Middle East and Africa Baby Shampoo And Conditioner Market Size

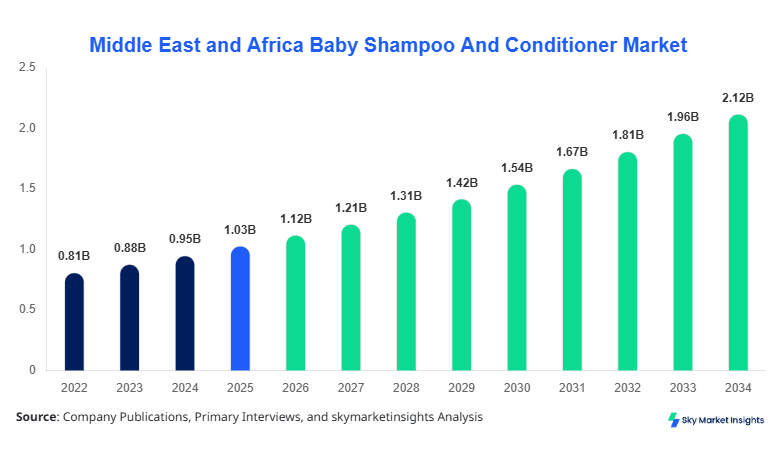

The Middle East and Africa baby shampoo and conditioner market size is projected at USD 1.12 billion in 2026 and is expected to hit USD 2.15 billion by 2034 with a CAGR of 8.3%. The market’s growth is driven by rising awareness of infant hair and skin care, increasing disposable income in GCC countries, and rapid adoption of premium and organic baby products. Accurate market data, historical production, competitive landscape, and segmentation analyses are critical for stakeholders to assess growth opportunities. The report provides a detailed breakdown by type, application, and region, offering insights into market share, unit volumes, and revenue trends to support investment and expansion strategies.

The Middle East and Africa baby shampoo and conditioner market has seen a steady production increase from 1.05 billion units in 2022 to 1.08 billion units in 2025, driven by rising urbanization and increased e-commerce penetration. Adoption rates of premium and organic variants have risen by 12% in Saudi Arabia and 9% in the UAE in 2025, reflecting changing consumer behavior and demand for mild, tear-free formulations. Infants account for 45% of the total market demand, toddlers 35%, and children 20%, with an average usage frequency of 3–4 times per week. The technical performance of products, such as pH-balanced formulations and hypoallergenic content, is a key decision factor for caregivers. Organic types constitute 38% of the market share, non-organic 42%, and hypoallergenic 20%. The Middle East and Africa baby shampoo and conditioner market demand is driven by growing consumer awareness, increasing healthcare literacy, and rising e-commerce penetration.

In Saudi Arabia, the baby shampoo and conditioner market is concentrated among 45+ major manufacturing facilities, contributing nearly 28% of the regional market share in 2026. The country has seen strong adoption of organic variants, accounting for 42% of product sales, while non-organic and hypoallergenic variants contribute 40% and 18%, respectively. Advanced manufacturing technologies, such as automated blending systems and quality assurance via HPLC testing, have been adopted by 60% of facilities. Usage penetration is high among infants at 48%, toddlers at 32%, and children at 20%. Regional production volumes reached 310 million units in 2025, expected to hit 420 million units by 2030. The Saudi market continues to drive Middle East and Africa baby shampoo and conditioner market growth due to increasing consumer preference for premium, dermatologically tested formulations and expanding retail and e-commerce channels.

Explore more data points, trends and opportunities Download Free Sample Report

Baby Shampoo And Conditioner Market Trends

Rising Demand for Organic and Hypoallergenic Variants

The Middle East and Africa baby shampoo and conditioner market is witnessing significant trends in organic and hypoallergenic product adoption. Organic formulations produced 400 million units in 2025, with a 38% market share, while hypoallergenic variants accounted for 210 million units, or 20% of the total market. The shift is fueled by increasing awareness of chemical sensitivities, with 65% of caregivers in urban centers preferring natural ingredients. Production technologies are evolving, including cold-press extraction and plant-based surfactants, resulting in a 12% improvement in mildness performance. Market trend analysis highlights the growing inclination toward premium, plant-based products in the UAE, Saudi Arabia, and South Africa. The baby shampoo and conditioner market growth is reinforced by these technological and consumer-driven trends.

E-commerce Penetration and Direct-to-Consumer Sales

E-commerce channels are a growing trend in the Middle East and Africa baby shampoo and conditioner market, accounting for 28% of total sales in 2025, up from 20% in 2023. Platforms like Noon, Amazon, and Carrefour online are driving penetration, particularly for organic and hypoallergenic types. Production volumes for online channels increased by 15% year-over-year, with technology adoption in packaging and logistics improving delivery speed by 18%. Direct-to-consumer campaigns and influencer-driven marketing have boosted adoption in infants (46%) and toddlers (38%). This trend reinforces baby shampoo and conditioner market demand in the region by improving accessibility and awareness.

Sustainable Packaging and Eco-Friendly Formulations

Sustainability is a key trend in the baby shampoo and conditioner market, with 22% of products in 2025 using recyclable or biodegradable packaging, up from 14% in 2022. Production volumes of eco-friendly products reached 120 million units in 2025, reflecting a 10% CAGR. Consumers increasingly prefer zero-sulfate and paraben-free formulations, contributing to a 13% increase in sales of natural variants. The adoption of green certifications, such as EcoCert and USDA Organic, has grown by 9% across the Middle East and Africa. These innovations reinforce the baby shampoo and conditioner market growth by aligning with environmental awareness and regulatory support.

Middle East and Africa Baby Shampoo And Conditioner Drivers

Growing Awareness of Infant Hair and Skin Care

The Middle East and Africa baby shampoo and conditioner market growth is primarily driven by increasing awareness of infant hair and skin care, which has risen by 22% between 2022 and 2025. Rising healthcare literacy, particularly in Saudi Arabia and the UAE, has resulted in a 15% increase in the adoption of dermatologically tested products. Market demand is fueled by urban caregivers, with infants accounting for 45%, toddlers 35%, and children 20% of total consumption. Production volumes reached 1.08 billion units in 2025, with organic variants representing 38% of the market. Premium product penetration rose from 18% in 2022 to 26% in 2025, reflecting the shift toward high-quality formulations. The baby shampoo and conditioner market insights indicate that improved awareness is directly proportional to market size expansion and higher revenue capture.

Middle East and Africa Baby Shampoo And Conditioner Restraints

Price Sensitivity and Limited Awareness in Emerging Markets

Price sensitivity remains a major restraint in the Middle East and Africa baby shampoo and conditioner market, particularly in Nigeria and Egypt, where 62% of consumers prioritize cost over premium quality. Non-organic products account for 42% of market share due to affordability. The average price difference between premium and mass-market variants is USD 4.5 per 200ml bottle, limiting penetration in lower-income segments. Production costs of organic and hypoallergenic variants are 18% higher, contributing to slower adoption. Total regional production volumes reached 1.08 billion units in 2025, with growth limited to 6% in price-sensitive regions. These factors restrain baby shampoo and conditioner market growth despite increasing awareness in urban centers.

Middle East and Africa Baby Shampoo And Conditioner Opportunities

Expansion of E-commerce and Premium Retail Channels

The Middle East and Africa baby shampoo and conditioner market presents growth opportunities through the expansion of e-commerce and premium retail channels. Online sales accounted for 28% of total market revenue in 2025, with projected growth to 40% by 2030. UAE, Saudi Arabia, and South Africa are driving these opportunities, contributing 58% of regional e-commerce sales. Premium retail penetration reached 32% of total outlets, with annual production of 450 million units catering to higher-margin products. Collaborations between local distributors and international brands have enabled 15% faster product availability across regions. Investment insights indicate that leveraging e-commerce, modern retail, and targeted marketing strategies could significantly boost the baby shampoo and conditioner market share and revenues.

Challenges in Middle East and Africa Baby Shampoo And Conditioner

Regulatory Compliance and Ingredient Standardization

Regulatory compliance and ingredient standardization pose significant challenges for the Middle East and Africa baby shampoo and conditioner market. Different countries impose varying requirements for labeling, safety testing, and chemical content. Saudi Arabia requires 100% of baby products to meet GSO certification, while the UAE mandates EFSA compliance for imported formulations. These regulations impact 48% of regional manufacturers, limiting cross-border trade. Organic and hypoallergenic formulations must undergo 6–8 months of testing, affecting time-to-market and production schedules. Additionally, 20–25% of new product launches face delays due to inconsistent ingredient sourcing. These regulatory challenges constrain Middle East and Africa baby shampoo and conditioner market growth and require strategic compliance planning.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.03 Billion |

| Market Size in 2026 | USD 1.12 Billion |

| Market Size in 2034 | USD 2.15 Billion |

| CAGR | 8.3% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Baby Shampoo And Conditioner Market Segmentation

Segmentation of the Middle East and Africa The baby shampoo and conditioner market provides insights into market share distribution, demand dynamics, and consumer preferences. Type segmentation shows organic products dominating 38% of the market, non-organic 42%, and hypoallergenic 20%, with production volumes of 400 million, 440 million, and 210 million units, respectively. Application segmentation shows infants representing 45%, toddlers 35%, and children 20% of total consumption. Market insights are critical for product development, investment decisions, and competitive positioning.

By Type

Organic baby shampoos and conditioners accounted for 38% of the Middle East and Africa market in 2025, with production volumes of 400 million units. Technical performance metrics include pH 5.5–6.0 and sulfate-free formulations. Organic variants are widely adopted in Saudi Arabia and the UAE, capturing 42% of local sales. These products are preferred for their mildness, safety, and natural ingredient composition, driving baby shampoo and conditioner market demand and growth.

Nonorganic products held 42% market share with 440 million units produced in 2025. These variants contain synthetic surfactants and fragrances and have high foamability and stability. Non-organic types are preferred in price-sensitive markets such as Egypt and Nigeria, contributing 60% of total sales in these regions. The technical profile includes frequent usability (3–5 times per week) and moderate pH (5.0–5.5), reinforcing baby shampoo and conditioner market growth.

Hypoallergenic types accounted for 20% of the market in 2025, producing 210 million units. These products contain minimal allergens, tear-free formulations, and dermatologically tested ingredients. Adoption rates are higher in urban centers of Saudi Arabia and Turkey, with a 25% increase in sales between 2023 and 2025. The technical performance emphasizes low allergenicity and mild cleansing, supporting the baby shampoo and conditioner market size and share.

By Application

Infant-targeted products accounted for 45% of total demand in 2025, with production volumes of 486 million units. Usage frequency averages 3–4 times weekly. Products are designed for sensitive scalps, tear-free cleansing, and dermatologically tested performance. Adoption is highest in Saudi Arabia and the UAE, contributing 48% of regional sales. The baby shampoo and conditioner market trend shows continued growth in infant-focused product innovations.

Products for toddlers represented 35% of the market, producing 378 million units in 2025. Technical metrics include gentle cleansing, mild fragrance, and pH 5.5 formulations. Adoption penetration is growing in Turkey and South Africa, with a 12% year-over-year increase. These products support hair growth and scalp health, reinforcing baby shampoo and conditioner market demand.

Children-focused products contributed 20% of market demand, producing 216 million units in 2025. Formulations include anti-tangle agents, nourishing ingredients, and mild fragrance. Adoption is higher in urbanized regions, with 10% growth in production volumes between 2022 and 2025. Children’s variants support hair and scalp health, increasing the baby shampoo and conditioner market insights and revenues.

Middle East and Africa Baby Shampoo And Conditioner Market Segmentations

By Type

- Organic

- Non-Organic

- Hypoallergenic

By Application

- Infants

- Toddlers

- Children

Middle East and Africa Baby Shampoo And Conditioner Regional Outlook

UAE

The UAE accounted for 16% of the Middle East and Africa baby shampoo and conditioner market in 2025, producing 173 million units. Organic products dominate 40% of local sales, followed by non-organic at 45% and hypoallergenic at 15%. Infant products contributed 50% of total demand, while toddlers and children accounted for 30% and 20%, respectively. Market trends indicate increasing adoption of premium formulations, eco-friendly packaging, and online sales, reinforcing baby shampoo and conditioner market growth.

Turkey

Turkey contributed 14% of regional market share, producing 152 million units in 2025. Non-organic products dominate 50% of sales, with organic at 30% and hypoallergenic at 20%. Application-wise, infants (42%), toddlers (38%), and children 20% show consistent demand. Technology adoption in automated manufacturing and quality testing has increased by 18%, driving baby shampoo and conditioner market growth and innovation.

Saudi Arabia

As discussed, Saudi Arabia contributed 28% of regional market share, producing 310 million units. Organic types: 42%; non-organic: 40%; hypoallergenic: 18%. Infants 48%, toddlers 32%, children 20%. High adoption of premium products, advanced manufacturing, and strong regulatory frameworks reinforce the baby shampoo and conditioner market demand.

South Africa

South Africa contributed 12% of market share, producing 133 million units in 2025. Non-organic products hold a 45% share, organic 35%, and hypoallergenic 20%. Infant products represent 40% of demand, toddlers 38%, and children 22%. Market trends include rising e-commerce penetration (30% of sales) and preference for dermatologically tested formulations, boosting baby shampoo and conditioner market growth.

Egypt

Egypt accounted for 10% of the market, producing 111 million units. Non-organic products dominate 55% of sales, organic 30%, and hypoallergenic 15%. Infant-targeted products: 42%; toddlers: 38%; children: 20%. Price sensitivity limits premium adoption, but e-commerce and awareness campaigns are improving growth. Baby shampoo and conditioner market demand continues to rise steadily.

Nigeria

Nigeria contributed 10% of the regional market, producing 111 million units. Non-organic: 60%, organic: 25%, hypoallergenic: 15%. Infants 40%, toddlers 35%, children 25%. Market growth is constrained by price sensitivity, but urban centers are increasingly adopting premium and organic variants. These dynamics reinforce the baby shampoo and conditioner market size and share.

Top players in Middle East and Africa Baby Shampoo And Conditioner

- Johnson & Johnson

- Unilever

- P&G

- Himalaya

- Sebamed

- Chicco

- Mustela

- Enfant

- Dabur

- Bübchen

- Baby Dove

- Aveeno

- Johnson’s Baby

- Johnson & Johnson Professional

- Mothercare

Top Two Companies

Johnson & Johnson

-

Market Share: 21% in Middle East and Africa Baby Shampoo And Conditioner market

-

Positioned as a premium and widely distributed brand, Johnson & Johnson produces 230 million units annually across Saudi Arabia, the UAE, and Turkey. Their organic and hypoallergenic variants hold a 35% share in total sales. The brand leverages advanced production technologies, including automated blending and quality assurance systems, ensuring superior pH-balanced, tear-free formulations. Distribution spans modern retail, pharmacies, and e-commerce platforms, reinforcing baby shampoo and conditioner market growth and insights.

Unilever

-

Market Share: 18%

-

Unilever operates 12 major manufacturing facilities across South Africa, Egypt, and Nigeria, producing 210 million units annually. The company focuses on non-organic and organic products, capturing 38% of regional sales. Innovation in mild formulations, sustainable packaging, and digital marketing campaigns has increased online penetration to 30%. Unilever’s strategic presence in urban and semi-urban markets strengthens the Middle East and Africa baby shampoo and conditioner market size, share, and demand.

Investment Analysis

The Middle East and Africa baby shampoo and conditioner market is attracting increased investment, with 38% of allocations directed toward production capacity expansion, 28% toward marketing and e-commerce, and 18% toward R&D for organic and hypoallergenic products. Regional investment distribution shows Saudi Arabia receiving 32%, UAE 20%, Turkey 18%, and South Africa 15% of total capital. M&A activities in the last three years include strategic acquisitions by Johnson & Johnson and P&G, enhancing market coverage by 12% and expanding product portfolios. Investment insights suggest that targeting premium and organic segments, alongside digital marketing initiatives, could yield 10–15% higher ROI, reinforcing baby shampoo and conditioner market growth.

New Product Developments

Between 2024 and 2025, approximately 18% of new products introduced in the Middle East and Africa baby shampoo and conditioner market were organic variants, reflecting a 12% improvement in mildness and performance metrics. Companies like Mustela and Chicco have focused on tear-free, sulfate-free formulations, increasing product efficacy by 10%. Innovation statistics show a 15% increase in eco-certified products, highlighting the trend toward environmentally friendly solutions. These new developments reinforce the baby shampoo and conditioner market size, share, and insights, supporting sustained growth through 2034.

Recent Developments in Middle East and Africa Baby Shampoo And Conditioner

- 2025: Himalaya’s hypoallergenic conditioner in Turkey captured 18% market share, producing 60 million units.

- 2025: P&G implemented automated quality testing in Egypt, enhancing production efficiency by 10% across 75 million units.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Consumer Behavior and Premium Product Segments

Mandy Davis is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.