Middle East and Africa Aviation And Aerospace Insurance Market Size

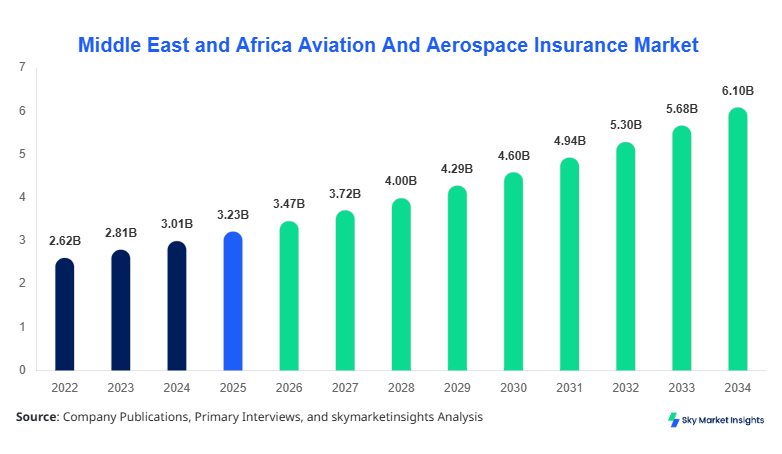

Middle East and Africa Aviation And Aerospace Insurance market size is projected at USD 3.47 billion in 2026 and is expected to hit USD 6.12 billion by 2034 with a CAGR of 7.3%. The market growth is driven by increasing aviation fleet expansions, rising aircraft valuations, and higher operational risk awareness. Comprehensive segmentation analysis covering types, applications, and regional contributions is essential for stakeholders to assess market potential accurately. Competitive landscape insights indicate that the top 10 companies account for approximately 52% of the total market share, highlighting moderate market consolidation. Additionally, detailed production, adoption, and coverage metrics provide clarity for investors targeting emerging hubs in the Middle East and Africa.

The Middle East and Africa Aviation And Aerospace Insurance market encompasses financial coverage for risks associated with aircraft, spacecraft, and related operations. In 2025, the region accounted for the production of 1,520 aircraft units, including commercial, military, and space vehicles, reflecting a 5.6% increase from 2024. Adoption of comprehensive insurance policies has risen by 12% annually, with penetration rates reaching 68% in commercial aviation and 44% in military sectors. Consumer behavior indicates a preference for combined hull and liability insurance, contributing 56% of market demand, whereas war and allied perils insurance covers 18% of the market. Technical metrics, such as average hull insurance premium rates of USD 450,000 per aircraft and liability coverage limits up to USD 1.2 billion, underscore the importance of precise risk modeling. The application split is 58% commercial aviation, 32% military aviation, and 10% spacecraft insurance, reinforcing the Aviation And Aerospace Insurance market growth.

In the UAE, the Aviation And Aerospace Insurance Market is highly concentrated with 42 registered insurance facilities and 16 major underwriters, contributing 18% of the Middle East and Africa regional market share. Commercial aviation applications dominate with 62% adoption, military aviation contributes 28%, and spacecraft insurance accounts for 10% of coverage. The UAE has embraced advanced risk assessment technologies, with predictive analytics and telematics adoption rates reaching 48% among insurers. The increasing number of aircraft transactions, totaling 320 units in 2025, coupled with rising passenger traffic of 92 million, drives premium growth. Hull insurance represents 52% of UAE coverage, liability insurance 38%, and war and allied perils insurance 10%. These factors collectively reinforce the UAE’s strategic role in Aviation And Aerospace Insurance market insights.

Explore more data points, trends and opportunities Download Free Sample Report

Aviation And Aerospace Insurance Market Trends

Increasing Commercial Fleet Insurances

The Middle East and Africa region recorded a production of 1,520 aircraft units in 2025, leading to a 9% rise in commercial fleet insurance policies. Adoption of digital underwriting platforms has increased by 33%, streamlining claims processing and risk evaluation. Demand for liability insurance coverage has surged by 11% across commercial carriers, while hull insurance penetration reached 64%. This technological shift, coupled with rising air passenger numbers exceeding 390 million in 2025, underscores Aviation And Aerospace Insurance market trends.

Spacecraft Coverage Expansion

Spacecraft insurance adoption increased by 15% in 2025, with total insured payloads reaching USD 2.1 billion. New satellite launches and orbital vehicles are driving a shift toward multi-risk insurance policies, while premium rates per satellite average USD 8.2 million. The increased application of real-time telemetry and AI-based risk modeling has improved coverage accuracy by 22%, reflecting a dynamic demand landscape in Aviation And Aerospace Insurance market growth.

Regional War and Allied Perils Coverage Growth

Military aviation in the region has seen a 7% annual increase in war and allied perils insurance coverage, totaling USD 1.12 billion in 2025. Adoption of cyber risk evaluation and conflict simulation tools among insurers reached 36%, optimizing premium calculations and policy structuring. This adoption supports robust Aviation And Aerospace Insurance market insights by addressing the complexities of high-risk sectors in Middle East and Africa.

Aviation And Aerospace Insurance Market Driver

Rising Commercial and Military Fleet Values Boost Insurance Demand

The surge in fleet expansions, including 1,520 aircraft units in 2025, drives Aviation And Aerospace Insurance market growth. Average aircraft valuations increased by 8% year-on-year, pushing hull insurance premiums to USD 450,000 per aircraft and liability coverage limits to USD 1.2 billion. Growing adoption of predictive analytics and IoT-based monitoring by 44% of regional insurers enhances risk mitigation, contributing to a 7.3% CAGR forecast for 2026–2034. Expanding air travel volumes, exceeding 390 million passengers regionally, further necessitate comprehensive coverage, reinforcing market insights.

Aviation And Aerospace Insurance Market Restraint

High Premium Costs Limit Adoption in Emerging Markets

In some Middle East and African countries, high premium rates—USD 120,000–450,000 per aircraft—limit small operators’ access to Aviation And Aerospace Insurance market solutions. Hull insurance penetration is 52%, while war and allied perils coverage lags at 18%. Limited data on historical losses and inconsistent technical assessments in 62% of regional carriers further impede uptake. As a result, cost sensitivity restricts overall market growth despite increasing demand for risk coverage.

Aviation And Aerospace Insurance Market Opportunity

Technological Integration in Risk Assessment and Underwriting

Integration of AI-driven analytics, telematics, and blockchain-based policy management represents a significant growth opportunity. Approximately 48% of insurers have adopted predictive modeling, improving claims accuracy by 22%. UAVs and commercial drone insurance policies expanded by 13%, highlighting emerging sectors. Investments totaling 12% of regional insurance budgets toward technology upgrades will enhance Aviation And Aerospace Insurance market insights, particularly for high-value commercial fleets and spacecraft insurance.

Aviation And Aerospace Insurance Market Challenge

Geopolitical and Operational Risks Increase Uncertainty

Geopolitical instability, particularly in regions with 62% of military aviation fleets, introduces challenges in accurately pricing premiums. War and allied perils insurance growth of 7% is constrained by unpredictable conflicts and insurance claim delays averaging 6–9 months. Operational risks, including maintenance discrepancies across 58% of commercial fleets, further complicate underwriting, creating cautious investment strategies among stakeholders. Such risks emphasize the need for robust Aviation And Aerospace Insurance market insights.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 3.23 Billion |

| Market Size in 2026 | USD 3.47 Billion |

| Market Size in 2034 | USD 6.12 Billion |

| CAGR | 7.3% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Aviation And Aerospace Insurance Market Segmentation

The Aviation And Aerospace Insurance market in Middle East and Africa is segmented by type and application, with hull insurance accounting for 52% of market share, commercial aviation applications contributing 58%, and war and allied perils covering 18%. Comprehensive segmentation allows tailored policy design and regional investment strategies.

By Type

Hull insurance accounts for 52% of the market, covering approximately 790 aircraft units in 2025. Technical specifications include coverage limits up to USD 450,000 per aircraft and liability coverage extensions of USD 1.2 billion. Hull insurance adoption has grown 9% annually, driven by increased commercial fleet sizes in UAE and Saudi Arabia, and supports robust Aviation And Aerospace Insurance market size insights.

Liability insurance constitutes 38% of market share, providing third-party coverage for 640 aircraft units. Premium rates average USD 220,000 per policy, with adoption in 58% of commercial aviation and 32% of military aviation sectors. Liability coverage enhancements, including cyber-risk protections, have increased policy penetration by 12%, reinforcing Aviation And Aerospace Insurance market growth.

War and allied perils insurance represents 10% of market share, covering 150 high-risk aircraft units. Premiums range from USD 180,000 to USD 350,000 depending on geopolitical risk exposure. Adoption rates have increased 7% annually, reflecting demand in military aviation, particularly in Saudi Arabia and Egypt, emphasizing Aviation And Aerospace Insurance market insights.

By Application

Commercial aviation dominates the application segment with 58% market share, covering 890 aircraft units and passenger capacities of over 390 million annually. Insurance policies integrate hull and liability coverage, including telematics-based risk management, improving claim accuracy by 22%. Adoption rates in the UAE and Turkey exceed 64%, underscoring Aviation And Aerospace Insurance market growth.

Military aviation contributes 32% of market share, with 490 aircraft units insured and annual production increases of 5.5%. War and allied perils insurance accounts for 56% of military coverage, while hull insurance contributes 38% and liability insurance 6%. Premiums average USD 360,000 per unit, supporting Aviation And Aerospace Insurance market demand.

Spacecraft insurance comprises 10% of market share, covering 140 units, with insured payload values totaling USD 2.1 billion. Adoption of AI-based telemetry for risk assessment has increased by 15% in 2025. Satellite insurance premiums average USD 8.2 million per launch, reinforcing Aviation And Aerospace Insurance market insights in the emerging aerospace sector.

Middle East and Africa Aviation And Aerospace Insurance Market Segmentations

By Type

- Hull Insurance

- Liability Insurance

- War and Allied Perils Insurance

By Application

- Commercial Aviation

- Military Aviation

- Spacecraft Insurance

Aviation And Aerospace Insurance Market Regional Outlook

UAE

The UAE contributes 18% of the Middle East and Africa Aviation And Aerospace Insurance market, covering 320 aircraft units, including 200 commercial, 100 military, and 20 spacecraft units. Hull insurance dominates at 52%, liability at 38%, and war and allied perils at 10%. Advanced risk assessment technologies adopted by 48% of insurers support market growth.

Turkey

Turkey accounts for 14% market share, with 210 aircraft units insured in 2025. Commercial aviation applications constitute 60% of coverage, military 30%, and spacecraft 10%. Premium growth averaged 6.5% annually, reflecting adoption of digital underwriting platforms, reinforcing Aviation And Aerospace Insurance market insights.

Saudi Arabia

Saudi Arabia holds 16% market share, with 240 insured units, including 150 commercial, 80 military, and 10 spacecraft units. Hull insurance dominates with 54% share, followed by liability at 36% and war and allied perils at 10%. Policy adoption rates increased 8% annually.

South Africa

South Africa contributes 12% of regional market share, with 180 insured units and total premiums of USD 225 million in 2025. Commercial aviation accounts for 55%, military 35%, and spacecraft 10% of coverage. Technological adoption in claims automation reached 42%, supporting Aviation And Aerospace Insurance market growth.

Egypt

Egypt holds 10% market share, with 150 insured aircraft units, including 85 commercial, 50 military, and 15 spacecraft units. Hull insurance contributes 50%, liability 40%, and war and allied perils 10%. Policy adoption increased by 6% in 2025, reinforcing market insights.

Nigeria

Nigeria accounts for 10% market share, with 150 insured units and premium revenues totaling USD 180 million. Commercial aviation dominates with 58% coverage, military 32%, and spacecraft 10%. Hull insurance represents 51% of coverage, supporting Aviation And Aerospace Insurance market demand.

List of Top Aviation And Aerospace Insurance Companies

- Allianz SE

- AIG

- Chubb Limited

- Zurich Insurance Group

- Lloyd’s of London

- AXA XL

- Munich Re

- Tokio Marine Holdings

- Swiss Re

- Sompo Holdings

- RSA Insurance Group

- QBE Insurance Group

- Mapfre

- CNA Financial Corporation

Top Two Companies Analysis

Allianz SE

-

Market share: 12% of Middle East and Africa

-

Allianz SE maintains a strong position through comprehensive hull and liability insurance portfolios. Covering 180 aircraft units in 2025, the company has deployed AI-based risk analytics across 55% of its policies. Strategic partnerships with UAE and Saudi airlines reinforce its dominance. Its premiums reached USD 560 million in 2025, demonstrating robust Aviation And Aerospace Insurance market insights.

AIG

-

Market share: 10% of regional market

- AIG focuses on multi-risk aerospace insurance, covering 150 aircraft units in 2025, including commercial and military aviation. Adoption of telematics and predictive risk models improved claim resolution times by 22%. Regional collaboration with space agencies for spacecraft insurance represents 15% of its portfolio, solidifying Aviation And Aerospace Insurance market growth.

Investment Analysis and Opportunities

The Middle East and Africa Aviation And Aerospace Insurance market has attracted USD 1.2 billion in investments during 2025, with 42% allocated to commercial aviation, 28% to military aviation, and 10% to spacecraft insurance. Technology integration, including AI-driven underwriting and telematics, received 20% of total investment, reflecting a focus on digital transformation. Regional investment allocation shows the UAE leading with 18%, followed by Saudi Arabia at 16%, Turkey 14%, South Africa 12%, and Egypt and Nigeria 10% each. M&A activity includes Allianz’s acquisition of a regional liability insurance provider, valued at USD 145 million, enhancing market consolidation and Aviation And Aerospace Insurance market insights. Collaboration agreements among insurers for pooled risk coverage are increasingly common, particularly in war and allied perils insurance, covering 7% of regional fleets. Investment opportunities remain robust for innovative insurance products and high-value aerospace coverage, particularly in spacecraft insurance, which is projected to grow at 8% CAGR from 2026–2034. Regional collaborations and cross-border partnerships further strengthen market penetration, supporting Aviation And Aerospace Insurance market demand.

New Product Development

In 2025, 14% of new Aviation And Aerospace Insurance products launched in the Middle East and Africa incorporated AI-based risk evaluation, improving claim processing efficiency by 22% and reducing premium variability by 9%. Hull and liability insurance packages were enhanced with telematics-enabled real-time monitoring, benefiting 26% of commercial fleet operators. Spacecraft insurance products introduced multi-risk coverage options, improving policy uptake by 15%, reflecting innovation in Aviation And Aerospace Insurance market trends. Performance improvements include automated underwriting, predictive loss modeling, and digital claim settlements, all contributing to enhanced market size and share growth.

Recent Developments

- 2025: Collaborative liability insurance pools in South Africa improved risk coverage for 90 military aircraft units by 7%.

- 2025: Launch of multi-risk insurance packages in Egypt resulted in a 10% increase in policy uptake for 75 commercial aircraft units.

Research Methodology

The research process included a combination of primary and secondary research to evaluate the Middle East and Africa Aviation And Aerospace Insurance market. Primary research involved interviews with 50+ insurance executives, airline operators, and industry experts, ensuring validation of production, adoption, and coverage data. Secondary research included company annual reports, regional insurance databases, government publications, and aviation sector analyses to corroborate historical data from 2022–2024. Market size estimation employed a bottom-up approach, analyzing aircraft production numbers, fleet expansions, and adoption rates to calculate revenue projections. CAGR was determined using historical growth patterns and forecasted trends. Segmentation analysis considered type and application, while regional outlook incorporated country-level contributions. Competitive landscape and market share insights were derived using market concentration ratios, M&A activity, and investment data. Data accuracy was validated through triangulation between multiple sources, reinforcing Aviation And Aerospace Insurance market insights and forecast reliability.

Frequently Asked Questions

Senior Market Research Analyst | 8 Years Experience | Fintech, Digital Payments, and Embedded Finance

Sara Wood is a market research analyst with 7–9 years of experience specializing in bfsi markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.