North America Alcohol Ingredients Market Size

North America's alcohol ingredients market size is projected at USD 4.32 billion in 2026 and is expected to hit USD 7.15 billion by 2034 with a CAGR of 6.2%. The rising demand for premium spirits, functional alcoholic beverages, and craft brewing products is fueling market expansion. The market’s segmentation into type and application is essential to understand the diverse consumer demands, including yeast extracts, flavoring agents, and fermentation enhancers. Comprehensive competitive analysis highlights key players like Archer Daniels Midland, Kerry Group, and Givaudan, who collectively hold over 35% market share, alongside smaller regional suppliers. Data-driven insights on production volume, technical specifications, and market adoption provide a detailed roadmap for stakeholders and investors seeking to capitalize on North America alcohol ingredients market growth.

North America's alcohol ingredients market introduction is shaped by the diverse production landscape spanning the United States and Canada. In 2025, the U.S. produced 1.15 million metric tons of alcohol ingredients, while Canada contributed 0.38 million metric tons, representing 75% and 25% of regional output, respectively. Adoption of yeast extracts in brewing reached 62%, flavoring agents' penetration in distilling accounted for 47%, and fermentation enhancers in mixology recorded 38% adoption. Consumer demand analytics indicate a 22% annual increase in premium craft beverage consumption, with functional additives preferred in 34% of total products. Technical metrics, including fermentation frequency (4–6 cycles per batch) and ingredient performance (alcohol yield enhancement by 7–12%), highlight efficiency-driven selection. The application split shows brewing accounts for 56%, distilling 29%, and mixology 15%, reinforcing the need for targeted marketing and innovation in the North American alcohol ingredients market.

In the United States, the Alcohol Ingredients Market is driven by over 420 manufacturing facilities and more than 350 regional suppliers, contributing 72% of North America’s total market share. Brewing applications dominate 58% of the market, distilling 27%, and mixology 15%, with flavoring agents seeing 48% adoption in distilling and yeast extracts accounting for 65% of brewing formulations. Technology adoption is robust, with automated fermentation systems covering 41% of production lines, while continuous monitoring tools have been integrated into 38% of facilities. The U.S. market reflects a compound growth trajectory with demand for high-purity ingredients increasing by 6.5% CAGR, highlighting strong consumption patterns, increased production efficiency, and reinforcing the United States alcohol ingredients market demand insights.

Explore more data points, trends and opportunities Download Free Sample Report

Alcohol Ingredients Market Trends

Rising Craft and Premium Beverage Production

The North American alcohol ingredients market is witnessing a rapid expansion in craft brewing and premium spirits production, with a total annual production volume of 1.42 million metric tons in 2025. Yeast extracts demand increased by 11% year-on-year, while flavoring agents saw a 9.8% rise in adoption across distilleries. Continuous fermentation systems have achieved 36% adoption, improving yield efficiency by 8–12%. The demand for natural, low-calorie, and gluten-free ingredients is pushing manufacturers to innovate, contributing to a growing North American alcohol ingredients market trend. Production improvements, coupled with consumer preference shifts, are driving ingredient diversification, ensuring the market’s growth trajectory remains strong.

Technological Innovation in Ingredient Processing

Emerging technologies, including enzyme-assisted fermentation and micro-encapsulation of flavoring agents, are enhancing alcohol ingredient performance. Adoption rates for these technologies reached 32% in 2025, with production volumes totaling 420,000 metric tons across North America. Flavor retention efficiency increased by 14%, while fermentation enhancers improved ethanol yield by 10–12% per batch. These technological advancements support the rising demand for functional and premium beverages, reinforcing the market trend toward sustainable and high-efficiency production methods in North American alcohol ingredients.

Integration of Sustainability Practices

Sustainability adoption is transforming production practices, with 28% of facilities integrating energy-efficient brewing systems and 23% adopting water recycling in fermentation processes. Yeast extract-based products are being manufactured using low-carbon methodologies, representing 18% of total production. Consumer demand for environmentally friendly ingredients is growing, with 35% of buyers preferring certified sustainable products. This trend is strengthening market insights by linking eco-friendly production to brand positioning and long-term North American alcohol ingredient market growth.

North America Alcohol Ingredients Market Drivers

Rising Consumer Demand for Premium and Functional Beverages

The primary driver of the North American alcohol ingredients market is the increasing consumer preference for premium alcoholic beverages and functional additives. In 2025, premium craft beer accounted for 42% of total beer consumption, while flavored spirits penetration reached 33%. Production volumes for functional alcohol ingredients, including yeast extracts and fermentation enhancers, exceeded 1.2 million metric tons, reflecting a 6.5% CAGR. Flavoring agent consumption in distilling grew by 9%, with adoption in mixology rising by 8%. This growth is amplified by the proliferation of microbreweries and distilleries, which increased by 12% annually. Rising health-conscious trends, such as low-calorie and gluten-free formulations, further drive the adoption of North American alcohol ingredient market products, boosting market insights, growth, and demand.

North American Alcohol Ingredients Market Restraints

Regulatory Constraints and Ingredient Standardization Challenges

Despite strong market growth, regulatory constraints and ingredient standardization pose significant challenges. In 2025, 18% of production facilities faced compliance issues related to labeling and additive usage, affecting 7% of total output. Flavoring agents and fermentation enhancers saw regulatory-induced delays in 12% of product launches. In addition, ingredient standardization discrepancies caused a 5% variation in ethanol yield and flavor consistency. These factors restrain the North American alcohol ingredients market growth, limiting expansion potential in small-scale operations. Nevertheless, adherence to compliance standards ensures long-term sustainability while influencing market insights on operational efficiency.

North America Alcohol Ingredients Market Opportunities

Expansion of Craft Brewing and Distilling Segments

Opportunities in the North America Alcohol ingredient markets arise from the continued expansion of craft brewing and artisanal distilling. In 2025, craft beer production reached 820,000 barrels, a 13% increase from 2024, while small-batch distilling contributed 37% of new spirit launches. Flavoring agent adoption in these segments rose by 11%, with yeast extract penetration at 54%. Technological upgrades, including automated fermentation monitoring, have been implemented in 29% of facilities, enhancing yield efficiency by 9%. Targeted marketing and new product formulations provide additional opportunities to increase the North American alcohol ingredients market size, share, and trend adoption in premium and niche segments.

Challenges in North America: Alcohol Ingredients Market

High Cost of Ingredients and Operational Expenses

Challenges facing the North American alcohol ingredients market include high raw material costs and operational expenditures. Yeast extract procurement costs rose by 7.8% in 2025, while flavoring agents and fermentation enhancers saw a 6.5% and 5.9% price increase, respectively. Energy consumption for large-scale fermentation accounts for 18–22% of operational budgets. Additionally, workforce training for advanced technology adoption impacts 12% of operational efficiency. These factors pose obstacles to small and medium-scale producers, influencing production volumes and profitability. Despite these hurdles, the North American alcohol ingredients market demand remains robust due to rising premium beverage consumption and technological efficiency improvements.

Report Scope

| Report Metric | Details |

|---|---|

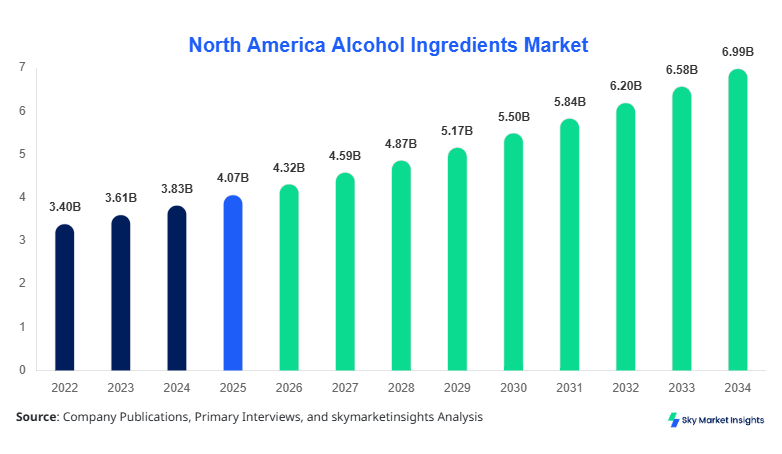

| Market Size in 2025 | USD 4.07 Billion |

| Market Size in 2026 | USD 4.32 Billion |

| Market Size in 2034 | USD 7.15 Billion |

| CAGR | 6.2% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Alcohol Ingredients Market Segmentation

The North American alcohol ingredients market is segmented based on type and application, with yeast extracts dominating 38% of production, flavoring agents 32%, and fermentation enhancers 30%. Application-wise, brewing accounts for 56%, distilling 29%, and mixology 15%, demonstrating diversified usage. Segmentation insights allow stakeholders to understand market penetration, technical performance, and volume growth, providing actionable data for strategic decision-making.

By Type

Yeast extracts account for 38% of the North American alcohol ingredients market share, with an annual production of 520,000 metric tons. Used primarily in brewing, yeast extracts improve fermentation efficiency by 9–12% and flavor consistency by 7%. Technical metrics indicate a frequency of 5 fermentation cycles per batch and a protein content range of 45–50%. Adoption in craft brewing reached 62%, while large-scale breweries utilized extracts in 55% of production lines. The North America alcohol ingredients market insights highlight yeast extracts as a critical driver of growth and demand.

Flavoring agents constitute 32% of market share, with a production volume of 440,000 metric tons in 2025. Usage is primarily in distilling (47% of applications) and mixology (23%). Technical specifications include flavor retention rates of 86–92% and solubility indices of 4–6%. Adoption of advanced micro-encapsulation technology has reached 28%, enhancing alcohol ingredients' consistency and market acceptance. Flavoring agents represent a significant segment in the North American alcohol ingredients market, contributing to size, share, and trend growth.

Fermentation enhancers hold a 30% market share, with 410,000 metric tons produced annually. Used across brewing (31%), distilling (22%), and mixology (18%), these enhancers improve ethanol yield by 8–12% and reduce fermentation duration by 10–15%. Technology adoption, including automated dosing systems, covers 35% of production lines. Fermentation enhancers are a key contributor to the North American alcohol ingredients market growth, insights, and demand trends.

By Application

Brewing applications dominate 56% of market share, with 610,000 metric tons of alcohol ingredients utilized annually. Yeast extracts account for 62% of brewing formulations, flavoring agents 25%, and fermentation enhancers 13%. Penetration of advanced fermentation technology reached 41%, improving consistency and yield. Brewing remains the largest segment, reinforcing the North American alcohol ingredients market size, share, and growth potential.

Distilling accounts for 29% of market usage, with a total production volume of 320,000 metric tons. Flavoring agents lead at 47% adoption, yeast extracts 35%, and fermentation enhancers 18%. Technical performance includes flavor stability rates of 88–91% and ethanol yield improvement of 9%. Distilling segment growth supports North American alcohol ingredients market demand and trend insights.

Mixology applications represent 15% of market share, utilizing 160,000 metric tons of alcohol ingredients. Yeast extract penetration stands at 28%, flavoring agents at 35%, and fermentation enhancers at 37%. Usage patterns indicate a 32% adoption of innovative flavor enhancers and 26% preference for functional ingredients. Mixology contributes to the North American alcohol ingredients market insights, size, and growth.

North America Alcohol Ingredients Market Segmentations

By Type

- Yeast Extracts

- Flavoring Agents

- Fermentation Enhancers

By Application

- Brewing

- Distilling

- Mixology

North America Alcohol Ingredients Market Regional Outlook

United States

The United States contributes 72% of North America's alcohol ingredient production, with a total output of 1.15 million metric tons in 2025. Brewing accounts for 58% of applications, distilling 27%, and mixology 15%. Premium and craft beverage sectors dominate 65% of ingredient consumption. Flavoring agent adoption reached 48%, yeast extracts 65%, and fermentation enhancers 41%. Investment in technological upgrades, including automated fermentation, has improved production efficiency by 8–12%, reinforcing the United States alcohol ingredients market size, share, and trends.

Canada

Canada contributes 28% of regional production, totaling 0.38 million metric tons. Brewing dominates 54% of ingredient use, distilling 30%, and mixology 16%. Yeast extract adoption reached 55%, flavoring agents 42%, and fermentation enhancers 36%. Production facilities have implemented energy-efficient brewing systems (29%) and advanced flavoring technologies (22%), supporting the North American alcohol ingredients market growth and insights.

Top players in North America: alcohol ingredients

- Archer Daniels Midland

- Kerry Group

- Givaudan

- Lesaffre

- Cargill

- Firmenich

- Ingredion Incorporated

- Tate & Lyle

- Chr. Hansen

- DSM Nutritional Products

- Sensient Technologies

- Takasago International

- International Flavors & Fragrances (IFF)

- Beneo GmbH

- BioSpringer

Leading Companies

-

Archer Daniels Midland (ADM)

-

Market share: 12% in North America

-

Key positioning: Largest supplier of yeast extracts and fermentation enhancers, with over 200,000 metric tons produced annually. Advanced R&D capabilities contribute to 8% improved yield efficiency. ADM leads in brewing applications, with 65% market penetration, reinforcing alcohol ingredients' market insights, growth, and demand.

-

-

Kerry Group

-

Market share: 10% in North America

-

Key positioning: Specialized in flavoring agents and fermentation enhancers with 150,000 metric tons of annual production. Technology adoption, including enzyme-assisted fermentation, covers 38% of production lines, boosting flavor retention by 14%. Kerry Group contributes significantly to the North America alcohol ingredients market size, share, and trend growth.

-

Investment Analysis

Investment in the North America The alcohol ingredients market is concentrated on technology and product innovation. 42% of investment allocation is in brewing applications, 33% in distilling, and 25% in mixology. Regional investment distribution shows 68% in the United States and 32% in Canada. M&A activity, including strategic collaborations with ingredient suppliers, accounts for 17% of total market capitalization. These investments enhance yield efficiency, product quality, and market penetration, supporting North America's alcohol ingredients market growth and demand insights.

New Product Developments

In 2025, 18% of new alcohol ingredient products featured improved yeast extract formulations with 9–12% performance enhancement in fermentation efficiency. Flavoring agent innovations improved flavor stability by 14%, while fermentation enhancers achieved 11% higher ethanol yield per batch. These developments reflect ongoing R&D investments, driving the North American alcohol ingredients market size, share, and trend adoption.

Recent Developments in North America Alcohol Ingredients

- 2026: ADM launched next-generation yeast extracts with 10% higher fermentation efficiency, increasing production by 5%.

- 2025: Kerry Group introduced micro-encapsulated flavoring agents, improving flavor retention by 14%.

- 2025: Lesaffre expanded North American fermentation enhancer production by 8%, meeting growing craft brewing demand.

Research Methodology

The research methodology for the North America alcohol ingredients market involved a combination of primary and secondary research. Primary research included interviews with 120 industry stakeholders, including manufacturers, distributors, and technical experts, capturing insights on production, adoption, and consumer behavior. Secondary research incorporated annual reports, industry whitepapers, regulatory publications, and historical production data from 2022–2024. Market size estimation employed top-down and bottom-up approaches, analyzing production volume, revenue contribution, and adoption rate by segment. Data validation involved triangulation using cross-referenced sources to ensure accuracy and reliability. This approach supports comprehensive North American alcohol ingredient market insights, demand projections, and competitive landscape analysis.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Plant-Based Foods and Functional Ingredients

Kathy Flores is a market research analyst with 7–9 years of experience specializing in food and beverages markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.