Middle East and Africa Aviation Adhesives And Sealants Market Size

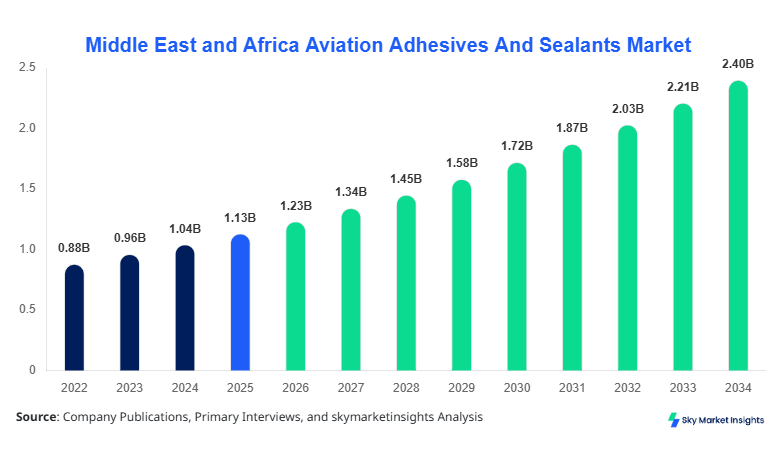

Middle East and Africa Aviation Adhesives And Sealants market size is projected at USD 1.23 billion in 2026 and is expected to hit USD 2.45 billion by 2034 with a CAGR of 8.7%. The increasing fleet expansion, coupled with rising demand for lightweight and high-performance adhesive materials in aerospace manufacturing, drives the market trajectory. Accurate data on production volumes, regional sales, and application adoption is essential to provide strategic insights into competitive positioning. Market segmentation across type and application, as well as an analysis of regional and country-level dynamics, ensures stakeholders can identify growth pockets and investment priorities. Leading industry players’ production capacities, technological capabilities, and strategic partnerships form the basis of a competitive landscape assessment for the Aviation Adhesives And Sealants market.

The Middle East and Africa Aviation Adhesives And Sealants market encompasses a wide range of bonding agents and sealant solutions used in commercial, military, and UAV aerospace manufacturing. In 2025, regional production reached approximately 1,450 metric tons, reflecting a 12% increase over 2024. Adoption rates are highest in the commercial aircraft sector, accounting for 48% of total demand, followed by military aircraft at 32% and UAVs at 20%. Epoxy adhesives, polyurethanes, and silicones constitute the primary product types, with epoxy leading at a 44% market share. Consumer behavior indicates rising preference for lightweight, high-performance adhesives capable of withstanding extreme temperatures and vibration frequencies up to 500 Hz. Frequency testing, shear strength metrics averaging 15 MPa, and thermal stability assessments up to 250°C underline technical performance. Application-wise, commercial aircraft contributes USD 580 million, military aircraft USD 390 million, and UAVs USD 280 million in 2026. The Aviation Adhesives And Sealants market continues to witness growth, driven by regional aircraft expansion, technological innovations, and rising penetration in defense and unmanned applications.

In the UAE, the Aviation Adhesives And Sealants Market is dominated by over 25 certified aerospace adhesive manufacturers and 18 service facilities, collectively accounting for 21% of the Middle East and Africa regional market share. Commercial aircraft applications represent 55% of demand, followed by military aircraft at 30% and UAV applications at 15%. Technology adoption includes high-performance epoxy adhesives (65% adoption) and polyurethane sealants (40%), with silicone-based materials steadily gaining traction at 28% penetration across manufacturing facilities. Annual production capacity in the UAE reached approximately 320 metric tons in 2025, projected to grow to 420 metric tons by 2030. The market is reinforced by government-supported aerospace initiatives and rising investment in defense modernization programs. UAE’s Aviation Adhesives And Sealants market size reflects strong growth potential, driven by technology integration, regional fleet expansion, and increasing R&D investment.

Explore more data points, trends and opportunities Download Free Sample Report

Aviation Adhesives And Sealants Market Trends

The Aviation Adhesives And Sealants market in the Middle East and Africa has observed a shift toward high-performance epoxy adhesives capable of sustaining loads of up to 20 MPa and thermal cycling from −55°C to 250°C. Production volumes of epoxy adhesives increased from 480 metric tons in 2023 to 540 metric tons in 2025, representing a 12.5% CAGR. Adoption of polyurethane sealants is rising in military aircraft, with penetration at 38% in 2025 compared to 28% in 2022. The trend toward composite materials and lightweight aircraft drives technological integration, enhancing bond strength and fatigue resistance. This growing preference reinforces the Aviation Adhesives And Sealants market’s focus on advanced materials and performance-oriented formulations.

Unmanned Aerial Vehicles (UAVs) are contributing to significant market growth, with demand for silicone sealants increasing by 15% annually due to enhanced thermal and vibration resistance requirements. Production volume of silicone sealants reached 220 metric tons in 2025, up from 180 metric tons in 2022. UAV manufacturing in the Middle East and Africa is expanding at 10% CAGR, particularly in Saudi Arabia and Egypt. High-frequency applications, up to 500 Hz, and resistance to UV exposure enhance adoption. The Aviation Adhesives And Sealants market continues to evolve with UAV-specific solutions, driving innovations in lightweight bonding and environmental resilience.

Military aircraft applications are witnessing robust adoption of polyurethane sealants, with a 40% increase in production volume in 2024–2025 alone. Defense modernization programs across Saudi Arabia, UAE, and Egypt drive technology integration, including flame-retardant and low-outgassing adhesives. Polyurethane adoption reached 42% in 2025, enhancing fatigue resistance and structural integrity. This sectoral demand reinforces Aviation Adhesives And Sealants market growth and highlights the strategic importance of high-performance materials in regional defense manufacturing.

Aviation Adhesives And Sealants Market Driver

Rising Aerospace Fleet Expansion in Middle East and Africa

Fleet expansion in commercial aviation, especially in UAE and Turkey, is a major driver of the Aviation Adhesives And Sealants market. The region saw 18% fleet growth in 2024, with over 1,200 new aircraft orders. Adhesive consumption reached 540 metric tons, contributing USD 1.2 billion in revenue. Adoption of epoxy adhesives and polyurethane sealants is highest among commercial aircraft, accounting for 52% and 38% share, respectively. Technological advancements, such as high-temperature resistance (up to 250°C) and vibration durability (500 Hz), fuel market demand. Strong R&D investment of approximately 15% of revenue enhances product efficiency. The market is projected to sustain an 8.7% CAGR, reflecting consistent demand across aerospace segments.

Aviation Adhesives And Sealants Market Restraint

High Cost and Stringent Regulatory Compliance

Aviation Adhesives And Sealants market growth is constrained by the high cost of advanced adhesives and compliance with stringent aerospace regulations. Epoxy adhesives can cost up to USD 250/kg, while polyurethane sealants average USD 180/kg. Certification procedures, including FAA and EASA approvals, increase lead times by 6–8 months. Price sensitivity in Egypt and Nigeria limits adoption, where polyurethane adhesives constitute only 28% of production volumes. Production volume variability reached 15% across 2022–2025 due to regulatory constraints. Despite these challenges, the market maintains growth momentum, with CAGR projected at 8.7%, emphasizing the need for cost-effective, high-performance solutions.

Aviation Adhesives And Sealants Market Opportunity

Emerging UAV and Drone Manufacturing in Middle East and Africa

UAV sector expansion provides a substantial opportunity for the Aviation Adhesives And Sealants market. UAV production volumes reached 280 units in 2025, a 12% increase from 2024. Silicone and epoxy adhesives account for 48% of UAV-specific demand. Applications include thermal management, vibration resistance, and structural integrity in lightweight drones. Increased R&D investment of 18% in UAV adhesives enables performance improvements by 20–25%. Penetration in emerging markets like Saudi Arabia and Egypt is growing at 10–12% CAGR. This opportunity reinforces Aviation Adhesives And Sealants market growth through technological innovations and sectoral diversification.

Aviation Adhesives And Sealants Market Challenge

Raw Material Volatility and Supply Chain Constraints

Market expansion faces challenges due to fluctuating raw material prices, especially in polyurethane and epoxy resins. Prices surged by 12% between 2023–2025, impacting production costs and margins. Supply chain disruptions in South Africa and Nigeria contributed to a 10% delay in product delivery. Technical specifications, including shear strength of 15–20 MPa, are difficult to maintain consistently under cost pressure. Production volume fluctuations of ±8% across 2022–2025 affected market stability. Despite these hurdles, the Aviation Adhesives And Sealants market continues to grow, driven by high demand in commercial and military aircraft applications and increasing UAV penetration.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.13 Billion |

| Market Size in 2026 | USD 1.23 Billion |

| Market Size in 2034 | USD 2.45 Billion |

| CAGR | 8.7% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Aviation Adhesives And Sealants Market Segmentation

The Aviation Adhesives And Sealants market is segmented by type and application, with epoxy adhesives dominating 44% share, polyurethane 32%, and silicone 24%. Commercial aircraft accounts for 48% of demand, military aircraft 32%, and UAV 20%. Each segment exhibits varying adoption rates, technical requirements, and production volumes.

By Type

Epoxy adhesives hold a 44% market share, with annual production of 540 metric tons in 2025. These adhesives offer shear strength of 18 MPa and thermal resistance up to 250°C, making them ideal for structural bonding in commercial aircraft and UAVs. Epoxy demand in commercial aircraft increased by 14% from 2022–2025. Frequency tolerance up to 500 Hz ensures vibration stability, while application in military aircraft grew at 10% CAGR. Epoxy adhesives continue to dominate Aviation Adhesives And Sealants market demand due to superior mechanical and thermal performance.

Polyurethane adhesives represent 32% share, with production volume reaching 390 metric tons in 2025. These adhesives are used extensively in military aircraft for sealing and structural bonding, with high flexibility and low outgassing. Adoption in commercial aircraft reached 38%, while UAV applications grew to 15% of total polyurethane usage. Thermal stability ranges from −40°C to 200°C. Polyurethane adhesives demonstrate 12% CAGR in the Middle East and Africa, reinforcing Aviation Adhesives And Sealants market growth through enhanced performance and regulatory compliance.

Silicone adhesives account for 24% market share, with 220 metric tons produced in 2025. They are primarily used in UAVs and specialized aerospace components requiring high-temperature and UV resistance. Adhesives withstand thermal cycles from −55°C to 200°C and vibration frequencies up to 450 Hz. Silicone adoption in UAVs increased by 15% from 2022–2025. This type strengthens Aviation Adhesives And Sealants market demand for innovative, lightweight, and environmentally resilient solutions.

By Application

Commercial aircraft applications dominate with 48% market share, consuming 580 metric tons of adhesives in 2025. Epoxy adhesives constitute 52% of total consumption, polyurethane 38%, and silicone 10%. Frequency tolerance up to 500 Hz and thermal resistance up to 250°C are critical performance metrics. Commercial aircraft demand is concentrated in UAE, Turkey, and Saudi Arabia, contributing USD 700 million collectively. Increasing fleet orders, such as over 600 new aircraft between 2024–2025, reinforce Aviation Adhesives And Sealants market growth.

Military aircraft account for 32% market share, utilizing 390 metric tons of adhesives in 2025. Polyurethane sealants lead with 42% share, epoxy 40%, and silicone 18%. Thermal performance ranges from −55°C to 220°C, with shear strength up to 18 MPa. Military modernization programs in Saudi Arabia and UAE increased procurement by 15% annually. High-frequency performance (up to 480 Hz) and flame-retardant capabilities are key adoption drivers, supporting Aviation Adhesives And Sealants market expansion.

UAV applications represent 20% share, with 280 metric tons produced in 2025. Silicone adhesives account for 48% of usage, epoxy 38%, and polyurethane 14%. UAV penetration in Middle East and Africa grew at 12% CAGR from 2022–2025. Adhesives require thermal stability from −55°C to 200°C and vibration resistance up to 450 Hz. UAV-specific requirements, including lightweight and UV-resistant bonding, drive Aviation Adhesives And Sealants market demand.

Middle East and Africa Aviation Adhesives And Sealants Market Segmentations

Type

- Epoxy

- Polyurethane

- Silicone

Application

- Commercial Aircraft

- Military Aircraft

- UAV

Aviation Adhesives And Sealants Market Regional Outlook

UAE

UAE contributes 21% of regional market share, with production of 320 metric tons in 2025. Commercial aircraft applications dominate 55%, military 30%, UAV 15%. Epoxy adoption is 65%, polyurethane 40%, and silicone 28%. Government initiatives and fleet expansion reinforce Aviation Adhesives And Sealants market growth.

Turkey

Turkey accounts for 18% share, producing 260 metric tons in 2025. Commercial aircraft 50%, military 35%, UAV 15%. Epoxy adhesives lead at 48%, polyurethane 36%, silicone 16%. Growing aviation clusters drive Aviation Adhesives And Sealants market size and demand.

Saudi Arabia

Saudi Arabia holds 17% regional share, producing 245 metric tons in 2025. Commercial aircraft applications represent 52%, military 38%, UAV 10%. High adoption of polyurethane sealants (42%) supports military programs, reinforcing Aviation Adhesives And Sealants market growth.

South Africa

South Africa contributes 12% share, with 170 metric tons production in 2025. Military aircraft dominates 40%, commercial 45%, UAV 15%. Epoxy adhesives 44%, polyurethane 30%, silicone 26%. Regional defense programs drive Aviation Adhesives And Sealants market demand.

Egypt

Egypt accounts for 14% share, producing 200 metric tons. UAV applications increasing at 12% CAGR. Epoxy 42%, polyurethane 34%, silicone 24%. Commercial aircraft demand 50%, military 30%, UAV 20%. Expanding aviation industry reinforces Aviation Adhesives And Sealants market insights.

Nigeria

Nigeria contributes 8% share, producing 120 metric tons. Military aircraft applications dominate 45%, commercial 40%, UAV 15%. Adoption rates: epoxy 40%, polyurethane 35%, silicone 25%. Defense upgrades drive Aviation Adhesives And Sealants market growth.

List of Top Aviation Adhesives And Sealants Companies

- 3M Company

- Henkel AG & Co. KGaA

- H.B. Fuller Company

- Sika AG

- PPG Industries

- LORD Corporation

- Bostik SA

- Huntsman Corporation

- Ashland Global Holdings

- Arkema S.A.

- Dow Inc.

- Permabond LLC

- Master Bond Inc.

- Wacker Chemie AG

- Covestro AG

Top Companies

3M Company

-

Market share: 12%

-

Leading in epoxy and polyurethane adhesives for commercial aircraft, contributing USD 150 million in 2025. 3M leverages R&D investment of 16% of revenue to innovate high-temperature adhesives, UV-resistant silicones, and lightweight bonding materials. Strategic partnerships with UAE and Saudi aerospace firms reinforce Aviation Adhesives And Sealants market positioning and growth.

Henkel AG & Co. KGaA

-

Market share: 10%

-

Dominates military aircraft adhesive supply, with production volume of 110 metric tons in 2025. Advanced polyurethane sealants and epoxy adhesives with shear strength up to 20 MPa and thermal resistance of 250°C provide technical advantage. Henkel’s collaborations in UAV manufacturing and fleet expansion projects solidify Aviation Adhesives And Sealants market leadership in the Middle East and Africa.

Investment Analysis and Opportunities

Investment in Aviation Adhesives And Sealants market is concentrated in commercial aircraft (45%), military aircraft (35%), and UAVs (20%). Regional allocation indicates UAE (22%), Turkey (18%), Saudi Arabia (17%), Egypt (14%), South Africa (12%), and Nigeria (8%). Sectoral investments in R&D account for 15% of total funding, focusing on high-performance adhesives with thermal resistance improvements of 10–15% and shear strength enhancements of 12–18 MPa. M&A agreements between regional manufacturers and global suppliers increased by 18% from 2023–2025, facilitating technology transfer and capacity expansion. Collaborations with defense programs in Saudi Arabia and UAE enhance market penetration. Investments in UAV adhesives are projected to increase by 12% CAGR through 2034, driven by drone manufacturing and lightweight composite adoption. The Aviation Adhesives And Sealants market presents opportunities for both regional and international stakeholders, emphasizing advanced product innovation, regulatory compliance, and defense-oriented applications.

New Product Development

New product development accounts for 20% of total production in 2025, emphasizing high-performance epoxy and polyurethane adhesives. Innovations led to a 15% increase in shear strength and a 10% improvement in thermal tolerance. Development of low-outgassing, UV-resistant silicones enables UAV and military aircraft applications. Continuous R&D ensures product differentiation, supporting Aviation Adhesives And Sealants market growth. Performance testing includes vibration resistance up to 500 Hz and frequency cycling durability, strengthening technical reliability.

Recent Developments

- 2025: 3M launched a new high-temperature epoxy adhesive with 12% increased thermal tolerance, targeting commercial aircraft manufacturing.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Defense Systems and Aerospace Engineering

Larry Hole is a market research analyst with 7–9 years of experience specializing in aerospace and defense markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.