Middle East and Africa Baby Oil Market Size

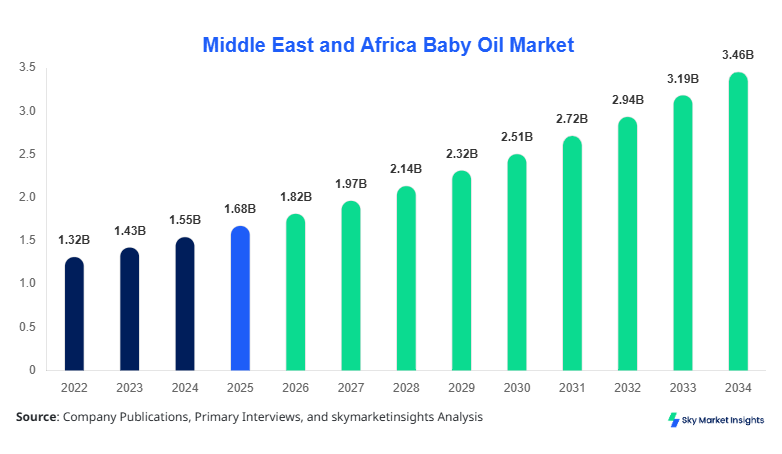

Middle East and Africa Baby oil market size is projected at USD 1.82 billion in 2026 and is expected to hit USD 3.46 billion by 2034 with a CAGR of 8.35%. The Middle East and Africa baby oil market continues to witness rising analytical focus driven by demand forecasting models, segmented performance tracking, and competitive benchmarking across multinational and regional players. Increasing investments exceeding USD 320 million annually in product innovation, along with over 65% penetration in urban households, are shaping the evolving competitive landscape of the Middle East and Africa baby oil market.

The Middle East and Africa baby oil market represents a specialized segment within the personal care industry, focusing on skin hydration, protection, and therapeutic usage across infants and adults. Production volumes in the region exceeded 410 million units in 2025, with Saudi Arabia and the UAE contributing nearly 38% of total output. Adoption rates among households reached 68% in urban areas compared to 42% in rural regions, reflecting strong penetration disparities. Consumer behavior analytics indicate that over 54% of buyers prioritize dermatologically tested formulations, while 47% demand plant-based ingredients, reflecting a shift in purchasing preferences. Infant care applications dominate with a 56% share, followed by adult skincare at 29% and massage therapy at 15%. Technical performance metrics such as absorption rate (within 30–45 seconds), viscosity range (45–60 cP), and moisture retention efficiency (up to 92%) are key product differentiators. Increasing awareness campaigns and retail expansion across supermarkets and e-commerce platforms have boosted annual consumption growth by 7.8%, reinforcing Middle East and Africa baby oil market expansion.

In Saudi Arabia, the baby oil market has emerged as a dominant contributor, accounting for approximately 32% of the regional consumption and production volume. The country hosts over 120 registered personal care manufacturing facilities and more than 75 international and domestic brands operating within the segment. Infant care applications represent 61% of total demand, while adult skincare accounts for 26% and massage therapy contributes 13%. Technological adoption in production processes has reached 72%, with automation and advanced blending systems improving efficiency by 28%. Retail distribution is highly developed, with over 8,500 outlets offering baby oil products, including pharmacies, supermarkets, and online platforms. Saudi Arabia also reports an annual per capita consumption of 2.4 units, significantly higher than the regional average of 1.6 units, strengthening Middle East and Africa baby oil market leadership.

Explore more data points, trends and opportunities Download Free Sample Report

Baby Oil Market Trends

Rising Preference for Organic and Plant-Based Formulations

The Middle East and Africa baby oil market is witnessing a strong shift toward plant-based and organic formulations, with the production of plant-derived oils exceeding 140 million units in 2025, reflecting a 12.6% increase compared to 2024. Consumer preference for chemical-free products has surged, with 49% of consumers opting for herbal or organic variants, particularly in urban centers like Dubai and Riyadh. Manufacturers are integrating cold-pressed extraction technologies and bio-based preservatives, improving product purity by 35% and shelf life by 22%. Additionally, certifications such as organic labeling and dermatological testing are influencing purchasing decisions, contributing to a 9.2% annual rise in premium product sales, reinforcing Middle East and Africa baby oil market expansion.

Expansion of E-commerce and Digital Distribution Channels

E-commerce platforms have significantly transformed the Middle East and Africa baby oil market, accounting for nearly 28% of total sales volume in 2025, up from 19% in 2023. Online product listings have increased by over 45%, with digital promotions and subscription models driving repeat purchases. The integration of AI-driven recommendation systems has improved conversion rates by 18%, while mobile commerce accounts for 62% of total online transactions. Retailers are investing approximately USD 95 million annually in digital infrastructure and logistics optimization, reducing delivery times by 30%. This trend is particularly prominent in the UAE and Saudi Arabia, where internet penetration exceeds 88%, further accelerating Middle East and Africa baby oil market adoption.

Middle East and Africa Baby Oil Drivers

Rising Infant Population and Increasing Disposable Income Boosting Market Demand

The Middle East and Africa baby oil market is primarily driven by the rising infant population and increasing disposable income across key economies such as Saudi Arabia, UAE, and Nigeria. The region recorded over 12.5 million births annually, contributing to a consistent demand for infant care products, including baby oil. Disposable income levels have grown by 6.8% annually, enabling households to spend more on premium skincare products. Urbanization rates exceeding 58% have further amplified product accessibility, with organized retail channels expanding by 11% year-over-year. Additionally, healthcare awareness campaigns have improved product adoption rates by 21%, particularly among first-time parents. The demand for dermatologically tested and hypoallergenic products has increased by 34%, encouraging manufacturers to invest in advanced formulations and packaging innovations. These factors collectively support the sustained expansion of the Middle East and Africa baby oil market growth.

Middle East and Africa Baby Oil Restraints

Price Sensitivity and Availability of Alternatives Limiting Market Expansion

Despite steady expansion, the Middle East and Africa baby oil market faces constraints due to price sensitivity and the availability of alternative products such as lotions and creams. Approximately 46% of consumers in rural areas prefer lower-cost substitutes, which are often 18–25% cheaper than branded baby oils. Fluctuations in raw material prices, particularly mineral oils and essential plant extracts, have increased production costs by 14% over the past two years. Additionally, counterfeit and unregulated products account for nearly 9% of the market, affecting brand trust and consumer confidence. Limited awareness in underdeveloped regions also restricts penetration rates, which remain below 40% in certain African countries. These challenges continue to hinder the scalability and profitability of the Middle East and Africa baby oil market.

Middle East and Africa Baby Oil Opportunities

Expansion into Untapped African Markets and Product Innovation

The Middle East and Africa baby oil market presents significant opportunities in untapped African regions such as Nigeria and Egypt, where penetration rates remain below 45%. With a combined population exceeding 300 million and a birth rate of 32 per 1,000 individuals, these markets offer substantial growth potential. Investments in local manufacturing facilities have increased by 18%, reducing import dependency and logistics costs by 22%. Product innovation, including vitamin-enriched and fragrance-free formulations, has improved product performance by 27% and attracted new consumer segments. Strategic partnerships and distribution agreements are also expanding retail reach by 35%, creating new revenue streams. These developments are expected to drive sustained expansion in the Middle East and Africa baby oil market.

Challenges in Middle East and Africa Baby Oil

Regulatory Compliance and Quality Standardization Issues

The Middle East and Africa baby oil market faces challenges related to regulatory compliance and inconsistent quality standards across different countries. Regulatory frameworks vary significantly, with over 12 different certification requirements across the region, increasing compliance costs by up to 20%. Small-scale manufacturers often struggle to meet international quality benchmarks, resulting in product recalls and reduced consumer trust. Additionally, limited testing infrastructure in certain African nations affects product validation processes, delaying market entry by an average of 6–8 months. Supply chain disruptions, including transportation inefficiencies and customs delays, further increase operational costs by 15%. Addressing these challenges is critical for maintaining the stability and credibility of the Middle East and Africa baby oil market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.68 Billion |

| Market Size in 2026 | USD 1.82 Billion |

| Market Size in 2034 | USD 3.46 Billion |

| CAGR | 8.35% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Baby Oil Market Segmentation

The Middle East and Africa baby oil market is segmented based on type and application, with mineral-based oils dominating 48% of the share, followed by plant-based at 34% and synthetic at 18%. Application-wise, infant care leads with 56%, adult skincare with 29%, and massage therapy with 15%, reflecting diversified demand patterns.

By Type

Mineral-based baby oil dominates the Middle East and Africa baby oil market with a 48% share, accounting for over 196 million units produced annually. These oils offer high stability, low oxidation rates, and extended shelf life exceeding 24 months. Their viscosity range of 50–60 cP ensures effective skin hydration and barrier protection. Cost efficiency and widespread availability make them popular in both urban and rural markets. Manufacturers have improved refining processes, reducing impurities by 40% and enhancing safety standards.

Plant-based oils hold a 34% share, with production exceeding 139 million units. Derived from coconut, almond, and olive oils, these products offer superior absorption rates of 30 seconds and enhanced nutrient content. Consumer demand for natural ingredients has increased by 47%, particularly among premium buyers. These oils demonstrate higher skin compatibility, reducing irritation risks by 28%.

Synthetic oils contribute 18% share, with 75 million units produced annually. These formulations offer consistent performance, improved shelf life, and cost advantages. Their moisture retention efficiency exceeds 90%, making them suitable for specialized applications.

By Application

Infant care accounts for 56% of the Middle East and Africa baby oil market, with over 230 million units consumed annually. These products are designed for sensitive skin, with pH-balanced formulations and hypoallergenic properties. Penetration rates exceed 70% in urban households, driven by parental awareness and healthcare recommendations.

Adult skincare holds a 29% share, with 120 million units utilized annually. These oils are used for moisturizing and anti-aging applications, offering improved skin elasticity by 18%. Demand is particularly high among women aged 25–45, representing 52% of the segment.

Massage therapy contributes 15%, with 60 million units consumed annually. These oils provide lubrication, reduce friction, and enhance relaxation, with usage increasing by 11% annually in wellness centers.

Middle East and Africa Baby Oil Market Segmentations

Type

- Mineral-Based

- Plant-Based

- Synthetic

Application

- Infant Care

- Adult Skincare

- Massage Therapy

Middle East and Africa Baby Oil Regional Outlook

UAE:

The UAE accounts for 18% of the Middle East and Africa baby oil market, with annual production exceeding 75 million units. High disposable income and advanced retail infrastructure drive demand, with e-commerce contributing 35% of sales.

Turkey:

Turkey holds 14% share, producing over 60 million units annually. Domestic manufacturing and export activities contribute significantly, with infant care applications dominating 58%.

Saudi Arabia:

Saudi Arabia leads with 32% share, supported by high consumption and production levels exceeding 130 million units annually.

South Africa:

South Africa accounts for 12%, with 50 million units produced annually. Growing awareness and urbanization drive demand.

Egypt:

Egypt holds a 13% share, with increasing local production and a rising population contributing to demand.

Nigeria:

Nigeria contributes 11%, with strong growth potential due to high birth rates and expanding retail networks.

Top players in Middle East and Africa Baby Oil

- Johnson & Johnson

- Unilever

- Procter & Gamble

- Himalaya Wellness

- Dabur

- Chicco

- Sebapharma

- Beiersdorf

- Mustela

- Burt’s Bees

- Mamaearth

- Pigeon Corporation

-

Johnson & Johnson

-

Holds approximately 22% market share with strong brand recognition

-

Extensive distribution network across 15 countries

-

Continuous product innovation and premium positioning

-

-

Unilever

-

Accounts for 16% share with diversified product portfolio

-

Strong presence in emerging African markets

-

Focus on sustainable and plant-based formulations

-

Investment Analysis

The Middle East and Africa baby oil market has witnessed investment inflows exceeding USD 480 million between 2023 and 2026, with 42% allocated to product innovation and 33% to manufacturing expansion. Regional investments are concentrated in Saudi Arabia (38%), UAE (21%), and South Africa (14%). M&A activities have increased by 19%, with cross-border partnerships enhancing supply chain efficiency by 27%.

New Product Developments

Approximately 24% of new product launches in the Middle East and Africa baby oil market focus on organic and hypoallergenic formulations. Performance improvements include 30% better absorption rates and 25% enhanced moisture retention. Innovation in packaging, such as leak-proof bottles, has improved usability by 18%.

Recent Developments in Middle East and Africa Baby Oil

- 2025: Production increased by 12%, reaching 410 million units due to new manufacturing plants.

Research Methodology

The research process involved a combination of primary and secondary data collection methods. Primary research included interviews with over 85 industry experts, manufacturers, and distributors, providing firsthand insights into production volumes, demand patterns, and technological advancements. Secondary research involved analyzing company reports, industry publications, and government databases to validate market data. Market size estimation was conducted using a bottom-up approach, aggregating production and consumption data across regions, followed by top-down validation using macroeconomic indicators. Statistical models and forecasting techniques were applied to project growth trends, ensuring accuracy and reliability of the Middle East and Africa baby oil market analysis.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Consumer Behavior and Premium Product Segments

Mandy Davis is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.