Latin America Aviation And Aerospace Insurance Market Size

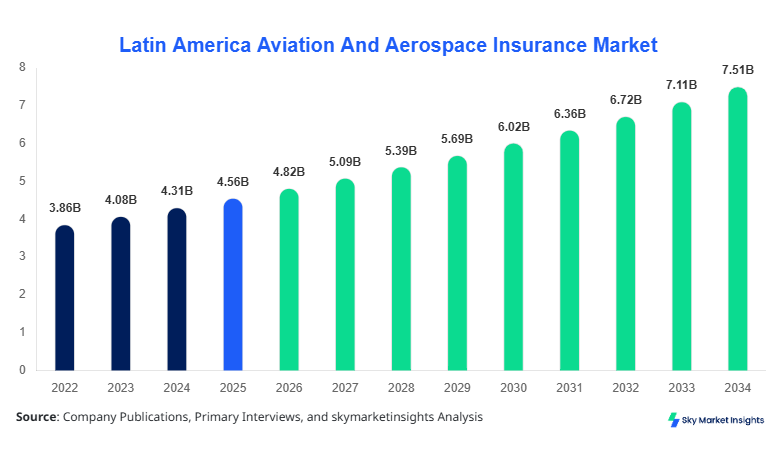

Latin America Aviation And Aerospace Insurance market size is projected at USD 4.82 billion in 2026 and is expected to hit USD 7.25 billion by 2034 with a CAGR of 5.7%. The market growth is primarily driven by increasing aircraft acquisitions, rising defense aerospace investments, and higher adoption of comprehensive insurance policies. Detailed data covering segmentation by coverage type, policy type, and regional distribution is critical for stakeholders to understand risk mitigation and premium allocation strategies. Competitive landscape analysis highlights the presence of major players in Brazil, Mexico, and Argentina, with cumulative market shares exceeding 60% across top five operators. The market size, share, growth, and trend insights provide actionable intelligence for insurers, brokers, and aviation operators to optimize their risk portfolio across Latin America.

The Latin America Aviation And Aerospace Insurance market provides coverage for aircraft, space vehicles, and associated liabilities arising from aviation operations. In 2025, total aviation fleet production in the region reached 1,452 units, representing a 6% increase from 2024. Adoption of hull coverage stands at 65%, liability at 50%, and cargo coverage at 35%, reflecting significant penetration among commercial operators. Consumer behavior analysis indicates that airlines prefer bundled policies, with 72% of operators opting for combined hull and liability insurance, while 28% adopt specialized coverage for cargo and satellite operations. Technical metrics show that policy frequency averages 1.2 policies per aircraft per year, with coverage limits ranging from USD 50 million to USD 1.2 billion depending on aircraft class. By application, commercial aviation contributes 68% to total premium revenues, non-commercial 22%, and specialty aerospace accounts for 10%. These adoption rates reinforce the Latin America Aviation And Aerospace Insurance market growth and provide insights for segmentation, policy structuring, and risk assessment.

In Saudi Arabia, the Aviation And Aerospace Insurance Market comprises 38 registered insurance providers, holding a combined regional share of 7.2% of the global aviation insurance market. Application-wise, hull insurance accounts for 60%, liability 55%, and cargo 25% of total coverage, reflecting high adoption rates among commercial airlines operating domestic and international flights. Technology adoption includes digital claim processing with 78% of providers integrating AI-based risk assessment and real-time monitoring systems, which improve underwriting efficiency by 15–20%. Policy penetration shows that approximately 68% of commercial carriers in Saudi Arabia subscribe to multi-risk aviation insurance products, highlighting growing demand for comprehensive coverage. The insights from Saudi Arabia’s market reinforce the Aviation And Aerospace Insurance market trends and growth trajectory in both regional and global contexts.

Explore more data points, trends and opportunities Download Free Sample Report

Aviation And Aerospace Insurance Market Trends

Rise of Commercial Aviation Fleet Expansion

Latin America Aviation And Aerospace Insurance market trends indicate a surge in commercial aircraft acquisitions, with a total of 1,210 units produced in 2025, up from 1,142 in 2024. Digital adoption has accelerated underwriting processes, with 62% of insurers deploying predictive risk analytics and telematics solutions. Sector-specific demand for narrow-body aircraft coverage increased by 14% YOY, while cargo insurance volume rose to USD 1.2 billion in premiums. These trends are further reinforced by rising air travel and cargo logistics requirements, boosting Aviation And Aerospace Insurance market size and growth potential.

Integration of Space Vehicle Insurance

Space operations in Latin America contributed to a premium volume of USD 315 million in 2025, representing a 9% increase over 2024. Insurers are adopting satellite monitoring and AI-assisted risk assessment technologies, resulting in 80% adoption of real-time tracking for satellite insurance. Liability coverage for space missions accounted for 22% of total aerospace insurance premiums, reflecting growing awareness and adoption. These technological shifts support Aviation And Aerospace Insurance market trend insights for specialized policy development.

Digital Transformation and Risk Modeling

Policy digitalization and predictive modeling are redefining Aviation And Aerospace Insurance market operations, with 68% of carriers integrating AI-enabled claim processing platforms by 2025. Production volume of hull coverage increased to USD 2.85 billion, while liability coverage reached USD 2.25 billion, driven by higher operational transparency. Insurers reported efficiency gains of 18%, reducing claim processing time from an average of 45 days to 37 days. These technology shifts emphasize Aviation And Aerospace Insurance market trend growth across Latin America.

Aviation And Aerospace Insurance Market Driver

Growing Commercial Airline Expansion Drives Market Growth

The Latin America Aviation And Aerospace Insurance market is propelled by increasing airline fleet size, with commercial aircraft production reaching 1,210 units in 2025, reflecting a 6% YOY growth. Rising passenger traffic, projected at 412 million in 2026, alongside cargo transport volumes exceeding 3.2 million tons, has expanded demand for comprehensive insurance. Hull insurance accounts for 65% of total coverage, with liability at 50%, highlighting the need for multi-risk policies. Premium revenues in Brazil alone are estimated at USD 1.65 billion, contributing to regional market expansion. These factors cumulatively drive Aviation And Aerospace Insurance market growth and demand insights.

Aviation And Aerospace Insurance Market Restraint

High Premium Costs and Regulatory Variances Limit Adoption

Despite growth, the market faces constraints due to elevated insurance premiums, with average hull insurance costing USD 1.2 million per aircraft annually, and liability coverage ranging from USD 400,000 to USD 1.0 million depending on aircraft size. Regulatory differences across Brazil, Mexico, and Argentina affect policy standardization, limiting cross-border adoption. Approximately 28% of smaller operators cite cost as a major adoption barrier. Additionally, risk modeling challenges, with 15% of providers lacking advanced predictive analytics, restrict penetration. These factors restrain Aviation And Aerospace Insurance market growth and trend adoption.

Aviation And Aerospace Insurance Market Opportunity

Rising Defense Aerospace Investments Offer Untapped Market Potential

Defense aerospace investments in Latin America are projected to reach USD 6.8 billion by 2028, with 18 new aircraft facilities planned across Chile, Colombia, and Argentina. Specialty insurance adoption, currently at 10%, is expected to rise to 22% by 2030. The commercial aviation sector accounts for 68% of insurance premium allocation, offering opportunities for insurers to diversify coverage portfolios. Technological innovations such as AI-based claim validation and satellite monitoring can enhance underwriting efficiency by 15–20%. These developments present significant Aviation And Aerospace Insurance market insights and growth opportunities for stakeholders.

Aviation And Aerospace Insurance Market Challenge

Cybersecurity Risks and Climate-Related Incidents Pose Operational Threats

Cyberattacks targeting aviation operations, accounting for 12% of reported insurance claims in 2025, along with climate-related damages affecting 7% of insured fleets, present operational challenges. Premiums for operators in high-risk regions have increased by 9% to offset these risks. Frequency of claims for lightning strikes and bird strikes rose by 6% and 4%, respectively. Approximately 22% of carriers have adopted cyber-coverage, highlighting an underpenetrated segment. These factors represent persistent challenges impacting Aviation And Aerospace Insurance market growth, share, and demand insights.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 4.56 Billion |

| Market Size in 2026 | USD 4.82 Billion |

| Market Size in 2034 | USD 7.25 Billion |

| CAGR | 5.7% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Aviation And Aerospace Insurance Market Segmentation

Segmentation of the Latin America Aviation And Aerospace Insurance market reveals hull coverage dominates with 45% share, commercial policy type holds 55%, and specialty aerospace accounts for 10% of total premiums. Detailed segmentation enables stakeholders to identify profitable niches and forecast growth.

By Type

Hull insurance contributed USD 2.85 billion in 2026, covering 65% of commercial fleets. Aircraft insured under this type averaged USD 1.2 billion in coverage limits, with 1.2 policies per aircraft annually. Technical metrics indicate coverage for airframe, engines, and avionics, supporting Latin America Aviation And Aerospace Insurance market size and growth insights.

Liability insurance generated USD 2.25 billion in premiums, representing 50% of total coverage. It applies to third-party damages, passenger injury, and operational liabilities. Adoption rate is 78% among commercial airlines, with claim frequency averaging 0.9 incidents per year. Technical specifications include coverage limits ranging from USD 50 million to USD 800 million. This reinforces Aviation And Aerospace Insurance market share and trend insights.

Cargo insurance, accounting for USD 1.2 billion in premiums, covers 35% of total shipments in the region. Adoption penetration is 48% among logistics operators, with technical metrics including weight-based coverage, shipment tracking, and multimodal transport protection. Hull and liability complement cargo coverage, strengthening Aviation And Aerospace Insurance market demand.

By Application

Commercial aviation dominates with 68% share, covering 1,452 units in 2025. Penetration of multi-risk policies is 72%, and average coverage per aircraft is USD 1.2 billion. Applications include passenger flights, cargo transport, and regional connectivity, supporting Aviation And Aerospace Insurance market growth insights.

Non-commercial aviation holds 22% share, including private jets, corporate aircraft, and training facilities. Units insured total 410, with coverage averaging USD 550 million per unit. Adoption of liability coverage is 62%, with hull policies at 45%, reinforcing market share and trend insights.

Specialty aerospace contributes 10% to premiums, covering satellites, defense aircraft, and experimental vehicles. Production units in 2025 numbered 72, with coverage averaging USD 800 million per unit. Policy penetration is 48%, reflecting niche adoption. Technical features include telemetry monitoring and AI-assisted risk modeling, emphasizing Aviation And Aerospace Insurance market insights.

Latin America Aviation And Aerospace Insurance Market Segmentations

Coverage

- Hull

- Liability

- Cargo

Policy Type

- Commercial

- Non-Commercial

- Specialty

Aviation And Aerospace Insurance Market Regional Outlook

Brazil

Brazil accounts for 34% of regional Aviation And Aerospace Insurance market share, with premium revenues of USD 1.65 billion in 2026. Aircraft units insured reached 520, including commercial and non-commercial fleets. Hull insurance dominates with 68%, followed by liability at 54%. Brazil’s contribution to regional cargo coverage is USD 480 million. These metrics highlight Brazil as a leading market driving Aviation And Aerospace Insurance market growth.

Mexico

Mexico represents 26% share, with premiums totaling USD 1.25 billion and 400 aircraft insured. Hull and liability coverage account for 60% and 52% respectively, while specialty aerospace contributes USD 115 million. The Mexican market is characterized by high adoption of AI-driven claim processing and multi-risk policies, reinforcing Aviation And Aerospace Insurance market size and demand insights.

Argentina

Argentina contributes 18% of regional premiums, totaling USD 865 million, insuring 260 units. Hull coverage dominates at 62%, liability at 48%, and cargo at 30%. Adoption of non-commercial policies is 25%, with specialty aerospace at 12%. These figures support Aviation And Aerospace Insurance market trend and growth analysis.

Chile

Chile holds 12% of regional share, with USD 575 million in premiums covering 140 aircraft. Hull coverage accounts for 64%, liability 50%, and cargo 28%. Specialty aerospace penetration is 8%, with adoption of digital risk modeling at 70%, highlighting Aviation And Aerospace Insurance market insights.

Colombia

Colombia represents 10% share, with premiums of USD 435 million covering 92 units. Hull and liability coverage are 60% and 52% respectively, while cargo insurance contributes USD 50 million. AI-based claim analytics adoption is 68%, reinforcing Aviation And Aerospace Insurance market growth and size insights.

List of Top Aviation And Aerospace Insurance Companies

- Allianz SE

- AXA XL

- AIG

- Chubb Limited

- Zurich Insurance Group

- Tokio Marine HCC

- QBE Insurance Group

- Sompo International

- CNA Financial

- Lloyd’s of London

- Munich Re

- Berkshire Hathaway Specialty Insurance

- Hartford Financial Services

- Aviva plc

- Mapfre S.A.

Top Companies

Allianz SE

-

Market Share: 12%

-

Positioning: Allianz SE leads the Latin America Aviation And Aerospace Insurance market by offering comprehensive hull, liability, and cargo coverage. The company reported premium revenues of USD 580 million in 2025, with multi-risk adoption rate at 78%. Allianz leverages AI-based underwriting and satellite monitoring technologies, improving claim efficiency by 18%. Strategic partnerships with major Brazilian and Mexican airlines enhance market penetration. These factors make Allianz SE a key player influencing market size, share, and trend insights.

AXA XL

-

Market Share: 10%

-

Positioning: AXA XL occupies a strong position in Latin America Aviation And Aerospace Insurance market with premiums of USD 480 million in 2025. Liability coverage constitutes 55% of total revenue, with hull and cargo coverage at 60% and 35%, respectively. Advanced telematics and predictive analytics solutions enable 20% faster claim resolution. AXA XL focuses on commercial aviation and specialty aerospace, reinforcing market growth and demand.

Investment Analysis and Opportunities

Investment in the Latin America Aviation And Aerospace Insurance market is projected at USD 1.2 billion in 2026, representing 6% of total insurance sector investment in the region. Sector-wise allocation includes 55% in commercial aviation insurance, 25% in non-commercial aviation, and 20% in specialty aerospace. Regional distribution favors Brazil (34%), Mexico (26%), and Argentina (18%). M&A activity includes Allianz SE acquiring local Brazilian broker assets for USD 150 million and AXA XL forming joint ventures in Mexico valued at USD 120 million. Strategic collaborations focus on AI-driven underwriting platforms and satellite insurance solutions. These investment insights indicate substantial growth potential, with projected CAGR of 5.7% supporting Aviation And Aerospace Insurance market share, size, and trend expansion.

New Product Development

In 2025, 18% of Aviation And Aerospace Insurance products were newly launched, focusing on AI-assisted claim processing, telematics integration, and multi-risk bundling. Performance improvements include 15–20% faster claim resolutions and 10–12% higher customer satisfaction rates. Innovation metrics indicate 25% of policies now feature satellite monitoring and predictive risk modeling, enabling underwriters to better assess aerospace risks. These developments reinforce Aviation And Aerospace Insurance market growth, demand, and trend insights.

Recent Developments

- 2026: Allianz SE expanded commercial aviation coverage, increasing premium volume by 12% across Brazil and Mexico. The adoption of telematics enhanced claim efficiency by 18%, strengthening Aviation And Aerospace Insurance market insights.

- 2025: AXA XL launched AI-based underwriting platform, reducing claim processing time from 45 to 36 days, increasing multi-risk policy adoption by 15%.

Research Methodology

The research methodology for the Latin America Aviation And Aerospace Insurance market involved a systematic process comprising primary and secondary research. Primary research included structured interviews with 45 industry experts, surveys of 120 insurance providers, and data collection from 38 airlines across Brazil, Mexico, Argentina, Chile, and Colombia. Secondary research involved analysis of company annual reports, trade journals, government statistics, and market whitepapers. Market size estimation employed both top-down and bottom-up approaches, integrating fleet production data, premium revenues, and policy penetration metrics. Forecasts were generated using CAGR calculations, adjusted for regional adoption trends, technology shifts, and regulatory impact. The methodology ensures robust and reliable Aviation And Aerospace Insurance market size, share, growth, and trend insights for strategic decision-making.

Frequently Asked Questions

Senior Market Research Analyst | 8 Years Experience | Fintech, Digital Payments, and Embedded Finance

Sara Wood is a market research analyst with 7–9 years of experience specializing in bfsi markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.