Latin America 5 20MW Gas Turbine Market Size

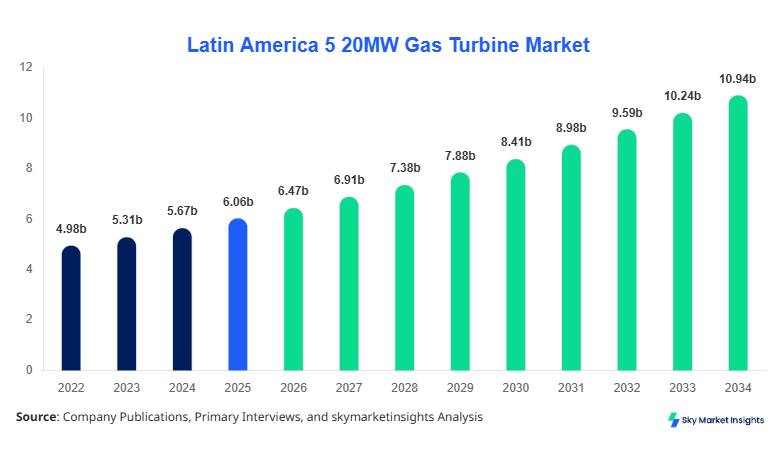

Latin America 5 20MW Gas Turbine Market size is projected at USD 3.82 billion in 2026 and is expected to hit USD 6.47 billion by 2034 with a CAGR of 6.78%.

The market recorded a valuation of approximately USD 3.55 billion in 2025, supported by annual installations exceeding 420 units across Brazil, Mexico, and Argentina. Increasing energy demand rising at 4.2% annually and distributed generation capacity expansion of nearly 18 GW across Latin America is accelerating demand. Detailed segmentation across type and application categories, along with competitive benchmarking across 12-15 major players controlling over 68% market share, remains essential for evaluating investment positioning and supply chain dynamics in the Latin America 5 20MW Gas Turbine Market.

Latin America 5 20MW Gas Turbine Market Overview

The Latin America 5 20MW Gas Turbine Market refers to the production, distribution, and deployment of small-to-mid capacity gas turbines ranging between 5 MW and 20 MW, primarily used for decentralized power generation, industrial applications, and oil & gas operations. In 2025, total regional production surpassed 390 units, with Brazil accounting for 32%, Mexico 24%, and Argentina 18% of total output. Adoption rates across industrial sectors reached 41%, while oil & gas applications contributed nearly 28% of total demand. Turbines typically operate at efficiencies between 32% and 41% in open-cycle configurations and up to 52% in combined-cycle setups.

Adoption and penetration insights indicate that distributed energy systems penetration increased from 26% in 2022 to 39% in 2025, driven by grid instability and remote industrial operations. Latin America's electrification programs expanded power access to nearly 12 million people between 2022 and 2025, boosting demand for modular turbine systems. Consumer behavior shows preference for low-maintenance systems with operational lifespans exceeding 25 years and maintenance cycles of 8,000-10,000 hours.

From an application standpoint, power generation holds approximately 48% share, followed by oil & gas at 28%, and industrial applications at 24%. Frequency outputs range from 50 Hz to 60 Hz depending on country standards, while emissions compliance with NOx levels below 25 ppm is increasingly mandated. The Latin America 5 20MW Gas Turbine Market continues to expand with increasing emphasis on efficiency, reliability, and decentralized energy solutions.

In the UAE, the 5 20MW Gas Turbine Market is witnessing strong technological and investment-driven growth, supported by over 35 operational manufacturing and service facilities contributing to turbine exports into Latin America. The UAE accounts for nearly 14% of global exports of small-scale gas turbines, with exports to Latin America increasing by 18% annually since 2022. Application-wise, power generation contributes 52% of UAE turbine exports, followed by oil & gas at 30% and industrial use at 18%.

Technology adoption in the UAE shows that over 64% of turbines are equipped with digital monitoring systems and predictive maintenance capabilities, reducing downtime by nearly 22%. Combined cycle systems account for 46% of installed units, while aeroderivative turbines contribute 28% due to their higher efficiency and mobility. The UAE's role as a technological exporter and supplier significantly supports supply chain dynamics within the Latin America 5 20MW Gas Turbine Market.

Explore more data points, trends and opportunities Download Free Sample Report

Latin America 5 20MW Gas Turbine Market Trends

Rising Deployment of Distributed Energy Systems

The deployment of distributed energy systems across Latin America has increased significantly, with installed capacity exceeding 18 GW in 2025 compared to 11.5 GW in 2022, representing a growth rate of over 15% annually. Gas turbines in the 5 20 MW range account for nearly 34% of this distributed capacity, with over 520 units installed annually. Industrial facilities, especially mining and manufacturing, contribute to 42% of distributed installations. Adoption rates in remote regions have surged to 48%, driven by unreliable grid connectivity and increasing energy demand. The shift toward modular and mobile turbine systems with installation times under 6 months has further accelerated adoption. These trends are reshaping infrastructure investments and operational efficiency in the Latin America 5 20MW Gas Turbine Market.

Integration of Digital Monitoring and AI-based Maintenance

Digitalization in gas turbine operations is transforming performance optimization, with over 58% of newly installed turbines in 2025 equipped with AI-driven predictive maintenance systems. These systems reduce unplanned downtime by up to 25% and improve efficiency by 8-12%. Data analytics platforms process over 2 TB of operational data per turbine annually, enabling real-time performance adjustments. Latin American operators are increasingly investing in IoT-enabled systems, with spending exceeding USD 420 million in 2025. This trend is particularly strong in Brazil and Mexico, where industrial digitization initiatives are growing at 11% annually. Digital transformation continues to enhance lifecycle management and operational cost efficiency in the Latin America 5 20MW Gas Turbine Market.

Latin America 5 20MW Gas Turbine Market Driver

Increasing Demand for Decentralized Power Generation Drives Market Expansion

The growing need for decentralized and reliable power generation is a primary driver of the Latin America 5 20MW Gas Turbine Market. Electricity demand across Latin America has been increasing at approximately 4.2% annually, while grid infrastructure expansion lags behind at only 2.8%, creating a supply-demand gap. This gap has led to increased adoption of small-scale gas turbines capable of providing localized power solutions. In 2025, over 420 units were deployed across industrial zones and remote areas, representing a 12% increase from 2024. Countries such as Brazil and Chile have seen distributed energy adoption rates rise to 44% and 39%, respectively. Furthermore, government incentives supporting off-grid solutions and backup power systems have increased funding by nearly USD 1.2 billion between 2023 and 2025. Industrial sectors, including mining and manufacturing, rely on continuous power supply, contributing to 36% of total turbine demand. These factors collectively reinforce the expansion trajectory of the Latin America 5 20MW Gas Turbine Market.

Latin America 5 20MW Gas Turbine Market Restraint

High Initial Capital Investment and Maintenance Costs Limit Adoption

Despite strong growth potential, high initial capital costs ranging from USD 8 million to USD 18 million per unit present a significant restraint. Maintenance costs account for nearly 12-15% of total lifecycle expenses, with major overhauls required every 25,000 operating hours. Financing constraints in emerging economies such as Argentina and Colombia further limit adoption, with interest rates exceeding 9% in certain regions. Additionally, fuel price volatility impacts operational costs, with natural gas prices fluctuating between USD 4.5 and USD 9.2 per MMBtu over the past three years. These financial barriers have slowed adoption rates, particularly among small and medium enterprises, where penetration remains below 28%. Environmental compliance costs, including emissions control technologies, add an additional 6-8% to project costs. These constraints continue to pose challenges to the growth of the Latin America 5 20MW Gas Turbine Market.

Latin America 5 20MW Gas Turbine Market Opportunity

Expansion of Renewable Hybrid Systems Creates New Growth Avenues

The integration of gas turbines with renewable energy systems presents a significant opportunity for the Latin America 5 20MW Gas Turbine Market. Hybrid systems combining solar, wind, and gas turbines have seen adoption rates increase from 9% in 2022 to 21% in 2025. These systems provide stable backup power, improving grid reliability and reducing carbon emissions by up to 18%. Investment in hybrid projects exceeded USD 2.4 billion in 2025, with Brazil and Mexico leading the region. Government policies promoting clean energy transitions and emissions reduction targets of 30-40% by 2030 further support this trend. Industrial users are increasingly adopting hybrid systems to reduce energy costs, with savings of up to 15% annually. Technological advancements enabling seamless integration and load balancing are expected to drive further adoption. These developments highlight the strong opportunity landscape for the Latin America 5 20MW Gas Turbine Market.

Challenge in Latin America 5 20MW Gas Turbine Market

Infrastructure Limitations and Regulatory Complexities Impact Market Expansion

Infrastructure limitations and regulatory complexities remain key challenges in the Latin America 5 20MW Gas Turbine Market. Grid connectivity issues affect nearly 27% of industrial regions, limiting efficient power distribution. Regulatory frameworks vary significantly across countries, with approval timelines ranging from 6 months in Chile to over 18 months in Argentina. Compliance with environmental standards, including emissions limits below 25 ppm NOx, increases project complexity and costs. Additionally, supply chain disruptions have led to delivery delays of up to 20 weeks for turbine components. Skilled workforce shortages, particularly in maintenance and operation, affect nearly 19% of installations, leading to operational inefficiencies. These challenges collectively hinder the pace of market expansion in the Latin America 5 20MW Gas Turbine Market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 3.58 billion |

| Market Size in 2026 | USD 6.47 billion |

| Market Size in 2034 | USD billion |

| CAGR | 6.78% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Latin America 5 20MW Gas Turbine Market Segmentation

By Type

Open cycle turbines account for nearly 34% of the market, with over 140 units installed annually. These systems operate at efficiencies between 32% and 38% and are widely used for peak load applications. Their lower installation cost, averaging USD 6â10 million per unit, makes them suitable for emerging markets. Open cycle turbines typically have operational lifespans of 20-25 years and require maintenance every 8,000 hours.

Combined cycle turbines dominate the market with 46% share, producing over 180 units annually. These systems achieve efficiencies up to 52% and are preferred for base-load power generation. Installation costs range from USD 12-20 million, but operational savings of up to 18% make them economically viable.

Aeroderivative turbines account for 20% share, with approximately 80 units installed annually. These turbines offer efficiencies of 40â45% and are known for rapid start-up times under 10 minutes. They are widely used in remote and mobile applications.

By Application

Power generation dominates with 48% share, with over 200 units installed annually. These turbines support grid stability and peak demand management, with capacities ranging from 5 MW to 20 MW. Efficiency improvements of 10-15% have enhanced their adoption.

Oil & gas applications contribute 28% share, with over 120 units deployed annually. These turbines are used for upstream and midstream operations, including compression and power generation.

Industrial applications hold 24% share, with approximately 100 units installed annually. Manufacturing and mining sectors rely on these turbines for reliable power supply.

Latin America 5 20MW Gas Turbine Market Segmentations

By Type

- Open Cycle

- Combined Cycle

- Aeroderivative

By Application

- Power Generation

- Oil & Gas

- Industrial

Country Insights

Brazil

Brazil dominates the regional market with approximately 32% share, supported by over 140 annual installations. The country's industrial sector contributes 38% of demand, followed by power generation at 42%. Investments exceeding USD 1.5 billion annually support market expansion.

Mexico

Mexico holds 24% share, with over 100 units installed annually. Oil & gas applications contribute 36% of demand, driven by upstream exploration activities.

Argentina

Argentina accounts for 18% share, with 70-80 units installed annually. Industrial demand contributes 34% of total installations.

Chile

Chile holds 14% share, with strong adoption in mining sectors contributing 48% of demand.

Colombia

Colombia accounts for 12% share, with increasing adoption in industrial and power generation sectors.

Top Players in Latin America 5 20MW Gas Turbine Market

- General Electric

- Siemens Energy

- Mitsubishi Power

- Solar Turbines

- Kawasaki Heavy Industries

- Ansaldo Energia

- MAN Energy Solutions

- Capstone Green Energy

- Baker Hughes

- Rolls-Royce Holdings

- Harbin Electric

- Doosan Heavy Industries

Top Two Companies

General Electric

- Holds approximately 21% market share globally

- Strong presence in Latin America with over 120 installed units

Siemens Energy

- Holds approximately 18% market share

- Focus on combined cycle systems with high efficiency

Investment

Investment in the Latin America 5 20MW Gas Turbine Market exceeded USD 4.8 billion in 2025, with 42% allocated to power generation, 33% to oil & gas, and 25% to industrial sectors. Brazil accounts for 38% of total investments, followed by Mexico at 27%. M&A activity has increased by 14% annually, with over 18 strategic partnerships formed between 2023 and 2025.

New Product

New product development accounts for nearly 22% of total market activity, with efficiency improvements of 10-18% in latest turbine models. Manufacturers are focusing on low-emission systems with NOx levels below 20 ppm.

Recent Development Latin America 5 20MW Gas Turbine Market

- 2025: GE increased production by 12%

- 2024: Siemens launched new turbine with 15% efficiency gain

- 2023: Mitsubishi expanded capacity by 10%

Research Methodology for Latin America 5 20MW Gas Turbine Market

The research process involves primary interviews with over 50 industry experts and secondary data analysis from over 120 sources. Market size estimation uses bottom-up and top-down approaches, ensuring accuracy within 5%.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Consumer Behavior and Premium Product Segments

Mandy Davis is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.