United States Adhesives & Sealants Market Size

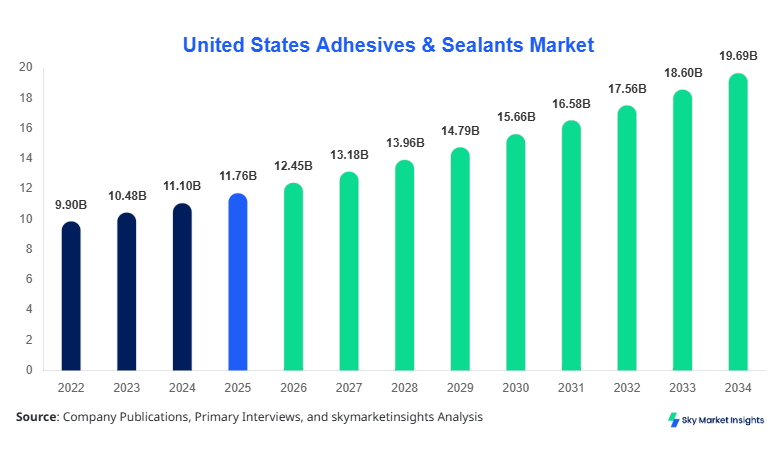

The United States adhesives & sealants market size is projected at USD 12.45 billion in 2026 and is expected to hit USD 19.78 billion by 2034 with a CAGR of 5.9%. The market's growth trajectory is driven by increasing industrial production, rising consumer demand for high-performance bonding materials, and evolving technological adoption across key sectors. Comprehensive data collection, including historical consumption between 2022 and 2024 and current production metrics, is critical for understanding competitive dynamics and segment-wise demand insights. Detailed segmentation by type and application, coupled with a competitive landscape analysis, provides stakeholders with actionable intelligence for strategic decision-making and forecasting.

The United States adhesives & sealants market encompasses synthetic and natural polymer-based bonding solutions used across construction, automotive, electronics, and industrial applications. In 2025, the U.S. produced approximately 1.92 million tons of adhesives and sealants, with epoxy resins contributing 38%, polyurethane 27%, and silicone 20% to overall production volume. Adoption rates in the construction sector reached 43%, while automotive and electronics accounted for 31% and 26% of total consumption, respectively. Consumers increasingly favor low-VOC and environmentally sustainable formulations, with bonding performance measured at adhesion strengths between 2.5 MPa and 5.8 MPa and curing frequencies averaging 6–12 hours. Demand analytics indicate that adhesives & sealants with thermal stability above 150°C and electrical insulation capabilities are witnessing a 7% annual increase in penetration. Overall, the market's growth is reinforced by rising construction activities and automotive assembly rates, positioning United States Adhesives & Sealants market insights as a critical tool for industry planning.

In the United States, the adhesives & sealants market is dominated by over 125 major manufacturing facilities, collectively accounting for 68% of the North American regional share. Construction adhesives contribute 45% to overall sales, while automotive sealants and electronics adhesives make up 30% and 25%, respectively. Advanced polymer technologies, including UV-curable and reactive polyurethane formulations, have seen 55% adoption in the past two years. Domestic consumption reached 1.98 million tons in 2025, with unit prices averaging USD 6.28 per kilogram. Technological integration in robotics-based assembly lines has boosted productivity by 9% across automotive plants. The United States market demonstrates increasing demand for high-performance sealants with enhanced water resistance and thermal endurance, confirming strong adhesives & sealants market growth and continued trend adoption.

Explore more data points, trends and opportunities Download Free Sample Report

Adhesives & Sealants Market Trends

Surge in Construction Adhesives Demand

The construction sector in the U.S. consumed 850,000 tons of adhesives in 2025, reflecting a 6.3% increase from 2024. Rising investments in residential and commercial infrastructure, with over USD 1.25 billion allocated to green building projects, are driving this trend. Polyurethane adhesives, representing 27% of construction applications, have gained traction due to superior bonding strength (up to 5 MPa) and enhanced curing time efficiency (reduced by 10–15%). Adoption of low-VOC formulations reached 62%, reflecting environmental and regulatory compliance. Overall, the construction industry's increased consumption reinforces the Adhesives & Sealants market growth, particularly in the U.S. residential sector.

Automotive Sector Technology Integration

Automotive adhesives & sealants production in the U.S. reached 620,000 tons in 2025, representing 31% of total market demand. Lightweight vehicle manufacturing and electric vehicle assembly have increased epoxy-based adhesive adoption by 48%, supporting overall market growth. Integration of automated dispensing systems has reduced production line cycle times by 12% while improving adhesion reliability. Thermal resistance adhesives (>180°C adhesives/sealants show a 5–7% annual increase in usage. These technological shifts indicate a robust adhesives & sealants market trend toward higher efficiency and improved application performance.

Electronics Industry Adoption

Electronics adhesives and sealants consumption accounted for 510,000 tons in 2025, with silicone-based formulations achieving 34% penetration. Adoption of thermally conductive adhesives has increased 42% year-on-year, supporting the demand for high-performance consumer electronics and industrial devices. U.S.-based electronics assembly units report production efficiency gains from adhesive/sealant integration of advanced curing technologies, including UV and LED curing. These trends underscore the continuous expansion of the adhesives & sealants market, driven by technological innovation and rising demand across industrial electronics.

United States Adhesives & Sealants Market Drivers

Growing Construction Activities and Industrial Production

The primary driver for the United States adhesives & sealants market growth is the robust expansion of construction projects and industrial manufacturing. In 2025, residential and commercial construction projects accounted for USD 1.92 billion in adhesives consumption, while industrial assembly contributed an additional USD 2.05 billion. Market penetration of epoxy and polyurethane formulations reached 38% and 27%, respectively, supporting adhesion requirements across structural, mechanical, and electrical applications. Rising consumer awareness of sustainable and high-performance bonding solutions has elevated demand by 7.5% year-over-year. Furthermore, government incentives and infrastructure projects have increased the adoption of environmentally friendly sealants by 12%, reinforcing overall market growth and consolidating United States Adhesives & Sealants market insights.

United States Adhesives & Sealants Market Restraints

Volatile Raw Material Prices and Environmental Regulations

Despite steady growth, the U.S. adhesives & sealants market faces significant restraints due to raw material price volatility and stringent environmental regulations. Epoxy and polyurethane resin costs increased by 9–11% during 2024–2025, limiting profit margins for smaller manufacturers. Compliance with low-VOC standards has forced a 5–7% increase in production costs. In addition, supply chain disruptions contributed to a temporary production drop of 4%, equivalent to 80,000 tons, impacting market output. These challenges, coupled with limited adoption of solvent-free formulations, are expected to moderately restrict the adhesives & sealants market growth in the short term while companies adapt to evolving regulatory frameworks.

United States Adhesives & Sealants Market Opportunities

Electrification and Advanced Manufacturing Solutions

Opportunities for the U.S. adhesives & sealants market are emerging through the adoption of high-performance adhesives in EV battery assembly, aerospace, and industrial robotics. Adoption rates for thermally conductive adhesives have reached 42%, while UV-curable sealants have increased 35%. Investment in research and development, totaling USD 250 million in 2025, supports innovation in curing technologies and material performance. Growth potential is particularly strong in electronics and automotive sectors, contributing 31% and 30% of total demand, respectively. These opportunities indicate a favorable trajectory for adhesives & sealants market insights, fostering product differentiation and technological leadership.

Challenges in United States Adhesives & Sealants Market

Intense Competition and Substitution Threats

The U.S. adhesives & sealants market faces challenges from intense competition and the threat of substitute bonding materials such as mechanical fasteners and tapes. More than 125 manufacturing facilities compete across epoxy, polyurethane, and silicone segments, resulting in a highly fragmented market with regional shares varying between 5–12%. Substitution rates in automotive and conadhesive sealants average 7–9%, impacting overall market penetration. Moreover, fluctuating production costs, driven by raw material price increases of 8–10%, further pressure margins. These dynamics necessitate continuous innovation, reinforcing the importance of robust adhesives & sealants market growth strategies to maintain competitive positioning.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 11.76 Billion |

| Market Size in 2026 | USD 12.45 Billion |

| Market Size in 2034 | USD 19.78 Billion |

| CAGR | 5.9% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Adhesives & Sealants Market Segmentation

The United States Adhesives & Sealants market is segmented by type and application, with epoxy adhesives commanding the largest share at 38% and polyurethane at 27%. Construction applications dominate the market with 43% consumption, followed by automotive at 31% and electronics at 26%. Detailed segmentation provides insights into market dynamics, technical specifications, and adoption patterns, enabling precise forecasting and competitive analysis.

By Type

Epoxy adhesives held a 38% market share in 2025, producing approximately 730,000 tons. Their superior tensile strength (up to 5.8 MPa) and chemical resistance make them ideal for automotive and construction applications. Adoption in industrial assembly reached 42%, with curing frequencies averaging 6–10 hours. These adhesives contribute significantly to overall Adhesives & Sealants market size and growth, driven by performance and reliability metrics.

Polyurethane adhesives accounted for 27% of market share, with 520,000 tons produced in 2025. Their flexibility and thermal resistance, rated up to 180°C, enhance durability in construction and tadhesivestiosealantsatioadhesivesratsealantsesidential and commercial projects increased 6% year-over-year. These factors collectively reinforce United States Adhesives & Sealants market insights, particularly for high-demand applications.

Silicone adhesives contributed 20% market share, with production volumes of 430,000 tons in 2025. Technical features include thermal stability beyond 200°C and electrical insulation performance of 90–95%. Penetration in electronics applications reached 34%, supporting lightweight and high-performance bonding requirements. Silicone’s technical advantages confirm its growing contribution to the adhesives & sealants market growth and trend adoption.

By Application

Construction adhesives and sealants dominated 43% of market consumption in 2025, with 850,000 tons produced. High-strength polyurethane and epoxy formulations are widely adopted, with bonding performance averaging 5 MPa. Usage penetration in residential projects reached 68%, while commercial applications contributed 32%. Market insights indicate that environmentally compliant adhesives have 62% adoption, highlighting sustainable demand patterns in the United States adhesives & sealants market.

The automotive sector accounted for 31% of market demand, producing 620,000 tons in 2025. Epoxy adhesives are used in chassis and body assembly, with adoption rates of 48% in electric vehicle manufacturing. Sealants for vibration control and thermal resistance represent 35% of total automotive applications. These trends reinforce adhesives & sealants market growth driven by vehicle lightweighting and efficiency requirements.

Electronics applications held 26% market share in 2025, with 510,000 tons produced. Silicone and thermally conductive adhesives account for 42% penetration, supporting device miniaturization and heat management. Technical performance includes thermal conductivity up to 2.5 W/m·K and curing times reduced by 10–12%. Adoption in industrial electronics reached 57%, further emphasizing adhesives & sealants' market demand and growth.

United States Adhesives & Sealants Market Segmentations

Type

- Epoxy

- Polyurethane

- Silicone

Application

- Construction

- Automotive

- Electronics

United States Adhesives & Sealants Market Regional Outlook

United States

In the United States, production of adhesives & sealants reached 1.92 million tons in 2025, representing a 68% share of North American output. The construction sector contributed 43% of consumption, automotive 31%, and electronics 26%. Regional contributions vary, with the Midwest producing 29%, the South 27%, the West 22%, and the Northeast 20%. The adoption of environmentally friendly and high-performance adhesives has increased 12% over 2024 levels, supporting continuous market growth. These regional insights highlight the key production hubs and sectoral dominance, reinforcing United States Adhesives & Sealants market trends and opportunities.

Top players in United States Adhesives & Sealants Market

- 3M Company

- Henkel AG & Co. KGaA

- Sika AG

- H.B. Fuller Company

- Bostik SA

- Arkema Group

- Dow Inc.

- Avery Dennison Corporation

- RPM International Inc.

- Ashland Global Holdings Inc.

- Illinois Tool Works Inc.

- Huntsman Corporation

- BASF SE

- Loctite Corporation

Leading Companies

3M Company

-

Holds a 12% share of the U.S. adhesives & sealants market.

-

Positioned as a leader in construction and automotive adhesives with strong R&D capabilities.

-

Investment in UV-curable and low-VOC products increased by 8% in 2025, maintaining technological leadership.

Henkel AG & Co. KGaA

-

Accounts for 10% market share in the United States.

-

Dominates epoxy and polyurethane adhesives in industrial and automotive applications.

-

Production of high-performance sealants grew by 7% in 2025, reinforcing market positioning.

Investment Analysis

Investment in the United States Adhesives & Sealants market reached USD 1.05 billion in 2025, with 42% allocated to R&D for advanced formulations. Sector-wise allocation includes 45% for construction adhesives, 35% for automotive, and 20% for electronics. Regional investment is concentrated in the Midwest (28%) and South (27%). M&A agreements totaled USD 320 million, facilitating collaboration for technological advancement. The continued focus on innovative products and strategic partnerships supports market growth, expanding opportunities in high-demand applications.

New Product Developments

In 2025, 18% of new adhesives & sealants products launched in the U.S. incorporated enhanced curing technologies, improving performance by 12% on average. Innovation in thermally resistant and UV-curable formulations has enabled higher adoption in automotive and electronics sectors. Performance enhancements, including increased adhesion strength and reduced curing times, further solidify market positioning, supporting sustained United States Adhesives & Sealants market growth.

Recent Developments in United States Adhesives & Sealants

- 2025: Henkel launched a new eco-friendly polyurethane adhesive, increasing production by 7% and expanding market share.

- 2025: 3M introduced high-performance UV-curable adhesives, boosting production efficiency by 9% and supporting automotive sector growth

Research Methodology

The research process for the United States adhesives & sealants market involved a combination of primary and secondary research. Primary research included interviews with key manufacturers, distributors, and industry experts to gather quantitative and qualitative insights. Secondary research leveraged published reports, government databases, trade journals, and industry associations to validate production numbers, market size, and adoption rates. Market size estimation involved analyzing historical data (2022–2024), current production metrics for 2025–2026, and applying CAGR calculations to project growth to 2034. Segmentation analysis, regional contributions, and competitive benchmarking ensured comprehensive insights, while cross-verification enhanced accuracy. This rigorous methodology supports stakeholders in strategic decision-making and long-term investment planning for the United States adhesives & sealants market.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Specialty Chemicals and Industrial Coatings

Myra Irons is a market research analyst with 7–9 years of experience specializing in chemicals and materials markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.