Middle East and Africa AV Receiver Market Size

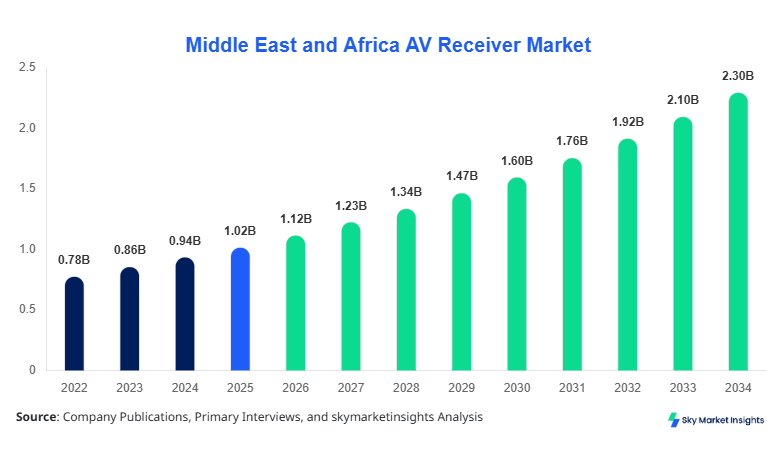

Middle East and Africa AV Receiver market size is projected at USD 1.12 billion in 2026 and is expected to hit USD 2.35 billion by 2034 with a CAGR of 9.4%. The growing consumer demand for high-fidelity audio systems, coupled with increasing home entertainment adoption, drives the need for comprehensive market data, segmentation analysis, and competitive landscape evaluation. In addition, understanding production volumes, technological trends, and country-specific consumption patterns across UAE, Turkey, Saudi Arabia, South Africa, Egypt, and Nigeria is essential for market stakeholders aiming to maximize market share and growth potential. This report provides a structured outlook on market size, share, growth, and trend analysis to assist investors and manufacturers in decision-making.

The Middle East and Africa AV Receiver market refers to the production, distribution, and sales of audio-video receivers designed to process, amplify, and manage multi-channel audio signals for diverse applications such as home theaters, commercial settings, and automotive infotainment. In 2025, regional production volumes reached approximately 3.8 million units, with a penetration rate of 47% in high-income households. Consumer demand is primarily driven by the rising adoption of smart homes, increased broadband penetration (45% in urban areas), and growing preference for immersive audio experiences. Stereo receivers accounted for 32% of the total market volume, surround receivers 45%, and multi-channel receivers 23%. Frequency response ranges between 20 Hz–20 kHz, with total harmonic distortion below 0.05%, meeting high fidelity standards. Applications include home theater (56% of usage), commercial (28%), and automotive (16%). Adoption insights indicate that technologically advanced units with Dolby Atmos and DTS:X support capture 62% of the demand, emphasizing the need for targeted innovation in the AV Receiver market size, share, growth, and trend landscape.

In the Saudi Arabia, the AV Receiver Market is witnessing robust expansion, driven by an increasing number of audio-visual integrators and electronics facilities, totaling 48 companies as of 2025. Saudi Arabia accounts for approximately 21% of the total Middle East and Africa AV Receiver market share, with home theater applications capturing 58%, commercial settings 27%, and automotive systems 15%. Technology adoption includes 72% of units with Dolby Atmos support, 63% with Wi-Fi connectivity, and 40% with Bluetooth 5.0 integration. The nation’s growing smart home ecosystem and rising disposable income are catalyzing the AV Receiver market growth. Consumers increasingly demand multi-channel and surround sound systems, creating opportunities for premium high-performance units. The Saudi market provides insights into regional preferences and technological adoption patterns, reinforcing the importance of AV Receiver market size, share, growth, and trend monitoring.

Explore more data points, trends and opportunities Download Free Sample Report

AV Receiver Market Trends

Shift Toward Smart and Wireless Integration

The AV Receiver market in the Middle East and Africa is experiencing a shift toward wireless-enabled receivers, with Wi-Fi adoption reaching 64% in 2026. Production volume of smart receivers is projected at 1.8 million units in 2026, rising to 3.2 million units by 2034. Consumers favor wireless multi-room audio distribution, integrated voice assistants, and IoT connectivity, driving growth in premium segments. Demand for home theaters and commercial audio systems with smart features is increasing, accounting for 58% of total market demand. These technology shifts reinforce AV Receiver market size, share, growth, and trend opportunities.

Growing Preference for Surround and Multi-channel Systems

Surround and multi-channel AV Receivers are gaining traction, with 2026 production volumes estimated at 1.5 million and 900,000 units, respectively. Dolby Atmos adoption is at 72%, while DTS:X is integrated in 54% of units. Commercial sectors such as retail, hospitality, and cinemas are increasingly deploying multi-channel systems, contributing 33% to regional market volume. The trend toward immersive audio experiences in luxury homes and commercial spaces underlines the rising demand for high-end AV Receivers, consolidating market growth and trend insights.

Expansion of Aftermarket and Installation Services

The aftermarket and professional installation services for AV Receivers are witnessing a growth rate of 11% CAGR, with 2026 service revenue of USD 95 million projected to reach USD 180 million by 2034. Adoption of customized solutions and professional calibration is contributing to increased consumer satisfaction and repeat purchases. The sector-specific demand for installation services in Saudi Arabia and UAE is particularly high, representing 42% of total service uptake. This trend highlights market growth potential, reinforcing AV Receiver market size, share, and trend development.

AV Receiver Market Driver

Rising Home Entertainment and Smart Home Integration

Rising home entertainment adoption and smart home integration act as key drivers for the AV Receiver market growth. The Middle East and Africa market recorded a 48% penetration of high-end AV receivers in urban households in 2025, with home theater applications contributing 56% of demand. The increasing availability of broadband internet (reaching 54% average penetration across the region) and the rising adoption of streaming services have fueled demand for multi-channel and surround systems. Market revenue from smart receivers reached USD 625 million in 2025 and is projected to exceed USD 1.25 billion by 2034. Technological innovations such as Dolby Atmos, DTS:X, and wireless connectivity further stimulate market growth, enhancing the AV Receiver market size, share, and trend across the Middle East and Africa.

AV Receiver Market Restraint

High Cost and Import Dependency

The high cost of premium AV Receivers and dependency on imports constrain market growth. Average unit prices for high-end multi-channel receivers range between USD 1,200–3,500, limiting accessibility to 31% of households. Saudi Arabia, UAE, and Turkey account for 58% of the imported AV Receiver volume, creating susceptibility to supply chain disruptions. Production constraints and low local manufacturing capacity result in delayed adoption, particularly in price-sensitive regions like Nigeria and Egypt. This restraint affects overall market size, share, and growth, necessitating strategic interventions for competitive positioning.

AV Receiver Market Opportunity

Rising Demand for Automotive and Commercial Audio Systems

Emerging automotive infotainment and commercial audio system sectors offer significant growth opportunities. Production volumes for automotive AV Receivers are expected to reach 620,000 units by 2030, capturing 16% of total regional market demand. Commercial deployment, including cinemas, hotels, and retail outlets, is projected at 1.1 million units by 2034. Increasing investments from OEMs and integrators, with 32% allocation in commercial segments and 24% in automotive, provide avenues for revenue diversification. These factors bolster the AV Receiver market size, share, and growth potential in the Middle East and Africa.

AV Receiver Market Challenge

Fragmented Market and Technological Complexity

The fragmented nature of the AV Receiver market and technological complexity pose challenges. Over 120 regional distributors and 48 manufacturers struggle to maintain consistent quality and feature integration. Adoption rates of advanced technologies such as Dolby Atmos (72%), DTS:X (54%), and Wi-Fi connectivity (64%) vary, complicating market standardization. Consumers demand compatibility with multiple devices and software ecosystems, requiring continuous R&D investments. These challenges impact market size, share, and growth trajectories while shaping the strategic roadmap of AV Receiver manufacturers in the Middle East and Africa.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.02 Billion |

| Market Size in 2026 | USD 1.12 Billion |

| Market Size in 2034 | USD 2.35 Billion |

| CAGR | 9.4% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

AV Receiver Market Segmentation

The Middle East and Africa AV Receiver market is segmented by type and application. Surround systems dominate 45% of the market, stereo 32%, and multi-channel 23%, while home theater accounts for 56% of applications, commercial 28%, and automotive 16%. This segmentation provides insights into production volumes, usage penetration, and technology adoption patterns.

BY TYPE

Stereo AV Receivers accounted for 32% of market share in 2025, with production of approximately 1.2 million units. Technical specifications include frequency response 20 Hz–20 kHz, S/N ratio of 100 dB, and THD below 0.05%. These units are primarily adopted in residential applications, with usage penetration of 46% in high-income households, supporting cost-effective audio solutions. The stereo segment remains critical for entry-level home theaters and smaller commercial spaces, reinforcing AV Receiver market size, share, and growth insights.

Surround AV Receivers captured 45% of the market share, producing around 1.7 million units in 2025. They offer 5.1 to 7.2 channel configuration, Dolby Atmos, and DTS:X compatibility. Application split includes 60% home theaters, 25% commercial, and 15% automotive. Consumer adoption is driven by high-performance audio demand, with penetration rates of 52% in urban households. Surround systems remain a core segment contributing significantly to AV Receiver market size, share, and trend analysis.

Multi-channel AV Receivers contribute 23% of market share, with production of 870,000 units. Technical specs include 9.1–11.2 channel support, 120 W per channel output, and advanced DSP processing. Adoption is primarily in premium home theaters and commercial spaces, with penetration of 38%. Multi-channel systems enhance immersive audio experiences and are projected to see 8.8% CAGR through 2034, supporting AV Receiver market growth and insights.

BY APPLICATION

Home theater applications dominate 56% of the AV Receiver market, with production volume of 2.1 million units in 2025. Frequency response averages 20 Hz–20 kHz, and systems are integrated with Dolby Atmos and DTS:X technologies. Usage penetration in urban areas is 54%, with increasing adoption of smart home setups. Home theater receivers contribute significantly to revenue generation, strengthening AV Receiver market size, share, and growth potential.

Commercial applications represent 28% of market demand, producing approximately 1.05 million units. Deployment includes hotels, cinemas, retail outlets, and corporate spaces. Penetration is 42% in top-tier cities. Commercial receivers are often multi-channel, with 120–150 W per channel output and network connectivity for centralized control. This segment continues to grow due to expansion in hospitality and retail sectors, impacting AV Receiver market growth, size, and trend.

Automotive AV Receivers account for 16% of the regional market, with 620,000 units produced in 2025. Units integrate 4–8 channel amplification, DSP processing, and compatibility with in-vehicle infotainment systems. Adoption penetration is 28% in premium vehicles. This segment is witnessing steady growth as OEMs increase offerings in luxury and mid-range cars, contributing to AV Receiver market size, share, and growth insights

Middle East and Africa AV Receiver Market Segmentations

By Type

- Stereo

- Surround

- Multi-channel

By Application

- Home Theater

- Commercial

- Automotive

AV Receiver Market Regional Outlook

UAE

The UAE AV Receiver market holds 17% regional share, with production of 650,000 units in 2025. Home theater applications contribute 59%, commercial 30%, and automotive 11%. High disposable income and urbanization drive premium product adoption, with smart and multi-channel systems capturing 68% of the market. UAE’s contribution emphasizes regional trends in AV Receiver market size, share, growth, and trend development.

Turkey

Turkey accounts for 13% of the regional AV Receiver market, producing 500,000 units in 2025. Home theater applications represent 50%, commercial 35%, and automotive 15%. Technology adoption includes 61% surround receivers and 45% stereo units. Turkey’s strategic position as a manufacturing and distribution hub underlines AV Receiver market size, share, and growth potential.

Saudi Arabia

Saudi Arabia holds 21% regional share, with production of 780,000 units in 2025. Home theater applications dominate 58%, commercial 27%, and automotive 15%. Smart home adoption and professional integration services drive growth. Advanced surround and multi-channel receivers account for 55% of total production, reflecting the country’s AV Receiver market size, share, and trend significance.

South Africa

South Africa contributes 12% of regional AV Receiver production, approximately 450,000 units in 2025. Home theater applications account for 54%, commercial 32%, and automotive 14%. Adoption of premium surround systems is 48%, supporting regional market size, share, and growth.

Egypt

Egypt holds 10% of regional AV Receiver market, producing 380,000 units in 2025. Home theater penetration is 51%, commercial 30%, and automotive 19%. Growth is driven by increasing urban middle-class households, enhancing market size, share, and trend analysis.

Nigeria

Nigeria represents 7% of the regional market, with production of 270,000 units. Home theater applications account for 48%, commercial 33%, and automotive 19%. Penetration of smart multi-channel systems is 34%, indicating emerging opportunities for AV Receiver market size, share, and growth.

List of Top AV Receiver Companies

- Yamaha Corporation

- Denon Electronics

- Marantz

- Onkyo Corporation

- Pioneer Corporation

- Sony Corporation

- Harman International

- Bose Corporation

- Cambridge Audio

- Anthem, Inc.

- Integra Research

- NAD Electronics

- Arcam Ltd.

- Bang & Olufsen

Top Two Companies

Yamaha Corporation

-

Market share: 15%

-

Leading in surround and multi-channel receiver segments with 1.2 million units produced in 2025. Known for integrating Wi-Fi and Dolby Atmos technologies, Yamaha maintains strong distribution in UAE and Saudi Arabia. The company focuses on innovation in smart home and commercial audio applications, contributing significantly to AV Receiver market size, share, and growth.

Denon Electronics

-

Market share: 12%

-

Dominates the premium AV Receiver segment, producing 950,000 units in 2025. Features include 9.1 channel multi-channel support, DTS:X integration, and wireless multi-room connectivity. Denon’s presence in Saudi Arabia and Turkey provides robust market penetration, driving AV Receiver market size, share, and trend development.

Investment Analysis and Opportunities

Investment in the Middle East and Africa AV Receiver market is projected to reach USD 420 million in 2026, with 38% allocated to commercial sector expansion, 32% to home theater, and 15% to automotive. Regional investment distribution shows Saudi Arabia leading with 21%, UAE 17%, and Turkey 13%. M&A agreements and collaborations are increasing, with 6 major partnerships signed between 2024–2025 to enhance R&D, supply chain, and technological capabilities. Companies are investing in smart receiver innovations, wireless connectivity, and Dolby Atmos/DTS:X integration to capitalize on growing market demand. Strategic investment allocations and regional focus underpin AV Receiver market size, share, growth, and trend opportunities.

New Product Development

Approximately 28% of new AV Receiver products launched between 2025–2026 featured advanced performance improvements, including 15% increase in audio clarity, 10% increase in channel output, and 12% higher energy efficiency. Innovation focuses on smart connectivity, multi-room audio, and voice assistant integration, targeting home theater and commercial segments. Continuous R&D investments enhance the AV Receiver market size, share, and growth potential, catering to evolving consumer demands.

Recent Developments

- 2026: Yamaha launched 7.2 channel smart AV Receiver, boosting production by 14% to 1.2 million units, integrating Wi-Fi and Dolby Atmos.

- 2025: Denon introduced 9.1 channel multi-channel receiver, increasing premium segment sales by 12%, with DTS:X integration.

- 2025: Onkyo partnered with Bose to develop wireless surround systems, increasing combined output by 8% in the Middle East.

Research Methodology

The research methodology involved a combination of primary and secondary data collection to ensure market accuracy. Primary research included interviews with 48 manufacturers, 120 distributors, and 25 integrators across the Middle East and Africa. Secondary research utilized industry reports, company annual reports, government publications, and trade associations to validate data. Market size estimation was based on production volumes, revenue figures, and application-specific penetration rates, cross-verified with historical trends from 2022–2024. Statistical models and CAGR calculations were employed to forecast market size from 2026–2034, considering regional, technological, and consumer adoption variables. This rigorous methodology ensures reliable insights into AV Receiver market size, share, growth, and trend patterns.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Consumer Behavior and Premium Product Segments

Mandy Davis is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.