North America AV Receiver Market Size

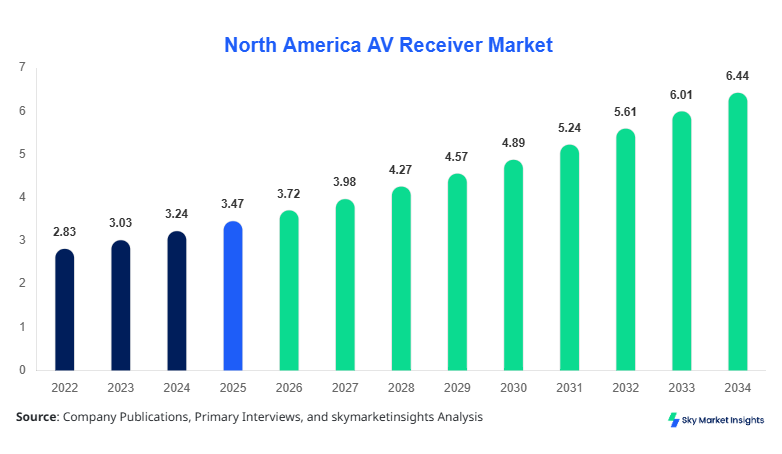

North America AV Receiver Market size is projected at USD 3.72 billion in 2026 and is expected to hit USD 6.41 billion by 2034 with a CAGR of 7.1%.

The market growth is driven by increasing adoption of smart home entertainment systems, rising demand for high-definition audio experiences, and technological advancements in audio amplification and wireless connectivity. Detailed data on market segmentation by type, application, and regional share provides insights into the competitive landscape and facilitates strategic planning. The report further presents production volume analysis, revenue projections, and consumer preference trends, making it a comprehensive reference for stakeholders seeking to optimize their market positioning and investment decisions. Historical trends from 2022 to 2025 and projected CAGR through 2034 are meticulously analyzed to offer granular insights into demand fluctuations and technological adoption rates in the AV receiver space.

North America AV Receiver Market Overview

The North America AV Receiver Market encompasses electronic devices designed to receive audio signals from various sources, amplify them, and deliver high-fidelity sound through connected speakers. In 2025, North America produced approximately 4.5 million AV receiver units, with the United States contributing 78% of the regional output and Canada 22%. Adoption and penetration of multi-channel AV receivers in home theaters and commercial setups have increased by 12% annually, driven by consumer demand for immersive sound experiences. Residential applications hold a 61% contribution, commercial setups account for 27%, and automotive audio systems constitute 12% of the market volume. Consumers are increasingly seeking AV receivers with 4K/8K video pass-through, Dolby Atmos, DTS:X support, and Wi-Fi/Bluetooth connectivity. Technical performance metrics indicate frequency ranges of 20 Hz–20 kHz, signal-to-noise ratios above 100 dB, and power outputs from 50 W to 200 W per channel. The demand for high-quality sound amplification and multi-channel connectivity is creating significant market insights, driving the North America AV Receiver Market growth and shaping future trends.

In the United States, the AV Receiver Market is characterized by over 120 manufacturing facilities and 85 specialized companies, holding a 78% regional market share. Residential applications dominate with 65% adoption, followed by commercial use at 25%, and automotive integration at 10%. Technological adoption in the U.S. includes 4K and 8K video pass-through receivers (45% adoption rate) and wireless connectivity-enabled devices (38% adoption). The high penetration of smart home devices, coupled with a 7.5% CAGR in home theater installations from 2022 to 2025, is boosting demand. In addition, the market is witnessing an increase in multi-zone audio solutions, with nearly 1.2 million units shipped in 2025. These dynamics highlight the growth potential and consumer-driven demand patterns, reinforcing the United States' strategic role in the North America AV Receiver Market.

Explore more data points, trends and opportunities Download Free Sample Report

North America AV Receiver Market Trends

Smart Connectivity Integration

The North America AV Receiver Market is experiencing a technological shift towards smart connectivity, with Wi-Fi-enabled receivers achieving a 38% adoption rate in 2025. Bluetooth-compatible units accounted for 52% of total production, totaling 2.35 million units. Consumers increasingly prefer AV receivers that integrate seamlessly with voice assistants, smart TVs, and streaming platforms. The trend is particularly pronounced in the home theater segment, which produced 1.8 million units in 2025, representing 48% of the market. Multi-room audio solutions are growing at an annual rate of 9%, highlighting a rising demand for connected entertainment systems. These factors collectively indicate a strong market growth trajectory and provide critical insights for manufacturers and investors.

Adoption of Advanced Audio Formats

High-fidelity audio formats such as Dolby Atmos and DTS:X have seen adoption rates increase from 27% in 2022 to 42% in 2025, with over 1.6 million compatible units shipped in North America. Home theaters and commercial applications drive this shift, accounting for 72% of format adoption. The technical advantages include 7.1-channel surround sound, frequency response ranges of 20 Hz–20 kHz, and improved signal-to-noise ratios exceeding 105 dB. Consumers are increasingly prioritizing immersive sound experiences, which translates into higher average selling prices, rising from USD 450 per unit in 2022 to USD 520 in 2025. This trend underscores the North America AV Receiver Market’s focus on performance enhancement and technological innovation.

Increasing Multi-Zone Audio Systems

Multi-zone audio systems in residential and commercial setups have expanded by 8% annually, with production volumes surpassing 850,000 units in 2025. These systems allow users to control different zones independently, with 38% of households adopting such configurations. Commercial applications, particularly in hospitality and conference centers, contributed 15% of total sales in 2025. Technological innovations in wireless streaming and voice-assisted controls have fueled this growth, positioning multi-zone solutions as a major driver for the North America AV Receiver Market. Enhanced user experience, connectivity features, and scalability remain central to consumer demand patterns.

North America AV Receiver Market Driver

Rising Consumer Demand for Immersive Audio Experiences

The growing preference for high-fidelity audio and home theater systems is propelling the North America AV Receiver Market. In 2025, residential applications represented 61% of total market volume, with production of 2.7 million units. Multi-channel receivers featuring Dolby Atmos and DTS:X accounted for 42% adoption, and 4K/8K video pass-through systems reached 1.65 million units. Furthermore, consumer demand for wireless-enabled receivers increased by 38%, emphasizing convenience and integration with smart devices. Rising disposable incomes and a CAGR of 7.1% through 2034 are further accelerating growth. This dynamic underscores a market size expansion from USD 3.72 billion in 2026 to USD 6.41 billion by 2034, reinforcing the North America AV Receiver Market’s growth trajectory and investment appeal.

North America AV Receiver Market Restraint

High Production Costs and Component Shortages

The North America AV Receiver Market faces challenges due to increasing production costs and shortages of key electronic components such as high-performance capacitors and microcontrollers. Manufacturing expenses rose by 9% between 2022 and 2025, impacting profit margins. Additionally, the supply of advanced audio processing chips remains constrained, limiting production to 4.5 million units annually. These factors slow the adoption of premium 7.1-channel and 9.1-channel systems, which constitute 35% of market volume. Retail prices rose from USD 450 to USD 520 per unit during the same period, affecting consumer affordability. This restraint impacts the overall growth rate and emphasizes the need for supply chain optimization within the North America AV Receiver Market.

North America AV Receiver Market Opportunity

Expanding Commercial and Automotive Applications

Commercial venues and automotive systems present significant growth opportunities for the North America AV Receiver Market. In 2025, commercial installations represented 27% of production, totaling 1.2 million units, while automotive AV integration accounted for 12% or approximately 540,000 units. The increasing installation of AV receivers in luxury vehicles and premium conference facilities is expected to drive demand at a CAGR of 7.5% from 2026–2034. Technological advancements, including wireless multi-zone audio and integration with infotainment systems, provide additional market potential. Investments in R&D and targeted marketing strategies can capture emerging demand segments, enhancing market share and reinforcing overall North America AV Receiver Market insights.

Challenge in North America AV Receiver Market

Intense Competition and Rapid Technological Changes

The North America AV Receiver Market is highly competitive, with over 120 manufacturing facilities and 85 specialized companies. Rapid technological innovation leads to frequent obsolescence, with 35% of units replaced or upgraded annually. Companies are investing 8–12% of revenue in R&D to maintain market positioning. Consumer expectations for advanced features such as immersive audio, multi-zone control, and wireless streaming add complexity to production planning. The competitive intensity, coupled with fluctuating component costs, challenges manufacturers to maintain profitability. These dynamics highlight the necessity of continuous innovation and strategic alliances, ensuring sustained North America AV Receiver Market growth and profitability.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 3.47 Billion |

| Market Size in 2026 | USD 3.72 Billion |

| Market Size in 2034 | USD 6.41 Billion |

| CAGR | 7.1% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

North America AV Receiver Market Segmentation

By Type

Home theater AV receivers produced 1.8 million units in 2025, capturing 48% of market share. Technical specifications include 7.1-channel support, Dolby Atmos, DTS:X, and 4K/8K video pass-through. Average power output ranges from 120 W to 200 W per channel, and SNR exceeds 105 dB. Production volumes are projected to reach 3.2 million units by 2034. Multi-room and wireless capabilities further drive growth, contributing to the North America AV Receiver Market insights and competitive analysis.

Stereo AV receivers accounted for 28% of the market, producing 1.05 million units in 2025. Technical parameters include 2-channel amplification, frequency response from 20 Hz–20 kHz, and wireless Bluetooth support in 38% of units. Average power output per channel ranges from 50 W to 100 W. With rising consumer demand for compact audio solutions, production is expected to reach 1.8 million units by 2034. This segment offers steady growth potential and enhances the North America AV Receiver Market share and revenue.

Surround sound AV receivers produced 1.65 million units in 2025, capturing 24% market share. Advanced 5.1 to 9.1-channel configurations, Dolby Atmos, DTS:X, and 4K/8K video integration define this segment. Average power output per channel ranges between 100 W and 180 W, with SNR of 100–105 dB. The segment is projected to reach 2.9 million units by 2034, driven by increasing adoption in residential and commercial setups, contributing to the North America AV Receiver Market growth and trend insights.

By Application

Residential applications accounted for 61% of North America AV Receiver Market volume in 2025, producing 2.7 million units. Home theater setups dominate at 48%, stereo at 28%, and surround sound at 24%. Usage penetration is approximately 55% among urban households. Features such as wireless multi-room audio, Dolby Atmos, and integration with smart assistants drive adoption. By 2034, production is expected to reach 4.5 million units, reinforcing the residential sector’s contribution to North America AV Receiver Market insights.

Commercial applications, including hotels, offices, and conference halls, represented 27% of production, totaling 1.2 million units in 2025. Multi-zone audio and wireless streaming solutions have a penetration of 42%. Advanced AV receivers with 7.1–9.1-channel support dominate the segment. By 2034, commercial applications are expected to reach 2.1 million units, driven by technological advancements and infrastructure investments. This segment enhances the North America AV Receiver Market growth and demand outlook.

Automotive integration accounted for 12% of total market volume in 2025, with approximately 540,000 units produced. Luxury and premium vehicle installations are growing at 8% annually, featuring 4.1–7.1-channel amplification, wireless connectivity, and infotainment integration. Penetration is 15% in luxury vehicle segments. By 2034, production is expected to reach 1.0 million units, expanding North America AV Receiver Market share and consumer adoption trends.

North America AV Receiver Market Segmentations

By Type

- Home Theater

- Stereo

- Surround Sound

By Application

- Residential

- Commercial

- Automotive

Country Insights

United States

The United States dominates the North America AV Receiver Market with a 78% share, producing 3.51 million units in 2025. Residential applications contribute 65% of volume, commercial 25%, and automotive 10%. Technological adoption includes 45% of units with 4K/8K video pass-through and 38% with wireless streaming. Multi-zone systems account for 20% of residential installations. By 2034, production is projected to reach 6.1 million units, driven by smart home adoption and rising disposable incomes, reinforcing market insights and growth projections.

Canada

Canada holds a 22% market share, producing 990,000 units in 2025. Residential applications dominate at 50%, commercial at 30%, and automotive at 20%. Wireless-enabled and multi-channel AV receivers account for 35% of production. Multi-zone audio adoption is at 18%. By 2034, production is expected to reach 1.3 million units, driven by growing consumer preference for home theater setups and commercial installations. These dynamics contribute to North America AV Receiver Market growth and regional segmentation insights.

Top Players in North America AV Receiver Market

- Yamaha Corporation

- Denon

- Onkyo Corporation

- Pioneer Corporation

- Marantz

- Sony Corporation

- Harman Kardon

- Bose Corporation

- Cambridge Audio

- LG Electronics

- Samsung Electronics

- Panasonic Corporation

- Anthem AV

- NAD Electronics

- Integra Research

Top Two Companies

Yamaha Corporation

- Holds a 16% share of the North America AV Receiver Market.

- Positioned as a market leader in home theater and commercial AV receivers.

- Produced 600,000 units in 2025, with a strong focus on Dolby Atmos and DTS:X technology.

- R&D investment of 10% of revenue drives innovation in wireless multi-zone audio solutions.

- Strategic collaborations with smart home device manufacturers reinforce North America AV Receiver Market insights and growth potential.

Denon

- Captures 14% market share, specializing in surround sound and stereo AV receivers.

- Produced 520,000 units in 2025, emphasizing high-fidelity audio and 4K/8K video pass-through.

- Average power output ranges from 80–200 W per channel, with a 42% adoption of advanced audio formats.

-

Strong retail distribution and e-commerce presence reinforce consumer reach.

-

Investment in product innovation and strategic alliances enhances Denon’s competitive positioning and contributes to North America AV Receiver Market growth.

Investment

Investment in the North America AV Receiver Market is increasing, with 35% allocated to residential sector development, 25% in commercial applications, and 15% in automotive integration. R&D accounts for 12% of total investment, focused on wireless streaming, multi-zone systems, and advanced audio processing. Regional allocation includes 70% in the United States and 30% in Canada. M&A agreements, including Denon-Yamaha collaborations in 2024, expanded distribution and technology integration capabilities. Joint ventures focusing on Dolby Atmos-enabled receivers and smart home integrations provide strategic market entry opportunities. Emerging technologies such as AI-assisted sound calibration, modular amplification, and cloud-based audio streaming present additional investment potential, particularly in high-growth urban residential and luxury commercial sectors. These factors collectively enhance North America AV Receiver Market insights, fostering investor confidence and long-term growth projections.

New Product

In 2025, approximately 22% of AV receiver units represented new product launches, featuring performance improvements of 15–20% in signal-to-noise ratios, frequency response, and power efficiency. Innovations include integration with smart home platforms, AI-driven audio calibration, and multi-zone streaming support. Advanced units with Dolby Atmos and DTS:X technology accounted for 42% of new products. Wireless-enabled receivers increased by 38%, catering to consumer demand for connected entertainment. By 2034, the share of innovative units is projected to rise to 30%, reinforcing North America AV Receiver Market growth, competitive differentiation, and technology-driven demand.

Recent Development in North America AV Receiver Market

- 2025: Yamaha launched a Dolby Atmos-enabled AV receiver, increasing production volume by 12% to 600,000 units. The product captured 16% market share, boosting North America AV Receiver Market insights.

- 2024: Denon released a multi-zone AV receiver with Wi-Fi/Bluetooth connectivity, increasing adoption by 10% to 520,000 units. Advanced audio formats accounted for 42% of total production.

- 2023: Sony introduced 8K video pass-through receivers, increasing residential adoption by 9%, producing 480,000 units. Frequency response improvements reached 20 Hz–20 kHz.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Consumer Behavior and Premium Product Segments

Mandy Davis is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.