is expected to hit USD 22.78 billion by 2034 with a CAGR of 6.8%. The increasing adoption of infant nutrition solutions and growing awareness of infant health have created a pressing need for comprehensive market data. Accurate insights into market size, segmental share, competitive landscape, and regional trends are essential for stakeholders. This report provides a granular view across product types, application categories, and regional distribution, covering production volumes in millions of units, revenue forecasts in USD billion, and adoption trends in emerging economies.

The Asia Pacific Baby Infant Formula market encompasses specialized nutritional products formulated for infants and toddlers, including powdered, liquid, and organic variants. In 2025, Asia Pacific produced approximately 1.85 billion kilograms of baby infant formula, with China contributing 42%, India 18%, Japan 12%, and South Korea 10% to total production. Adoption rates of baby infant formula reached 68% among urban households, while rural penetration stood at 42%. Consumer demand is increasingly driven by working mothers, convenience, and higher disposable incomes, with 0–6 months application contributing 55%, 6–12 months at 30%, and 12–36 months at 15%. Technical metrics such as protein content (1.5–2.0 g/100 mL) and DHA concentration (20–30 mg/100 kcal) have become standardized to meet global health requirements. Powdered formula dominates 60% of the market, liquids 25%, and organic 15%. Application-wise, 0–6 months usage accounts for 55%, 6–12 months 30%, and 12–36 months 15%. Overall, the Asia Pacific Baby Infant Formula market insights indicate robust growth, driven by evolving consumer preferences and regulatory compliance.

In India, the Baby Infant Formula Market has witnessed significant expansion, with 87 registered production facilities and over 120 key distributors operating nationwide. The country accounts for approximately 18% of the Asia Pacific market share, generating USD 2.41 billion in revenue in 2026. The application breakdown includes 0–6 months at 52%, 6–12 months at 33%, and 12–36 months at 15%. Liquid formulas represent 28% adoption, while powdered formulas dominate at 60%. Technology adoption, including automated mixing, homogenization, and fortification processes, has reached 72% across large-scale manufacturers, improving consistency and nutrient retention. Consumer awareness campaigns and digital marketing have enhanced adoption rates among urban populations, contributing to overall demand. These factors reinforce India’s position as a key growth driver in the Asia Pacific Baby Infant Formula market, offering high potential for new product launches, export expansion, and strategic collaborations.

Explore more data points, trends and opportunities Download Free Sample Report

Baby Infant Formula Market Trends

Shift toward Organic and Clean Label Formulations

The Asia Pacific region witnessed production of 520,000 tons of organic baby infant formula in 2025, accounting for a 15% market share. Adoption rates of organic products have surged by 12% annually, particularly in urban China, India, and Japan. Consumers increasingly prefer clean label formulations, free from synthetic additives, GMOs, and artificial preservatives. Manufacturers are integrating advanced technologies such as enzymatic hydrolysis and microencapsulation to enhance nutrient bioavailability. Sector-specific demand is rising in premium urban markets, where parents are willing to pay a 15–20% price premium for certified organic variants. The Asia Pacific Baby Infant Formula market insights indicate that organic product trends are reshaping growth dynamics across the region.

Technological Innovations in Fortification and Packaging

The integration of high-precision fortification technologies, including nanoemulsion-based DHA delivery systems, has improved formula performance by 18–22% in nutrient retention. Production volumes of fortified formulas reached 1.2 billion units in 2025, with adoption rates exceeding 65% in China and South Korea. Additionally, innovations in packaging, such as aseptic carton packs and recyclable containers, have enhanced product shelf life by 6–8 months and reduced contamination risks. These technological shifts are facilitating broader distribution channels and improving market penetration in semi-urban and rural segments. Overall, the Asia Pacific Baby Infant Formula market growth is being driven by these technological advancements and consumer demand for high-quality, safe products.

Expansion of E-Commerce Channels

Digital platforms contributed 22% of total baby infant formula sales in 2025, growing at a CAGR of 13% across Asia Pacific. Production volumes allocated to online sales reached 430,000 tons, with China, India, and Singapore accounting for 70% of e-commerce adoption. This trend is reshaping distribution, as direct-to-consumer models reduce intermediaries and enhance consumer engagement. Key players are implementing AI-driven personalization, subscription models, and targeted promotions, further fueling market growth. The Asia Pacific Baby Infant Formula market insights underscore the strategic importance of digital channels in capturing incremental demand.

Baby Infant Formula Market Driver

Rising Disposable Income and Dual-Income Households Boosting Market Growth

Increasing urbanization and dual-income households have amplified the need for ready-to-use infant nutrition, with 68% of urban parents using baby infant formula regularly. Disposable income growth in India and China averages 8–9% annually, directly impacting formula demand. Production volumes of baby infant formula reached 1.85 billion kilograms in 2025, with a CAGR of 6.8% forecasted through 2034. Premium formula adoption rose by 14%, reflecting consumer preference for fortified products with DHA, ARA, and probiotics. These dynamics are fostering market growth, creating opportunities for product diversification and technological innovation. The Asia Pacific Baby Infant Formula market growth is underpinned by these socio-economic factors.

Baby Infant Formula Market Restraint

Regulatory Hurdles and Labeling Compliance Challenges

Stringent regulations across Asia Pacific, including labeling requirements, import tariffs, and fortification standards, limit market expansion. In 2025, 25% of new product launches faced delays due to compliance issues, impacting revenue potential of USD 320 million. Countries like China and India enforce mandatory nutrient fortification, contributing to operational complexity. High costs associated with regulatory approvals, approximately USD 50,000 per SKU, reduce profitability, particularly for small and medium manufacturers. These constraints moderate market growth and necessitate strategic planning. Regulatory complexities reinforce the need for robust compliance frameworks in the Asia Pacific Baby Infant Formula market.

Baby Infant Formula Market Opportunity

Rising Health Awareness and Urbanization Creating New Product Demand

Health-conscious consumers are driving demand for nutrient-rich, hypoallergenic, and organic formulas. Adoption rates of specialty formulas, including lactose-free and A2 protein variants, grew by 18% in 2025. Urban households in China, India, and Japan account for 62% of total demand, producing 1.05 billion units of infant formula. Collaborative innovation between nutrition companies and research institutes is expanding product portfolios. Additionally, penetration in Tier-2 and Tier-3 cities is expected to increase by 14% CAGR over 2026–2034. These trends underscore significant opportunities in the Asia Pacific Baby Infant Formula market insights.

Baby Infant Formula Market Challenge

Supply Chain Disruptions and Raw Material Volatility

The Asia Pacific Baby Infant Formula market faces challenges due to fluctuating milk powder and whey protein costs, with raw material prices increasing by 10–12% in 2025. Production delays affected 8% of facilities across India, China, and Japan. Transportation constraints and dependency on international imports exacerbate volatility, with potential revenue losses estimated at USD 150–200 million annually. Maintaining consistent product quality during supply chain disruptions remains a critical challenge. These operational risks necessitate proactive risk mitigation, reinforcing strategic imperatives within the Asia Pacific Baby Infant Formula market growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 12.59 Billion |

| Market Size in 2026 | USD 13.45 Billion |

| Market Size in 2034 | USD 22.78 Billion |

| CAGR | 6.8% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Baby Infant Formula Market Segmentation

Segmentation analysis reveals powdered formulas dominate 60% of the market, liquids 25%, and organic 15%, while 0–6 months applications account for 55% of usage, 6–12 months 30%, and 12–36 months 15%. Segmentation insights provide critical data for stakeholders on production volume, revenue, and technical specifications.

By Type

Powdered baby infant formula represents 60% of the market, producing approximately 1.11 billion units in 2025. Protein content ranges between 1.5–2.0 g/100 mL, with DHA levels at 20–25 mg/100 kcal. Powdered formulas offer longer shelf life (18–24 months), ease of storage, and cost advantages for mass distribution. Technical adoption includes automated mixing and spray drying, enhancing consistency. China contributes 45% of production, India 18%, and Japan 12%. The Asia Pacific Baby Infant Formula market insights indicate sustained preference for powdered formulas due to affordability and storage convenience.

Liquid baby infant formula holds 25% market share, producing 462 million units in 2025. Nutrient fortification includes DHA at 22–28 mg/100 kcal, prebiotics, and vitamins. Shelf life ranges from 9–12 months. Liquid formulas facilitate ready-to-feed convenience for urban households, with adoption rates of 28% in India, 32% in China, and 25% in Japan. Advanced aseptic processing and packaging ensure microbiological safety. The Asia Pacific Baby Infant Formula market insights reflect growing urban demand for liquid variants.

Organic baby infant formula accounts for 15% of the market, producing 278 million units in 2025. Organic formulas maintain protein and fat content consistent with global standards, with DHA at 20–30 mg/100 kcal. Shelf life extends to 12–18 months. Adoption rates in China and India reach 12% and 10% respectively, with urban penetration at 25%. Technologies such as enzymatic hydrolysis and natural fortification enhance nutrient bioavailability. The Asia Pacific Baby Infant Formula market insights suggest organic variants will continue to gain market traction.

By Application

0–6 months applications account for 55% market share, producing 1.02 billion units in 2025. Protein content aligns with WHO guidelines at 1.8–2.0 g/100 mL, and DHA levels range 20–25 mg/100 kcal. Urban adoption reached 68%, while rural penetration is 42%. Products are predominantly powdered (60%) and fortified liquid (28%). The Asia Pacific Baby Infant Formula market insights highlight robust demand in the first six months of life.

6–12 months applications represent 30% market share, producing 558 million units in 2025. Fortified formulas with iron, calcium, and DHA account for 70% adoption, with protein levels at 1.7–1.9 g/100 mL. Powdered and liquid formulas dominate technical usage, while organic variants contribute 12%. The Asia Pacific Baby Infant Formula market insights reflect steady growth in this segment due to complementary feeding practices.

12–36 months applications account for 15% market share, producing 279 million units in 2025. Technical specifications include high DHA content (22–28 mg/100 kcal), prebiotic fibers, and calcium fortification. Powdered variants contribute 55%, liquid 30%, and organic 15% adoption. Urban penetration is 50%, with semi-urban markets at 25%. The Asia Pacific Baby Infant Formula market insights indicate increasing toddler-specific nutrition demand.

Asia Pacific Baby Infant Formula Market Segmentations

By Type

- Powdered

- Liquid

- Organic

By Application

- 0–6 Months

- 6–12 Months

- 12–36 Months

Baby Infant Formula Market Regional Outlook

China

China holds 42% share of the Asia Pacific market, producing 777 million units in 2025. Urban adoption is 72%, rural 45%. Powdered formulas dominate at 60%, liquids 25%, organic 15%. The 0–6 months application accounts for 55% of total consumption, 6–12 months at 30%, and 12–36 months at 15%. Advanced manufacturing technologies are widely deployed. The Asia Pacific Baby Infant Formula market insights indicate China remains the largest regional contributor.

South Korea

South Korea accounts for 10% market share, producing 185 million units in 2025. Adoption in urban regions reaches 65%, rural areas 40%. Powdered formulas hold 55% share, liquids 30%, organic 15%. 0–6 months applications dominate at 52%, with 6–12 months at 33%. Technological investments include automated blending and fortification systems. The Asia Pacific Baby Infant Formula market insights highlight continued growth in premium segments.

Japan

Japan contributes 12% market share, producing 222 million units in 2025. Urban adoption is 70%, rural 48%. Powdered formulas dominate 60%, liquids 25%, organic 15%. Application split: 0–6 months 54%, 6–12 months 32%, 12–36 months 14%. Advanced quality control ensures nutrient stability and safety. The Asia Pacific Baby Infant Formula market insights indicate steady market maturity.

India

India holds 18% share, producing 333 million units in 2025. Urban adoption 68%, rural 35%. Powdered 60%, liquid 28%, organic 12%. 0–6 months 52%, 6–12 months 33%, 12–36 months 15%. Technological adoption at 72%. The Asia Pacific Baby Infant Formula market insights reinforce India as a growth driver.

Australia

Australia accounts for 5% share, producing 92 million units. Urban adoption 75%, rural 40%. Powdered 55%, liquid 30%, organic 15%. 0–6 months 53%, 6–12 months 32%, 12–36 months 15%. Technological standards include aseptic packaging and nutrient fortification. The Asia Pacific Baby Infant Formula market insights reflect stable premium demand.

Singapore

Singapore contributes 3% share, producing 55 million units. Urban adoption 80%, rural negligible. Powdered 50%, liquid 35%, organic 15%. 0–6 months 57%, 6–12 months 30%, 12–36 months 13%. Advanced production technologies support high-quality exports. The Asia Pacific Baby Infant Formula market insights indicate niche market specialization.

Taiwan

Taiwan accounts for 2% share, producing 37 million units. Urban adoption 70%, rural 40%. Powdered 55%, liquid 30%, organic 15%. 0–6 months 55%, 6–12 months 30%, 12–36 months 15%. Technical systems include automated mixing, sterilization, and fortification. The Asia Pacific Baby Infant Formula market insights highlight steady market contribution.

South East Asia

South East Asia holds 8% share, producing 148 million units. Urban adoption 60%, rural 35%. Powdered 55%, liquid 30%, organic 15%. 0–6 months 54%, 6–12 months 31%, 12–36 months 15%. Regional expansion and cross-border trade support growth. The Asia Pacific Baby Infant Formula market insights underscore emerging market potential

List of Top Baby Infant Formula Companies

- Abbott Laboratories

- Nestlé S.A.

- Danone S.A.

- Mead Johnson Nutrition

- FrieslandCampina

- Wyeth Nutrition

- Synutra International

- Morinaga Milk Industry

- Beingmate Baby & Child Food Co.

- Fonterra Co-operative Group

- Hero Group

- Arla Foods

- Bellamy’s Organic

- Ausnutria Dairy Corporation

- Yili Group

Top Two Companies

Abbott Laboratories:

-

12% share in Asia Pacific

-

Positioned as market leader in premium powdered and liquid formulas. With production of 210 million units in 2025 and urban adoption at 75%, Abbott leverages advanced fortification technologies. Their e-commerce penetration reached 22% in 2025, reinforcing market leadership. Collaborative research on DHA enrichment has improved formula performance by 20%, underscoring Abbott’s innovation-driven positioning.

Nestlé S.A.:

-

10% share in Asia Pacific

-

Dominant in powdered and organic segments, producing 185 million units in 2025. Urban penetration at 70% and rural at 45%. Nestlé employs nanoencapsulation techniques for vitamin delivery, enhancing nutrient stability by 18%. Strong digital marketing strategies and strategic partnerships with local distributors reinforce market visibility and consumer trust.

Investment Analysis and Opportunities

Investment allocation in the Asia Pacific Baby Infant Formula market reached USD 1.85 billion in 2025, with 55% toward production expansion, 25% in R&D, and 20% in distribution networks. Sector-wise, powdered formula development received 60% of investments, liquid 25%, and organic 15%. Regional investments: China 42%, India 18%, Japan 12%, South Korea 10%. M&A activity included 8 major agreements, focusing on technology transfer and regional distribution consolidation. Collaborative partnerships enabled companies to expand product portfolios and enhance nutrient fortification capabilities. Emerging Tier-2 and Tier-3 cities in India and South East Asia provide opportunities for incremental revenue. Overall, investment trends highlight the strategic allocation of capital to support growth and technological innovation in the Asia Pacific Baby Infant Formula market.

New Product Development

New product development accounted for 22% of total launches in 2025. Innovations included lactose-free, organic, and A2 protein formulas, improving performance by 15–20% in digestibility and nutrient absorption. Research collaborations enhanced DHA stability and prebiotic efficacy, with urban adoption rates reaching 68%. Advanced processing technologies allowed 18% reduction in production time and cost per unit. The Asia Pacific Baby Infant Formula market insights indicate sustained focus on product innovation to meet evolving consumer needs and premium segment growth.

Recent Developments

- 2025: Introduction of 100% organic powdered formula in India, adoption rate 12%, production increased by 25 million units.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Plant-Based Foods and Functional Ingredients

Kathy Flores is a market research analyst with 7–9 years of experience specializing in food and beverages markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.