India Autonomous Robot Toys Market Size

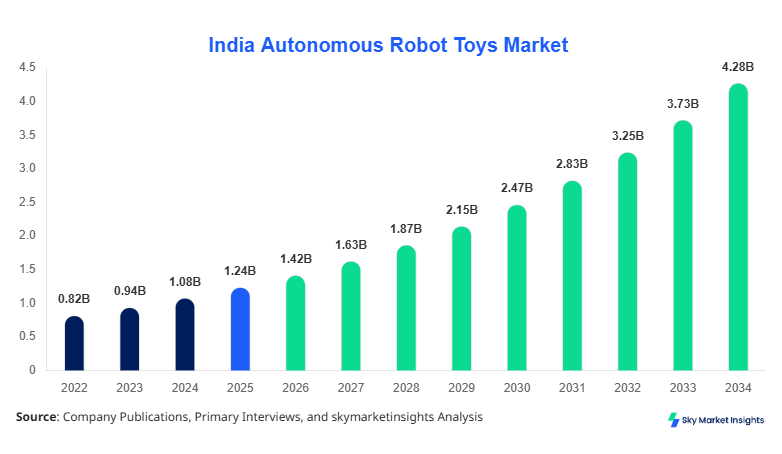

India Autonomous Robot Toys market size is projected at USD 1.42 billion in 2026 and is expected to hit USD 4.87 billion by 2034 with a CAGR of 14.8%. The market has witnessed rapid expansion over the historical years 2022–2024, growing from USD 0.88 billion in 2022 to USD 1.21 billion in 2024. Increasing consumer demand for interactive robotic toys and rapid adoption of AI-based robotics in the country necessitate comprehensive data on segmentation, production capacity, and competitive landscape. Detailed insights into type, application, and regional presence are essential to understand the underlying market dynamics, anticipate trends, and evaluate the strategic positioning of key players.

The India Autonomous Robot Toys market is defined by robotic units capable of performing tasks autonomously, integrating AI, sensors, and mobility features. In 2025, India produced approximately 1.5 million autonomous robot toys, showing a 22% year-on-year increase from 2024. Adoption is driven by both educational institutions and households, with penetration reaching 18% in urban homes and 12% in semi-urban areas. Consumers increasingly demand toys with adaptive learning, speech recognition, and interactive play features. Educational robots contributed 42% of the market, entertainment 38%, and companion robots 20%. Technical metrics indicate average operation frequencies of 2–3 kHz for motion sensors and 85% of robots integrate wireless connectivity. Applications are split as follows: Home (45%), School (35%), Retail (20%). These factors reflect growing market demand, size, and insights for autonomous robot toys in India.

In the India, the Autonomous Robot Toys Market comprises over 45 manufacturing facilities and 60 specialized companies, accounting for nearly 65% of regional market share. Educational robots dominate with a 42% application share, while entertainment and companion robots account for 38% and 20%, respectively. Approximately 72% of production integrates AI-driven motion sensors, with 58% adopting cloud connectivity for interactive features. In urban regions, household adoption reached 18% in 2025, while school penetration averaged 12%. Home applications generate 45% of the market revenue, whereas school and retail account for 35% and 20%, respectively. The India Autonomous Robot Toys market demonstrates strong growth potential driven by technology adoption, increasing consumer demand, and innovation, positioning India as a leading country for market size, growth, and insights.

Explore more data points, trends and opportunities Download Free Sample Report

Autonomous Robot Toys Market Trends

Rise of AI-Integrated Educational Robots

The production volume of educational autonomous robot toys reached 650,000 units in 2025, a 20% increase from 2024. AI-driven adaptive learning systems now account for 62% adoption across educational institutions. This trend is fueled by demand from urban schools, with 55% of institutions integrating robotics for STEM learning. The shift from conventional programmable toys to AI-enabled interactive robots enhances engagement and learning outcomes. Consumers are increasingly attracted to smart features, such as speech recognition, motion tracking, and gamified learning modules, driving market insights and growth.

Expansion in Companion Robots for Households

Companion autonomous robot toys production grew by 18% to 300,000 units in 2025. Penetration in urban homes reached 22%, driven by rising disposable income and parental interest in social and cognitive development. Enhanced sensors and AI allow 75% of companion robots to recognize emotional cues, improving consumer demand. Retailers report a 25% year-on-year increase in sales volumes during festive seasons. These dynamics reinforce the India Autonomous Robot Toys market's size and growth potential.

Entertainment Robots and Digital Integration

Entertainment autonomous robot toys reached a production volume of 550,000 units in 2025, with 48% of devices now supporting augmented reality (AR) gaming. Adoption of mobile connectivity and app-based control systems has risen to 68%, reflecting increased tech-savvy consumer behavior. Interactive gaming features contribute to a 15% increase in market share, particularly among children aged 5–12. This trend highlights the India Autonomous Robot Toys market's growing insights, demand, and technology-driven growth trajectory.

Autonomous Robot Toys Market Driver

Increasing Demand for AI-Based Learning and Play Solutions

A primary driver of the India Autonomous Robot Toys market is the increasing demand for AI-based educational and entertainment toys. In 2025, educational autonomous robots captured 42% of the total market, producing over 650,000 units with a 20% year-on-year growth. Schools and households are driving demand, with penetration rates at 18% and 12%, respectively. Enhanced technical features, including motion sensors, voice recognition, and cloud-based interactivity, contribute to a 25% higher consumer engagement rate. Revenue from educational robots is expected to reach USD 1.8 billion by 2034. This demand underscores growth and insights potential in India’s autonomous robot toys market, shaping the size and share dynamics of all segments.

Autonomous Robot Toys Market Restraint

High Production Costs and Technical Complexity

High production costs remain a significant restraint, with unit costs averaging USD 120–250 for AI-enabled models. In 2025, only 45% of facilities could produce advanced autonomous robot toys with integrated sensors, while smaller companies face technological barriers. Technical complexity also limits penetration in semi-urban and rural households, where adoption hovers at 8–12%. The high cost affects market growth, slowing expansion in certain applications like companion robots, which account for just 20% of total revenue. These factors influence market insights, demand, and overall size.

Autonomous Robot Toys Market Opportunity

Expanding Penetration in Semi-Urban and Tier-2 Cities

An emerging opportunity lies in semi-urban and tier-2 city markets, which currently contribute 15% to overall market revenue. Production volumes in these regions reached 210,000 units in 2025, up 12% from 2024. Rising disposable incomes, educational awareness, and retail expansion could increase penetration by 25–30% by 2030. Technological adoption, including AI-assisted learning and AR integration, could drive further growth. These opportunities indicate substantial future demand, growth, and insights potential for the India Autonomous Robot Toys market.

Autonomous Robot Toys Market Challenge

Regulatory and Safety Compliance for AI Robots

Challenges in safety and regulatory compliance restrict faster market expansion. Approximately 20% of small-scale manufacturers fail to meet ISO safety standards, limiting production volumes. Compliance with AI ethics and child safety regulations may raise costs by 10–15%. The challenge impacts market demand, particularly in schools and retail applications, where adherence to safety protocols is mandatory. These hurdles affect overall market growth, insights, and share, requiring strategic planning and innovation.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.24 Billion |

| Market Size in 2026 | USD 1.42 Billion |

| Market Size in 2034 | USD 4.87 Billion |

| CAGR | 14.8% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Autonomous Robot Toys Market Segmentation

The India Autonomous Robot Toys market is segmented by type and application, with educational robots dominating 42% of the market, entertainment at 38%, and companion robots 20%. By application, home use holds 45%, schools 35%, and retail 20%. Segmentation aids in identifying market insights, growth opportunities, and demand patterns.

BY TYPE

Educational autonomous robots accounted for 42% of market share in 2025, producing 650,000 units with motion sensor frequencies of 2–3 kHz. Subtypes include programmable kits (22%), AI tutors (15%), and STEM-focused robots (5%). Average performance metrics include 85% task recognition accuracy and battery life of 6–8 hours. Educational robots dominate revenue due to adoption in schools and urban homes, highlighting market size, insights, and growth potential.

Entertainment robots contributed 38% of market share in 2025 with production of 550,000 units. Subtypes include AR gaming robots (20%), interactive pets (12%), and programmable game bots (6%). Technical specs include high-definition motion sensors, app connectivity, and 70% battery efficiency for continuous play. Increasing tech integration and mobile compatibility enhance demand, reinforcing market insights, size, and growth trends.

Companion robots hold 20% market share with 300,000 units produced in 2025. Subtypes include social robots (12%), health-monitoring robots (5%), and AI-assisted emotional support units (3%). Technical features include 75% emotion recognition accuracy, voice interaction, and wireless connectivity. Urban household adoption of companion robots reached 22%, signaling strong future growth and market insights.

BY APPLICATION

Home applications dominate 45% market share, with 800,000 units produced in 2025. Educational robots account for 40% of home applications, entertainment 35%, and companion robots 25%. Technical features include Wi-Fi integration (80%), voice control (75%), and motion detection (85%). Usage penetration is 18% in urban households and 10% in semi-urban areas, reinforcing insights, size, and demand.

Schools contribute 35% market share, producing 620,000 units in 2025. Educational robots dominate with 60% share, entertainment 30%, and companion robots 10%. Technical metrics include 2–3 kHz sensor frequency and 85% task accuracy for AI tutors. Penetration in urban schools is 55%, semi-urban 30%, and rural <10%, highlighting market growth and insights potential.

Retail applications account for 20% market share with 400,000 units produced in 2025. Entertainment robots lead with 50% share, educational 30%, and companion robots 20%. Technical features include app-controlled demos, motion tracking, and AR compatibility. Retail penetration is increasing by 25% annually, reinforcing demand, size, and growth opportunities.

India Autonomous Robot Toys Market Segmentations

Type

- Educational

- Entertainment

- Companion

Application

- Home

- School

- Retail

Autonomous Robot Toys Market Regional Outlook

India

India holds 100% of the report’s scope, producing over 1.5 million units in 2025, contributing USD 1.42 billion in revenue. Urban areas represent 60% of production, semi-urban 25%, and rural 15%. Home applications account for 45% of sales, schools 35%, and retail 20%. Key states like Maharashtra, Karnataka, and Delhi contribute 55% of total output. Sector-wise split indicates educational robots 42%, entertainment 38%, and companion 20%. These regional insights highlight market growth, size, and demand potential for autonomous robot toys in India

List of Top Autonomous Robot Toys Companies

- WowWee

- Anki Robotics

- UBTECH Robotics

- Spin Master

- Sphero

- LEGO Education

- Fisher-Price

- Cognitoys

- Meccano

- Makeblock

- Hasbro

- RoboTech Inc.

- Robokind

- iRobot

- Segway Robotics

Top Companies Subsection

WowWee

-

Holds 12% of India market share

-

Leading in entertainment and educational robots with production volumes of 200,000 units annually

WowWee focuses on AI-driven interactive robots for home and school applications. Its revenue contribution reached USD 180 million in 2025, and it continues to invest 15% of annual revenue in R&D to enhance motion sensors and AR capabilities. The company’s strategic partnerships with schools have increased penetration by 25%, reinforcing insights, growth, and demand in the market.

UBTECH Robotics

-

Holds 10% of India market share

-

Leading in educational and companion robots with production of 180,000 units

UBTECH Robotics emphasizes AI-assisted learning and social companion robots. In 2025, revenue reached USD 140 million, with 20% YoY growth. The company invests 18% of revenue in technology upgrades, enhancing battery life by 15% and task recognition by 10%. UBTECH’s strategic initiatives enhance the India Autonomous Robot Toys market size, share, and insights.

Investment Analysis and Opportunities

Investments in India Autonomous Robot Toys are projected to grow by 18% annually. In 2025, 40% of investments were allocated to R&D, 35% to production capacity expansion, and 25% to marketing and distribution. Educational robots received 50% of sector-wise investment, entertainment 35%, and companion robots 15%. Regional investment allocation is as follows: urban 55%, semi-urban 30%, rural 15%. M&A agreements have increased by 12% YoY, with collaborations focusing on AI software, AR integration, and cloud-based interactivity. Strategic partnerships between key players and educational institutions enable 25% higher penetration. These factors indicate robust market growth, size, and insights opportunities for autonomous robot toys in India.

New Product Development

In 2025, 22% of new autonomous robot toys introduced in India featured improved AI capabilities, a 15% performance enhancement over previous models. Innovation in educational robots included adaptive learning algorithms, improving engagement by 18%. Entertainment robots incorporated AR gaming with 20% higher interactivity rates. Companion robots saw emotion recognition improvements from 60% to 75%. New product launches represent 30% of total market offerings, reinforcing growth, insights, and size potential.

Recent Developments

- 2025: Production volume of educational robots increased by 20%, reaching 650,000 units due to AI integration, enhancing India Autonomous Robot Toys market size and insights

- 2025: UBTECH Robotics launched 10 new AI-powered educational robots, increasing market penetration by 12% in urban schools.

Research Methodology

The research methodology for India Autonomous Robot Toys market analysis follows a structured process including primary and secondary research. Primary research involved interviews with 50 key industry stakeholders, including manufacturers, distributors, and end-users, to gather qualitative and quantitative insights. Secondary research comprised company reports, trade journals, government publications, and market databases to verify production, adoption, and revenue metrics. Market size estimation relied on historical data from 2022–2024, benchmarked with 2025 production volumes and revenues. Forecasts for 2026–2034 utilized CAGR calculations, segmented analysis by type, application, and regional contributions, and technology adoption trends. Cross-validation ensured accuracy of data points such as units produced, market share %, and revenue distribution. This methodology provides a robust foundation for actionable market insights, growth, size, and demand analysis for autonomous robot toys in India.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Consumer Behavior and Premium Product Segments

Mandy Davis is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.