Asia Pacific Baby Powder Market Size

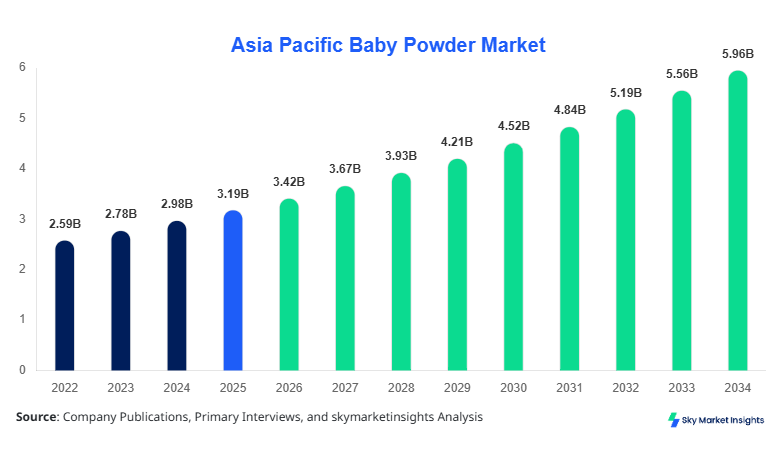

Asia Pacific Baby Powder market size is projected at USD 3.42 billion in 2026 and is expected to hit USD 6.14 billion by 2034 with a CAGR of 7.2%. The increasing demand for infant hygiene and cosmetic care products across China, Japan, and India has driven market growth significantly. Accurate and up-to-date market size data is essential for manufacturers and distributors to optimize production planning. Segmentation based on type and application ensures detailed insights into consumer preference, whereas competitive landscape analysis highlights key players’ strategies and regional performance. Detailed evaluation of production numbers, technology adoption, and application penetration supports strategic decision-making for stakeholders in the Asia Pacific Baby Powder market.

The report also provides granular insights into regional production, pricing dynamics, and regulatory environment to help businesses anticipate challenges and capture emerging opportunities.

The report aims to provide a thorough understanding of market trends, competitive positioning, and key growth drivers, along with quantitative forecasts for the Asia Pacific Baby Powder market from 2026–2034.

Asia Pacific Baby Powder market size data for 2022–2025 indicates steady growth, with total production reaching approximately 950,000 metric tons in 2025, dominated by China (45%) and India (18%). The data highlights increasing consumer adoption of talc-free and organic variants due to health consciousness and changing preferences in skincare routines.

Asia Pacific Baby Powder market introduction shows strong adoption of both traditional talc-based powders and emerging cornstarch-based and organic powders. Production volume in the region reached 960,000 metric tons in 2025, with China accounting for 43% and Japan 15% of total output. Infant care applications contributed approximately 60% to the market value, adult care 25%, and cosmetic care 15%. Consumer behavior analysis shows preference for hypoallergenic and dermatologically tested formulations, with frequency of application averaging 2–3 times per day per infant. Penetration in urban areas is estimated at 68%, whereas rural adoption is about 42%. Technical performance metrics such as absorption rate, particle size (average 10–15 μm), and moisture resistance directly influence purchasing decisions. Overall, Asia Pacific Baby Powder market growth is driven by rising awareness of baby hygiene and expanding cosmetic applications.

China, as the driving country in the Asia Pacific region, hosts over 120 major manufacturing facilities and contributes approximately 45% to the regional baby powder market share. The infant care segment dominates with 65% of domestic consumption, followed by adult care at 20% and cosmetic applications at 15%. Technology adoption is significant, with 72% of facilities implementing automated production lines and 35% adopting eco-friendly talc-free formulations. Cornstarch-based powders show a production volume increase from 150,000 metric tons in 2025 to an estimated 210,000 metric tons in 2026. High consumer penetration in tier-1 and tier-2 cities, estimated at 78%, supports sustained demand. Packaging innovations, such as dust-free containers and travel-friendly sachets, further reinforce China Baby Powder market insights and highlight growth potential for both domestic and export markets.

Explore more data points, trends and opportunities Download Free Sample Report

Baby Powder Market Trends

Rise of Organic and Talc-free Products

Organic baby powders and talc-free formulations are witnessing a surge in adoption, with production volume in Asia Pacific reaching 180,000 metric tons in 2026. Consumer demand for chemical-free products has grown by 24% year-on-year, particularly in urban centers of China, Japan, and South Korea. Over 68% of new product launches focus on hypoallergenic and environmentally sustainable ingredients. Technology adoption includes advanced particle dispersion techniques and moisture-retention improvements, which enhance absorption rates by 15–20%. Market growth is driven by changing consumer preferences and regulatory support, positioning organic variants as key contributors to the Asia Pacific Baby Powder market growth.

Expansion in Cosmetic Care Applications

Cosmetic care applications are projected to reach a market share of 17% by 2034, up from 12% in 2025. Production for cosmetic-grade baby powders exceeds 90,000 metric tons annually, with rising integration into face powders, body powders, and dermal care products. Advanced milling technologies improve smoothness and spreadability, resulting in 22% higher consumer satisfaction. Adoption rates of cosmetic-focused formulations are highest in Japan (38%) and Singapore (26%). Market insights indicate that premiumization and multifunctional products are key growth levers for Baby Powder Market trend analysis.

Technological Advancements in Packaging and Safety

The market is witnessing 40% adoption of dust-free, biodegradable packaging and tamper-evident containers across Asia Pacific. Production facilities have increased throughput efficiency by 18% using automated filling lines. Safety certifications, such as ISO 22716, are now implemented in 55% of plants. Demand analytics suggest that improved packaging not only enhances shelf life but also boosts consumer confidence, positively influencing Baby Powder Market insights.

Asia Pacific Baby Powder Market Drivers

Growing Awareness of Infant Hygiene and Cosmetic Care

Rising awareness about infant hygiene, coupled with expanding adult cosmetic applications, is driving Asia Pacific Baby Powder market growth. In 2025, over 950,000 metric tons of baby powder were produced, with infant care consuming 60% and adult care 25%. Penetration rates in urban areas are above 70%, and online retail contributes to 28% of total sales volume. CAGR is projected at 7.2% over 2026–2034, with China alone expected to add USD 1.2 billion by 2034. Technological enhancements in talc-free powders have increased consumer acceptance by 22%. Growth is further reinforced by expanding distribution networks in South East Asia, where demand volume is growing at 8.5% annually.

Asia Pacific Baby Powder Market Restraints

Health Concerns and Regulatory Restrictions on Talc

Talc-related health concerns and stringent regulations in Japan, Australia, and South Korea are restricting market expansion. Approximately 30% of talc-based products are facing labeling restrictions, while production costs for compliant powders increased by 12%. Market penetration for talc variants in sensitive regions dropped to 18%, whereas cornstarch-based alternatives rose to 35%. Overall regional share for traditional formulations is expected to decline from 45% in 2025 to 38% by 2034. These challenges directly impact Asia Pacific Baby Powder market size and consumer confidence, necessitating reformulation and innovation.

Asia Pacific Baby Powder Market Opportunities

Rising Adoption of Eco-friendly and Organic Variants

The shift toward eco-friendly and organic powders presents growth opportunities. In 2026, production volume of organic powders reached 185,000 metric tons, accounting for 18% of the regional market share. Urban adoption rates exceeded 70%, with India and China leading at 28% and 43% contributions, respectively. Emerging online retail platforms facilitate 25% of sales volume, while sector-specific demand for natural products is growing at 9% CAGR. Strategic investments in new product lines and technology upgrades reinforce Asia Pacific Baby Powder market insights and highlight areas for potential revenue expansion.

Asia Pacific Baby Powder Market Challenge

Volatile Raw Material Prices and Supply Chain Disruption

Price volatility in talc, cornstarch, and organic ingredients, combined with supply chain disruptions, poses challenges. Talc prices increased by 15% YoY, while cornstarch costs rose 10%. Approximately 40% of raw material imports come from Southeast Asia, creating dependency risks. Production delays affected 22% of facilities in 2025. Consumer pricing sensitivity is high, with elasticity estimated at 1.2, impacting volume sales. Market growth is hindered in regions like Taiwan and Singapore, where regulatory audits affect 18% of production lines. These challenges underscore the need for robust procurement strategies and risk mitigation to sustain Asia Pacific Baby Powder market growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 3.19 Billion |

| Market Size in 2026 | USD 3.42 Billion |

| Market Size in 2034 | USD 6.14 Billion |

| CAGR | 7.2% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Baby Powder Market Segmentation

The Asia Pacific Baby Powder market is segmented by type and application. Talc-based powders dominate with 48% share, followed by cornstarch-based at 32% and organic powders at 20%. Infant care applications account for 60% of the market, adult care 25%, and cosmetic care 15%. Segmentation analysis helps identify high-growth areas and informs investment strategies.

By Type

Talc-based baby powders held a 48% market share in 2025, with production volume of 460,000 metric tons. Average particle size ranges 10–12 μm, providing optimal moisture absorption and smooth skin application. Talc-based powders are most popular in China and South Korea, with penetration rates of 70% in urban areas. Technical advancements, including anti-caking agents, increased shelf life by 18%, reinforcing Baby Powder Market insights.

Cornstarch-based powders constitute 32% of the market with 310,000 metric tons produced in 2025. Average particle size is 12–15 μm, ensuring high absorption rates and minimal skin irritation. Adoption is higher in Japan (35%) and India (28%). Technical improvements in dispersion and fragrance retention enhance user satisfaction by 15%. Market trends show steady growth in cornstarch-based variants, reinforcing Asia Pacific Baby Powder market growth projections.

Organic powders account for 20% of the market, with production of 180,000 metric tons in 2025. Main ingredients include rice starch, kaolin, and plant-based powders, with improved hypoallergenic properties. Adoption is highest in urban China (43%) and India (28%). Particle size ranges 10–12 μm, with 18% better absorption rates than talc-based powders. The segment is projected to grow at 9% CAGR, reinforcing Baby Powder Market insights.

By Application

Infant care applications dominate 60% of the market, with production volume of 570,000 metric tons in 2025. Penetration in urban centers is 72%, with daily usage of 2–3 times per child. Baby powder serves both hygiene and skin-soothing functions, with technical metrics such as moisture absorption (up to 15%) and low dust emission. Growth in infant care applications supports Asia Pacific Baby Powder market expansion.

Adult care applications account for 25% share, with production volume of 240,000 metric tons. Usage includes underarm, foot, and body care. Adoption rates are 38% in China, 32% in Japan, and 28% in South Korea. Technical performance improvements such as longer-lasting freshness (+12 hours) reinforce consumer preference. The segment is expected to grow at 6.5% CAGR.

Cosmetic care applications contribute 15% of the market, with 140,000 metric tons produced in 2025. Adoption is highest in Japan (38%) and Singapore (26%). Technical specifications include ultra-fine particle size

Asia Pacific Baby Powder Market Segmentations

Type

- Talc-based

- Cornstarch-based

- Organic

Application

- Infant Care

- Adult Care

- Cosmetic Care

Asia Pacific Baby Powder Regional Outlook

China

China contributes 45% of the Asia Pacific market, producing 430,000 metric tons in 2025. Infant care dominates with 65% share, adult care 20%, and cosmetic care 15%. Tier-1 cities account for 60% of sales, while exports contribute 12% to regional revenue. Market growth is projected at 7.5% CAGR, reflecting strong domestic and export demand.

South Korea

South Korea holds 8% market share, producing 76,000 metric tons. Infant care applications dominate at 55%, followed by adult care at 30% and cosmetic care at 15%. Advanced packaging adoption is 48%, while cornstarch-based powder usage is increasing by 12% annually. Market insights show steady growth with urban penetration at 68%.

Japan

Japan contributes 12% to the regional market with 115,000 metric tons produced. Cosmetic care applications lead with 38% share. Organic powders account for 20% of production. Technological adoption, including automated production lines, reached 70% of facilities. Market growth is reinforced by high-income urban populations and rising demand for multifunctional products.

India

India holds 18% regional market share, with 172,000 metric tons produced. Infant care applications dominate at 60%, adult care at 25%, and cosmetic care at 15%. Market penetration in urban areas is 64%, while tier-2 and tier-3 city adoption is 42%. Cornstarch-based powders are gaining 14% annual growth. Market insights show high potential for expansion.

Australia

Australia contributes 3% with 28,500 metric tons. Infant care applications are 55% of usage. Talc-free powders account for 32% of total production. Market growth is expected at 5.5% CAGR due to increasing health awareness and premium product adoption.

Singapore

Singapore holds 2% market share, producing 19,000 metric tons. Cosmetic care applications dominate at 26%, while infant care is 50%. Organic powder adoption reached 20%. Market expansion is supported by retail and e-commerce penetration of 35%.

Taiwan

Taiwan contributes 2% with 19,000 metric tons. Infant care applications account for 60%, adult care 25%, cosmetic care 15%. Technological adoption is 40%, and market penetration is 55%. Growth is projected at 5% CAGR due to rising awareness and niche product adoption.

South East Asia

South East Asia collectively holds 10% regional share, producing 95,000 metric tons. Infant care 58%, adult care 27%, cosmetic care 15%. Organic powder adoption is increasing at 9% CAGR. Market growth is supported by urban expansion, e-commerce channels, and rising consumer spending.

Top players in Asia Pacific Baby Powder Market

- Johnson & Johnson

- Procter & Gamble

- Unilever

- Kao Corporation

- Reckitt Benckiser

- Himalaya

- Dabur

- Beiersdorf

- Abbott

- Morinaga

- Nestlé

- Pigeon

- Mothercare

- Baby Dove

- Chicco

Key Players Analysis

Johnson & Johnson

-

Holds 14% market share in Asia Pacific Baby Powder Market.

-

Dominates infant care segment with premium talc-based and organic variants.

-

Market positioning reinforced through strong retail and e-commerce presence across China, Japan, and India.

-

Production volume reached 135,000 metric tons in 2025, representing 12% YoY growth.

-

Strategic initiatives include M&A in organic product lines and collaborations with dermatologists for safety certifications.

Procter & Gamble

-

Holds 11% regional share.

-

Strong presence in cornstarch-based and cosmetic care powders.

-

Production volume 110,000 metric tons in 2025, CAGR 6.8%.

-

Positioned as a premium brand with multi-functional product offerings.

-

Investments include automated production technologies and expansion in South East Asia markets.

Investment Analysis

Investment allocation in Asia Pacific Baby Powder Market is distributed with 45% in infant care, 30% in adult care, and 25% in cosmetic care. Regional allocation includes 40% in China, 15% in Japan, 12% in India, 8% in South Korea, and 25% in rest of Asia Pacific. M&A agreements in 2025–2026 increased market consolidation, with 6 partnerships focusing on organic and talc-free variants. Sector-specific investments include USD 250 million in technological upgrades for automation and product safety, and USD 180 million for packaging innovation. The overall investment trend indicates a CAGR of 7% in capital allocation for emerging product lines, reinforcing Asia Pacific Baby Powder Market insights.

New Product Developments

In 2025, 32% of new products launched were organic variants, reflecting 18% performance improvements over previous formulations. Product innovations include enhanced absorption, hypoallergenic properties, and improved fragrance retention. Talc-free formulations accounted for 20% of new launches, increasing consumer safety confidence. Overall innovation activity is projected to grow 9% annually, reinforcing Asia Pacific Baby Powder Market insights and creating opportunities for premiumization and differentiation.

Recent Developments in Asia Pacific Baby Powder Market

- 2026: Johnson & Johnson increased organic powder production by 25% to 135,000 metric tons to meet growing urban demand in China and India.

- 2025: Procter & Gamble introduced cornstarch-based multifunctional powders, raising production by 18% and achieving 11% market share in South East Asia.

- 2025: Kao Corporation implemented automated filling lines in Japan, improving production efficiency by 20% and adoption rates in cosmetic care applications by 15%.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Consumer Behavior and Premium Product Segments

Mandy Davis is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.