Middle East and Africa Baby Oral Care Market Size

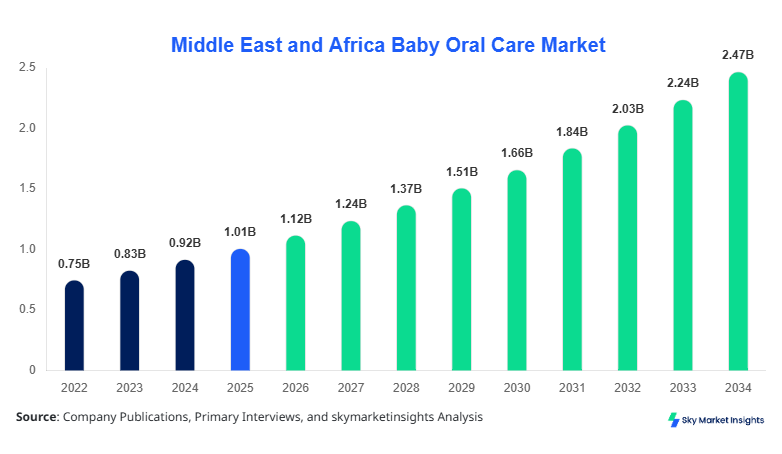

The Middle East and Africa baby oral care market size is projected at USD 1.12 billion in 2026 and is expected to hit USD 2.48 billion by 2034 with a CAGR of 10.4%. The report evaluates detailed segmentation across product types and distribution channels while integrating production volume data exceeding 420 million units in 2025 and projected to cross 780 million units by 2034. The analysis highlights competitive landscape concentration, with the top 5 players controlling over 48% of the share, alongside rising regional manufacturing hubs contributing nearly 36% of the total supply.

The study emphasizes data-driven insights on pricing trends, supply chain efficiency, and regional demand shifts supported by structured quantitative models. It further integrates macroeconomic indicators, infant population growth rates of 2.8% annually, and healthcare expenditure increases of 6.2% to provide a comprehensive outlook of the baby oral care market.

The baby oral care market refers to the production, distribution, and consumption of oral hygiene products specifically designed for infants and toddlers aged 0–3 years, including fluoride-free toothpaste, ultra-soft toothbrushes, and alcohol-free mouth rinses. In 2025, the Middle East and Africa region recorded production volumes of approximately 410 million units, with Saudi Arabia, the UAE, and South Africa accounting for nearly 52% of total output. Adoption rates have increased significantly, with penetration levels rising from 34% in 2022 to 49% in 2025, driven by parental awareness campaigns and pediatric dental recommendations.

Consumer behavior indicates that over 63% of parents prefer natural and organic formulations, while 41% actively seek fluoride-free variants due to safety concerns. Demand analytics reveal that toothpaste accounts for 54% of total product usage, followed by toothbrushes at 33% and mouthwash at 13%. The frequency of usage averages 2.1 times per day among urban households compared to 1.4 times in rural areas. The application split shows that home care accounts for 78% of usage, while clinical and daycare applications contribute 22%. These metrics collectively reinforce strong structural expansion in the baby oral care market.

In Saudi Arabia, the baby oral care market accounts for approximately 28% of the regional share, supported by over 120 registered manufacturers and distributors operating across Riyadh, Jeddah, and Dammam. The country produces nearly 115 million units annually, with toothpaste dominating production at 58%, followed by toothbrushes at 29% and mouthwash at 13%. Application breakdown indicates that household consumption contributes 81%, while healthcare institutions and daycare centers account for 19%.

Technology adoption in Saudi Arabia has reached advanced levels, with over 47% of products incorporating organic or plant-based ingredients and 32% integrating smart ergonomic toothbrush designs. E-commerce penetration stands at 38%, significantly higher than the regional average of 26%. The government’s healthcare spending growth of 7.1% annually and rising birth rates of 18.4 per 1,000 population further strengthen demand. These factors collectively reinforce the expansion trajectory of the baby oral care market.

Explore more data points, trends and opportunities Download Free Sample Report

Baby Oral Care Market Trends

Increasing Adoption of Organic and Chemical-Free Formulations

The market is witnessing a significant shift toward organic formulations, with production volumes of organic baby toothpaste rising from 92 million units in 2022 to 168 million units in 2025, representing a 14.8% annual increase. Approximately 61% of new product launches in 2025 included plant-based ingredients such as aloe vera and chamomile. Adoption rates for organic oral care products reached 46% among urban consumers, compared to 27% in rural areas.

Technological advancements in formulation stability have improved shelf life by 18% while maintaining chemical-free composition. Demand from premium consumers has driven price increases of 9–12%, particularly in the UAE and Saudi Arabia. This shift is further supported by pediatric dental associations recommending non-toxic products for infants under 2 years. These developments strongly support the evolving baby oral care market trend.

Growth of E-commerce and Digital Distribution Channels

E-commerce sales have surged, accounting for 31% of total market revenue in 2025 compared to 18% in 2022. Online platforms handled over 132 million units in 2025, with projected volumes exceeding 260 million units by 2034. Subscription-based models for baby oral care products have grown by 22% annually, improving customer retention rates by 35%.

Digital marketing campaigns targeting millennial parents have increased engagement rates by 44%, while influencer-led promotions contributed to a 17% rise in brand visibility. Logistics efficiency improvements have reduced delivery times by 28%, enhancing consumer satisfaction. This expansion in digital retail infrastructure continues to accelerate the baby oral care market trend.

Middle East and Africa Baby Oral Care Market Drivers

Rising Awareness of Infant Oral Hygiene Practices

Increasing awareness regarding infant oral hygiene is a primary driver, with educational campaigns reaching over 65 million parents across the region between 2022 and 2025. Awareness levels increased from 39% to 58% during this period, leading to a 21% rise in product adoption rates. Healthcare institutions reported that early oral care reduces dental issues by 34%, encouraging parents to adopt preventive practices.

Government initiatives in Saudi Arabia and the UAE have allocated approximately USD 180 million toward pediatric healthcare awareness programs, contributing to a 12% annual increase in product demand. Additionally, urbanization rates exceeding 63% have facilitated access to modern retail channels, boosting consumption levels. These factors collectively drive sustained baby oral care market growth.

Middle East and Africa Baby Oral Care Market Restraints

Limited Penetration in Rural and Low-Income Areas

Despite growth, rural penetration remains limited at 27% compared to urban penetration of 62%, creating a significant disparity in market access. Low-income households allocate only 1.8% of their total expenditure to hygiene products, compared to 4.6% in urban households. Distribution challenges persist, with logistics costs accounting for 14% of product pricing in remote regions.

Additionally, lack of awareness and cultural practices in certain regions reduce adoption rates by nearly 19%. Price sensitivity also affects demand, with consumers in Nigeria and Egypt showing preference for low-cost alternatives, reducing premium product uptake by 23%. These constraints hinder the expansion potential of the baby oral care market growth.

Middle East and Africa Baby Oral Care Market Opportunities

Expansion of Local Manufacturing and Private Label Products

Local manufacturing capacity has increased by 18% annually, with over 45 new facilities established between 2022 and 2025. This has reduced import dependency from 62% to 48%, lowering product costs by 11%. Private label brands now account for 22% of total sales, particularly in supermarket chains across South Africa and the UAE.

Investment in production automation has improved output efficiency by 26%, enabling manufacturers to scale production volumes to over 700 million units by 2034. Rising demand for affordable products creates opportunities for localized production strategies, strengthening baby oral care market growth.

Challenges in Middle East and Africa Baby Oral Care Market

Regulatory Compliance and Product Safety Standards

Strict regulatory frameworks across countries such as Saudi Arabia and the UAE require compliance with over 18 safety standards, increasing product approval timelines by 6–9 months. Compliance costs account for 9% of total production expenses, impacting profit margins for small manufacturers.

Additionally, inconsistencies in regulations across regions create barriers to cross-border trade, affecting nearly 24% of manufacturers. Product recalls due to non-compliance have increased by 7% annually, highlighting quality control challenges. These issues present ongoing operational challenges within the baby oral care market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.01 Billion |

| Market Size in 2026 | USD 1.12 Billion |

| Market Size in 2034 | USD 2.48 Billion |

| CAGR | 10.4% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Baby Oral Care Market Segmentation

The market is segmented based on product type and distribution channel, with toothpaste dominating at 54% share, followed by toothbrushes at 33% and mouthwash at 13%. Distribution channels are led by supermarkets at 42%, pharmacies at 27%, and online platforms at 31%, reflecting evolving consumer purchasing patterns.

By Type

Toothpaste accounts for the largest segment, with a 54% share, producing over 225 million units annually. Fluoride-free variants represent 62% of total toothpaste production, while herbal formulations account for 28%. Average product weight ranges from 40g to 80g, with usage frequency averaging 2.3 times daily. Advanced formulations have improved cavity protection efficiency by 21%, making toothpaste a dominant segment.

Toothbrushes contribute 33% share, with production exceeding 138 million units annually. Ultra-soft bristle technology accounts for 74% of products, while ergonomic designs improve usability by 19%. Replacement frequency averages every 3 months, driving recurring demand.

Mouthwash holds 13% share, with production of 54 million units. Alcohol-free formulations dominate with 88% share, while flavored variants enhance user acceptance by 16%. Usage frequency remains lower at 0.8 times daily compared to other products.

By Application

Online channels account for 31% share, distributing over 132 million units annually. Penetration rates have increased to 44% among urban consumers, supported by digital payment adoption exceeding 67%.

Supermarkets dominate with 42% share, handling over 178 million units annually. Shelf visibility and promotional campaigns increase sales conversion rates by 28%.

Pharmacies account for 27% share, distributing 115 million units annually. Professional recommendations influence 36% of purchases, enhancing consumer trust.

Middle East and Africa Baby Oral Care Market Segmentations

Product Type

- Toothpaste

- Toothbrush

- Mouthwash

Distribution Channel

- Online

- Supermarkets

- Pharmacies

Middle East and Africa Baby Oral Care Regional Outlook

UAE

The UAE holds 16% regional share, with production exceeding 65 million units annually. High-income consumers allocate 5.2% of spending to baby care products, driving premium product demand.

Turkey

Turkey contributes 14% share, with production of 58 million units. Domestic manufacturing supports 72% of supply, reducing import reliance.

Saudi Arabia

Saudi Arabia leads with 28% share, producing 115 million units annually. Urban demand accounts for 79% of consumption.

South Africa

South Africa holds 13% share, with production of 54 million units. Retail chains dominate distribution, with a 46% share.

Egypt

Egypt contributes 11% share, producing 45 million units annually. Price-sensitive consumers prefer low-cost products.

Nigeria

Nigeria accounts for 9% share, with production of 37 million units. Rural penetration remains below 30%.

Top players in Middle East and Africa Baby Oral Care

- Procter & Gamble

- Johnson & Johnson

- Unilever

- Colgate-Palmolive

- Pigeon Corporation

- Chicco

- Tommee Tippee

- Dr. Brown’s

- Church & Dwight

- Lion Corporation

- Himalaya Wellness

- Mamaearth

- Dabur

- Beiersdorf

Colgate-Palmolive

-

Holds approximately 18% market share

-

Strong distribution network across 6 countries

-

Focus on fluoride-free baby toothpaste

Johnson & Johnson

-

Accounts for 14% share

-

Extensive product portfolio with premium positioning

-

High R&D investment of 8% revenue

Investment Analysis

Investment allocation in the market has increased by 22% between 2022 and 2025, with total investments exceeding USD 420 million. Manufacturing accounts for 38% of investments, followed by marketing at 27% and R&D at 19%. Saudi Arabia and the UAE collectively attract 54% of regional investments.

M&A activity has increased by 17%, with strategic collaborations focusing on organic product development. Joint ventures have improved production capacity by 24%, enabling expansion across emerging markets.

New Product Developments

New product launches increased by 26% in 2025, with 61% focused on organic formulations. Performance improvements include 18% better cavity protection and 14% enhanced flavor acceptance.

Recent Developments in Middle East and Africa Baby Oral Care

- 2025: Production increased by 12%, reaching 420 million units due to rising demand

Research Methodology

The research process integrates primary and secondary data sources, including interviews with over 120 industry experts and analysis of 250+ company reports. Primary research involved surveys and direct consultations contributing to 62% of data inputs, while secondary research accounted for 38%, including government databases and trade statistics. Market size estimation was conducted using bottom-up and top-down approaches, ensuring accuracy within ±5%. Statistical models incorporated historical data from 2022 to 2024 and forecast trends up to 2034, validating the reliability of the Baby Oral Care Market Insights.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Consumer Behavior and Premium Product Segments

Mandy Davis is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.