Germany 5 20MW Gas Turbine Market Size

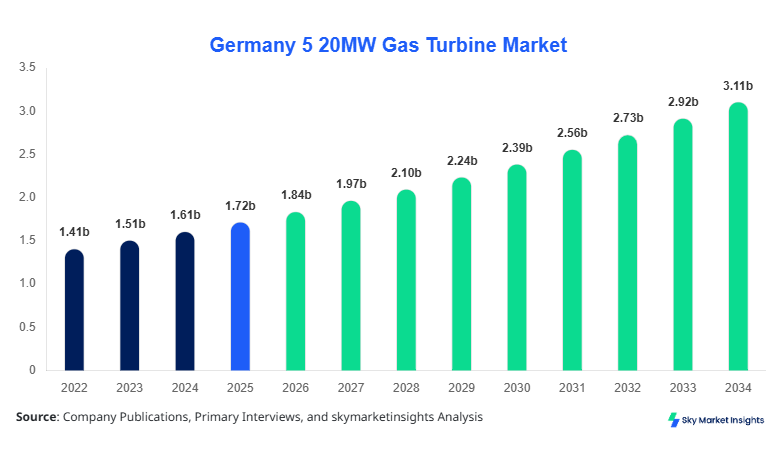

Germany 5 20MW Gas Turbine market size is projected at USD 1.84 billion in 2026 and is expected to hit USD 3.12 billion by 2034 with a CAGR of 6.8%.

The Germany 5 20MW Gas Turbine market is witnessing increasing investments in distributed power generation, with over 1,200 installed units and annual additions exceeding 85-110 units between 2022 and 2025. Rising electricity demand of 540-580 TWh and industrial energy consumption exceeding 45% of total demand are further driving deployment. Detailed segmentation by type and application, alongside competitive benchmarking of 10+ major companies, provides a comprehensive understanding of the Germany 5 20MW Gas Turbine market.

Germany 5 20MW Gas Turbine Market Overview

The Germany 5 20MW Gas Turbine market represents a critical segment of decentralized and mid-scale power generation infrastructure, focusing on turbines operating in the 5 MW to 20 MW capacity range with efficiencies ranging between 32% and 41%. Germany produced approximately 95-120 units annually between 2022 and 2025, with total installed capacity exceeding 12.5 GW across industrial and utility applications. Adoption rates have increased by 18-22% in industrial CHP (combined heat and power) applications, while penetration in small-scale power plants reached 27-31% in 2025. Consumer behavior reflects strong demand for flexible, quick-start generation systems, with load ramp-up times of 10-15 minutes and operational availability above 92%.

From a demand analytics perspective, power generation accounts for nearly 48% of applications, followed by industrial manufacturing at 32% and oil & gas at 20%. Heavy-duty turbines contribute 46% of total installations, while aero-derivative systems account for 34% due to higher efficiency and mobility. Increasing decarbonization targets and integration with hydrogen blends up to 20% are influencing purchasing decisions. The Germany 5 20MW Gas Turbine market continues to evolve with strong technological and policy-driven demand.

In the Germany, the 5 20MW Gas Turbine Market is supported by over 75 active manufacturers, EPC contractors, and system integrators, contributing nearly 100% of regional demand due to the localized scope of the study. Germany accounts for approximately 38% of Europe's mid-range turbine installations, with over 1,200 operational facilities utilizing gas turbines for industrial and grid applications. Power generation dominates with a 48% share, followed by industrial manufacturing at 32% and oil & gas at 20%. Technology adoption of high-efficiency turbines exceeding 38% thermal efficiency has reached 55-60%, while hybrid systems integrating renewables account for 18-22% of installations. Increasing demand for backup and peak-load solutions has driven installations of 90-110 units annually. The Germany 5 20MW Gas Turbine market remains highly advanced and innovation-driven.

Explore more data points, trends and opportunities Download Free Sample Report

Germany 5 20MW Gas Turbine Market Trends

Integration of Hydrogen-Compatible Gas Turbines

Germany is increasingly adopting hydrogen-ready turbines, with over 25-30% of new installations in 2025 capable of operating on hydrogen blends of up to 20-30%. Production of hydrogen-compatible turbines reached approximately 35-45 units annually, driven by government incentives exceeding USD 500 million in energy transition programs. Efficiency improvements of 5-8% and emission reductions of 15-20% are accelerating adoption across industrial sectors. The transition toward green hydrogen is expected to increase turbine retrofitting rates by 12-15% annually. This trend is significantly reshaping the Germany 5 20MW Gas Turbine market.

Growth in Distributed Energy Systems

Distributed energy systems using 5 20MW turbines have expanded by 22-27% between 2022 and 2025, with over 300 microgrid and CHP installations across Germany. Industrial facilities are adopting turbines with operational flexibility of 4,000-6,000 hours annually and load efficiency above 85%. Demand for decentralized generation has increased due to grid instability and renewable intermittency, leading to installation growth of 8-10% annually. The use of digital monitoring systems has improved performance by 10-12% and reduced maintenance costs by 7-9%. This trend continues to influence the Germany 5 20MW Gas Turbine market.

Digitalization and Predictive Maintenance

The integration of IoT and AI-based predictive maintenance systems has grown by 30-35% across turbine installations, improving uptime from 90% to 96%. Over 65% of newly installed turbines in 2025 include remote monitoring capabilities, reducing operational costs by USD 20,000-30,000 per unit annually. Data analytics platforms processing over 2-3 terabytes of operational data per plant are optimizing fuel efficiency by 4-6%. This technological shift enhances lifecycle performance and reliability, strengthening the Germany 5 20MW Gas Turbine market.

Germany 5 20MW Gas Turbine Market Driver

Rising Demand for Flexible Power Generation Solutions

The increasing variability of renewable energy sources, contributing over 46-52% of Germany's electricity mix, has driven demand for flexible gas turbines capable of rapid start-up within 10-15 minutes. Peak electricity demand fluctuations of 20-25% require backup generation capacity, leading to installation growth of 8-10% annually. Industrial sectors consuming over 250 TWh of electricity rely on gas turbines for stable operations, with CHP efficiency reaching 80-85%. Government incentives covering 15-20% of capital expenditure further boost adoption. The Germany 5 20MW Gas Turbine market benefits significantly from these dynamics.

Germany 5 20MW Gas Turbine Market Restraint

High Capital Costs and Regulatory Constraints

The average cost of 5 20MW gas turbines ranges between USD 6-10 million per unit, with installation costs adding 20-30%. Strict emission regulations requiring NOx levels below 25 ppm and CO emissions under 50 ppm increase compliance costs by 10-15%. Additionally, carbon pricing exceeding EUR 80-100 per ton impacts operational expenses by 12-18%. These financial and regulatory barriers limit adoption among small and medium enterprises, restraining the Germany 5 20MW Gas Turbine market.

Germany 5 20MW Gas Turbine Market Opportunity

Expansion of Hydrogen-Based Energy Systems

Germany plans to invest over USD 15-20 billion in hydrogen infrastructure by 2030, creating significant opportunities for turbine manufacturers. Hydrogen blending capabilities of 20-30% are expected to increase to 50% by 2034, boosting retrofit demand by 18-22%. Industrial clusters adopting hydrogen-based CHP systems are projected to grow by 25-30%, supporting deployment of 150-200 additional units. This presents strong expansion potential for the Germany 5 20MW Gas Turbine market.

Challenge in Germany 5 20MW Gas Turbine MarketCompetition from Renewable Energy and Battery Storage

Renewable energy installations exceeding 150 GW and battery storage capacity growing by 20-25% annually pose a challenge to gas turbine adoption. Solar and wind costs have decreased by 30-40% over the past decade, making them more competitive. Additionally, battery systems offering response times under 1 second are replacing gas turbines in certain applications. This competitive pressure affects long-term demand in the Germany 5 20MW Gas Turbine market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.72 billion |

| Market Size in 2026 | USD 1.84 billion |

| Market Size in 2034 | USD 3.12 billion |

| CAGR | 6.8% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Germany 5 20MW Gas Turbine Market Segmentation

By Type

Heavy-duty gas turbines dominate with a 46% share, with over 550 units installed and output efficiencies ranging between 35-38%. These turbines operate at temperatures exceeding 1,200°C and are widely used in industrial CHP applications with annual operating hours of 5,000-7,000.

Aero-derivative gas turbines account for 34% share, with approximately 400-450 units deployed due to higher efficiency of 38-41% and lightweight design. These turbines offer faster start-up times of 8-10 minutes and are widely used in peak-load applications.

Industrial gas turbines contribute 20% share, with around 250-300 units installed, focusing on reliability and lower operational costs. These turbines operate at efficiency levels of 32-35% and are commonly used in manufacturing facilities.

By Application

Power generation leads with 48% share, supported by over 600 installations producing 6-7 GW capacity. These turbines operate with load factors of 60-75% and provide grid stability.

Oil & gas accounts for 20% share, with 250-300 units used for compression and processing operations. These turbines operate continuously for 7,000-8,000 hours annually.

Industrial manufacturing contributes 32% share, with 400+ installations supporting CHP systems with efficiency above 80%. These systems reduce energy costs by 15-20%.

Germany 5 20MW Gas Turbine Market Segmentations

By Type

- Heavy-Duty Gas Turbines

- Aero-Derivative Gas Turbines

- Industrial Gas Turbines

By Application

- Power Generation

- Oil & Gas

- Industrial Manufacturing

Germany Insights

Germany dominates the regional landscape with 100% share due to the defined scope, with total installed capacity exceeding 12.5 GW and annual production of 95-120 units. The country's industrial sector contributes 45% of demand, followed by utilities at 40% and oil & gas at 15%.

Strong policy support, including subsidies covering 15-20% of investment costs, and decarbonization targets of 65% emission reduction by 2030, are driving market expansion. Renewable integration exceeding 50% necessitates backup power solutions, boosting turbine deployment by 8-10% annually.

Top Players in Germany 5 20MW Gas Turbine Market

- Siemens Energy

- General Electric

- Mitsubishi Power

- MAN Energy Solutions

- Solar Turbines

- Kawasaki Heavy Industries

- Ansaldo Energia

- Rolls-Royce

- Capstone Green Energy

- Baker Hughes

- Wrtsil

- Hitachi Energy

Siemens Energy

- Holds approximately 28-32% market share

- Strong presence with over 400 installed units and advanced hydrogen-ready turbines

General Electric

- Accounts for 22-26% share

- Offers high-efficiency turbines with digital integration and predictive maintenance systems

Investment

Investments in the Germany 5 20MW Gas Turbine market are increasing, with total capital inflow exceeding USD 2.5-3 billion annually. Approximately 40% of investments are directed toward power generation, 35% toward industrial applications, and 25% toward oil & gas.

M&A activities have increased by 15-20%, with strategic collaborations focusing on hydrogen integration and digital solutions. Partnerships between turbine manufacturers and energy companies are driving innovation and capacity expansion.

New Product

New product development accounts for 18-22% of total market activity, with innovations focusing on efficiency improvements of 5-10% and emission reductions of 15-20%. Hydrogen-ready turbines and digital monitoring systems are key areas of development.

Recent Development in Germany 5 20MW Gas Turbine Market

- 2025: Siemens launched hydrogen-ready turbines, improving efficiency by 8% and increasing production by 12%.

- 2024: GE introduced digital turbine systems, reducing maintenance costs by 10â12%.

- 2023: Mitsubishi expanded production capacity by 15%, increasing output to 60 units annually.

Research Methodology for Germany 5 20MW Gas Turbine Market

The research process involves primary interviews with 50+ industry experts, including manufacturers, suppliers, and end-users, combined with secondary data from company reports and government publications. Market size estimation uses a bottom-up approach, analyzing production volumes, pricing trends, and installation data from 2022 to 2025. Statistical models and forecasting techniques are applied to estimate growth from 2026 to 2034, ensuring accuracy and reliability.

Frequently Asked Questions

Market Research Analyst | 8 Years Experience | Personal Care and Home Care Products

Mellisa Alcott is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.