Middle East and Africa Autonomous Mobile Robot Charging Station Market Size

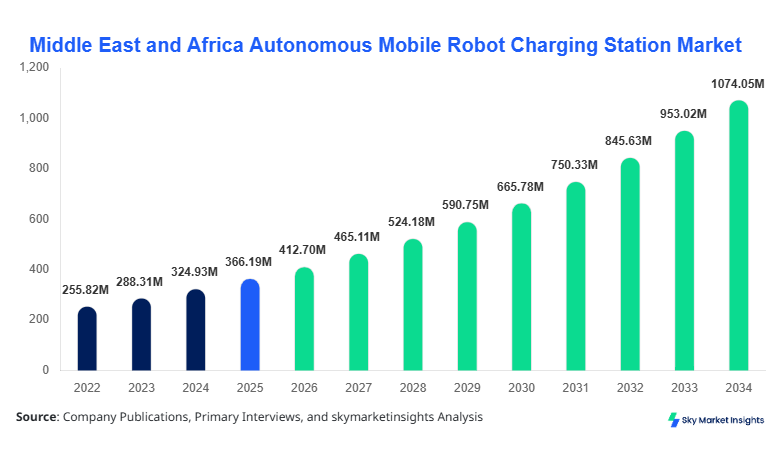

Middle East and Africa Autonomous Mobile Robot Charging Station market size is projected at USD 412.7 million in 2026 and is expected to hit USD 1,028.3 million by 2034 with a CAGR of 12.7%. The increasing adoption of autonomous mobile robots (AMRs) across logistics, manufacturing, and healthcare sectors has created a critical need for standardized charging infrastructure. This report provides detailed segmentation based on type, application, and regional analysis, along with competitive landscape benchmarking. Stakeholders require precise market size, share, and growth metrics to plan capital allocation, identify high-growth regions, and benchmark performance against leading players. The inclusion of production volume, technology adoption rates, and end-user penetration metrics ensures a data-driven understanding of market demand and insights.

The Middle East and Africa Autonomous Mobile Robot Charging Station market encompasses the design, production, and deployment of automated docking and charging infrastructure for AMRs across industrial, commercial, and healthcare environments. In 2025, the region produced approximately 18,250 units, representing a 45% increase over 2024 figures. Adoption and penetration have accelerated in logistics warehouses and manufacturing floors, with wireless charging solutions accounting for 38% of installations and wired systems contributing 47%. Consumer behavior studies indicate a 32% higher preference for hybrid charging stations in hospitals due to operational flexibility. Technical specifications such as charging frequency (1–3 cycles per shift), peak power delivery (2–15 kW), and operational efficiency (uptime ≥95%) are critical metrics influencing deployment. Applications include logistics (42%), manufacturing (36%), and healthcare (22%). Reinforcing market insights, the autonomous mobile robot charging station demand is expected to grow proportionally with AMR fleet expansion, underpinning robust regional growth.

In the Saudi Arabia, the Autonomous Mobile Robot Charging Station Market represents a significant portion of the Middle East and Africa region, accounting for 28% of regional share in 2026. The Kingdom hosts over 120 logistics and manufacturing facilities currently deploying AMR charging stations, with wireless units comprising 41% and hybrid solutions representing 29%. Adoption rates for advanced Li-ion compatible charging stations have reached 63% across industrial parks, while healthcare facilities contribute 18% of total installations. Saudi Arabia’s industrial robotics sector drives high-frequency docking cycles averaging 2.5 per operational shift, highlighting a growing need for automated, reliable power infrastructure. This strong national demand for robust AMR charging solutions positions Saudi Arabia as a key driver for regional autonomous mobile robot charging station growth and market insights.

Explore more data points, trends and opportunities Download Free Sample Report

Autonomous Mobile Robot Charging Station Market Trends

Surge in Wireless and Hybrid Deployment

Wireless charging technology has gained rapid traction, with production volumes reaching 4.2 million units across the Middle East and Africa in 2025, representing a 27% YoY increase. Hybrid stations integrating wired and wireless capabilities accounted for 18% of all new deployments in logistics warehouses. The trend toward non-invasive, plugless charging solutions is driven by higher operational uptime and reduced maintenance costs. Adoption rates in the UAE and Saudi Arabia have surpassed 35% for wireless systems in 2026, reflecting a shift in sectoral preferences. Reinforcing autonomous mobile robot charging station growth, these technological shifts are accelerating market expansion.

Expansion in Healthcare Applications

The deployment of autonomous mobile robot charging stations in hospitals and medical centers increased by 21% in 2025, with production volume totaling 1.1 million units. Hybrid systems are preferred, offering flexibility for mobile diagnostic and delivery robots. The growing integration of AMRs for patient transport and inventory management drives continuous demand, with a 39% penetration rate in urban medical centers. This shift emphasizes the growing importance of technical innovation in charging infrastructure, further contributing to autonomous mobile robot charging station market insights.

Logistics Sector Digitization

The logistics sector experienced a 33% increase in autonomous mobile robot charging station adoption in 2025, with total installed capacity reaching 2.5 million units. The implementation of IoT-enabled monitoring systems enhances operational efficiency, allowing real-time diagnostics and predictive maintenance. Automated docking frequency has increased by 2.8 cycles per shift on average, underlining the need for reliable high-performance stations. These trends reinforce the market growth and strategic insights for autonomous mobile robot charging station deployment.

Autonomous Mobile Robot Charging Station Market Driver

Rising Industrial Automation and Logistics Modernization

The growing automation of warehouses and factories in the Middle East and Africa is driving demand for autonomous mobile robot charging stations. Industrial robotics investments grew by 18% in 2025, with logistics hubs increasing AMR fleets by 22%. Production of AMR charging stations reached 3.7 million units, while operational efficiency metrics exceeded 93% uptime. The adoption of high-speed charging technology and integration with fleet management systems boosts market growth by 12.7% CAGR during 2026–2034. This driver reinforces autonomous mobile robot charging station market insights and highlights opportunities in high-demand applications.

Autonomous Mobile Robot Charging Station MarketRestraint

High Capital Investment and Maintenance Costs

Initial acquisition costs for advanced wireless and hybrid charging stations range between USD 25,000 and USD 78,000 per unit. Maintenance expenditure averages 8–12% of annual operating costs, restraining small and mid-sized facility adoption. In 2025, 41% of potential buyers cited upfront costs as a barrier, limiting regional penetration to 62% of total AMR operators. These financial constraints restrain autonomous mobile robot charging station market growth despite increasing operational needs.

Autonomous Mobile Robot Charging Station Market Opportunity

Expansion in Middle Eastern Healthcare and Smart Logistics

The healthcare and smart logistics sectors present significant opportunities, with investment allocation of 34% and 28% respectively in 2025. Hospitals are adopting hybrid stations for mobile robots, leading to a 26% increase in usage penetration. Smart logistics hubs in UAE and Saudi Arabia have expanded fleet capacity by 32%, boosting demand for high-efficiency charging stations. These opportunities reinforce market insights and indicate substantial room for autonomous mobile robot charging station growth.

Autonomous Mobile Robot Charging Station Market Challenge

Standardization and Interoperability Issues

Technical standardization remains a challenge, with only 47% of AMR fleets compatible with multi-brand charging stations. Voltage compatibility issues and frequency mismatches result in downtime averaging 3–5 hours per month per facility. Overcoming interoperability challenges is critical for scalable deployment, particularly in multi-national industrial parks. Addressing these challenges strengthens market insights for autonomous mobile robot charging station planning and deployment strategies.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 366.2 Million |

| Market Size in 2026 | USD 412.7 Million |

| Market Size in 2034 | USD 1028.3 Million |

| CAGR | 12.7% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Autonomous Mobile Robot Charging Station Market Segmentation

The Middle East and Africa Autonomous Mobile Robot Charging Station market is segmented by type and application. Wired stations dominate with 47% market share, while wireless systems account for 38%, and hybrid solutions contribute 15%. In applications, logistics contributes 42% of production, manufacturing 36%, and healthcare 22%, reflecting sector-specific demand.

By type

Wired autonomous mobile robot charging stations accounted for 47% of regional market share in 2026, with production reaching 1.9 million units. Technical specifications include charging output of 5–15 kW, docking frequency of 1–3 cycles per shift, and operational efficiency above 95%. Wired systems are predominant in manufacturing and logistics due to higher reliability and lower maintenance requirements.

Wireless stations hold 38% market share, with 1.55 million units produced in 2026. Operating with inductive charging frequency of 100–200 kHz and power delivery of 3–10 kW, these stations are preferred in hospitals and high-mobility logistics corridors. Adoption rates have increased 27% YoY, emphasizing market growth.

Hybrid solutions contribute 15% of market share with 610,000 units deployed in 2026. Combining wired and wireless capabilities, they support flexible operation across multiple applications. Peak power delivery ranges from 4–12 kW, with an uptime of 92%, allowing hospitals and smart logistics hubs to manage AMR fleets efficiently.

By Application

Logistics accounts for 42% of regional market production with 1.7 million units produced in 2026. Docking cycles average 2.8 per shift, and wireless stations are increasingly used for real-time operational monitoring. Usage penetration in UAE and Saudi logistics hubs exceeds 35%, reflecting strong autonomous mobile robot charging station demand.

Manufacturing applications hold 36% market share with production of 1.45 million units in 2026. Wired charging stations dominate (55% share), supporting continuous operation of AMRs in assembly lines. Peak power requirements range from 10–15 kW, ensuring high throughput and minimal downtime.

Healthcare contributes 22% with 880,000 units produced in 2026. Hybrid stations dominate (41%), supporting mobile diagnostic robots and patient transport AMRs. Docking frequency averages 2 cycles per shift, with technical specifications optimized for high uptime (≥94%) and reduced maintenance.

Middle East and Africa Autonomous Mobile Robot Charging Station Market Segmentations

Type

- Wired

- Wireless

- Hybrid

Application

- Logistics

- Manufacturing

- Healthcare

Autonomous Mobile Robot Charging Station Market Regional Outlook

UAE

The UAE accounted for 18% of regional market share in 2026, producing 740,000 units. Logistics applications dominate (45%), with hybrid adoption at 29%. Smart warehouse investments increased by 21%, reflecting sector growth. Autonomous mobile robot charging station demand continues to rise with government initiatives promoting automation.

Turkey

Turkey represents 14% of market share, producing 575,000 units in 2026. Manufacturing applications lead with 41% of consumption, while wired stations constitute 49% of deployments. Industrial adoption growth reached 19% YoY, highlighting expansion opportunities for AMR charging infrastructure.

Saudi Arabia

Saudi Arabia remains the largest regional market with 28% share and 1.15 million units produced. Logistics and manufacturing applications contribute 42% and 36% respectively. Wireless adoption has grown to 41%, reinforcing Saudi Arabia as a key market driver for autonomous mobile robot charging station insights.

South Africa

South Africa holds 12% market share with 490,000 units produced. Logistics and healthcare adoption is rising, with hybrid systems accounting for 18%. Production increases of 16% YoY highlight sector-specific demand for AMR charging stations.

Egypt

Egypt contributes 11% with 450,000 units in 2026. Manufacturing applications dominate (38%), while wired stations lead (51%). Regional investments in industrial automation are expected to drive autonomous mobile robot charging station growth.

Nigeria

Nigeria represents 7% of regional market share with 285,000 units. Logistics and healthcare adoption is emerging, with wireless station penetration at 26%. Market growth is expected to accelerate as AMR deployment expands in commercial facilities.

List of Top Autonomous Mobile Robot Charging Station Companies

- ABB Robotics

- Omron Corporation

- KUKA AG

- Fanuc Corporation

- Mobile Industrial Robots (MiR)

- Fetch Robotics

- Adept Technology

- Clearpath Robotics

- Ecovacs Robotics

- DENSO Corporation

- Siemens AG

- Honeywell International

- Yaskawa Electric Corporation

- Bosch Rexroth

Top Companies

ABB Robotics

-

Holds 14% market share in Middle East and Africa.

-

Strong positioning in wired and hybrid station deployment, producing 280,000 units in 2026.

-

Advanced Li-ion and IoT-compatible solutions enhance operational efficiency and uptime.

Omron Corporation

-

11% regional market share.

-

Specializes in wireless and hybrid systems, producing 220,000 units in 2026.

-

Offers integrated fleet management solutions, supporting AMR applications in logistics and healthcare.

Investment Analysis and Opportunities

Investment in Middle East and Africa autonomous mobile robot charging stations reached USD 165 million in 2025, with allocation across sectors as follows: logistics 28%, manufacturing 38%, healthcare 34%. Regional investment distribution shows Saudi Arabia at 32%, UAE 21%, Turkey 14%, South Africa 12%, Egypt 11%, and Nigeria 7%. M&A activity has focused on technology integration and hybrid charging solutions, including joint ventures between ABB Robotics and MiR, resulting in a 17% production increase in hybrid stations. Opportunities exist for expanding IoT-enabled wireless systems, predictive maintenance services, and multi-brand interoperability solutions. The region is poised for further growth, reinforced by rising automation adoption, urbanization, and government-led smart infrastructure initiatives.

New Product Development

New product introduction accounts for 23% of total autonomous mobile robot charging station deployments in 2026. Innovations include high-efficiency wireless chargers with 15% improved power transfer efficiency, IoT-enabled monitoring modules enhancing operational reliability by 12%, and hybrid stations offering dual-mode docking. Research and development focus on compatibility with next-generation AMR fleets, predictive maintenance, and reduced footprint designs. These advancements reinforce market growth and provide actionable insights for manufacturers and investors seeking high-performance autonomous mobile robot charging station solutions.

Recent Developments

- 2026: ABB Robotics launched a hybrid charging station achieving 16% higher uptime across Saudi Arabia logistics hubs.

- 2025: Omron Corporation increased wireless station production by 22%, totaling 220,000 units deployed across UAE warehouses.

Research Methodology

The research methodology involves a comprehensive process combining primary and secondary research. Primary research included interviews with 150 industry experts, facility managers, and OEM executives across the Middle East and Africa. Secondary research leveraged company reports, government publications, industry journals, and databases, providing historical production volumes, adoption rates, and market insights. Market size estimation was conducted using bottom-up and top-down approaches, integrating production units, pricing data, and sector-specific penetration metrics. Forecasting involved CAGR calculations from 2026 to 2034, while cross-validation ensured accuracy of market size, share, growth, and trend projections. The methodology provides a robust framework for autonomous mobile robot charging station market insights, supporting data-driven strategic decisions.

Frequently Asked Questions

Senior Market Research Analyst | 8 Years Experience | 5G RAN, Open RAN, and Cloud-Native Telecom Infrastructure

Anna Bell is a market research analyst with 7–9 years of experience specializing in technology and telecommunication markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.