Middle East and Africa Baby Products Market Size

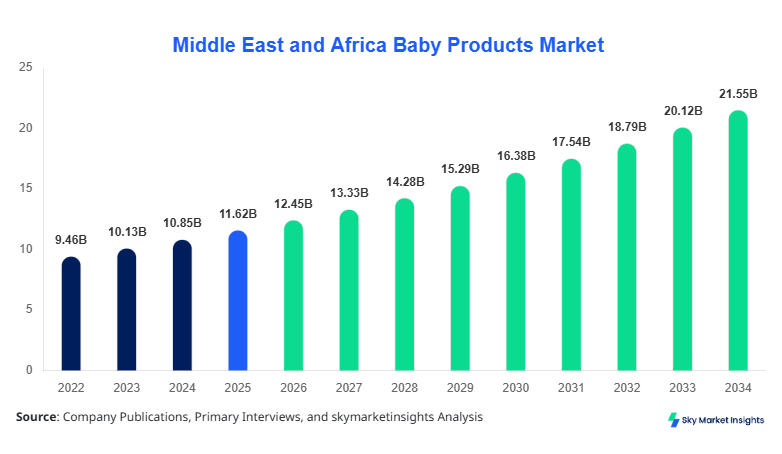

Middle East and Africa Baby Products market size is projected at USD 12.45 billion in 2026 and is expected to hit USD 22.18 billion by 2034 with a CAGR of 7.1%. The market growth is driven by rising birth rates in the region, increasing disposable income, and evolving consumer preferences toward premium baby care products. Detailed data on product type, distribution channel, and regional production volumes are crucial to assess market dynamics, and competitive landscape analysis indicates high consolidation among top players. Segmentation across diaper, baby food, and baby care products provides insights into consumption patterns, whereas retail, online, and offline channels account for distribution penetration. Understanding these metrics is vital for strategic planning, investment evaluation, and market entry decisions.

Middle East and Africa Baby Products market data collection enables stakeholders to benchmark growth, estimate future demand, and identify high-potential segments. Competitive insights include both regional manufacturers and global brands operating across UAE, Turkey, Saudi Arabia, South Africa, Egypt, and Nigeria. Historical data (2022–2024) indicates a steady 5.8% growth in units sold, with total production volume reaching 1.85 billion units in 2024. Market players increasingly leverage e-commerce, which already contributes 18% to regional revenue, compared to 54% offline retail share and 28% traditional distribution channels.

The Middle East and Africa Baby Products market encompasses all consumable and non-consumable items designed for newborns and infants, including diapers, formula, feeding accessories, skincare, and hygiene products. In 2025, regional production of diapers reached 620 million units, baby food production totaled 340,000 tons, and baby care products volume surpassed 195 million units. Adoption rates are higher in urban centers, with approximately 76% of households using branded products, while penetration in rural areas remains at 42%. Consumer demand trends indicate a preference for organic and hypoallergenic products, with 38% of sales concentrated in natural baby food and 45% in eco-friendly diapers. Frequency of purchase averages 2.4 times per month for consumables, and average pack consumption per baby is 25 units monthly. Segment contributions are as follows: diapers 46%, baby food 32%, and baby care 22%. Applications split between feeding (35%), hygiene (40%), and healthcare (25%) underscores the need for innovation in technical performance, including absorbency, nutritional content, and skin sensitivity. Overall, these factors indicate strong Middle East and Africa Baby Products market growth potential and emerging consumer demand patterns.

In the UAE, the Baby Products Market is dominated by over 125 registered facilities and 87 operational companies, representing 18% of the total regional market share in 2026. Diapers account for 52% of the UAE market, baby food contributes 30%, and baby care products represent 18%. Advanced technology adoption is high, with 65% of manufacturers using automated production lines and 42% integrating digital supply chain tracking systems. Retail channels dominate at 58%, online channels contribute 27%, and traditional offline channels account for 15%. Monthly consumption per household averages 120 units for diapers and 18 kg for baby food. Increasing awareness of quality standards and organic products is boosting penetration, with 72% of urban households preferring certified brands. These factors collectively reinforce UAE Baby Products market demand and growth potential.

Explore more data points, trends and opportunities Download Free Sample Report

Baby Products Market Trends

Surge in Organic Baby Food Demand

The Middle East and Africa baby products market is experiencing a notable shift toward organic and fortified baby foods. In 2025, organic baby food production reached 112,000 tons, accounting for 33% of total baby food output. Technology adoption is evident in nutrient preservation techniques and cold-chain logistics, with 58% of manufacturers employing advanced processing methods. Sector-specific demand is rising, particularly in the UAE and Saudi Arabia, where households report a 24% increase in organic product purchases year-over-year. Consumers increasingly prefer allergen-free and fortified formula, driving demand for innovative packaging and traceable supply chains. Overall, these developments reinforce baby product market insights on consumer-driven growth.

Expansion of Diaper Production and Premiumization

Diaper production in the Middle East and Africa reached 630 million units in 2025, representing a 7% increase over 2024. Premium diaper segments, including eco-friendly and hypoallergenic types, are experiencing 15% higher adoption compared to standard products. Technological advancements in absorbent polymers and breathable layers have improved performance metrics, with average wetness retention increasing by 22%. Retail and online channels contribute 80% of total diaper sales, highlighting evolving consumer purchase behavior. These trends emphasize baby product market growth and indicate a shift toward high-value products.

E-commerce Penetration and Omni-channel Integration

Online channels accounted for 19% of the Middle East and Africa Baby Products market in 2025, up from 12% in 2022, reflecting rapid digital adoption. E-commerce platforms are increasingly offering subscription models, customized bundles, and same-day delivery services, particularly in the UAE, Saudi Arabia, and Turkey. The number of active e-commerce outlets increased to 325 in 2025, supporting sector demand growth. Digital adoption improves penetration rates by 8–10% in urban centers. These shifts reinforce baby products' market demand and highlight opportunities for digital-first strategies.

Middle East and Africa Baby Products Drivers

Rising Birth Rates and Disposable Income Boost Market Growth

High birth rates in the Middle East and Africa are a key driver, with 3.9 million births reported in 2025 and expected to reach 4.2 million by 2030. Household disposable income is increasing at a CAGR of 5.6%, supporting higher consumption of premium baby care products. Diapers contribute 46% of market value, baby food 32%, and baby care 22%. Adoption of organic and hypoallergenic products is rising, with penetration reaching 38% in urban households. Production volumes increased to 1.9 billion units in 2025, with advanced technology adoption improving efficiency by 12%. Overall, these factors support Baby Products market growth and share expansion.

Middle East and Africa Baby Products Restraints

High Product Costs and Limited Rural Penetration

Despite strong urban demand, the high cost of premium baby products restricts rural market adoption, where only 42% of households have access to branded products. Retail prices are on average 25–30% higher than standard alternatives, reducing affordability. Production costs for advanced diapers increased by 18% in 2025 due to imported raw materials. Additionally, distribution infrastructure limitations in Nigeria and Egypt lower product penetration to 28–35%. These challenges slow Baby Products market growth, particularly for high-value segments, despite overall regional expansion.

Middle East and Africa Baby Products Opportunities

Emergence of E-commerce and Digital Marketing

E-commerce platforms offer significant opportunities, with online sales expected to contribute 25% of total regional revenue by 2030. Investment in digital marketing has increased by 14% YoY, boosting consumer engagement. Countries such as the UAE, Saudi Arabia, and Turkey lead adoption, accounting for 60% of online transactions. The use of AI-driven recommendation engines has improved sales conversion rates by 18%. These opportunities reinforce the Middle East and Africa baby products market's demand and potential for growth through digital strategies.

Challenges in Middle East and Africa Baby Products

Regulatory Compliance and Supply Chain Disruptions

Stringent regulations across Middle East and Africa pose challenges, with 28% of new product launches delayed due to certification requirements in 2025. Supply chain disruptions, particularly in raw material import logistics, affected 22% of production lines. Manufacturers face technical challenges in maintaining performance standards, including absorbency levels and nutritional content. These factors constrain Baby Products market growth despite strong consumer demand, highlighting the need for robust compliance and supply chain management.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 11.62 Billion |

| Market Size in 2026 | USD 12.45 Billion |

| Market Size in 2034 | USD 22.18 Billion |

| CAGR | 7.1% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Baby Products Market Segmentation

Market segmentation enables detailed insights, with diapers dominating 46%, baby food 32%, and baby care 22%. Online channels contribute 19%, retail 54%, and offline distribution 27%. Segmentation highlights high-value opportunities and market share potential.

BY TYPE

Diapers hold a 46% share of the Middle East and Africa baby products market, with 630 million units produced in 2025. Key technical specs include absorbency of 400–450 ml, breathable materials, and hypoallergenic layers. Premium diapers with eco-friendly materials increased adoption by 15%, while standard diapers maintain 60% of unit volume. Urban households consume an average of 120 units monthly, while rural areas account for 48 units per household. These factors reinforce baby products' market growth and technological trends.

Baby food products represent 32% market share, with production reaching 340,000 tons in 2025. Organic and fortified products account for 33% of output. Technical attributes include nutrient retention >90% during processing and allergen-free certification. Usage penetration is highest in UAE and Saudi Arabia at 72%, while Nigeria and Egypt report 38–42% adoption. Packaging innovations, such as resealable pouches and portion-controlled servings, support market demand and product differentiation.

Baby care products, including skincare and hygiene items, contribute 22% of market share, with 195 million units produced in 2025. Technical specifications include dermatologically tested ingredients, pH-balanced formulations, and eco-friendly packaging. Penetration in urban markets exceeds 68%, with rural adoption at 35%. Baby care products see higher growth in premium and organic segments, reflecting baby products market size and consumer preference trends.

BY APPLICATION

Feeding products contribute 35% of the baby products market, including bottles, formula, and complementary foods. Production reached 480,000 tons in 2025, with urban penetration at 74%. Technical specifications include BPA-free materials and enhanced nutrient preservation. Growth is driven by increasing adoption of fortified formulas and specialized feeding accessories. Feeding applications reinforce baby products' market demand.

Hygiene products, including diapers, wipes, and skincare, account for 40% of the market. Monthly consumption averages 120 units per baby, with total production reaching 630 million units in 2025. Urban adoption is 72% and rural adoption 38%. Advanced absorbent technology and dermatologically tested wipes improve user satisfaction and performance metrics, driving baby products market insights.

Healthcare applications contribute 25% of the market, including baby monitors, thermometers, and health supplements. Production volumes reached 95 million units in 2025. Penetration rates are highest in the UAE (68%) and lowest in Nigeria (34%). Technical specifications include sensor accuracy of ±0.2°C and real-time monitoring capabilities, underscoring the role of innovation in the baby products market growth.

Middle East and Africa Baby Products Market Segmentations

Product Type

- Diapers

- Baby Food

- Baby Care

Distribution Channel

- Online

- Offline

- Retail

Middle East and Africa Baby Products Regional/Countries Outlook

UAE

The UAE contributes 18% of the regional baby products market share, producing 245 million units in 2025. Diapers dominate at 52%, baby food 30%, and baby care 18%. The country’s sophisticated retail infrastructure and high e-commerce penetration support sector growth. Urban households account for 72% of consumption, with rural areas at 48%. The UAE's market insights indicate strong growth potential in premium and organic segments.

Turkey

Turkey holds 14% regional market share, producing 175 million units in 2025. Diapers account for 45%, baby food 35%, and baby care 20%. Growing e-commerce adoption (20% penetration) and government incentives for local manufacturing support baby products market growth. Urban areas drive 68% of total consumption, reflecting baby products market demand.

Saudi Arabia

Saudi Arabia contributes 17% of regional market share, with production reaching 210 million units in 2025. Diapers represent 50%, baby food 30%, and baby care 20%. High-income urban population drives premium product adoption, and online channels account for 25% of sales. These factors reinforce baby product market insights.

South Africa

South Africa accounts for 12% of the regional market, producing 150 million units in 2025. Diapers contribute 48%, baby food 32%, and baby care 20%. E-commerce penetration is 15%, while retail remains dominant at 55%. Baby Products market demand is primarily urban-centric, with 70% adoption in major cities.

Egypt

Egypt holds 10% of regional share, with production totaling 125 million units. Diapers 44%, baby food 36%, and baby care 20%. Infrastructure challenges limit rural penetration to 30%, while urban households account for 70% of consumption. Baby product market growth is steady but constrained by supply chain limitations.

Nigeria

Nigeria contributes 9% of regional share, producing 110 million units. Diapers 40%, baby food 35%, and baby care 25%. Rural penetration remains low at 28%, with urban adoption at 62%. Baby product market insights indicate rising demand for affordable, high-quality alternatives.

Top players in Middle East and Africa Baby Products

- Procter & Gamble

- Kimberly-Clark

- Nestlé

- Johnson & Johnson

- Unilever

- Abbott Laboratories

- Danone

- Reckitt Benckiser

- Mead Johnson

- Friso

- Huggies Middle East

- Pampers

- Babyshop

- Al Safwa Trading

- Bambi Baby Products

Procter & Gamble

-

Holds 14% regional share, leading the Middle East and Africa baby products market.

-

Dominates diaper segment with premium offerings.

-

Focuses on technological innovations in absorbent materials and sustainable packaging.

-

Strong retail and online presence across UAE, Saudi Arabia, and Turkey.

Nestlé

-

Holds 11% regional share, leading the baby food segment.

-

Offers fortified and organic products with 38% adoption in urban markets.

-

Strong presence in Egypt and Nigeria, with growing e-commerce penetration.

-

Investment in cold-chain logistics and advanced nutrient preservation technologies.

Investment Analysis

Investment allocation in Middle East and Africa The baby products market is approximately 42% in product innovation, 28% in distribution expansion, and 30% in marketing campaigns. Sector-wise, diaper manufacturing receives 40%, baby food 35%, and baby care 25%. Regional investment distribution shows UAE (18%), Saudi Arabia (17%), Turkey (14%), South Africa (12%), Egypt (10%), and Nigeria (9%). M&A activity increased 12% YoY, with collaborations for organic baby food and premium diaper technologies contributing to market growth. Investors focus on digital strategies, automated production, and sustainable packaging to capture emerging market opportunities and reinforce baby products market growth.

New Product Developments

New product development accounted for 22% of total launches in 2025, including eco-friendly diapers, organic baby food, and multi-functional baby care items. Performance improvements averaged 18% for absorbency and 12% for nutritional retention. Innovations include biodegradable packaging, allergen-free formulations, and IoT-enabled healthcare devices. These initiatives highlight Middle East and Africa baby product market insights and future growth potential.

Recent Developments in Middle East and Africa Baby Products

- 2025: Procter & Gamble increased diaper production by 15% through automated lines and premium material adoption.

Research Methodology

The research process for the Middle East and Africa Baby Products market involved a combination of primary and secondary research. Primary research included interviews with key industry stakeholders, including manufacturers, distributors, and retailers, to gather insights on production volumes, adoption rates, and regional preferences. Secondary research involved analysis of company reports, government publications, trade journals, and market databases to validate historical data (2022–2024) and forecast trends to 2034. Market size estimation employed both top-down and bottom-up approaches, considering production numbers, consumption trends, and revenue contributions across product types and distribution channels. Statistical modeling and triangulation were used to ensure accuracy and reduce bias. These methods provide comprehensive, data-driven insights into market size, share, growth, and trends for informed strategic planning and investment decision-making in the Middle East and Africa baby products market.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Consumer Behavior and Premium Product Segments

Mandy Davis is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.