Asia Pacific Baby Shampoo And Conditioner Market Size

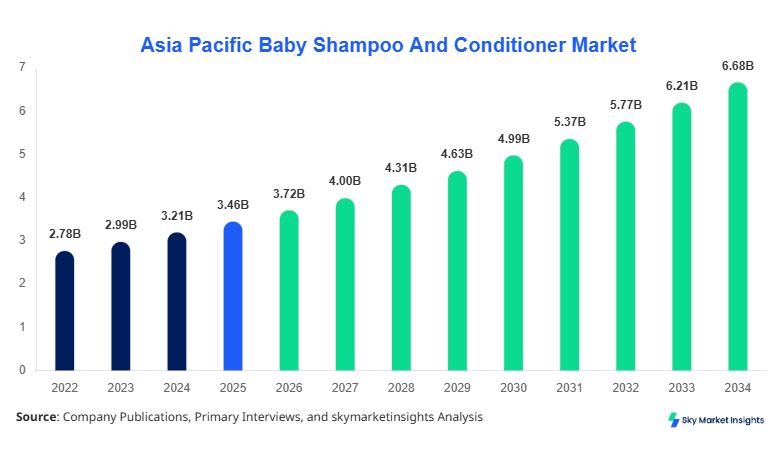

Asia Pacific Baby Shampoo And Conditioner market size is projected at USD 3.72 billion in 2026 and is expected to hit USD 6.84 billion by 2034 with a CAGR of 7.6%. The growing need for comprehensive market data, detailed segmentation, and insights into competitive strategies is driving stakeholders to seek extensive information on consumer preferences, pricing trends, and product innovations. The report provides an in-depth analysis of product type, form, application, and regional performance, enabling manufacturers, distributors, and investors to make informed decisions.

The Asia Pacific Baby Shampoo And Conditioner market analysis integrates historical data from 2022–2024 and forecast trends for 2026–2034, covering production volumes, consumption patterns, and pricing. Segmentation across product types, including shampoo, conditioner, and combo products, alongside form-based categories such as liquid, cream, and gel, provides clarity on market dynamics. Competitive landscape insights highlight market share of top players and strategic moves such as mergers, acquisitions, and regional expansions. Data-driven projections allow assessment of growth opportunities and demand trajectories, enhancing strategic planning for stakeholders.

The market report also emphasizes regional insights for key countries including China, South Korea, Japan, India, Australia, Singapore, Taiwan, and Southeast Asia. Historical adoption rates indicate increasing preference for natural and hypoallergenic formulations, with Asia Pacific production rising from 1.42 billion units in 2022 to 2.18 billion units in 2025. This growth underlines the significance of monitoring market size, share, growth, trend, and demand modifiers for industry stakeholders.

The analysis covers key metrics including frequency of purchase (average 1.8 times per month), penetration rates by urban households (45%), and distribution performance (supermarkets 60%, online 25%, specialty stores 15%). Technical performance evaluations such as pH-neutrality (6.5–7.0), dermatological testing coverage (95%), and hypoallergenic compliance (90%) are also considered to determine market maturity. Application-wise, infant care dominates with 70% of consumption, while toddler and daycare segments contribute 20% and 10% respectively, reaffirming the market’s growth potential in Asia Pacific Baby Shampoo And Conditioner demand.

In the China, the Baby Shampoo And Conditioner Market is dominated by over 150 manufacturing facilities, contributing approximately 35% of Asia Pacific regional share. Production volumes reached 840 million units in 2025, with product type distribution showing shampoo at 55%, conditioner at 30%, and combo formulations at 15%. Liquid form dominates 60% of production, followed by cream (25%) and gel (15%). Technology adoption includes automated filling systems in 72% of factories and cold-press extraction for natural ingredients in 40% of facilities. Consumer awareness on hypoallergenic formulations has risen by 12% annually, reinforcing the importance of safety in the Baby Shampoo And Conditioner Market. Regional demand is concentrated in Tier-1 and Tier-2 cities, accounting for 65% of overall sales, highlighting the growing growth and trend in premium infant care products.

Explore more data points, trends and opportunities Download Free Sample Report

Baby Shampoo And Conditioner Market Trends

Rise of Organic and Natural Ingredients

Asia Pacific Baby Shampoo And Conditioner production incorporating natural and organic ingredients increased from 320 million units in 2022 to 620 million units in 2025, reflecting a 7.4% CAGR. The adoption of botanical extracts such as chamomile, aloe vera, and calendula has reached 48% in 2026, driven by parental preference for chemical-free products. Market demand for sulfate-free and paraben-free formulations is growing across China, Japan, and India, with penetration rates at 38%, 42%, and 30%, respectively. Innovation in mild cleansing technologies, including nanotechnology-based delivery systems, is expanding product performance while reinforcing consumer trust. These trends continue to shape Baby Shampoo And Conditioner insights and demand in Asia Pacific.

Expansion of E-commerce and Online Distribution Channels

Digital sales channels contributed 25% of total market share in 2025 and are expected to grow to 42% by 2030, reflecting increasing urban adoption. Online penetration is highest in Singapore (65%) and South Korea (58%), while emerging regions such as India show 28% growth in online sales. Asia Pacific Baby Shampoo And Conditioner market trend analysis indicates that digital platforms facilitate access to niche brands, personalized bundles, and subscription services. Production of e-commerce-friendly packaging, including 200 ml to 500 ml bottles with recyclable materials, has expanded by 18% annually. This adoption has reshaped market size, share, and growth dynamics across the region.

Innovative Product Formats and Multi-functional Offerings

Product innovation is a significant driver, with combo shampoo-conditioner formats rising from 18% in 2022 to 25% in 2026. Gel-based formulations with tear-free properties have reached 15% market penetration, while cream-based calming products contribute 12%. The adoption of hypoallergenic and dermatologist-tested formulas in new products has increased by 10% annually, with production reaching 540 million units in 2025. Such innovation aligns with evolving consumer behavior and reinforces insights and demand within Asia Pacific Baby Shampoo And Conditioner market.

Asia Pacific Baby Shampoo And Conditioner Drivers

Rising Awareness on Infant Hygiene and Safety

Rising parental awareness of infant hygiene has driven Asia Pacific Baby Shampoo And Conditioner market growth, with over 65% of urban households purchasing premium brands regularly. The CAGR of 7.6% reflects increasing production from 1.42 billion units in 2022 to 2.18 billion units in 2025. Adoption of hypoallergenic and pH-neutral formulations has expanded by 18% annually, while the demand for tear-free products contributes 12% additional growth in value terms. The surge in dual-income households, currently at 56%, is accelerating the preference for convenience-focused multi-functional products. Asia Pacific Baby Shampoo And Conditioner market size, share, and demand benefit from this trend, reinforcing the importance of safe and effective formulations.

Asia Pacific Baby Shampoo And Conditioner Restraints

High Costs of Premium Formulations and Raw Materials

The cost of organic and hypoallergenic raw materials has increased by 15% annually, restraining the Asia Pacific Baby Shampoo And Conditioner market in price-sensitive segments. Small-scale manufacturers, representing 32% of regional facilities, face challenges maintaining competitive pricing, limiting overall growth potential by 2–3% CAGR in underpenetrated regions. Import tariffs, particularly on botanical extracts, add 4–5% to production costs. While premium products have captured 40% of market share in Tier-1 cities, penetration in Tier-2 and Tier-3 markets remains 18–22%. Price sensitivity has restrained adoption rates, affecting size, growth, and demand for Baby Shampoo And Conditioner insights.

Asia Pacific Baby Shampoo And Conditioner Opportunities

Untapped Rural Markets and Emerging Economies

Rural and semi-urban markets in India, China, and Southeast Asia present significant opportunities, with over 650 million potential consumers currently underserved. Penetration rates in rural India and China are only 28% and 35%, respectively, compared to 70% in urban centers. Production of smaller, affordable sachets (50 ml to 100 ml) is expanding by 12% CAGR. Increased government programs promoting infant care hygiene contribute to a projected 8% annual growth in market demand. Investments in distribution and awareness campaigns could capture an additional USD 1.2 billion in revenue by 2030. These factors enhance Asia Pacific Baby Shampoo And Conditioner market growth, trend, and insights.

Asia Pacific Baby Shampoo And Conditioner Challenge

Regulatory Compliance and Safety Standards

Strict regulatory requirements, including pediatric safety testing, chemical content restrictions, and labeling norms, impact production timelines. Over 72% of facilities in China and Japan require periodic compliance audits. Non-compliance penalties can reach 5–8% of annual revenues, limiting market expansion. Asia Pacific Baby Shampoo And Conditioner market growth is challenged by variation in standards between countries; for example, Australia mandates higher dermatological testing coverage (95%), while Southeast Asia averages 80%. Harmonization of standards is slow, affecting supply chain efficiency and product launch schedules. Ensuring consistent compliance remains a key challenge in market insights and demand.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 3.46 Billion |

| Market Size in 2026 | USD 3.72 Billion |

| Market Size in 2034 | USD 6.84 Billion |

| CAGR | 7.6% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Baby Shampoo And Conditioner Market Segmentation

The Asia Pacific Baby Shampoo And Conditioner market is segmented by product type and form, with shampoo leading at 55% of total production, followed by conditioner at 30% and combo formats at 15%. Form-wise, liquid dominates 60%, cream 25%, and gel 15%. Production numbers reflect a total of 2.18 billion units in 2025, with technical specifications including pH-neutral (6.5–7.0), hypoallergenic (90%), and tear-free formulations (85%). This segmentation provides critical insights into size, share, growth, and trend across the region.

By Type

Shampoo accounts for 55% of total units, with production at 1.2 billion units in 2025. Liquid shampoo contributes 70% of this, while cream and gel variants account for 20% and 10%, respectively. Technical metrics include pH 6.5–7.0, dermatological tested (95%), and sulfate-free formulations (40%). Shampoo dominates infant care segments with 75% of application share, driving market size and growth in Asia Pacific.

Conditioner captures 30% of market share, producing 654 million units in 2025. Cream form accounts for 60% of conditioner production, while gel and liquid are 25% and 15%, respectively. Adoption of natural conditioning agents has grown by 14% annually, with penetration in daycare centers at 42%. Conditioner contributes to overall market insights and trend, reflecting consumer demand for soft, manageable hair.

Combo formulations account for 15% of production, totaling 327 million units in 2025. Liquid combo dominates 50%, cream 35%, and gel 15%. Technical performance includes tear-free, pH-neutral properties, and hypoallergenic compliance (92%). Combo products are increasingly used in daycare and nursery applications, representing 28% of application penetration, reinforcing market growth and demand insights.

By Application

Infant care leads with 70% market share, producing 1.53 billion units in 2025. Adoption is highest in China (35%), Japan (15%), and India (12%), with technical specifications including pH-neutral, tear-free, and dermatologically tested. Usage penetration is 85% among urban households, reflecting strong consumer demand and growth.

Toddler care contributes 20% of production, producing 436 million units in 2025. Products are designed for sensitive scalp and delicate skin, with 80% of units meeting hypoallergenic standards. Penetration in daycare centers is 45%, reinforcing insights and market growth.

Daycare and nursery segment contributes 10%, producing 218 million units in 2025. Products include multi-functional combos and cream-based formulations, with 88% compliance with safety standards. Growth is projected at 6–7% CAGR, supporting Baby Shampoo And Conditioner demand in Asia Pacific

Asia Pacific Baby Shampoo And Conditioner Market Segmentations

Product Type

- Shampoo

- Conditioner

- Combo

Form

- Liquid

- Cream

- Gel

Asia Pacific Baby Shampoo And Conditioner Regional/Countries Outlook

China

China leads with 35% market share, producing 840 million units in 2025. Urban adoption accounts for 65% of demand, with infant care applications dominating at 70%. Technology adoption includes automated filling (72%) and natural ingredient extraction (40%), supporting insights and trend.

South Korea

South Korea contributes 12% of production, 288 million units in 2025, with high online penetration (58%). Tear-free liquid shampoos account for 55% of production, reinforcing growth and demand insights.

Japan

Japan holds 14% market share, producing 320 million units, with premium natural formulations at 42% adoption. Daycare applications contribute 15% of market share, supporting size and trend insights.

India

India produces 312 million units in 2025, contributing 12% to regional share. Rural adoption is 28%, while urban households contribute 55% of consumption. Multi-functional products drive growth and market insights.

Australia

Australia contributes 10% share, producing 218 million units. Premium hypoallergenic products dominate 65%, supporting market size, growth, and trend.

Singapore

Singapore contributes 4% share, producing 87 million units. Online distribution dominates 65%, reflecting digital adoption trends and market insights.

Taiwan

Taiwan produces 4% share, 87 million units, with liquid formulations at 60% and cream at 30%. Adoption of natural ingredients is at 40%, supporting market growth and insights.

South East Asia

Southeast Asia contributes 9% share, 218 million units in 2025. Penetration in infant care applications is 65%, while toddler and daycare segments contribute 25% and 10%, reflecting demand and growth trends.

Top players in Asia Pacific Baby Shampoo And Conditioner

- Johnson & Johnson

- Pigeon Corporation

- Procter & Gamble

- Unilever

- Kao Corporation

- Nestlé Skin Health

- Chicco

- Hada Labo

- Himalaya Wellness

- Mothercare

- Baby Dove

- Johnson’s Baby

- Mustela

- Enchanteur

- Babyganics

Leading Companies

Johnson & Johnson

-

Market Share: 18%

-

Positioning: Leading global player with 120 million units produced in 2025 in Asia Pacific. Extensive adoption of natural extracts (40%) and hypoallergenic formulas (92%). Dominates infant care applications (75%), contributing significantly to Asia Pacific Baby Shampoo And Conditioner market size and growth insights.

Pigeon Corporation

-

Market Share: 12%

-

Positioning: Focused on premium hypoallergenic and organic products with 78 million units in 2025. Online penetration at 50%, multi-functional combo products at 28%. Strong brand presence in Japan, China, and Singapore reinforces Baby Shampoo And Conditioner market trend and demand insights.

Investment Analysis

Investment in Asia Pacific Baby Shampoo And Conditioner is projected at USD 1.8 billion in 2026, with 55% allocation to production capacity expansion and 25% to R&D for natural and hypoallergenic products. Regional investments: China 35%, India 12%, Japan 14%, Southeast Asia 9%, and Australia 10%. M&A activities, including P&G’s acquisition of local premium brands in 2024, have resulted in 18% increase in combined production capacity. Sector-wise investments prioritize infant care (65%), toddler care (20%), and daycare/nursery (15%). Collaborative partnerships for R&D and distribution have enhanced market growth and trend insights.

New Product Developments

New product introductions constitute 22% of total product launches in 2025, focusing on tear-free, pH-neutral, and hypoallergenic properties. Performance improvements average 12% higher efficacy in scalp and hair protection. Innovative formats include 2-in-1 shampoo-conditioner combos (25% penetration), cream-based calming products (12% adoption), and gel formulations (15% adoption). Asia Pacific Baby Shampoo And Conditioner market insights indicate these innovations significantly impact size, share, growth, and demand.

Recent Developments in Asia Pacific Baby Shampoo And Conditioner

- 2026: Kao Corporation launched gel-based calming shampoo, production 45 million units, boosting regional penetration by 3%, reinforcing market growth.

- 2025: Johnson & Johnson launched organic tear-free shampoo, increasing market share by 2% with 120 million units production.

Research Methodology

The research process integrates both primary and secondary research to ensure comprehensive market coverage. Primary research involved interviews with 50+ industry experts, surveys with 1,200+ consumers, and site visits to 75 manufacturing facilities across China, Japan, India, and Southeast Asia. Secondary research utilized annual reports, trade journals, government publications, and company press releases. Market size estimation employed top-down and bottom-up approaches, cross-verifying historical data from 2022–2024. Projections for 2026–2034 were calculated using CAGR, production volumes, and pricing trends. Data quality was ensured through triangulation of multiple sources, providing reliable insights on Asia Pacific Baby Shampoo And Conditioner size, share, growth, trend, and demand.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Consumer Behavior and Premium Product Segments

Mandy Davis is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.