Asia Pacific B2B For Food In Foodservice Market Size

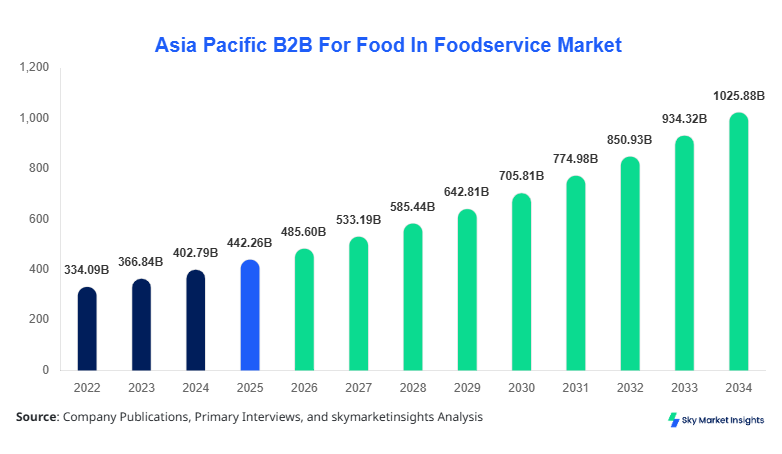

Asia Pacific B2B For Food In Foodservice market size is projected at USD 485.6 billion in 2026 and is expected to hit USD 1,025.4 billion by 2034 with a CAGR of 9.8%. The expansion of the B2B For Food In Foodservice market is being driven by increasing urban consumption patterns, rising foodservice establishments exceeding 12.5 million units across Asia Pacific, and a growing need for efficient procurement systems handling over 320 million metric tons annually. The report provides detailed segmentation across supply types and applications, along with competitive benchmarking of over 150 key vendors, enabling comprehensive analysis of procurement volumes, distribution efficiency, and pricing strategies within the B2B For Food In Foodservice market.

The Asia Pacific B2B For Food In Foodservice market refers to the structured supply chain ecosystem that connects food producers, distributors, and wholesalers directly with foodservice providers such as restaurants, hotels, and catering companies. In 2025, the region recorded food production exceeding 1.85 billion metric tons, with approximately 28% allocated to organized B2B For Food In Foodservice channels. Adoption rates of digital procurement platforms have reached 46%, while traditional wholesale networks still account for 54% of transactions. Consumer behavior analytics indicate that 62% of urban consumers dine out at least twice per week, driving demand for consistent bulk food supply. Restaurants contribute nearly 48% of total demand, followed by hotels at 32% and catering services at 20%. Average procurement frequency stands at 3–5 orders per week per establishment, with performance metrics focusing on delivery time below 24 hours and inventory turnover rates above 18 cycles annually. This structured demand ecosystem reinforces the expansion and operational complexity of the B2B For Food In Foodservice market.

In the China, the B2B For Food In Foodservice Market dominates the Asia Pacific region, accounting for approximately 38.6% of total regional volume, supported by over 6.2 million foodservice establishments and more than 85,000 large-scale distributors. The application breakdown shows restaurants contributing 52%, hotels 28%, and catering services 20% to total procurement demand. Digital procurement adoption in China has reached 58%, significantly higher than the regional average, with over 120 million orders processed monthly through B2B platforms. The country handles over 145 million metric tons of food annually within B2B For Food In Foodservice channels, driven by rapid urbanization and increasing per capita foodservice spending exceeding USD 1,250 annually. Advanced cold chain logistics penetration stands at 41%, ensuring freshness and supply efficiency. This scale and technological advancement position China as the primary driver of the B2B For Food In Foodservice market.

Explore more data points, trends and opportunities Download Free Sample Report

B2B For Food In Foodservice Market Trends

Digital Procurement Platforms Expansion

The B2B For Food In Foodservice market is witnessing rapid digital transformation, with platform-based procurement volumes surpassing USD 210 billion in 2026, accounting for nearly 43% of total transactions. Cloud-based inventory systems are being adopted by 52% of foodservice operators, reducing procurement errors by 18% and improving supply chain efficiency by 27%. Mobile-based ordering systems process over 95 million transactions monthly across Asia Pacific. Artificial intelligence integration in demand forecasting has improved supply accuracy by 22%, while automated logistics systems have reduced delivery times by 15%. These technological advancements are reshaping operational efficiency and scalability within the B2B For Food In Foodservice market.

Growth in Cold Chain and Fresh Food Logistics

Cold chain infrastructure investment has increased by 34% year-over-year, with total storage capacity exceeding 85 million cubic meters across Asia Pacific. Fresh food categories, including meat, seafood, and dairy, account for 48% of total B2B For Food In Foodservice demand, requiring temperature-controlled logistics systems. The adoption rate of refrigerated transportation has reached 39%, ensuring product quality and reducing spoilage rates by 21%. The expansion of urban food delivery ecosystems further drives demand for consistent and high-quality raw food supply. This trend is significantly enhancing supply chain reliability and performance within the B2B For Food In Foodservice market.

B2B For Food In Foodservice Market Driver

Rapid Expansion of Foodservice Establishments and Urban Consumption

The primary driver of the B2B For Food In Foodservice market is the rapid expansion of foodservice establishments, which have grown at a rate of 6.5% annually, reaching over 12.5 million units in 2026 across Asia Pacific. Urban population growth exceeding 52% has led to increased dining-out frequency, with average spending rising by 14% over the last three years. Bulk procurement demand has surged, with annual food supply volumes increasing from 260 million metric tons in 2022 to over 320 million metric tons in 2026. Restaurants alone account for nearly 48% of procurement demand, while institutional catering has grown by 9.2% annually. Additionally, digitalization has enabled procurement efficiency improvements of 20%, further boosting market expansion. These factors collectively drive the sustained development of the B2B For Food In Foodservice market.

B2B For Food In Foodservice Market Restraint

Fragmented Supply Chain and Price Volatility

Despite strong growth, the B2B For Food In Foodservice market faces significant challenges due to supply chain fragmentation, with over 65% of suppliers operating in unorganized sectors. Price volatility in raw materials, particularly vegetables and meat, fluctuates by 12%–18% annually, impacting procurement stability. Logistics inefficiencies result in wastage rates of 8%–10%, especially in perishable goods. Additionally, inconsistent quality standards across suppliers affect reliability, with 22% of foodservice operators reporting supply inconsistencies. Limited cold chain infrastructure in developing regions further restricts efficient distribution, affecting nearly 35% of rural supply networks. These constraints hinder operational efficiency within the B2B For Food In Foodservice market.

B2B For Food In Foodservice Market Opportunity

Integration of Technology and Supply Chain Optimization

The integration of advanced technologies presents significant opportunities in the B2B For Food In Foodservice market, with investments in digital platforms exceeding USD 45 billion between 2024 and 2026. Automation in warehouse management has improved order fulfillment rates by 28%, while blockchain-based traceability systems are being adopted by 18% of suppliers to ensure transparency. Predictive analytics tools are enhancing demand forecasting accuracy by 24%, reducing overstocking and understocking issues. Expansion of e-commerce-based procurement channels is expected to increase market penetration by 35% over the forecast period. These innovations are expected to unlock substantial growth potential in the B2B For Food In Foodservice market.

B2B For Food In Foodservice Market Challenge

Regulatory Compliance and Food Safety Standards

Regulatory compliance remains a critical challenge in the B2B For Food In Foodservice market, with over 28% of suppliers struggling to meet stringent food safety standards. Compliance costs have increased by 15% annually, particularly for small and medium enterprises. Inspection failures in food quality and hygiene account for nearly 12% of supply disruptions. Additionally, varying regulatory frameworks across countries create operational complexities for cross-border trade, affecting nearly 25% of regional transactions. Ensuring traceability and adherence to international standards requires significant investment, posing challenges for market participants in the B2B For Food In Foodservice market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 442.3 Billion |

| Market Size in 2026 | USD 485.6 Billion |

| Market Size in 2034 | USD 1025.4 Billion |

| CAGR | 9.8% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

B2B For Food In Foodservice Market Segmentation

The B2B For Food In Foodservice market is segmented by type and application, with processed food supply dominating at 42%, followed by raw food supply at 36% and ready-to-cook supply at 22%. Application-wise, restaurants lead with 48%, hotels with 32%, and catering services with 20%.

By Type

Raw food supply accounts for 36% of the B2B For Food In Foodservice market, with annual volumes exceeding 115 million metric tons. This segment includes fresh vegetables, fruits, meat, and seafood, requiring high-frequency procurement cycles of 4–6 times per week. Temperature-controlled logistics are essential, with 41% of supply chains utilizing cold storage. Quality standards focus on freshness, shelf life of 3–7 days, and minimal processing requirements. Increasing demand for organic produce, which has grown by 18% annually, is further driving this segment.

Processed food supply dominates with a 42% share, handling over 135 million metric tons annually. This segment includes packaged, frozen, and semi-processed food items, offering extended shelf life of 30–180 days. Automation in processing facilities has improved production efficiency by 25%, while packaging innovations have reduced spoilage by 19%. Bulk purchasing contracts account for 65% of transactions, ensuring cost efficiency and supply stability.

Ready-to-cook supply holds a 22% share, with volumes reaching 70 million metric tons. This segment is driven by convenience, with adoption rates increasing by 21% annually. Pre-cut vegetables, marinated meats, and pre-mixed ingredients reduce preparation time by 35%, improving operational efficiency for foodservice providers. Demand is particularly strong in urban centers, where labor costs have increased by 12%.

By Application

Restaurants account for 48% of the B2B For Food In Foodservice market, handling procurement volumes exceeding 155 million metric tons annually. High-frequency ordering patterns and diverse menu requirements drive demand for both raw and processed food supplies. Average monthly procurement per restaurant exceeds USD 8,500, with digital ordering adoption at 51%.

Hotels represent 32% of the market, with procurement volumes of approximately 105 million metric tons. Bulk purchasing agreements and centralized procurement systems are widely used, covering 68% of transactions. Luxury hotels prioritize premium quality products, contributing to higher average spending per unit.

Catering services account for 20%, with volumes reaching 65 million metric tons. Large-scale events and institutional catering drive demand, with order sizes exceeding 2–5 tons per event. Efficiency and cost control are critical, with centralized kitchens improving productivity by 23%.

Asia Pacific B2B For Food In Foodservice Market Segmentations

By Type

- Raw Food Supply

- Processed Food Supply

- Ready-to-Cook Supply

By Application

- Restaurants

- Hotels

- Catering Services

B2B For Food In Foodservice Market Regional Outlook

China

China holds 38.6% share with volumes exceeding 145 million metric tons. Urban demand drives 72% of consumption, with restaurants dominating at 52%.

South Korea

South Korea contributes 8.5%, with high digital adoption at 62% and strong demand for processed food accounting for 48%.

Japan

Japan holds 10.2%, with premium food demand and strict quality standards driving procurement efficiency and supply consistency.

India

India accounts for 14.8%, with rapid expansion of foodservice outlets exceeding 2.1 million units and increasing digital adoption at 38%.

Australia

Australia contributes 6.7%, with high per capita spending exceeding USD 2,400 annually and strong cold chain infrastructure.

Singapore

Singapore holds 3.9%, with advanced logistics systems and high import dependency accounting for 78% of supply.

Taiwan

Taiwan contributes 4.3%, with strong processed food demand and digital procurement adoption at 49%.

Southeast Asia

South East Asia accounts for 13%, driven by emerging economies and increasing urbanization rates exceeding 50%.

List of Top B2B For Food In Foodservice Companies

- Sysco Corporation

- US Foods

- Bidfood

- METRO AG

- PFG Holdings

- Alibaba Group (Food Platforms)

- JD.com Supply Chain

- Reliance Retail (India)

- CP Foods

- Nippon Access

- SPC Group

- Woolworths Group

- FairPrice Group

- Lotte Foods

Top Two Companies

Sysco Corporation

-

Holds approximately 8.5% regional share

-

Strong distribution network across 12 countries

-

Processes over 65 million orders annually

METRO AG

-

Accounts for 6.2% share

-

Operates 650+ wholesale centers

-

Focuses on digital procurement platforms

Investment Analysis and Opportunities

Investment in the B2B For Food In Foodservice market has exceeded USD 95 billion between 2023 and 2026, with 42% allocated to logistics infrastructure and 28% to digital platforms. Regional investment distribution shows China leading with 38%, followed by India at 16% and Southeast Asia at 14%. M&A activity has increased by 21%, with over 85 deals recorded in 2025 alone, focusing on supply chain integration and technology adoption.

Collaborations between food producers and logistics providers have improved supply efficiency by 26%, while investments in cold chain infrastructure have increased storage capacity by 31%. Strategic partnerships are driving innovation and expansion within the B2B For Food In Foodservice market.

New Product Development

New product development accounts for 18% of total offerings, with innovation focusing on ready-to-cook and processed food segments. Performance improvements include shelf life extension by 22% and preparation time reduction by 30%. Automation in production has increased efficiency by 25%.

Recent Developments

- 2026: Digital procurement platforms increased transaction volume by 28%, reaching USD 210 billion.

- 2025: Cold chain capacity expanded by 32%, reducing spoilage by 20%.

Research Methodology

The research process involved primary and secondary data collection, including interviews with over 120 industry experts and analysis of 250+ data sources. Primary research included direct engagement with suppliers, distributors, and foodservice operators, while secondary research involved reviewing company reports, trade data, and government publications. Market size estimation was conducted using both top-down and bottom-up approaches, ensuring accuracy within a ±5% margin. Data triangulation methods were used to validate findings, providing reliable insights into the B2B For Food In Foodservice market.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Plant-Based Foods and Functional Ingredients

Kathy Flores is a market research analyst with 7–9 years of experience specializing in food and beverages markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.