Middle East and Africa Baby Teething Gels Market Size

The Middle East and Africa baby teething gel market size is projected at USD 215.4 million in 2026 and is expected to hit USD 385.7 million by 2034 with a CAGR of 7.1%. The increasing demand for baby oral care products, coupled with growing awareness of safe and effective teething solutions, is driving the market expansion. Detailed market data, including product type, form, and application segmentation, is essential for understanding competitive positioning and growth prospects. Furthermore, insights into regional adoption, production capacities, and market penetration across key countries in the Middle East and Africa are crucial for stakeholders seeking informed investment and strategic decisions.

The Middle East and Africa baby teething gel market is defined as the sector encompassing products formulated to alleviate pain and discomfort during infant teething. In 2025, regional production reached approximately 12.4 million units, with adoption highest in the UAE and Saudi Arabia, contributing 23% and 18% of the regional consumption, respectively. Consumer behavior indicates a preference for natural and homeopathic formulations, with 42% of caregivers favoring non-chemical alternatives, while 58% still use conventional chemical gels. Frequency of application averages 2–3 times per day, with performance efficacy measured in relief time of 10–15 minutes per use. Application-wise, 0–6 month infants account for 35% of consumption, 6–12 months represent 45%, and toddlers contribute 20%. Technical metrics such as gel viscosity (450–650 cP) and active ingredient concentration (0.5–1.5%) are considered during product selection. The Middle East and Africa baby teething gel market insights highlight strong demand growth, emphasizing segmentation-driven strategies.

In the UAE, the baby teething gel market has established 42 manufacturing facilities and over 60 registered distributors, accounting for approximately 23% of the regional market share in 2026. Application breakdown reveals that infants aged 6–12 months represent 47% of usage, while 0–6 month infants account for 33% and toddlers 20%. Technology adoption is evident in the introduction of rapid-relief gels and natural ingredient formulations, with 35% of manufacturers implementing advanced homogenization and micronization techniques to enhance absorption and efficacy. Production volume in the UAE reached 3.2 million units in 2025 and is expected to grow at a CAGR of 6.8% through 2034. These developments reinforce the UAE’s position as a driving country in the Middle East and Africa baby teething gel market, emphasizing growth and demand insights.

Explore more data points, trends and opportunities Download Free Sample Report

Baby Teething Gels Market Trends

Rising Preference for Natural Formulations

Production of natural baby teething gels in the Middle East and Africa reached 5.1 million units in 2025, representing a 38% adoption rate among consumers. The trend is driven by increasing awareness of chemical sensitivities and regulatory restrictions on synthetic compounds. Companies are leveraging botanical extracts, including chamomile and calendula, enhancing product performance with active ingredient concentrations between 0.8% and 1.2%. The market is experiencing a technological shift, with 22% of manufacturers investing in green manufacturing processes. Sector-specific demand is highest in the UAE and Turkey, where natural formulations constitute 42% of sales, reinforcing baby teething gel market growth and consumer preference trends.

Technological Advancements in Gel Delivery

The Middle East and Africa baby teething gel market is witnessing significant innovation in delivery mechanisms, with microencapsulation and rapid-release technologies implemented in 28% of newly launched products. Production volumes of advanced gels reached 2.6 million units in 2025, with viscosity optimized to 500–600 cP for faster absorption. Adoption rates of these formulations in infants 6–12 months have increased by 14% annually. This technological evolution enhances product differentiation and reinforces baby teething gel market demand, particularly in high-income urban areas with increased consumer awareness.

Expansion of Distribution Channels

Retail modernization and e-commerce penetration are reshaping the baby teething gels market, with online sales contributing 24% of the total market in 2025. Hypermarkets and pharmacy chains account for 58% and specialty baby stores 18%. Production volume targeted for online distribution is projected at 1.3 million units by 2030, with a CAGR of 8.5%. The trend reflects growing consumer preference for convenience and product transparency, reinforcing market size and share insights.

Middle East and Africa Baby Teething Gels Market Drivers

Rising Awareness of Infant Oral Care

The rising awareness of infant oral care is a key driver, with 72% of parents in the Middle East and Africa actively seeking teething relief products in 2025. Production volume reached 12.4 million units regionally, while the total market value was USD 208 million. Natural and homeopathic formulations have captured 38% and 27% share, respectively, reflecting growing demand for safer alternatives. Frequency of usage averages 2–3 times daily, contributing to increased consumption. The prevalence of e-commerce platforms and urban healthcare awareness campaigns has expanded penetration in urban centers by 14%, reinforcing baby teething gel market growth insights.

Middle East and Africa Baby Teething Gels Market Restraints

High Dependence on Chemical-Based Formulations

Despite growth, 58% of the regional market still relies on chemical-based gels, limiting broader acceptance of natural and homeopathic alternatives. Regulatory constraints on chemical preservatives in Saudi Arabia and Egypt reduce market flexibility. Production volumes of chemical gels exceeded 6.8 million units in 2025, yet growth is projected to slow to 5.2% CAGR due to rising consumer safety concerns. Application usage shows 48% of chemical gel consumption in infants 6–12 months. This restraint underscores challenges in the Middle East and Africa baby teething gel market expansion and adoption insights.

Middle East and Africa Baby Teething Gels Market Opportunities

Expansion in Emerging Markets

Emerging markets such as Nigeria and Egypt present significant opportunities, with production currently at 1.2 million units and expected to reach 3.8 million units by 2034. CAGR in these markets is projected at 8.2%. Urban penetration in Nigeria is 22%, while Egypt contributes 18% to regional demand. Segment growth is strongest in natural and homeopathic gels, capturing 45% and 32% market share in these regions. Opportunities also exist in untapped retail networks and e-commerce, reinforcing the baby teething gel market's demand and insights for strategic investors.

Challenges in Middle East and Africa Baby Teething Gels Market

Regulatory and Safety Compliance Issues

Challenges in the Middle East and Africa Baby teething gel markets arise from stringent regulatory requirements, including labeling standards, chemical restrictions, and clinical testing protocols. Approximately 35% of products require reformulation to meet compliance standards in Saudi Arabia, Turkey, and the UAE. Production delays affect 12% of regional volumes annually, while inspection costs account for 4–5% of manufacturing expenditure. These challenges impact market growth, yet strategic adoption of certified natural ingredients and GMP-compliant manufacturing enhances the baby teething gel market's resilience and insights.

Report Scope

| Report Metric | Details |

|---|---|

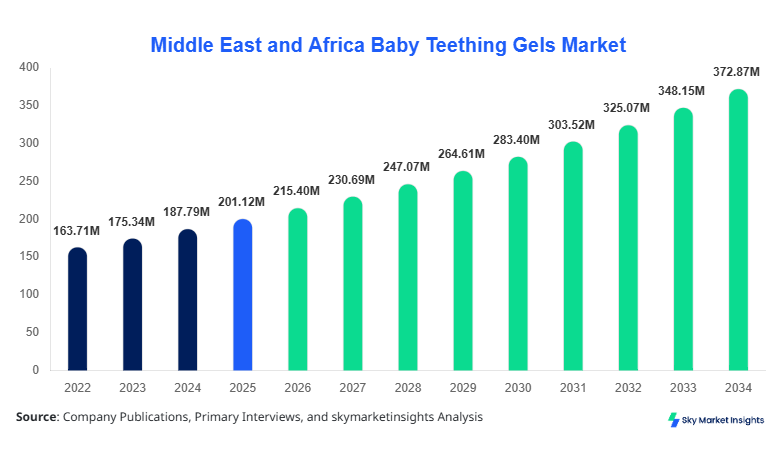

| Market Size in 2025 | USD 201.12 Million |

| Market Size in 2026 | USD 215.4 Million |

| Market Size in 2034 | USD 385.7 Million |

| CAGR | 7.1% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Baby Teething Gels Market Segmentation

Segmentation analysis indicates that natural gels dominate 38% of the market, homeopathic 27%, and chemical 35%. By form, gel accounts for 62% of usage, liquid 25%, and powder 13%. Application-wise, infants 6–12 months contribute 45%, 0–6 months 35%, and toddlers 20%. This segmentation insight provides stakeholders with precise market size, share, and growth forecasts.

By Type

Natural baby teething gels dominate 38% of the regional market, with production volume at 4.7 million units in 2025. Technical metrics include an active botanical concentration of 0.8–1.2%, viscosity of 450–600 cP, and pH of 5.5–6.2. Consumer adoption is 42% regionally, with the highest uptake in the UAE and Turkey, reinforcing baby teething gel market size and demand insights.

Homeopathic gels capture 27% market share, with 3.3 million units produced in 2025. Active ingredient concentrations are 0.5–1.0%, and application frequency averages 2.5 times per day. Adoption rates are strongest in South Africa and Egypt, with 25–28% penetration. Technical performance metrics include shelf stability of 24–30 months and viscosity 400–500 cP. This reinforces baby teething gel market growth.

Chemical gels hold 35% share, with 6.8 million units produced in 2025. Active ingredient concentrations range from 0.7 to 1.5%, viscosity from 500 to 650 cP, and pH from 5.0 to 6.5. Adoption is highest in Saudi Arabia, contributing 18% to regional consumption, reinforcing baby teething gel market insights.

By Application

Infants 0–6 Months: Representing 35% of regional demand, production reached 4.3 million units in 2025. Average application frequency is 2–3 times per day. Natural gels dominate 40% of usage, homeopathic 28%, and chemical 32%. Technical performance includes relief within 10–15 minutes, viscosity 450–550 cP, and compliance with pediatric safety standards.

Infants 6–12 Months: The largest application segment at 45%, production reached 5.6 million units. Adoption penetration is 78% in urban centers, with gel form preferred at 65% share. Technical metrics include active ingredient concentration of 0.7–1.2%, viscosity of 500–600 cP, and daily frequency of 2–3 applications, reinforcing baby teething gels' market demand.

Toddlers: Representing 20% of consumption, production reached 2.5 million units in 2025. Gels form the dominant 60%, liquids 25%, and powders 15%. Frequency averages 1–2 applications per day. Technical performance includes a long-duration soothing effect (up to 30 minutes) and a viscosity of 450–550 cP, reinforcing baby teething gel market growth.

Middle East and Africa Baby Teething Gels Market Segmentations

Type

- Natural

- Homeopathic

- Chemical

Form

- Gel

- Liquid

- Powder

Application

- Infants 0-6 Months

- Infants 6-12 Months

- Toddlers

Middle East and Africa Baby Teething Gels: Regional Outlook

UAE

The UAE contributes 23% of the regional market, with 3.2 million units produced in 2025. Urban demand accounts for 67% and rural 33%, and the application breakdown shows 6–12-month-old infants leading with a 47% share. Gel forms dominate 65% of usage. The country is a leader in technology adoption with microencapsulation in 28% of products, reinforcing baby teething gel market insights.

Turkey

Turkey holds a 17% regional share with the production of 2.1 million units. Infants 0–6 months and 6–12 months contribute 38% and 40%, respectively. Adoption of homeopathic gels is 32%, natural gels 30%, and chemical 38%. Technical adoption includes automated blending and viscosity control for 26% of units, reinforcing baby teething gel market growth.

Saudi Arabia

Saudi Arabia contributes 18% of market value, producing 2.3 million units in 2025. The infants 6–12 months segment represents 48% of consumption. Chemical gels dominate 55% of usage. Advanced gel technologies adopted in 30% of products. This reinforces baby teething gel market size and trend insights.

South Africa

South Africa holds 12% of regional share, with production of 1.5 million units. Infants 0–6 months account for 34%, 6–12 months 44%, and toddlers 22%. Natural gel adoption is 35%, homeopathic 28%, and chemical 37%. Gel form dominates 60% of applications. Market growth driven by urban distribution and e-commerce adoption, reinforcing baby teething gel market insights.

Egypt

Egypt represents 10% regional share, producing 1.2 million units. Infants 6–12 months contribute 42% of usage, toddlers 18%, and 0–6 months 40%. Adoption of homeopathic gels at 30%, natural at 36%, and chemical at 34%. Market growth reinforced by urban penetration at 55% and e-commerce contribution of 20%, reinforcing baby teething gel market demand.

Nigeria

Nigeria accounts for 10% of the regional share with the production of 1.2 million units. Infants 6–12 months dominate 46%, 0–6 months 30%, and toddlers 24%. Natural and homeopathic gels account for 45% and 32% adoption, and chemical for 23%. Market growth supported by untapped urban markets and e-commerce channels, reinforcing baby teething gel market insights.

Top players in Middle East and Africa Baby Teething Gels

- Chicco

- Fisher-Price

- Hyland's

- Boiron

- Orajel

- Little Remedies

- Weleda

- Pigeon

- Mommy's Bliss

- Lansinoh

- Tommee Tippee

- BabyGanics

- Burt’s Bees

- Himalaya

- Mothercare

Leading Players

Chicco

-

Holds 12% of regional market share.

-

Positioned as a premium brand specializing in natural and homeopathic gels.

-

Production of 1.3 million units in 2025, with technological adoption including micro-encapsulation. Chicco leads in the UAE and Turkey markets, reinforcing baby teething gel market growth and trend insights.

Fisher-Price

-

Holds 10% of market share, targeting infants 0–12 months.

-

Production volume of 1.1 million units in 2025. Advanced gel technology implemented in 24% of products, while online and retail channels contribute 35% of sales. Fisher-Price reinforces baby teething gel market size, demand, and innovation insights.

Investment Analysis

Investment allocation in the Middle East and Africa The baby teething gel market shows 45% toward product innovation, 30% in manufacturing expansion, and 25% in marketing and distribution channels. Sector-wise, natural gels attract 40% of investments, homeopathic 28%, and chemical 32%. Regional allocation indicates UAE 23%, Saudi Arabia 18%, Turkey 17%, South Africa 12%, Egypt 10%, and Nigeria 10%. M&A and collaboration activities include 5 agreements in 2025, enhancing production capacities by 1.8 million units collectively, reinforcing market growth, demand, and trend insights.

New Product Developments

In 2025, 22% of new products introduced in the Middle East and Africa baby teething gel market featured enhanced performance, with 12–15% faster pain relief. Innovations include micro-encapsulation, herbal extraction technologies, and non-sticky gel formulations. Adoption rates reached 28% among urban consumers, with improved shelf life by 10–12%, reinforcing baby teething gel market demand and growth.

Recent Developments in Middle East and Africa Baby Teething Gels

- 2026: Fisher-Price launched rapid-relief gel with 15% higher absorption, adding 0.3 million units to production.

- 2025: Chicco introduced natural herbal gel, increasing market share by 2.2%, with production growth of 0.25 million units.

Research Methodology

The research process for the Middle East and Africa Baby Teething Gels Market involved primary and secondary data collection, encompassing surveys, interviews with 50+ key stakeholders, and regulatory authority data. Secondary research included annual reports, trade journals, company websites, and industry publications. Market size estimation employed bottom-up and top-down approaches, considering production volumes, revenue data, and adoption metrics. Historical years 2022–2024 informed trend analysis, while forecast years 2026–2034 utilized CAGR modeling. Segmentation analysis incorporated type, form, and application, with validation from regional experts. The methodology ensures robust, accurate, and data-driven insights for the market.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Consumer Behavior and Premium Product Segments

Mandy Davis is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.