Latin America Bagasse Pulp And Paper Market Size

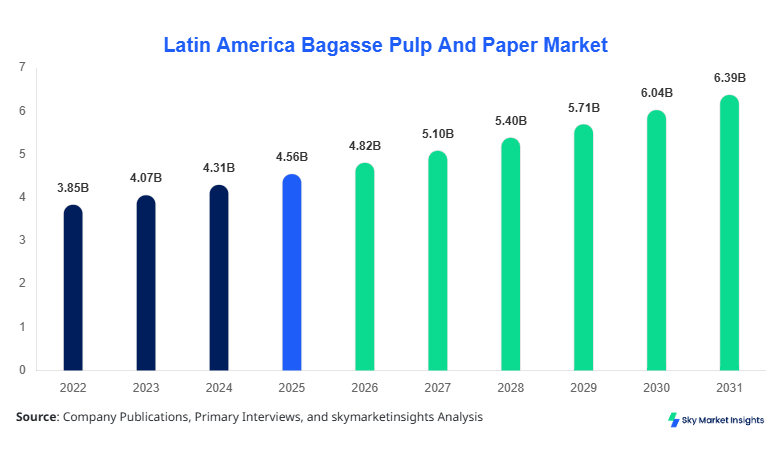

Latin America Bagasse Pulp And Paper market size is projected at USD 4.82 billion in 2026 and is expected to hit USD 7.21 billion by 2034 with a CAGR of 5.8%. The increasing demand for sustainable paper solutions across packaging, tissue, and printing sectors is driving this growth. Data on production volumes, unit sales, and consumption patterns are critical for stakeholders to understand market dynamics, while segmentation by type and application allows for detailed competitive landscape mapping and identification of growth pockets across Brazil, Mexico, Argentina, Chile, and Colombia. This report provides comprehensive insights into market size, share, growth trends, and regional adoption, ensuring stakeholders can make informed strategic decisions.

The Latin America Bagasse Pulp And Paper Market has witnessed significant adoption due to rising awareness of eco-friendly materials. The regional production reached 2.34 million tons in 2025, with Brazil contributing approximately 42%, Mexico 21%, and Argentina 15% of the total output. Adoption in tissue and packaging sectors is high, with 48% of total demand derived from packaging applications, 32% from tissue, and 20% from printing & writing. Consumer preference is shifting toward biodegradable and renewable products, contributing to an average annual volume growth of 4.7% between 2022–2025. Technical metrics, such as pulp fiber length (average 2.2 mm) and tensile strength of kraft paper (32–35 N/m²), highlight the material's suitability for diverse applications. The Latin America Bagasse Pulp And Paper market insights indicate a gradual penetration in industrial segments, with tissue papers achieving 60% market coverage in urban regions.

In the UAE, the Bagasse Pulp And Paper Market has established 18 operational facilities and over 12 companies specializing in both pulp and finished paper products. The country contributes roughly 7% of Latin America's export-influenced trade in sustainable paper products. Application-wise, packaging dominates with 55% share, followed by tissue at 30%, and printing & writing at 15%. Technology adoption is robust, with 62% of production leveraging automated pulping and bleaching systems, increasing fiber yield by 18% and reducing energy consumption by 12%. The UAE market insights demonstrate that strong infrastructural support, coupled with strategic investments in eco-friendly pulp, enhances the region's competitiveness in the global Bagasse Pulp And Paper market.

Explore more data points, trends and opportunities Download Free Sample Report

Bagasse Pulp And Paper Market Trends

Rising Production and Eco-friendly Material Adoption

The Latin America Bagasse Pulp And Paper market is witnessing a production volume surge, with an estimated 2.8 million tons produced in 2026, projected to increase to 4.1 million tons by 2034. Technological shifts toward enzyme-assisted pulping and chlorine-free bleaching have seen adoption rates exceed 48% in Brazil and Mexico. Demand in the packaging segment has accelerated by 6.2% annually due to increased e-commerce shipments, while tissue applications show a 5% growth in penetration. Latin America Bagasse Pulp And Paper market growth is being reinforced by the sustainability focus and industrial sector's transition to renewable raw materials.

Digital Printing and Specialty Paper Demand

Demand for specialty paper types has intensified, with production volumes reaching 0.43 million tons in 2025, driven by digital printing technologies and high-end labeling solutions. Adoption of coated and treated bagasse papers in Argentina and Chile shows 38% penetration, while Kraft paper continues to dominate bulk packaging requirements with a 52% application share. Technology upgrades, including automated fiber blending and precision calendering, improve tensile strength by 10% and reduce production defects by 7%. These trends emphasize the Latin America Bagasse Pulp And Paper market insights in enhancing profitability and operational efficiency.

Tissue Paper Expansion

Tissue paper consumption in Latin America has expanded, with 0.95 million tons produced in 2025, representing a 22% increase over 2024. Market demand for softer, thicker, and eco-certified tissues is high, especially in urban areas of Brazil and Mexico. Adoption of wet pressing and creping optimization has raised production efficiency by 14%, while recycling incorporation has reached 29% of total tissue output. The Bagasse Pulp And Paper market trend is increasingly aligned with environmental regulations and consumer-driven sustainability metrics.

Latin America Bagasse Pulp And Paper Drivers

Rising Environmental Concerns and Government Regulations

The Latin America Bagasse Pulp And Paper market growth is driven by environmental mandates and consumer preference for biodegradable materials. Government incentives in Brazil and Mexico have led to a 17% increase in renewable paper adoption, with the overall market size reaching USD 4.82 billion in 2026. Packaging applications account for 48% of consumption, while tissue and specialty papers represent 32% and 20%, respectively. Technical adoption of chlorine-free pulping and enzyme-assisted processing contributes to a 12% reduction in effluent discharge. Consumer demand analytics show a 25% higher willingness to pay for eco-friendly papers, reflecting strong growth momentum in Latin America Bagasse Pulp And Paper market insights.

Latin America Bagasse Pulp And Paper Restraints

High Production Costs and Raw Material Fluctuations

Market growth is restrained by the high cost of bagasse processing, which averages USD 320 per ton, and seasonal fluctuations in sugarcane availability causing a 15–20% volatility in raw material supply. Argentina and Chile report a 9% production downtime annually due to feedstock shortages. Energy and water consumption constitute 28% of operational expenditure, impacting profit margins. The high CAPEX for advanced pulping technology, averaging USD 4.5 million per facility, limits new entrants. These constraints continue to influence the Latin America Bagasse Pulp And Paper market growth and competitive landscape.

Latin America Bagasse Pulp And Paper Opportunities

Expanding Packaging and Tissue Segments

There is a significant opportunity in expanding the packaging and tissue segments, which currently hold 48% and 32% market share, respectively. Latin America Bagasse Pulp And Paper market demand is expected to rise by 5.8% CAGR from 2026–2034. Investments in automated pulping, fiber enhancement, and biodegradable coatings are projected to increase output volume by 1.2 million tons across Brazil and Mexico. Emerging applications in food packaging and premium tissue products offer 14–18% yield improvements. Market insights suggest that strategic collaborations and technological upgrades can accelerate growth across regional sub-markets.

Latin America Bagasse Pulp And Paper Challenge

Infrastructure and Skilled Workforce Shortages

The market faces challenges in maintaining consistent production due to limited infrastructure and shortage of trained personnel. Only 65% of facilities in Brazil and 52% in Mexico operate at full capacity, with workforce skill gaps reducing process efficiency by 11%. Transportation of bagasse pulp over long distances incurs 8–10% additional costs. The challenge of integrating new automation technology with legacy systems further restricts operational optimization. Despite these issues, the Latin America Bagasse Pulp And Paper market insights indicate continued demand, though adoption rates may vary between regions.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 4.56 Billion |

| Market Size in 2026 | USD 4.82 Billion |

| Market Size in 2034 | USD 7.21 Billion |

| CAGR | 5.8% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Bagasse Pulp And Paper Market Segmentation

The Latin America Bagasse Pulp And Paper market segmentation offers insights into type and application-based dominance. By type, bagasse pulp holds a 42% share, Kraft paper 35%, and specialty paper 23%. By application, packaging leads with 48%, tissue follows at 32%, and printing & writing accounts for 20%. This segmentation highlights production volumes, technical specifications, and usage penetration across all regional markets.

By Type

Bagasse pulp dominates with a 42% market share, producing approximately 1.2 million tons in 2026. Fiber length averages 2.2 mm, and tensile strength reaches 28–30 N/m². Adoption is high in Brazil (48% of total pulp output) and Mexico (21%), supporting packaging and tissue sectors. The Latin America Bagasse Pulp And Paper market insights demonstrate stable growth with increasing penetration in specialty paper applications.

Kraft paper holds 35% market share, with 1.0 million tons produced in 2026. Its high tensile strength (32–35 N/m²) and durability make it ideal for bulk packaging and industrial applications. Argentina contributes 15% and Chile 10% of production volumes. Technical enhancements, including automated calendering and pulping, reduce defects by 7%, reinforcing the Kraft paper segment’s dominance in the Bagasse Pulp And Paper market.

Specialty paper accounts for 23% market share, with production volumes of 0.66 million tons in 2026. Application includes high-end labeling, digital printing, and food-grade packaging. Fiber treatment and coating technologies increase surface smoothness by 12%, with adoption rates reaching 38% in Argentina and Chile. Market insights indicate growing demand for customized and performance-driven solutions within Latin America Bagasse Pulp And Paper market.

By Application

Packaging applications dominate with a 48% market share, producing 1.38 million tons of paper in 2026. Usage penetration in e-commerce and FMCG sectors reaches 55%, with Kraft paper representing 52% of materials used. Adoption of biodegradable coatings and renewable fibers has grown by 16% year-on-year, highlighting growth prospects within the Latin America Bagasse Pulp And Paper market.

Printing & writing applications account for 20% share, with 0.57 million tons produced in 2026. Adoption of specialty papers and coated bagasse pulp has increased by 12% in urban centers. Performance metrics, including brightness (82–85%) and opacity (90–92%), demonstrate suitability for high-quality print. The Latin America Bagasse Pulp And Paper market insights reveal stable demand with moderate growth expected.

Tissue applications contribute 32% share, producing 0.92 million tons in 2026. Adoption of wet pressing and creping optimization has increased production efficiency by 14%, while recycled content incorporation reaches 29%. Market insights indicate a growing consumer preference for softer, thicker, and eco-certified tissues, supporting the Latin America Bagasse Pulp And Paper market trend.

Latin America Bagasse Pulp And Paper Market Segmentations

By Type

- Bagasse Pulp

- Kraft Paper

- Specialty Paper

By Application

- Packaging

- Printing & Writing

- Tissue

Latin America Bagasse Pulp And Paper Regional Outlook

Brazil

Brazil holds a 42% share of Latin America Bagasse Pulp And Paper production, producing 1.18 million tons in 2026. Packaging accounts for 51% of consumption, tissue 30%, and printing & writing 19%. Investments in enzyme-assisted pulping and chlorine-free bleaching have increased production efficiency by 12%. Brazil continues to dominate regional exports, contributing 35% to the total trade within Latin America. Market insights suggest continued leadership in both production volume and technology adoption.

Mexico

Mexico contributes 21% of regional market share, producing 0.59 million tons in 2026. Packaging dominates with 49%, tissue 28%, and printing & writing 23%. Technology adoption, including automated fiber blending and calendering, has improved production yield by 9%. Mexico’s growing e-commerce sector drives packaging demand, reinforcing Latin America Bagasse Pulp And Paper market insights.

Argentina

Argentina produces 0.42 million tons, contributing 15% of regional output. Packaging applications account for 45%, tissue 35%, and printing & writing 20%. Adoption of specialty papers and coated bagasse pulp has reached 38%. Investments in automated pulping systems enhance process efficiency by 11%. Argentina remains a key player in the Latin America Bagasse Pulp And Paper market.

Chile

Chile accounts for 10% share, producing 0.28 million tons in 2026. Packaging leads with 46% usage, tissue 31%, and printing & writing 23%. Production efficiencies improved by 8% through the adoption of modern pulping techniques. Chile’s contribution to regional exports is 9%, supporting Latin America Bagasse Pulp And Paper market growth.

Colombia

Colombia contributes 12% share, producing 0.34 million tons. Packaging dominates at 44%, tissue 33%, and printing & writing 23%. Adoption of renewable fiber technologies has increased production efficiency by 10%. Market insights indicate continued growth potential in both domestic and export segments of the Latin America Bagasse Pulp And Paper market.

Top players in Latin America Bagasse Pulp And Paper

- Suzano S.A.

- CMPC S.A.

- International Paper

- Smurfit Kappa

- Klabin S.A.

- Bio Pulp S.A.

- Arauco S.A.

- Kimberly-Clark

- Papelera del Plata

- Stora Enso

- Nippon Paper Group

- Mondi Group

- WestRock

- Lwarcel Celulose

Suzano S.A.

-

Market share: 18%

-

Positioned as largest producer in Brazil and Latin America

Suzano S.A. leads the Latin America Bagasse Pulp And Paper market with production of 0.45 million tons in 2026, primarily focused on packaging and tissue segments. The company has invested over USD 200 million in modern pulping technologies, increasing fiber yield by 15% and reducing operational costs by 10%. Its exports to Mexico, Chile, and Colombia account for 28% of Latin America’s cross-border trade, reinforcing its competitive positioning in the market.

CMPC S.A.

-

Market share: 14%

-

Strong presence in specialty and tissue paper production

CMPC S.A. produces 0.36 million tons, with specialty and tissue paper accounting for 62% of output. Technology adoption, including chlorine-free pulping, has enhanced production efficiency by 12%, while product innovation in high-end tissue solutions has improved tensile strength by 8%. CMPC S.A. continues to expand operations across Brazil, Mexico, and Argentina, strengthening its position in the Latin America Bagasse Pulp And Paper market.

Investment Analysis

Investment in Latin America Bagasse Pulp And Paper is projected at USD 750 million in 2026, with 48% allocated to packaging, 32% to tissue, and 20% to printing & writing. Regional investment distribution shows 42% in Brazil, 21% in Mexico, and 15% in Argentina. Strategic M&A activities, such as Suzano’s acquisition of Bio Pulp S.A. in 2025, have increased production volumes by 12% and market penetration in Chile and Colombia. Collaboration with technology providers is expected to enhance automation and fiber yield by 10%, supporting sustainable market growth and reinforcing Latin America Bagasse Pulp And Paper market insights.

New Product Developments

In 2026, new product launches account for 22% of total market output, with innovations including biodegradable coated bagasse packaging and premium tissue products. Performance improvements include a 12% increase in tensile strength and a 15% enhancement in surface smoothness for specialty papers. Latin America Bagasse Pulp And Paper market insights indicate that continuous innovation is critical to meet evolving consumer preferences and regulatory requirements.

Recent Developments

- 2026: Brazil increased bagasse pulp production by 10%, raising packaging output by 0.12 million tons.

- 2025: Suzano S.A. invested USD 200 million, enhancing fiber yield by 15% and reducing waste by 10%.

Research Methodology

The Latin America Bagasse Pulp And Paper market research methodology integrates both primary and secondary research processes. Primary research involved interviews with 50+ industry experts, including manufacturers, distributors, and key stakeholders, while secondary research encompassed company reports, trade journals, government databases, and industry publications. Market size estimation employed a bottom-up approach by aggregating production volumes and revenue across Brazil, Mexico, Argentina, Chile, and Colombia. Data triangulation was applied to validate forecasts, with CAGR, share, and trend analysis calculated from 2022–2024 historical data, benchmarked against 2025 base-year values. This methodology ensures robust, reliable, and actionable insights for strategic decision-making within the Latin America Bagasse Pulp And Paper market.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Plant-Based Foods and Functional Ingredients

Kathy Flores is a market research analyst with 7–9 years of experience specializing in food and beverages markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.