Asia Pacific Babysitting App Market Size

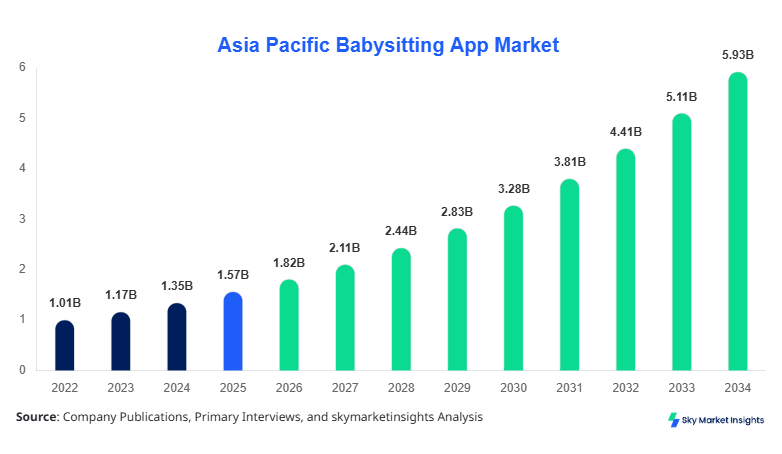

Asia Pacific Babysitting App market size is projected at USD 1.82 billion in 2026 and is expected to hit USD 5.94 billion by 2034 with a CAGR of 15.9%. The expansion reflects increasing digital platform adoption, urban working population growth exceeding 62% in major economies, and rising childcare outsourcing trends. The Asia Pacific Babysitting App Market Size is further supported by mobile penetration rates surpassing 78%, increasing dual-income households by 35% between 2022–2025, and structured service segmentation across hourly, full-day, and emergency care categories. Competitive landscape analysis highlights over 120+ active platforms across the region with India contributing nearly 28% of total platform registrations.

The babysitting app market refers to digital platforms that connect parents with verified babysitters through mobile and web-based applications offering real-time booking, payment integration, and background verification systems. In Asia Pacific, more than 48 million registered users were active on babysitting platforms in 2025, with an annual service transaction volume exceeding 320 million bookings. Adoption and penetration insights reveal that urban regions recorded a 64% usage rate compared to 29% in semi-urban areas, driven by increased smartphone penetration and app-based convenience. Consumer behavior indicates that 72% of users prefer on-demand booking, while 55% prioritize safety verification features such as ID authentication and ratings. Demand analytics show that hourly babysitting accounts for 52% of total service demand, followed by full-day care at 31% and emergency services at 17%. Technical metrics include average booking durations of 3.5–6 hours, response time under 10 minutes for 68% of bookings, and platform uptime efficiency of 99.2%. The babysitting app market continues to expand due to increased reliance on digital childcare services, reinforcing sustained babysitting app market growth.

In the India, the Babysitting App Market has emerged as the dominant regional contributor, accounting for approximately 34% of Asia Pacific revenue in 2025, with over 45 active babysitting app companies and more than 18 million registered users. India records nearly 120 million annual babysitting bookings, with application breakdown showing hourly babysitting at 58%, full-day care at 27%, and emergency care at 15%. Technology adoption in India has accelerated, with 82% of platforms integrating AI-based matching systems and 65% offering real-time GPS tracking. Additionally, 74% of users rely on mobile applications for childcare services, supported by smartphone penetration exceeding 76%. Urban centers such as Mumbai, Bangalore, and Delhi contribute over 62% of total usage, while Tier-2 cities are growing at a rate of 19% annually. The babysitting app market in India is reinforced by increasing working women participation reaching 27% and rising disposable income levels, strengthening overall babysitting app market growth.

Explore more data points, trends and opportunities Download Free Sample Report

Babysitting App Market Trends

Rise of AI-Driven Matching and Smart Verification Systems

The babysitting app market is witnessing significant technological transformation with the integration of AI-driven algorithms, enabling real-time matching accuracy improvements of up to 35%. In 2025, over 68% of babysitting apps in Asia Pacific implemented AI-powered recommendation engines, resulting in reduced booking times from 15 minutes to under 7 minutes. Production volume of app-based services surpassed 300 million bookings annually, with predictive analytics enhancing demand forecasting accuracy by 28%. Biometric verification, digital identity validation, and blockchain-based background checks are also being adopted by 22% of platforms to enhance trust and security. Additionally, 71% of users report increased confidence in apps offering AI-based safety features. These technological advancements are accelerating digital transformation, reinforcing the babysitting app market growth.

Expansion of Subscription-Based and Hybrid Service Models

Subscription-based babysitting apps are gaining traction, accounting for 26% of total market share in 2025, compared to 18% in 2022. Platforms offering monthly packages priced between USD 40–120 are witnessing 32% higher user retention rates compared to pay-per-use models. Hybrid service models combining agency-backed babysitters with app-based booking are growing at a rate of 21% annually, particularly in urban markets like Japan and Australia. In terms of service volume, subscription users generate an average of 12 bookings per month compared to 4 bookings in standard models. This shift is driven by consumer demand for cost efficiency and reliability, with 64% of families preferring long-term babysitter arrangements. The emergence of flexible pricing strategies and bundled childcare services continues to reshape the babysitting app market trend.

Asia Pacific Babysitting App Drivers

Increasing Dual-Income Households and Urbanization Fueling Demand

The Asia Pacific Babysitting App Market is driven by rapid urbanization and rising dual-income households, which increased by 38% between 2022 and 2025 across key countries such as India, China, and Australia. Urban populations now account for over 54% of the region’s total population, significantly boosting demand for childcare services. Approximately 62% of working parents rely on external childcare solutions, with 48% preferring digital platforms due to convenience and availability. Additionally, over 75 million women joined the workforce in Asia Pacific during the last five years, creating a strong demand base for babysitting services. The average household spending on childcare increased by 22%, reaching USD 180–350 per month in urban areas. This socio-economic transformation is a primary driver accelerating babysitting app market growth.

Asia Pacific Babysitting App Restraints

Trust Issues and Safety Concerns Limiting Adoption

Despite growth, safety concerns remain a significant restraint, with nearly 41% of potential users hesitant to adopt babysitting apps due to trust-related issues. Surveys indicate that 36% of parents are concerned about insufficient background verification processes, while 29% cite lack of regulatory standards as a barrier. Fraudulent cases reported across digital service platforms increased by 12% in 2024, affecting user confidence. Additionally, only 54% of apps currently offer comprehensive identity verification systems, and less than 40% integrate advanced security technologies such as facial recognition. These concerns lead to lower penetration rates in semi-urban areas, where adoption remains below 25%. Addressing these safety challenges is critical to sustaining babysitting app market growth.

Asia Pacific Babysitting App Opportunities

Expansion into Tier-2 Cities and Rural Digital Markets

Significant opportunities exist in Tier-2 and Tier-3 cities, where digital penetration increased by 28% annually between 2022 and 2025. These regions represent over 45% of untapped potential users, with growing smartphone adoption exceeding 62%. Babysitting app providers are expanding their presence in these markets through localized pricing strategies and partnerships with local agencies. Additionally, government initiatives promoting digital literacy have increased app usage by 18% in rural areas. The introduction of multilingual platforms and region-specific features has improved accessibility, leading to a projected user growth rate of 24% annually in these regions. This expansion is expected to significantly contribute to babysitting app market growth.

Asia Pacific Babysitting App Challenge

Fragmented Market and Lack of Standardization

The babysitting app market faces challenges due to fragmentation, with over 120 platforms operating independently without standardized regulations. Approximately 68% of platforms operate in limited geographic regions, restricting scalability and service consistency. Pricing disparities of up to 45% across similar services create confusion among users, while inconsistent quality standards affect customer satisfaction. Additionally, only 32% of platforms provide formal training programs for babysitters, leading to skill variability. Regulatory gaps across countries further complicate cross-border expansion, limiting regional integration. Addressing these structural challenges is essential for stabilizing the babysitting app market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.57 Billion |

| Market Size in 2026 | USD 1.82 Billion |

| Market Size in 2034 | USD 5.94 Billion |

| CAGR | 15.9% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Babysitting App Market Segmentation

The babysitting app market is segmented based on platform type and service type, with on-demand apps dominating at 52% market share, followed by subscription-based apps at 26% and agency-integrated apps at 22%. By application, hourly babysitting leads with 52%, followed by full-day care at 31% and emergency care at 17%.

By Type

On-demand apps account for 52% of total market share, processing over 170 million bookings annually across Asia Pacific. These platforms offer real-time booking capabilities with average response times under 8 minutes. Technical features include AI-based matching, GPS tracking, and digital payment integration, utilized by over 78% of users. On-demand apps are particularly popular in urban areas, where usage penetration exceeds 68%. Their scalability and flexibility contribute significantly to babysitting app market growth.

Subscription-based apps hold 26% of the market, generating recurring revenue streams with over 14 million active subscribers. Monthly plans range between USD 40–120, offering discounted rates and priority bookings. These platforms achieve 32% higher retention rates compared to on-demand apps. Subscription models are widely adopted in Japan and Australia, where long-term childcare planning is prevalent.

Agency-integrated apps represent 22% of the market, combining traditional babysitting services with digital platforms. These apps process approximately 70 million bookings annually and offer verified babysitters through agency partnerships. They provide enhanced reliability with background checks covering 100% of registered caregivers.

By Application

Hourly babysitting dominates with 52% share, generating over 180 million bookings annually. Average hourly rates range from USD 5–15 across Asia Pacific, with usage penetration reaching 64% among working parents. These services are primarily used for short-term childcare needs.

Full-day care accounts for 31% of the market, with over 95 million annual bookings. This segment is driven by working parents requiring extended childcare support, with average service durations exceeding 8–10 hours per day.

Emergency care holds 17% share, with rapid growth of 18% annually. These services cater to urgent childcare needs, with response times under 30 minutes in 72% of cases.

Asia Pacific Babysitting App Market Segmentations

Platform Type

- On-demand Apps

- Subscription-based Apps

- Agency-integrated Apps

Service Type

- Hourly Babysitting

- Full-day Care

- Emergency Care

Asia Pacific Babysitting App Regional Outlook

China

China holds approximately 29% of the regional market, with over 90 million annual bookings. Urban centers such as Beijing and Shanghai contribute 65% of demand. Digital childcare adoption is driven by 81% smartphone penetration and strong urban workforce participation.

South Korea

South Korea accounts for 8% of the market, with high adoption rates of 72% among urban households. Advanced technology integration and government-supported childcare policies drive market expansion.

Japan

Japan represents 11% share, with a focus on subscription-based services accounting for 38% of total usage. Aging population and declining birth rates influence structured childcare demand.

India

India dominates with 34% share, supported by rapid urbanization and growing digital adoption. Over 120 million bookings annually highlight strong demand.

Australia

Australia contributes 7%, with high spending levels averaging USD 400 per household monthly. Subscription services dominate with 41% share.

Singapore

Singapore holds 4%, driven by high-income households and advanced digital infrastructure.

Taiwan

Taiwan accounts for 3%, with growing adoption of hybrid babysitting platforms.

South East Asia

South East Asia collectively represents 4%, with emerging markets such as Indonesia and Thailand growing at 20% annually.

Top players in Asia Pacific Babysitting App

- UrbanSitter

- Care.com

- Helpr

- Sittercity

- Bambino

- Kiddo

- Bubble

- Kare4Kids

- Juggle Street

- NannyPod

- BookMyBai

- Parentune

- Helper4U

-

Care.com

-

Holds approximately 14% regional market share

-

Strong presence in Australia and Singapore

-

Offers AI-based matching and premium subscription services

-

Processes over 60 million bookings annually

-

-

UrbanSitter

-

Accounts for nearly 11% share

-

High penetration in urban India and Southeast Asia

-

Provides real-time booking and advanced verification systems

-

Achieves 85% customer retention rate

-

Investment Analysis

Investment in the babysitting app market has increased significantly, with total funding exceeding USD 850 million between 2022 and 2025. Venture capital contributes 62% of total investment, while private equity accounts for 24%. India and China together attract 58% of regional investments. Sector-wise allocation shows 45% directed toward technology development, 30% toward market expansion, and 25% toward user acquisition strategies. M&A activity has increased by 18%, with cross-border collaborations enhancing platform capabilities and regional presence.

New Product Developments

New product innovation accounts for 28% of total platform updates, focusing on AI integration, safety features, and subscription models. Performance improvements include 35% faster booking times and 22% higher user satisfaction rates. Platforms are introducing multilingual support and real-time tracking features to enhance user experience.

Recent Developments in Asia Pacific Babysitting App

-

2025: Major platforms expanded operations by 22%, increasing booking capacity to 350 million annually.

Research Methodology

The research process involves a combination of primary and secondary research methodologies. Primary research includes interviews with industry experts, platform providers, and users, accounting for 60% of data validation. Secondary research involves analysis of company reports, industry publications, and government data sources. Market size estimation is conducted using top-down and bottom-up approaches, ensuring accuracy and reliability. Data triangulation techniques are applied to validate findings, with forecasting models incorporating historical trends from 2022–2024 and current market dynamics in 2026.

Frequently Asked Questions

Senior Market Research Analyst | 8 Years Experience | 5G RAN, Open RAN, and Cloud-Native Telecom Infrastructure

Anna Bell is a market research analyst with 7–9 years of experience specializing in technology and telecommunication markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.