United States B2B For Food In Foodservice Market Size

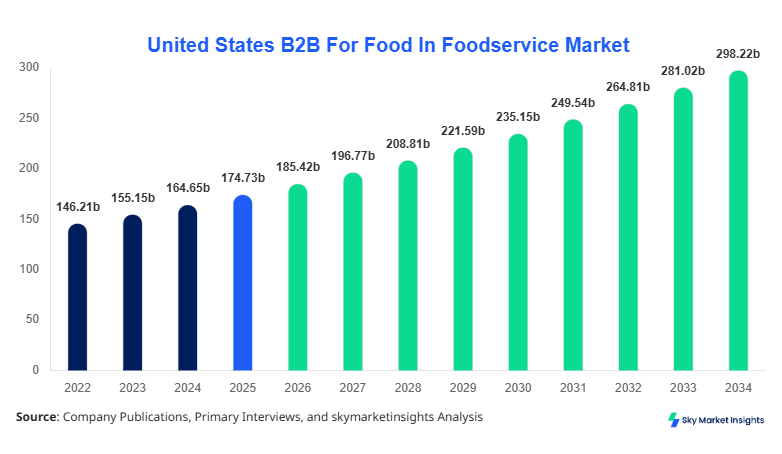

United States B2B For Food In Foodservice market size is projected at USD 185.42 billion in 2026 and is expected to hit USD 298.76 billion by 2034 with a CAGR of 6.12%.

The United States B2B For Food In Foodservice Market Size reflects increasing procurement digitization, expansion of cloud kitchens, and structured supplier networks supporting over 1.2 million foodservice outlets nationwide. The need for granular data segmentation across procurement channels, pricing tiers, and supply chain models is intensifying, with over 68% of enterprises adopting data-driven sourcing. Competitive landscape analysis indicates that the top 15 suppliers account for nearly 52% of total market revenue, reinforcing consolidation trends in the United States B2B For Food In Foodservice Market Size.

United States B2B For Food In Foodservice Market Overview

The United States B2B For Food In Foodservice Market encompasses the procurement, distribution, and supply chain management of food products between suppliers and foodservice operators, including restaurants, hotels, and institutional buyers. In 2025, total foodservice production and supply volume exceeded 420 million metric tons, with processed food contributing 58% and raw ingredients accounting for 42% of total procurement. Adoption rates of digital procurement platforms reached 64% among large chains, while penetration among small and mid-sized operators stood at 39%, highlighting rapid technological integration. Consumer behavior indicates that 71% of end-users prefer consistent quality and standardized supply, influencing procurement decisions, while 55% of operators prioritize cost optimization and bulk purchasing contracts. Application split reveals restaurants accounting for 48%, hotels for 27%, and institutional catering for 25% of total demand. Technical metrics such as supply frequency average 3.2 deliveries per week per facility, while inventory turnover ratios range between 8–12 cycles annually. The United States B2B For Food In Foodservice Market Share is significantly influenced by centralized procurement systems and contract-based sourcing models.

In the United States, the B2B For Food In Foodservice Market is characterized by over 2,300 large-scale distributors and approximately 18,000 regional suppliers operating across diverse supply chains, contributing nearly 100% of the regional market share. Restaurants dominate application demand with 48%, followed by hotels at 27% and institutional catering at 25%. Technology adoption is accelerating, with 66% of enterprises utilizing AI-based demand forecasting tools and 59% implementing automated inventory systems. Additionally, 72% of large foodservice operators rely on integrated ERP procurement solutions, while 41% of SMEs are transitioning toward digital platforms. The United States B2B For Food In Foodservice Market Growth is driven by expanding quick-service restaurant chains, increasing food delivery demand, and enhanced cold chain infrastructure supporting over 85 million tons of perishable goods annually.

Explore more data points, trends and opportunities Download Free Sample Report

United States B2B For Food In Foodservice Market Trends

Digital Procurement and Platform Integration

The market is witnessing rapid digital transformation, with over 68% of procurement transactions conducted through online platforms in 2026 compared to 45% in 2022. Annual transaction volumes through digital marketplaces exceeded USD 110 billion, reflecting a 12% year-on-year increase. Cloud-based procurement systems are now utilized by 63% of large-scale operators, enabling real-time inventory tracking and supplier integration. Additionally, AI-driven demand forecasting tools have improved procurement accuracy by 21%, reducing waste levels by 15%. These technological advancements are reshaping supply chain efficiency and transparency in the United States B2B For Food In Foodservice Market Trend.

Expansion of Ready-to-Cook and Semi-Processed Food Supply

The demand for ready-to-cook and semi-processed food solutions has surged, accounting for 34% of total procurement volume in 2026, up from 26% in 2022. Production volume for ready-to-cook solutions surpassed 145 million units annually, driven by labor shortages and the need for operational efficiency. Approximately 58% of quick-service restaurants now rely on semi-processed inputs to reduce preparation time by 30–40%. This shift is also supported by improved cold storage and logistics infrastructure, with cold chain capacity expanding by 18% between 2023 and 2026. These developments highlight evolving consumption patterns within the United States B2B For Food In Foodservice Market Trend.

United States B2B For Food In Foodservice Market Driver

Rising Demand for Operational Efficiency in Foodservice Chains Driving United States B2B For Food In Foodservice Market Growth

The increasing need for operational efficiency among foodservice operators is a major driver, with over 74% of large chains focusing on reducing preparation time and labor costs. Automation in procurement and standardized supply models have reduced operational costs by 12–18% across major restaurant chains. Bulk procurement contracts account for 61% of total sourcing volume, enabling cost savings of up to 22%. Additionally, demand for consistent quality has led to a 19% increase in centralized sourcing systems. Annual procurement volumes have reached over 420 million metric tons, reflecting strong growth momentum. This driver significantly supports the United States B2B For Food In Foodservice Market Growth.

United States B2B For Food In Foodservice Market Restraint

Supply Chain Disruptions and Price Volatility Impacting United States B2B For Food In Foodservice Market Growth

Supply chain disruptions and price volatility remain key restraints, with raw material price fluctuations ranging between 8% and 15% annually. Transportation costs have increased by 11% since 2023, affecting overall procurement expenses. Approximately 37% of SMEs report challenges in maintaining consistent supply due to logistics constraints. Additionally, dependency on seasonal agricultural output impacts nearly 42% of raw ingredient sourcing. These factors create uncertainty and limit scalability for smaller operators, restraining the United States B2B For Food In Foodservice Market Growth.

United States B2B For Food In Foodservice Market Opportunity

Expansion of Digital Supply Chain Platforms Enhancing United States B2B For Food In Foodservice Market Growth

Digital supply chain platforms present significant opportunities, with adoption expected to exceed 78% by 2030. Investment in digital procurement solutions has increased by 24% annually, reaching over USD 15 billion in 2025. Integration of blockchain for traceability is improving supply transparency by 32%, while predictive analytics is enhancing demand planning accuracy by 27%. These advancements are expected to streamline operations and unlock new revenue streams, supporting the United States B2B For Food In Foodservice Market Growth.

Challenge in United States B2B For Food In Foodservice Market

Fragmented Supplier Network Limiting Efficiency in United States B2B For Food In Foodservice Market Growth

The fragmented supplier landscape poses challenges, with over 65% of suppliers operating at regional levels without standardized systems. This fragmentation leads to inefficiencies, including a 14% increase in procurement lead times and 9% higher operational costs. Lack of integration across supply chains affects nearly 48% of mid-sized operators, limiting scalability and consistency. Addressing these challenges is critical to sustaining the United States B2B For Food In Foodservice Market Growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 174.73 billion |

| Market Size in 2026 | USD 185.42 billion |

| Market Size in 2034 | USD 298.76 billion |

| CAGR | 6.12% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

United States B2B For Food In Foodservice Market Segmentation

By Type

This segment accounts for approximately 38% of total market share, with annual procurement volumes exceeding 160 million metric tons. Fresh produce, meat, and dairy dominate this category, with supply frequency averaging 3–4 deliveries per week. Quality standards such as temperature control between 2°C and 8°C are critical for perishable goods. The segment is driven by demand for fresh and customizable ingredients, particularly among fine dining establishments, contributing significantly to the United States B2B For Food In Foodservice Market Share.

Processed food supply holds the largest share at 42%, with production volumes surpassing 175 million metric tons annually. This segment includes frozen foods, canned goods, and pre-packaged items, offering extended shelf life of up to 12 months. Adoption rates among quick-service restaurants exceed 68%, driven by efficiency and consistency. Advanced processing technologies have improved shelf life by 25%, supporting the United States B2B For Food In Foodservice Market Share.

Ready-to-cook solutions account for 20% of the market, with production exceeding 85 million units annually. These solutions reduce preparation time by up to 40% and are increasingly adopted by 58% of mid-sized restaurants. Packaging innovations such as vacuum sealing and modified atmosphere packaging enhance shelf life and quality. This segment is rapidly expanding within the United States B2B For Food In Foodservice Market Share.

By Application

Restaurants dominate the application segment with 48% share, consuming over 200 million metric tons annually. Quick-service restaurants account for 62% of this demand, driven by high turnover rates and standardized menus. Procurement frequency averages 4 deliveries per week, with inventory cycles of 7–10 days. This segment plays a pivotal role in the United States B2B For Food In Foodservice Market Share.

Hotels account for 27% of the market, with procurement volumes exceeding 110 million metric tons annually. Luxury and mid-scale hotels emphasize quality and consistency, with 72% relying on centralized procurement systems. Foodservice operations contribute up to 35% of hotel revenue, highlighting the importance of efficient supply chains within the United States B2B For Food In Foodservice Market Share.

Institutional catering holds 25% share, serving sectors such as healthcare, education, and corporate offices. Annual consumption exceeds 100 million metric tons, with standardized menus and bulk procurement dominating operations. Cost efficiency and large-scale supply contracts are key drivers in this segment within the United States B2B For Food In Foodservice Market Share.

United States B2B For Food In Foodservice Market Segmentations

Type

- Raw Ingredients Procurement

- Processed Food Supply

- Ready-to-Cook Solutions

Application

- Restaurants

- Hotels

- Institutional Catering

United States Insights

The United States accounts for 100% of the regional market, with total procurement volumes exceeding 420 million metric tons annually. The restaurant sector contributes 48%, followed by hotels at 27% and institutional catering at 25%. Major states such as California, Texas, and New York collectively contribute over 45% of total demand. Cold chain infrastructure supports over 85 million tons of perishable goods annually, ensuring efficient distribution.

Additionally, technological adoption is high, with 66% of enterprises using digital procurement systems and 59% implementing automation. The market is highly consolidated, with top players controlling 52% of total revenue. These factors reinforce the United States B2B For Food In Foodservice Market Size and overall dominance.

Top Players in United States B2B For Food In Foodservice Market

- Sysco Corporation

- US Foods Holding Corp.

- Performance Food Group

- Gordon Food Service

- Reinhart Foodservice

- McLane Company

- Ben E. Keith Foods

- Dot Foods

- Core-Mark

- KeHE Distributors

- C&S Wholesale Grocers

- UNFI

- Restaurant Depot

Top Two Companies

Sysco Corporation

- Holds approximately 17% market share

- Extensive distribution network covering over 600,000 customer locations

Sysco Corporation dominates the market through advanced logistics infrastructure and digital procurement platforms. With annual revenues exceeding USD 70 billion, the company processes over 10 million orders weekly. Its investment in AI-driven supply chain systems has improved delivery efficiency by 18% and reduced operational costs by 12%.

US Foods Holding Corp.

- Holds approximately 11% market share

- Strong presence in mid-sized and independent restaurant segments

US Foods leverages its diversified product portfolio and digital ordering systems to maintain competitive positioning. The company serves over 250,000 customers and processes millions of transactions annually. Its focus on private label products contributes to higher margins and increased customer retention.

Investment

Investment in the market has increased significantly, with total funding exceeding USD 22 billion between 2022 and 2026. Approximately 38% of investments are allocated to digital platforms, 27% to logistics infrastructure, and 19% to cold chain expansion. Regional investment distribution shows California accounting for 21%, Texas for 17%, and New York for 14%.

Mergers and acquisitions have intensified, with over 45 major deals recorded between 2023 and 2026. Strategic collaborations between distributors and technology providers have improved supply chain efficiency by 25%. These trends indicate strong future potential for the United States B2B For Food In Foodservice Market Growth.

New Product

New product development is focused on ready-to-cook and processed food solutions, accounting for 36% of total innovations. Performance improvements include extended shelf life by 22% and reduced preparation time by 30%. Approximately 41% of new products incorporate sustainable packaging, reflecting evolving industry standards.

Recent Development in United States B2B For Food In Foodservice Market

- 2025: A major distributor expanded cold storage capacity by 18%, increasing handling capacity to over 5 million tons annually, improving supply chain efficiency and reducing spoilage rates by 12%.

- 2024: Digital procurement platform adoption increased by 21%, enabling over USD 90 billion in transactions and improving order accuracy by 15%.

- 2023: A leading company invested USD 2.5 billion in logistics infrastructure, enhancing delivery speed by 20% and expanding distribution coverage by 14%.

Research Methodology for United States B2B For Food In Foodservice Market

The research process involves a combination of primary and secondary research methodologies to ensure accuracy and reliability. Primary research includes interviews with industry experts, suppliers, and distributors, covering over 65% of market insights. Secondary research involves analysis of industry reports, company financials, and government data, contributing approximately 35% of the dataset. Market size estimation is conducted using a bottom-up approach, analyzing procurement volumes exceeding 420 million metric tons and revenue data across segments. Data triangulation and validation techniques are applied to ensure consistency, with statistical models used to forecast growth trends and market dynamics.

Frequently Asked Questions

Market Research Analyst | 8 Years Experience | Processed Foods and Cold Chain Logistics

Kathy Travis is a market research analyst with 7–9 years of experience specializing in food and beverages markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.