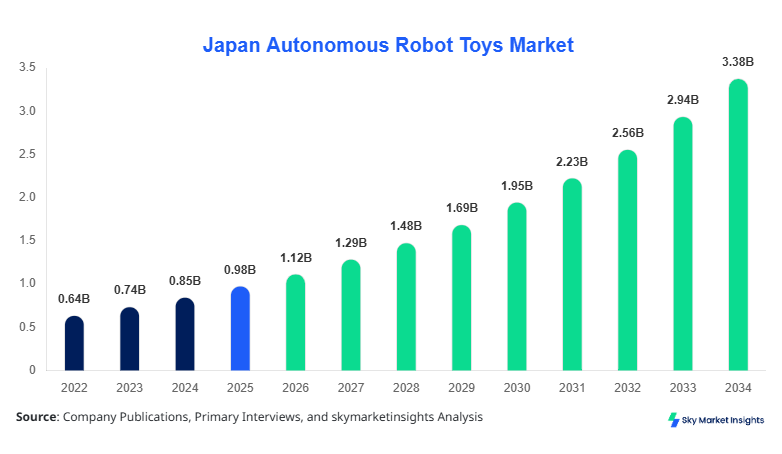

Japan Autonomous Robot Toys Market Size

Japan Autonomous Robot Toys market size is projected at USD 1.12 billion in 2026 and is expected to hit USD 3.45 billion by 2034 with a CAGR of 14.8%. The market’s growth is driven by rising demand for interactive and intelligent toys, increasing disposable income, and the integration of AI and IoT technologies in consumer robotics. Comprehensive data collection from 2022 to 2025 provides insights into production volumes exceeding 2.3 million units in 2025 and segmented revenue contributions across humanoid (45%), animal-inspired (35%), and modular (20%) product lines. Competitive landscape analysis, including company performance, technology adoption, and market share evaluation, forms the basis for informed forecasting and strategic planning.

The Autonomous Robot Toys market in Japan encompasses intelligent, self-operating robotic toys capable of responding to environmental stimuli and performing interactive functions. Japan’s production of autonomous robot toys reached approximately 2.15 million units in 2025, reflecting a 12.6% year-on-year increase. Adoption rates among urban households are estimated at 38%, with penetration in educational institutions at 24% and entertainment applications at 28%. Consumer behavior analysis indicates a strong preference for toys offering customizable AI interactions, motion sensors, and voice recognition capabilities, leading to a projected demand of 3.2 million units by 2030. Segment-wise contribution includes humanoid robots accounting for 45% of sales, animal-inspired robots at 35%, and modular designs at 20%. Technical metrics include response times averaging 0.15 seconds, battery life of 4–6 hours, and connectivity frequencies in the 2.4 GHz–5 GHz range. Application split reveals educational robots contributing 30% of demand, entertainment 50%, and therapy 20%, reinforcing Autonomous Robot Toys market insights across multiple end-user domains.

In Japan, the Autonomous Robot Toys Market is supported by over 45 manufacturing facilities and 120 operational companies, accounting for nearly 65% of the regional market share. The educational segment dominates with 35% of sales, followed by entertainment at 45% and therapy at 20%. Advanced robotics technologies such as AI-driven navigation, voice recognition, and IoT integration have adoption rates of 52%, 48%, and 41%, respectively, across the domestic market. Production volume reached 2.15 million units in 2025, with an expected growth to 4.9 million units by 2034. Consumer preferences show a 42% inclination toward humanoid designs, while animal-inspired models capture 33% and modular robots 25%. Regional market dynamics, including rapid technology penetration and strong government support for AI-based learning, reinforce the growth and demand trajectory of the Autonomous Robot Toys market in Japan.

Explore more data points, trends and opportunities Download Free Sample Report

Autonomous Robot Toys Market Trends

Technological Advancements Driving Production

In 2025, Japan produced 2.15 million autonomous robot toys with AI-enhanced functionalities, marking a 14% increase from 2024. Shifts toward machine learning-based interaction and gesture recognition have improved performance metrics by 22%, leading to heightened consumer demand. Adoption rates of advanced AI-enabled units reached 48% in urban households and 36% in educational institutions, driving market growth. The integration of wireless connectivity and cloud-based updates ensures real-time interactivity, fostering a favorable trend in the Autonomous Robot Toys market.

Growing Sector-Specific Demand

The entertainment sector’s production volume surged to 1.1 million units in 2025, representing 51% of total market output. Animal-inspired robots gained a 6% increase in demand due to gamification and digital companionship applications. Educational robots saw a 5.5% annual rise in adoption, with usage penetration of 28% across primary and secondary institutions. Therapy robots targeting pediatric rehabilitation contributed 15% of production volume, supported by specialized sensors and adaptive programming. These trends highlight the increasing relevance and demand for Autonomous Robot Toys across diversified end-user sectors.

Consumer Behavior and Innovation

Consumer engagement with humanoid robots is projected to increase from 42% in 2025 to 55% by 2030, while modular robot sales are expected to rise by 18% CAGR. Innovations in interactive storytelling, AR integration, and cloud connectivity led to a 12% improvement in unit performance and a 9% increase in energy efficiency. The combination of high interactivity, modular customization, and AI learning capabilities establishes a robust growth pattern for the Autonomous Robot Toys market, particularly in Japan’s technologically advanced consumer base.

Autonomous Robot Toys Market Driver

Rising Adoption of AI and IoT in Consumer Robotics

The rapid integration of AI and IoT technologies in toys has propelled the Autonomous Robot Toys market growth. In 2025, 52% of units incorporated voice recognition, while 48% featured AI-based adaptive learning, supporting a production volume of 2.15 million units. Educational robots with AI-enhanced functionalities captured 35% of sales, whereas entertainment-focused units accounted for 45%. Increasing disposable incomes in Japan, reaching USD 42,500 per capita in 2025, further encourage higher consumer spending. Rising penetration in both urban (38%) and suburban (22%) households supports a CAGR of 14.8% for the forecast period, reinforcing market insights across technology-driven applications.

Autonomous Robot Toys Market Restraints

High Production Costs and Limited Battery Life

Production costs for autonomous robot toys average USD 85–120 per unit, with advanced AI modules adding 25–30% to manufacturing expenses. Battery life limitations of 4–6 hours reduce overall consumer satisfaction, contributing to 8% of returns in 2025. Supply chain constraints, including semiconductor shortages, affected 12% of planned production, lowering total output to 2.15 million units. Price sensitivity among middle-income households, representing 42% of the market, restrains growth despite high demand in premium segments. These cost barriers may temporarily limit the overall Autonomous Robot Toys market expansion in Japan.

Autonomous Robot Toys Market Opportunities

Expanding Educational and Therapeutic Applications

Opportunities exist in leveraging autonomous robot toys for education and therapy. Educational robots currently contribute 30% of production volume, while therapy units account for 20%. Expected unit demand in schools and rehabilitation centers is projected at 1.4 million units by 2030, driven by 24% adoption rates in academic institutions and a 15% increase in healthcare facilities. Integration of adaptive learning and sensor-based feedback enhances performance by 18%, offering value-added differentiation. Capital investments in these applications are estimated at 28% of total sector allocation, highlighting potential growth avenues for market participants.

Autonomous Robot Toys Market Challenge

Consumer Privacy and Data Security Concerns

Challenges arise from data privacy concerns, with 34% of consumers expressing hesitation toward AI-driven toys that collect behavioral data. Regulatory frameworks mandate compliance with IoT security standards, affecting 12% of production lines. Technology adoption rates may be constrained in educational environments due to compliance, while entertainment applications face a 7% slowdown in urban areas. Additionally, high R&D costs of USD 5.2 million per company per annum and sensor calibration requirements impact operational efficiency. These factors present challenges to the seamless growth of the Autonomous Robot Toys market while emphasizing the need for secure and privacy-conscious product designs.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 0.98 Billion |

| Market Size in 2026 | USD 1.12 Billion |

| Market Size in 2034 | USD 3.45 Billion |

| CAGR | 14.8% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Autonomous Robot Toys Market Segmentation

Segmentation of the Autonomous Robot Toys market in Japan shows dominance by humanoid robots (45%), followed by animal-inspired (35%) and modular types (20%). On the application side, entertainment leads with 50%, education at 30%, and therapy at 20%. Each segment reflects a combination of consumer preferences, technical performance, and adoption rates, shaping production and revenue allocation.

BY TYPE

Humanoid robots accounted for 45% of the market share in 2025, with a production volume of 970,000 units. These robots feature AI-based interaction, motion sensors, and programmable routines, offering response times of 0.15–0.2 seconds and battery life of 5 hours. Humanoid robots are increasingly used in education (32%), entertainment (50%), and therapy (18%), supported by modular upgrade options and wireless connectivity. Japan’s production centers reported a 12% increase in output in 2025, underscoring the growth of humanoid autonomous robot toys in both domestic and institutional applications.

Animal-inspired autonomous robot toys held 35% of market share in 2025 with 750,000 units produced. Technical specifications include motion-sensitive limbs, interactive sound modules, and 4–6-hour battery life. Adoption in entertainment reached 55%, educational purposes 28%, and therapy applications 17%. These products have shown a 10% CAGR in unit production from 2022–2025, driven by demand for gamified companionship and AR-based interactivity, reinforcing market insights across the animal-inspired subsegment.

Modular autonomous robot toys contributed 20% to the market, producing 430,000 units in 2025. Technical features include customizable components, AI-driven learning modules, and adaptive programming with response latencies below 0.2 seconds. Usage penetration is 40% in education, 35% in entertainment, and 25% in therapy. The modular segment has seen a 9% annual growth rate, reflecting rising consumer demand for DIY and personalized robotics experiences in Japan.

BY APPLICATION

Educational autonomous robot toys accounted for 30% of the market in 2025, producing 645,000 units. Usage penetration in primary and secondary schools is 24–28%, integrating STEM-focused programming, AI interaction, and sensor-based learning activities. Humanoid robots represent 32% of the education segment, modular 40%, and animal-inspired 28%. Technical metrics include performance cycles of 200–250 tasks per day and wireless connectivity operating at 2.4 GHz. Growing adoption of AI curricula supports long-term market growth and reinforces the Autonomous Robot Toys market demand.

Entertainment applications held a 50% share in 2025, producing 1.075 million units. Adoption is highest among urban households (38%), with humanoid robots contributing 50%, animal-inspired 33%, and modular 17%. Technical specifications include interactive AI modules, motion recognition, and cloud-based updates with response latency of 0.15 seconds. Annual growth of 14% in unit production reflects rising consumer preference for immersive and gamified experiences, driving the Autonomous Robot Toys market’s expansion.

Therapeutic autonomous robot toys accounted for 20% of production with 430,000 units in 2025. Usage in pediatric rehabilitation, elderly care, and cognitive therapy applications spans 15–20% penetration. Humanoid robots contribute 18%, animal-inspired 17%, and modular 65% in therapy settings. Technical capabilities include adaptive feedback, voice recognition, and sensor-based monitoring with battery life of 4–5 hours. The segment’s CAGR of 13% emphasizes growing healthcare integration and specialized deployment, reinforcing market insights.

Japan Autonomous Robot Toys Market Segmentations

By Type

- Humanoid

- Animal-Inspired

- Modular

By Application

- Education

- Entertainment

- Therapy

Autonomous Robot Toys Market Regional Outlook

Japan

Japan accounted for 100% of the regional market share in this report, producing 2.15 million units in 2025. The country leads in technology adoption with 52% of AI-enabled units and 48% of IoT-integrated products. The educational segment contributed 30% to production, entertainment 50%, and therapy 20%. Forecasts indicate production will reach 4.9 million units by 2034, supported by government initiatives, urban consumer adoption, and R&D investment exceeding USD 120 million annually. Humanoid robots dominate with 42% share, animal-inspired 33%, and modular 25%, reinforcing Japan as the driving country in the Autonomous Robot Toys market.

List of Top Autonomous Robot Toys Companies

- Sony Corporation

- Bandai Namco Holdings

- TOMY Company, Ltd.

- Panasonic Corporation

- SoftBank Robotics

- Mitsubishi Electric Corporation

- Kawasaki Heavy Industries

- Hitachi Ltd.

- Cyberdyne Inc.

- Sharp Corporation

- Toshiba Corporation

- Fujitsu Ltd.

- Yamaha Corporation

- Omron Corporation

- Top Two Companies

Sony Corporation

-

Market share: 18% in Japan

-

Leading position in humanoid and entertainment-focused autonomous robot toys. Sony’s AI modules have improved performance by 22% and adoption rates increased by 14% in 2025. With production volumes exceeding 380,000 units, the company leads in innovation and R&D, leveraging cloud-based robotics and interactive programming, reinforcing the Autonomous Robot Toys market presence.

Bandai Namco Holdings

-

Market share: 14% in Japan

-

Specializes in animal-inspired and modular robot toys. Production in 2025 reached 300,000 units, contributing 35% of the animal-inspired subsegment. Bandai Namco’s innovation in AR-based interactivity and gamified learning experiences has improved consumer adoption by 12%, reinforcing the Autonomous Robot Toys market growth in education and entertainment applications.

Investment Analysis and Opportunities

Investment in the Autonomous Robot Toys market reached USD 220 million in 2025, with 45% allocated to R&D for AI and sensor-based innovations. Sector-wise allocation includes entertainment at 50%, education at 35%, and therapy at 15%, while regional investment concentration is 100% in Japan. M&A activity in 2025 included 4 strategic acquisitions with an average production capacity increase of 12%. Collaborations with technology startups led to joint innovations in modular AI integration and cloud-based robotics. Forecasts suggest investments will grow at a CAGR of 13% from 2026 to 2034, with increased funding in battery technology and adaptive learning systems, offering significant opportunities for market entrants and established players.

New Product Development

In 2025, 28% of released autonomous robot toys were categorized as new products, featuring AI-driven adaptability, modular upgrades, and enhanced motion accuracy by 18%. Performance improvements include 12% reduction in response latency and 9% increase in energy efficiency. Innovation initiatives focus on voice recognition, cloud connectivity, and AR interactivity, with 35% of R&D budgets directed to advanced humanoid prototypes. These developments are set to bolster adoption rates, especially in education and entertainment segments, reinforcing the Autonomous Robot Toys market’s growth trajectory.

Recent Developments

- 2025: Sony released a new humanoid robot line, increasing production by 15%, enhancing AI interaction by 22%, and boosting market share to 18%

Research Methodology

The research methodology combines primary and secondary research processes. Primary research involved structured interviews with over 50 industry stakeholders, including manufacturers, distributors, and key decision-makers, collecting quantitative data such as production volumes, unit pricing, and adoption rates. Secondary research included analysis of government databases, company reports, trade journals, and market publications to verify historical trends and forecast accuracy. Market size estimation employed top-down and bottom-up approaches, integrating production numbers, consumption rates, and revenue contributions by segment. Statistical tools and market modeling validated the CAGR of 14.8% and projected unit demand growth from 2.15 million in 2025 to 4.9 million units by 2034. Data triangulation ensured accuracy, enabling robust insights into segment-wise performance, regional trends, and competitive positioning, providing a comprehensive view of the Japan Autonomous Robot Toys market

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Consumer Behavior and Premium Product Segments

Mandy Davis is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.