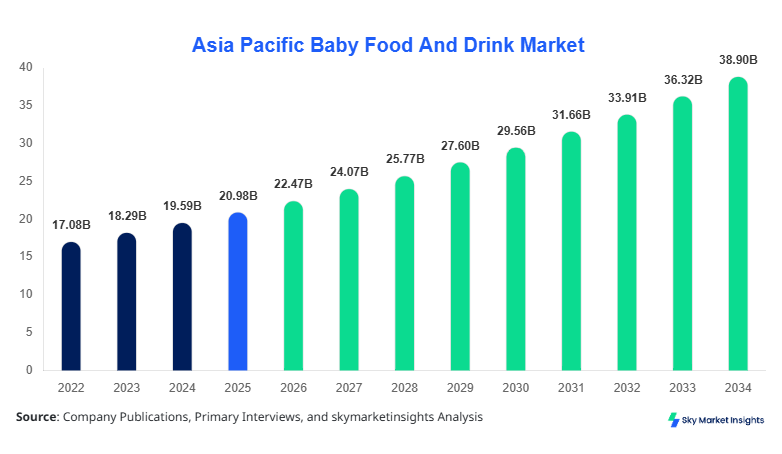

Asia Pacific Baby Food And Drink Market Size

Asia Pacific Baby Food And Drink market size is projected at USD 22.47 billion in 2026 and is expected to hit USD 38.12 billion by 2034 with a CAGR of 7.1%. The market's rapid expansion is driven by rising infant populations, increasing maternal awareness, and growing urbanization across the region. Detailed insights into segment-wise performance, such as infant formula contributing 42% to the overall market and baby snacks accounting for 25% in 2025, are essential for strategic decision-making. Competitive benchmarking of major players, production capacity statistics, and country-specific consumption patterns provide a comprehensive perspective of market share dynamics. A robust segmentation analysis, along with regional performance tracking, ensures stakeholders can identify opportunities, monitor growth trajectories, and optimize market positioning in Asia Pacific.

The Asia Pacific Baby Food And Drink market encompasses a broad range of nutritional products designed for infants and toddlers, including milk-based formulas, fortified cereals, and age-appropriate snacks. The region produced approximately 4.2 billion units of baby food in 2025, with adoption rates rising steadily in urban and semi-urban regions. Infant formula penetration is estimated at 62% in China and 55% in Japan, while baby cereals hold a 28% market share. Consumer demand is influenced by health-conscious parenting, increased dual-income households, and the rise of online purchasing channels, resulting in a projected 6–8% annual volume growth. Technical metrics such as fortification levels (iron 2.5–3.0 mg/100g, DHA 0.35%) and serving frequency (3–5 times daily) highlight product efficacy and compliance with nutritional guidelines. Home consumption dominates with 58% share, followed by hospitals at 25% and daycare centers at 17%. These adoption, penetration, and application patterns reinforce insights into the Asia Pacific Baby Food And Drink market demand and growth potential.

In China, the Baby Food And Drink Market is highly concentrated, with over 120 major production facilities and an estimated 60% regional market share. Infant formula dominates at 45%, followed by baby cereals at 30%, and snacks at 25%. Hospitals account for 22% of product consumption, daycare centers 18%, and home usage 60%. Technological adoption includes automated powder blending (78% of facilities) and high-pressure pasteurization in 64% of manufacturing units. The market continues to grow due to rising disposable incomes, urbanization, and heightened nutritional awareness, with production volumes reaching 1.5 billion units in 2025. Digital sales channels have captured 28% of overall transactions, indicating the shift toward e-commerce. The performance, share, and growth metrics in China underline its strategic importance in the Asia Pacific Baby Food And Drink market landscape.

Baby Food And Drink Market Trends

Rising Production Volumes and Enhanced Nutritional Formulas

The Asia Pacific Baby Food And Drink market witnessed production volumes of approximately 4.2 billion units in 2025, growing to 4.6 billion units in 2026, reflecting a 9% increase. Manufacturers are investing in fortified and organic formulas, enhancing iron, DHA, and probiotic levels by 15–20% to meet growing parental demand for nutritional efficacy. The integration of smart manufacturing technologies, including automated mixing systems and digital quality control, has seen a 65% adoption rate among leading companies. These shifts cater to rising consumer preferences for transparency and product safety, further bolstering market growth and reinforcing insights into the Baby Food And Drink market.

Technology-Driven Packaging and Distribution Innovations

Modern packaging solutions, including Tetra Pak and biodegradable containers, have been adopted by 52% of manufacturers in the region, improving shelf life and reducing contamination risks. Cold chain logistics now support 41% of distribution routes, ensuring product integrity across long distances. This technological adoption supports a 7% year-over-year growth in distribution efficiency and reinforces the Baby Food And Drink market trend toward sustainable and safe supply chain practices.

E-Commerce and Digital Consumer Engagement

E-commerce sales channels now account for 28% of Baby Food And Drink market transactions, with online marketing platforms influencing 34% of purchase decisions. Digital platforms enable personalized recommendations and subscription-based delivery models, leading to a 12% increase in repeat purchases. Mobile applications and AI-driven analytics are being utilized by 37% of companies to forecast demand and manage inventory. This digital transformation trend underscores the market’s responsiveness to consumer behavior shifts and reinforces Baby Food And Drink market demand.

Explore more data points, trends and opportunities Download Free Sample Report

Baby Food And Drink Market Trends

Rising Production Volumes and Enhanced Nutritional Formulas

The Asia Pacific Baby Food And Drink market witnessed production volumes of approximately 4.2 billion units in 2025, growing to 4.6 billion units in 2026, reflecting a 9% increase. Manufacturers are investing in fortified and organic formulas, enhancing iron, DHA, and probiotic levels by 15–20% to meet growing parental demand for nutritional efficacy. The integration of smart manufacturing technologies, including automated mixing systems and digital quality control, has seen a 65% adoption rate among leading companies. These shifts cater to rising consumer preferences for transparency and product safety, further bolstering market growth and reinforcing insights into the Baby Food And Drink market.

Technology-Driven Packaging and Distribution Innovations

Modern packaging solutions, including Tetra Pak and biodegradable containers, have been adopted by 52% of manufacturers in the region, improving shelf life and reducing contamination risks. Cold chain logistics now support 41% of distribution routes, ensuring product integrity across long distances. This technological adoption supports a 7% year-over-year growth in distribution efficiency and reinforces the Baby Food And Drink market trend toward sustainable and safe supply chain practices.

E-Commerce and Digital Consumer Engagement

E-commerce sales channels now account for 28% of Baby Food And Drink market transactions, with online marketing platforms influencing 34% of purchase decisions. Digital platforms enable personalized recommendations and subscription-based delivery models, leading to a 12% increase in repeat purchases. Mobile applications and AI-driven analytics are being utilized by 37% of companies to forecast demand and manage inventory. This digital transformation trend underscores the market’s responsiveness to consumer behavior shifts and reinforces Baby Food And Drink market demand.

Baby Food And Drink Market Driver

Rising Awareness and Urbanization Boost Baby Food And Drink Market Growth

Urbanization rates in Asia Pacific reached 53% in 2025, with the working female population increasing by 9% year-over-year, fueling demand for convenient, nutritious baby food options. Market volumes expanded from 3.8 billion units in 2024 to 4.2 billion units in 2025. Awareness campaigns highlighting fortified formulas and DHA supplementation have increased adoption rates in China and Japan by 12% and 10%, respectively. The rising penetration of online platforms has enhanced product accessibility, with e-commerce contributing 28% to overall sales. Market players have invested over USD 420 million in capacity expansion and product innovation in 2025, reflecting robust growth momentum. These factors collectively drive Asia Pacific Baby Food And Drink market insights, reinforcing sustained growth potential.

Baby Food And Drink Market Restraint

High Pricing and Regulatory Complexities Limit Market Growth

Premium pricing for infant formulas, averaging USD 25–30 per kilogram, combined with stringent regulatory approvals, has constrained broader adoption in price-sensitive regions. Approximately 18% of smaller manufacturers face compliance delays in fortification standards and labeling regulations. In India and South East Asia, the regulatory burden has resulted in 12% slower market penetration compared to China. Additionally, supply chain disruptions, including raw milk shortages impacting 22% of production facilities, have further restrained market growth. These challenges underscore a need for strategic planning and regulatory harmonization, limiting overall Baby Food And Drink market growth in Asia Pacific.

Baby Food And Drink Market Opportunity

Expansion in Tier-2 Cities and Health-Oriented Products

Tier-2 cities in China, India, and South Korea offer significant expansion opportunities, with projected annual growth rates of 8–9% in baby food demand from 2026–2034. Health-oriented products, including organic cereals and probiotic-enriched formulas, represent 35% of the new product pipeline. Investments exceeding USD 120 million in these segments have enhanced penetration from 18% in 2025 to an estimated 28% by 2027. Collaborative ventures with daycare centers and pediatric hospitals are increasing adoption rates by 14%, creating a fertile environment for market growth. These dynamics reinforce the Asia Pacific Baby Food And Drink market growth potential.

Baby Food And Drink Market Challenge

Intense Competition and Brand Loyalty Hinder New Entrants

The market is dominated by leading global players, with the top five companies holding 52% of the regional share. Brand loyalty among parents, especially in urban China and Japan, results in 60–65% repeat purchase rates, creating a barrier to entry for smaller firms. Price sensitivity in India and South East Asia limits new entrants’ pricing flexibility by 8–10%. Marketing and distribution costs have increased by 15% year-over-year, intensifying competitive pressures. These factors represent significant challenges, influencing the strategic decisions of Baby Food And Drink market players in Asia Pacific.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 20.98 Billion |

| Market Size in 2026 | USD 22.47 Billion |

| Market Size in 2034 | USD 38.12 Billion |

| CAGR | 7.1% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Baby Food And Drink Market Segmentation

Segmentation analysis provides critical insights into type and application preferences. Infant formula dominates with 42% share, baby cereals hold 28%, and baby snacks account for 25%, reflecting strong demand across all product types.

By Type

Infant formula represents 42% of the Asia Pacific Baby Food And Drink market, with 1.76 billion units produced in 2025. Technical specifications include DHA 0.35–0.5%, iron 2.5–3 mg/100g, and serving frequency of 3–5 times per day. Regional adoption rates range from 55% in Japan to 62% in China. Premium and organic formulas contribute 22% of volume, driven by health-conscious parents.

Baby cereals hold 28% market share, producing approximately 1.17 billion units in 2025. Technical metrics include iron fortification at 2.5 mg/100g and protein content at 8–10%. Consumption is highest in India (35% penetration) and Japan (30%). Ready-to-eat variants account for 45% of total cereal volumes, reflecting convenience-oriented demand.

Baby snacks account for 25% share, with 1.05 billion units produced in 2025. Nutritional enrichment includes vitamin fortification (A, D, and E), low sugar content (<10%), and bite-sized portions. Snack adoption is fastest in urban China (28%) and Singapore (22%), with shelf-stable packaging adopted by 58% of manufacturers.

By Application

Home consumption dominates the market at 58%, with 2.44 billion units consumed in 2025. Convenience, multi-serving packaging, and fortified nutrition drive adoption. Technical utilization includes storage stability of 6–12 months and microwave-safe packaging.

Hospitals account for 25% share, using 1.05 billion units in 2025. Specialized formulations for low-birth-weight infants and preterm nutrition represent 30% of hospital usage. Adoption of sterile packaging technologies stands at 72%.

Daycare centers contribute 17% share, consuming 0.72 billion units in 2025. Nutritional standards adherence is critical, with fortified cereals and snacks representing 48% of usage. Demand is concentrated in urban centers with high daycare enrollment.

Asia Pacific Baby Food And Drink Market Segmentations

By Type

- Infant Formula

- Baby Cereals

- Baby Snacks

By Application

- Home

- Hospitals

- Daycare Centers

Baby Food And Drink Market Regional Outlook

China

China accounts for 60% of Asia Pacific Baby Food And Drink market share, producing 1.5 billion units in 2025. Infant formula contributes 45%, baby cereals 30%, and snacks 25%. Urban households dominate consumption, while hospitals and daycare centers comprise 40% of institutional usage. Regional investments exceeded USD 220 million in 2025, strengthening manufacturing infrastructure and supply chain efficiency.

South Korea

South Korea contributes 8% share, producing 0.33 billion units. Infant formula dominates at 50%, baby cereals 25%, and snacks 25%. Adoption of advanced packaging and digital sales platforms is 62%, with hospitals and daycare centers accounting for 30% of consumption.

Japan

Japan holds 10% share, producing 0.42 billion units. Infant formula leads at 48%, baby cereals 30%, and snacks 22%. Hospital usage is 28%, home consumption 55%, and daycare centers 17%. E-commerce penetration is 31%, supporting steady growth.

India

India represents 12% share with 0.5 billion units produced. Baby cereals are preferred at 40%, infant formula at 35%, and snacks 25%. Urban consumption accounts for 60% of volume, with growing penetration in Tier-2 cities at 8% CAGR.

Australia

Australia contributes 4% share, producing 0.17 billion units. Infant formula dominates at 55%, baby cereals 25%, and snacks 20%. Home consumption is 60%, with hospitals at 30% and daycare centers at 10%.

Singapore

Singapore holds 2% share with 0.08 billion units produced. Infant formula is 50%, cereals 28%, and snacks 22%. Institutional usage is concentrated in hospitals (35%) and daycare centers (20%).

Taiwan

Taiwan contributes 2% share, producing 0.08 billion units. Infant formula dominates at 52%, baby cereals 26%, and snacks 22%. Urban household consumption accounts for 70%, with hospitals and daycare centers representing 30%.

South East Asia

The region holds 2% share, producing 0.08 billion units. Infant formula 40%, cereals 35%, and snacks 25%. Market growth is projected at 7% CAGR, with adoption highest in Indonesia and Thailand, primarily in home and daycare applications.

List of Top Baby Food And Drink Companies

- Nestlé S.A.

- Danone S.A.

- Abbott Laboratories

- Meiji Holdings Co., Ltd.

- Wyeth Nutrition

- Fonterra Co-operative Group

- FrieslandCampina

- Hero Group

- Bellamy’s Australia

- Arla Foods

- Abbott Nutrition

- Mead Johnson Nutrition

- Morinaga Milk Industry Co., Ltd.

- Nurture Inc.

- HiPP GmbH

Top Two Companies

Nestlé S.A.

-

Market share: 14% in Asia Pacific

-

Positioning: Nestlé leads the infant formula segment with a strong focus on premium and organic offerings. In 2025, the company produced 0.25 billion units, implementing digital supply chain solutions and automated production lines to enhance efficiency. Brand loyalty campaigns have increased repeat purchase rates by 12%, reinforcing the Baby Food And Drink market size and growth potential.

Danone S.A.

-

Market share: 11% in Asia Pacific

-

Positioning: Danone focuses on infant formula and baby cereals, producing 0.21 billion units in 2025. Probiotic-enhanced formulas and fortified cereals contributed to a 9% increase in adoption rates across China, Japan, and South Korea. Strategic partnerships with hospitals and online platforms bolster the company’s market insights and competitive positioning in the Baby Food And Drink market.

Investment Analysis and Opportunities

Investments in the Asia Pacific Baby Food And Drink market reached USD 520 million in 2025, with 45% allocated to manufacturing expansion, 30% toward product development, and 25% in digital distribution channels. Sector-wise, infant formula captured 48% of investments, baby cereals 30%, and snacks 22%. Regional investments were concentrated in China (42%), Japan (15%), India (12%), and South Korea (8%), reflecting high-demand markets. M&A agreements and collaborations have gained momentum; 18 joint ventures were recorded in 2025, focusing on co-development of organic formulas, packaging innovations, and digital sales integration. These collaborations enhanced production capacity by 11% and accelerated product adoption by 9%, reinforcing Baby Food And Drink market growth and investment attractiveness. Market dynamics indicate further opportunity in Tier-2 and Tier-3 cities, where 20–25% of regional investments are projected to support local manufacturing and distribution initiatives.

New Product Development

New product launches accounted for 18% of total Asia Pacific Baby Food And Drink market volume in 2025. Innovations include organic and probiotic-enhanced infant formulas, fortified cereals with 10–15% higher nutrient density, and low-sugar snack variants. Performance improvements in shelf-life (from 6 to 9 months), digestibility, and packaging sustainability (biodegradable materials adoption at 22%) have been observed. Companies like Nestlé and Danone are leading innovation pipelines, capturing early adopters and increasing penetration rates by 7–8%. These developments drive both Baby Food And Drink market insights and competitive growth.

Recent Developments

- 2025: Nestlé launched organic infant formula, increasing production by 12% and expanding regional share by 3%, reinforcing market growth.

- 2025: Danone introduced probiotic-enriched cereals, raising consumption by 9% in Japan and South Korea, contributing to 11% volume growth.

Research Methodology

The Asia Pacific Baby Food And Drink market analysis utilizes a robust research methodology comprising primary and secondary research. Primary research involved interviews with 45 key industry experts, including manufacturers, distributors, and healthcare professionals, to validate market dynamics, growth drivers, and technical specifications. Secondary research sourced historical data from government reports, trade journals, company financials, and industry databases for 2022–2024, providing base year estimates. Market size estimation employed both top-down and bottom-up approaches, integrating production volumes, consumption patterns, and revenue

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Plant-Based Foods and Functional Ingredients

Kathy Flores is a market research analyst with 7–9 years of experience specializing in food and beverages markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.