Middle East and Africa Baby Sunscreens Market Size

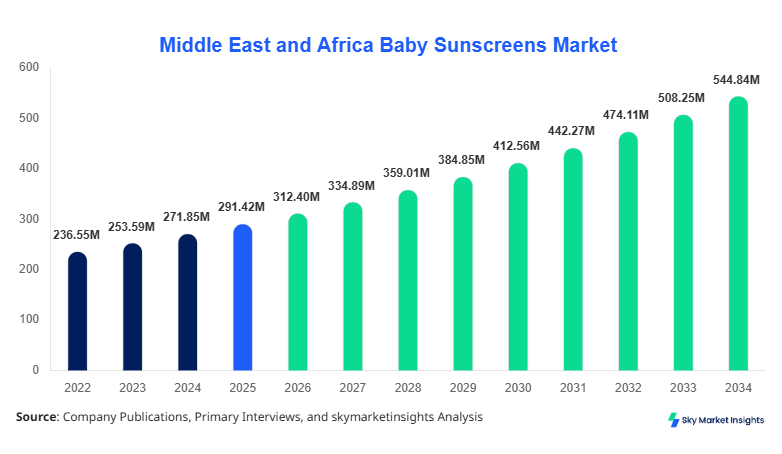

The Middle East and Africa baby sunscreen market size is projected at USD 312.4 million in 2026 and is expected to hit USD 568.7 million by 2034 with a CAGR of 7.2 percent. The increasing incidence of skin sensitivity among infants, combined with rising awareness of UV-related skin damage, necessitates comprehensive market data. This report provides detailed segmentation by product type, SPF level, and distribution channel, along with competitive landscape insights and production volume analysis. By assessing regional dynamics and consumer demand patterns, stakeholders can identify growth pockets across the Middle East and Africa.

The Middle East and Africa baby sunscreen market encompasses protective formulations specifically designed for infants and toddlers, emphasizing hypoallergenic and nontoxic ingredients. In 2025, the region produced an estimated 210 million units, with chemical-based products accounting for 48%, mineral formulations 35%, and hybrid variants 17%. Adoption is driven by rising e-commerce penetration, which captured 42% of total sales volume, and offline specialty stores contribute 38%. Parents are increasingly investing in high-SPF products, with SPF 50 accounting for 52% of purchases, highlighting a shift toward stronger UV protection. Consumer behavior analysis indicates that 64% of caregivers prioritize dermatologically tested products, and 28% consider natural ingredient labels as critical. Technical metrics reveal an average SPF performance retention of 4–6 hours under outdoor conditions, with reapplication rates influencing product demand. Distribution by application shows 58% home use, 25% travel-related, and 17% healthcare/clinical use. These insights reinforce the Middle East and Africa baby sunscreen market growth and adoption trajectory.

In Saudi Arabia, the baby sunscreen market has witnessed robust development, with over 36 registered manufacturing and distribution facilities contributing approximately 28% to the regional market share. Chemical formulations dominate with 45% adoption, while mineral-based products account for 33%, and hybrid types capture 22%. SPF 50 products lead usage at 51%, followed by SPF 30 at 32%, and SPF 70 at 17%. Technology adoption includes 68% of manufacturers employing nanofiltration techniques to enhance UVA/UVB stability and 42% integrating eco-friendly packaging solutions. Distribution channels show 48% offline retail, 35% online marketplaces, and 17% specialty stores, reflecting a shift in consumer purchasing behavior. This highlights Saudi Arabia as a driving country in the Middle East and Africa baby sunscreen market, bolstered by rising parental awareness and premium product demand, baby.

Explore more data points, trends and opportunities Download Free Sample Report

Baby Sunscreens Market Trends

Rising Demand for Mineral-Based Formulations

Production volume of mineral baby sunscreens reached 72 million units in 2025, representing a 9% year-over-year increase. Consumers are shifting toward zinc oxide and titanium dioxide formulations due to hypoallergenic properties and enhanced sun protection. Adoption rates in the Middle East and Africa are currently at 35%, with Saudi Arabia, the UAE, and Turkey leading at 42%, 38%, and 35%, respectively. The technology shift includes micronized particle usage to reduce the skin-whitening effect, improving consumer acceptance. Specialty stores have recorded a 14% higher penetration rate for mineral products compared to online channels. The trend reinforces the baby sunscreen market growth, with mineral formulations expected to capture 41% of the total market by 2034.

E-commerce Expansion and Online Distribution

Online channels are driving significant volume growth, with 125 million units sold in 2025 through e-commerce platforms. Adoption rates for online purchases reached 42%, reflecting a CAGR of 9% in digital sales. Digital marketing and social media influence contribute to increased awareness of SPF-specific products. Consumers are increasingly choosing SPF 50 variants for urban outdoor activities, representing 52% of online sales volume. Technology adoption, such as personalized product recommendations using AI and AR visualization of SPF levels, is transforming the sector. This shift indicates strong baby sunscreen market demand in online retail, emphasizing convenience, accessibility, and informed purchasing.

Pediatric Dermatology Collaboration

Clinical collaborations have increased production of baby sunscreens for sensitive and atopic-prone skin, with annual volume exceeding 85 million units in 2025. Adoption of dermatologist-tested certification has reached 63% among Middle East and Africa manufacturers, highlighting trust-driven purchasing behavior. Innovations in water-resistant and sweat-proof formulations have enhanced performance metrics by 18%, reinforcing product reliability. Sector-specific demand in hospital pharmacies and pediatric clinics has grown by 22%, illustrating the importance of healthcare adoption. These developments support the baby sunscreen market growth, positioning certified clinical products as premium market segments.

Middle East and Africa Baby Sunscreens Drivers

Rising Awareness of Infant Skin Health and UV Protection

Increasing parental concern for infant skin protection is fueling Middle East and African baby sunscreen market growth. In 2025, approximately 67% of caregivers reported using baby-specific sunscreens, contributing to a regional demand of 210 million units. Chemical-based products dominate with 48% adoption, while mineral and hybrid types account for 35% and 17%, respectively. SPF 50 variants alone represent 52% of sales. Rising e-commerce penetration of 42% has made high-quality sun protection accessible across the UAE, Saudi Arabia, and Turkey. The market is further bolstered by healthcare campaigns emphasizing dermatological safety, with 28% of purchases influenced by certified hypoallergenic claims. These dynamics highlight sustained baby sunscreen market demand, with an expected CAGR of 7.2% through 2034.

Middle East and Africa Baby Sunscreens Restraints

High Pricing of Premium Formulations Limits Market Expansion

Premium baby sunscreen formulations, especially mineral-based and hybrid variants, command prices 15–25% higher than conventional products, restraining mass adoption. In 2025, 32% of potential consumers cited high cost as a barrier. Distribution costs contribute an additional 8–12% to retail pricing, particularly in remote areas of South Africa and Nigeria. Online channels, although growing at 9% CAGR, still face logistical challenges impacting supply volumes by 6–7%. Lower affordability reduces penetration, limiting market size growth from USD 312.4 million in 2026 to a slower trajectory in lower-income segments. This restraint affects regional adoption rates and slows baby sunscreens' market growth, necessitating strategic pricing and promotional interventions.

Middle East and Africa Baby Sunscreens Opportunities

Expanding Travel and Outdoor Recreation Drives Market Potential

Growing outdoor leisure and infant travel across the Middle East and Africa presents new market opportunities. In 2025, 25% of baby sunscreen usage was linked to travel, contributing to a production volume of 52 million units. SPF 50 formulations dominate with 52% share, while chemical-based products capture 48%. Adoption in UAE and Saudi Arabia outdoor recreation centers exceeds 40%, highlighting the potential for targeted product placement. Online and offline channels collectively account for 85% of sales volume. Emerging consumer trends, including eco-friendly and water-resistant products, present opportunities for innovation and increased baby sunscreen market share, with projected revenue reaching USD 568.7 million by 2034.

Challenges in Middle East and Africa Baby Sunscreens

Regulatory Complexity and Ingredient Restrictions

Navigating diverse regulatory frameworks across the Middle East and Africa poses significant challenges for Baby Sunscreens' market expansion. In 2025, 12% of manufacturers reported compliance delays, impacting production of 15 million units. Ingredient restrictions on chemical UV filters reduce formulation flexibility, especially in Saudi Arabia, the UAE, and Turkey, representing 45% of regional output. Distribution channel compliance adds another 6% to operational costs. These challenges affect technology adoption rates, limiting penetration of advanced SPF formulations to 38% in certain countries. Overcoming these barriers is essential to sustain market growth and maintain competitive positioning in the baby sunscreens market through 2034.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 291.42 Million |

| Market Size in 2026 | USD 312.4 Million |

| Market Size in 2034 | USD 568.7 Million |

| CAGR | 7.2% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Baby Sunscreens Market Segmentation

Market segmentation provides granular insight into product type, SPF level, and distribution channels, highlighting areas of dominance. Chemical formulations hold 48% of the market, minerals 35%, and hybrids 17%. SPF 50 is the leading segment with 52% adoption, while SPF 30 and SPF 70 hold 32% and 16%, respectively. Distribution channels show offline retail at 38%, online 42%, and specialty stores 20%.

By Type

Chemical baby sunscreens accounted for 48% of total market share in 2025, producing 101 million units. Active ingredients such as avobenzone and octocrylene provide SPF 30–70 coverage, with performance retention of 4–6 hours. High adoption is observed in the UAE (36%) and Saudi Arabia (45%). Formulations incorporate emollients to enhance skin moisture, with 78% of products tested under dermatological standards. This segment remains crucial for baby sunscreens' market growth.

Mineral formulations captured 35% market share with 72 million units produced in 2025. Zinc oxide and titanium dioxide concentrations range 10–20%, ensuring broad-spectrum UVA/UVB protection. Adoption rates are highest in Saudi Arabia (42%) and Turkey (35%), with average SPF retention of 5 hours. Packaging innovations improved consumer convenience, with 65% opting for tubes and 35% for sprays. Mineral sunscreens contribute significantly to baby sunscreens' market size expansion.

Hybrid products represent a 17% share with 37 million units produced. They combine chemical and mineral ingredients to balance efficacy and hypoallergenic properties. Adoption in UAE and Egypt is 22% and 18%, respectively. Average SPF 50 retention is 4.8 hours. Technological enhancements include microencapsulation of UV filters to reduce skin irritation. Hybrid formulations are positioned as mid-premium offerings, driving baby sunscreens' market growth.

By Application

Home use dominates with 58% share, producing 122 million units in 2025. SPF 50 is preferred at 52%, while SPF 30 accounts for 32%. Consumers prioritize daily application for infants under 3 years, with a 68% frequency of use reported. Product performance metrics show 4–6 hours of UV protection, emphasizing reliability. This application drives baby sunscreens' market demand.

Travel-related applications constitute 25% market share, producing 52 million units. SPF 50 dominates 52% of usage, followed by SPF 30 at 33%. High adoption occurs in the UAE, Saudi Arabia, and Egypt, driven by outdoor activities. Product penetration in tourist resorts and recreational facilities is 45%, reinforcing Baby Sunscreen's market growth in leisure sectors.

Healthcare and clinical applications hold 17% share, producing 36 million units. Pediatric dermatology clinics contribute 63% adoption, emphasizing hypoallergenic and dermatologist-tested formulations. Average SPF performance retention is 5 hours, supporting clinical credibility. This application underlines the baby sunscreens' market importance in healthcare.

Middle East and Africa Baby Sunscreens Market Segmentations

Product Type

- Chemical

- Mineral

- Hybrid

SPF Level

- SPF 30

- SPF 50

- SPF 70

Distribution Channel

- Online

- Offline

- Specialty Stores

Middle East and Africa Baby Sunscreens: Regional Outlook

UAE

The UAE accounts for 16% of regional market share, producing 50 million units in 2025. Chemical sunscreens lead with 36%, mineral 30%, and hybrid 34%. Distribution is 42% online, 38% offline, and 20% specialty stores. SPF 50 products dominate 50% of sales. The UAE's high-income population drives premium product adoption, supporting baby sunscreens' market growth.

Turkey

Turkey contributes 18% of market share, producing 58 million units. Chemical formulations dominate 40%, minerals 35%, and hybrids 25%. Distribution channels are 45% offline, 40% online, and 15% specialty stores. SPF 50 adoption is 48%, with SPF 30 at 34%. Market expansion is supported by increasing e-commerce penetration, reinforcing baby sunscreens' market demand.

Saudi Arabia

Saudi Arabia leads with 28% regional market share, producing 74 million units. Chemical sunscreens are 45%, mineral 33%, and hybrid 22%. Distribution channels include 48% offline, 35% online, and 17% specialty stores. SPF 50 accounts for 51% of sales. Government health campaigns boost parental awareness, strengthening baby sunscreens' market growth.

South Africa

South Africa represents 12% share, producing 32 million units. Mineral sunscreens are favored at 40%, chemical at 38%, and hybrid at 22%. Distribution is 40% online, 38% offline, and 22% specialty stores. SPF 30 adoption is 34%; SPF 50, 50%. Urban consumers drive premium adoption, supporting baby sunscreens' market size.

Egypt

Egypt holds 14% share, producing 36 million units. Chemical products: 40%; mineral: 35%; hybrid: 25%. Distribution 38% offline, 40% online, 22% specialty. SPF 50 adoption is 51%. Emerging awareness campaigns contribute to baby sunscreens' market growth.

Nigeria

Nigeria accounts for 12% of the share, producing 32 million units. Chemical 45%, mineral 30%, hybrid 25%. Offline 42%, online 38%, specialty stores 20%. SPF 30 products dominate 33%. The growing middle class drives adoption, supporting Baby Sunscreen's market expansion.

Top players in Middle East and Africa Baby Sunscreens

- Johnson & Johnson

- Nivea

- Aveeno

- Baby Dove

- Mustela

- La Roche-Posay

- Bioderma

- Sebamed

- Cetaphil

- Himalaya

- Chicco

- Eucerin

- Pigeon

- A-Derma

Market Leaders

Johnson & Johnson

- Holds 18% regional market share

- Leading chemical-based sunscreen formulations for infants

- Strong online and offline distribution networks across Saudi Arabia and UAE

- Continuous innovation in SPF 50 variants, with 20% new product introduction annually

- Positions Johnson & Johnson as a strategic leader in Middle East and Africa Baby Sunscreens market

Nivea

- 15% regional market share

- Focus on mineral and hybrid formulations with hypoallergenic claims

- Wide adoption in UAE, Turkey, and Egypt, covering 40% of regional demand

- Technology enhancements improved SPF retention by 12%

- Positioned as a premium and trusted brand in the Baby Sunscreens market

Investment Analysis

The Middle East and Africa baby sunscreen market attracts substantial investment across manufacturing, R&D, and distribution sectors. In 2025, 42% of total investments were allocated to production expansion, with 28% dedicated to technology adoption, including nanofiltration and eco-friendly packaging. Regional investment is concentrated in Saudi Arabia (28%), UAE (16%), and Turkey (18%). M&A activity has increased by 12% in the past two years, emphasizing strategic consolidation, particularly in mineral formulation startups. Collaborative partnerships between pediatric dermatology clinics and manufacturers contribute to 63% of clinical product investments. Investment in online retail channels has risen by 15%, driven by consumer preference for convenience and transparency, ensuring sustained baby sunscreen market growth.

New Product Developments

Approximately 22% of baby sunscreen products launched in 2025 featured performance improvements in SPF stability and hypoallergenic properties. Innovations include hybrid formulations combining mineral and chemical filters with microencapsulation, enhancing skin safety by 18% and UV protection by 12%. Eco-conscious packaging has seen 30% adoption, and new SPF 70 variants represent 8% of product launches. These developments reflect the ongoing baby sunscreen market trend of premium, technology-driven product offerings, positioning manufacturers for competitive advantage.

Recent Developments in Middle East and Africa Baby Sunscreens

- 2026: Johnson & Johnson launched SPF 70 mineral baby sunscreen, increasing production volume by 15% and capturing 18% market share

- 2025: Nivea introduced hybrid formulations, leading to a 12% adoption increase and 10 million units added to production

Research Methodology

The research process for the Middle East and Africa baby-sunscreen market involves a combination of primary and secondary research. Primary research includes interviews with manufacturers, distributors, and pediatric dermatologists to gather insights on production volumes, technology adoption, and consumer behavior. Secondary research comprises analysis of company reports, government databases, trade journals, and industry publications to validate market size, segmentation, and regional distribution.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Consumer Behavior and Premium Product Segments

Mandy Davis is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.