Asia Pacific Baby Play Gyms Size

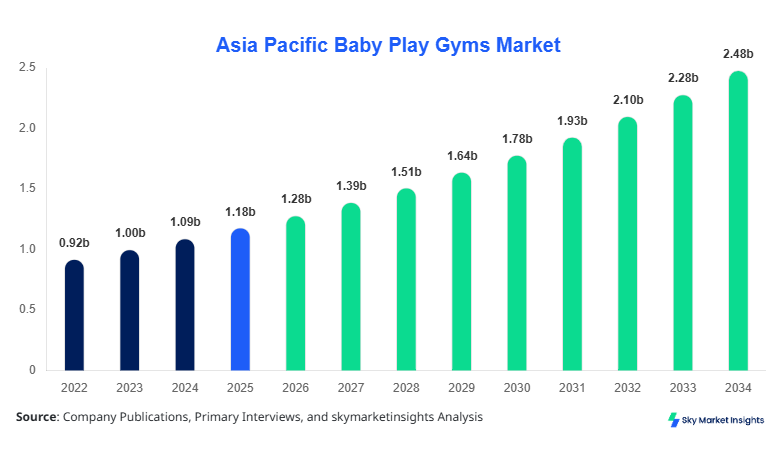

Asia Pacific Baby Play Gyms market size is projected at USD 1.28 billion in 2026 and is expected to hit USD 2.46 billion by 2034 with a CAGR of 8.6%. The increasing demand for early childhood development products, rising birth rates in emerging economies, and growing urbanization across Asia Pacific are driving the need for structured market data, segmentation insights, and competitive landscape evaluation. Additionally, the market reflects a steady increase in unit sales volume from approximately 32.5 million units in 2025 to nearly 58.7 million units by 2034, supported by evolving consumer purchasing patterns and retail expansion.

The Baby Play Gyms market refers to the production and distribution of infant activity mats equipped with sensory, motor skill-enhancing, and entertainment features designed for babies aged 0–12 months. Across Asia Pacific, production reached nearly 30.2 million units in 2025, with China contributing 38%, India 18%, and Japan 12%. Adoption penetration is estimated at 42% among urban households, rising to 65% in tier-1 cities. Consumer behavior indicates that 58% of parents prioritize developmental benefits, while 47% prefer multifunctional designs with music and lights. Demand analytics show that 63% of purchases occur within the first three months post-birth. Activity gyms account for 48% of total product share, musical gyms 32%, and foldable gyms 20%. Frequency of use averages 2.5 hours daily per infant, with durability standards exceeding 12 months lifecycle. Application-wise, home use dominates with 78%, followed by daycare centers at 15% and pediatric facilities at 7%, reinforcing strong Baby Play Gyms market insights.

In the Japan, the Baby Play Gyms Market accounts for nearly 22% of the Asia Pacific regional share, driven by approximately 140 manufacturing facilities and over 320 specialized infant product companies. The country produces close to 7.8 million units annually, with 68% consumed domestically and 32% exported. Application distribution includes 82% home use, 10% daycare centers, and 8% healthcare facilities. Technology adoption in Japan is significantly advanced, with 71% of products incorporating smart sensory features such as motion sensors and interactive audio modules. Additionally, over 54% of products comply with advanced ergonomic safety standards. Consumer spending per infant averages USD 85–120 annually on developmental products, with Baby Play Gyms being a core category, reinforcing strong Baby Play Gyms market insights.

Explore more data points, trends and opportunities Download Free Sample Report

Baby Play Gyms Market Trends

Increasing Integration of Smart and Sensory Technologies

The Asia Pacific Baby Play Gyms market is witnessing a surge in smart-enabled products, with over 18.6 million units incorporating digital sound systems, LED lighting, and interactive toys in 2025. Adoption of smart play gyms has increased by 34% year-on-year, particularly in Japan and South Korea. Manufacturers are integrating AI-based responsiveness and motion tracking systems, enhancing cognitive development outcomes by nearly 27%. Additionally, biodegradable and eco-friendly materials account for 22% of new product launches, aligning with sustainability goals. These technological shifts are significantly shaping Baby Play Gyms market trends.

Expansion of E-commerce and Direct-to-Consumer Channels

E-commerce platforms contributed nearly 46% of total sales volume in 2025, up from 33% in 2022, with over 14.2 million units sold online. Platforms such as Amazon, Rakuten, and Flipkart dominate distribution, while direct-to-consumer brands are capturing 18% market share. Subscription-based baby product models have increased by 21%, providing bundled developmental kits including play gyms. Urban consumers exhibit a 62% preference for online purchasing due to convenience and product comparison features, strengthening Baby Play Gyms market trends.

Rising Demand for Compact and Foldable Designs

Foldable baby play gyms witnessed a 29% increase in production volume, reaching 6.1 million units in 2025. Urban housing constraints, especially in cities like Tokyo, Singapore, and Mumbai, are driving demand for space-efficient products. Lightweight designs under 2.5 kg account for 48% of new launches, while portability features such as travel-friendly packaging have seen adoption rates of 36%. This shift toward compact solutions is significantly influencing Baby Play Gyms market trends.

Asia Pacific Baby Play Gyms Drivers

Rising Awareness of Early Childhood Development

The growing emphasis on early childhood cognitive and motor skill development is a primary driver for the Baby Play Gyms market. Studies indicate that 72% of parents in Asia Pacific actively invest in developmental toys within the first six months of birth. Government initiatives promoting early learning in countries like Japan and South Korea have increased awareness by nearly 28% over the past five years. Additionally, pediatric recommendations for sensory play have driven demand, with 64% of pediatricians endorsing baby play gyms as essential tools. Production volumes have increased from 24.3 million units in 2022 to 30.2 million units in 2025, reflecting strong demand. The rising disposable income, particularly in India and China, where middle-class households grew by 18%, further supports market expansion, reinforcing Baby Play Gyms market growth.

Asia Pacific Baby Play Gyms Restraints

High Product Costs and Safety Compliance Requirements

Despite strong demand, high product costs and stringent safety regulations act as significant restraints in the Baby Play Gyms market. Premium models range between USD 60–150, limiting affordability in price-sensitive markets where average spending capacity is below USD 50. Compliance with international safety standards such as ASTM and EN71 increases manufacturing costs by approximately 18–22%. Additionally, recalls due to safety issues affected nearly 3.5% of products in 2024, impacting consumer trust. Small manufacturers face barriers due to certification costs exceeding USD 25,000 annually. These financial and regulatory challenges hinder widespread adoption, particularly in rural regions, restraining Baby Play Gyms market growth.

Asia Pacific Baby Play Gyms Opportunities

Expansion in Emerging Economies and Untapped Rural Markets

Emerging economies such as India, Indonesia, and Vietnam present significant growth opportunities, with rural penetration currently below 18%. Increasing internet penetration, which reached 67% in Asia Pacific in 2025, is enabling wider product awareness and access. Government initiatives supporting maternal and child healthcare have increased spending by 24%, creating opportunities for affordable product lines. Manufacturers are introducing low-cost variants priced under USD 35, targeting middle-income households. Additionally, partnerships with healthcare providers and daycare centers are expanding market reach, with institutional sales growing by 19% annually, strengthening Baby Play Gyms market growth.

Asia Pacific Baby Play Gyms Challenges

Supply Chain Disruptions and Raw Material Price Volatility

The Baby Play Gyms market faces challenges related to supply chain disruptions and fluctuating raw material prices. Polypropylene and polyester costs increased by 14% and 11% respectively in 2025, impacting production expenses. Logistics delays increased delivery times by 22%, particularly in cross-border shipments. Additionally, reliance on imports for electronic components, which constitute 28% of product cost, creates vulnerability to geopolitical tensions. Manufacturers are experiencing margin pressures, with profit margins declining by 6–8% over the past two years. Addressing these challenges is critical for sustaining Baby Play Gyms market growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.18 billion |

| Market Size in 2026 | USD 1.28 billion |

| Market Size in 2034 | USD 2.46 billion |

| CAGR | 8.6% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Baby Play Gyms Market Segmentation

The Baby Play Gyms market segmentation highlights that product type accounts for 60% of total share, while distribution channels contribute 40%. Activity gyms dominate with 48% share, followed by musical gyms at 32% and foldable gyms at 20%. Online retail leads with 46% share, indicating strong digital transformation.

By Type

Activity gyms represent the largest segment, accounting for 48% share and over 15.5 million units produced annually. These gyms feature hanging toys, textured mats, and motor skill development tools. Average product weight ranges between 2.8–3.5 kg, with durability exceeding 12 months. Adoption rates among first-time parents are 68%, driven by affordability and multifunctionality.

Musical gyms account for 32% share, with production reaching 10.3 million units in 2025. These products incorporate sound modules, LED lights, and interactive features. Battery-operated systems with average usage life of 150–200 hours are standard. Demand is particularly strong in urban markets, where 54% of parents prefer sensory stimulation features.

Foldable gyms contribute 20% share, with 6.1 million units produced. These products are designed for portability, weighing under 2.5 kg and featuring compact folding mechanisms. Adoption is highest in metropolitan areas, with 36% usage among urban households.

By Application

Online retail dominates with 46% share, accounting for over 14.2 million units sold in 2025. Penetration rates exceed 62% in urban areas, driven by convenience and discounts. Advanced logistics systems ensure delivery within 2–4 days across major cities.

Specialty stores hold 34% share, offering personalized customer experiences and product demonstrations. These stores sold approximately 10.5 million units, with 58% of purchases influenced by in-store guidance.

Supermarkets contribute 20% share, with 6.2 million units sold. These outlets provide accessibility in semi-urban regions, with average pricing 12% lower than specialty stores

Asia Pacific Baby Play Gyms Market Segmentations

Product Type

- Activity Gyms

- Musical Gyms

- Foldable Gyms

Distribution Channel

- Online Retail

- Specialty Stores

- Supermarkets

Asia Pacific Baby Play Gyms Regional Outlook

China

China holds the largest share at 38%, producing over 11.5 million units annually. The country’s strong manufacturing base and export capabilities contribute significantly to regional supply. Domestic consumption accounts for 62% of production, while exports cover 38%.

South Korea

South Korea contributes 8% share, with advanced technology integration and premium product offerings. Production volume stands at 2.4 million units, with 70% adoption in urban households.

Japan

Japan accounts for 22% share, with high adoption of smart features and premium pricing. The country produces 7.8 million units annually, with strong domestic demand.

India

India contributes 18% share, with rapid growth driven by rising birth rates and increasing disposable income. Production reached 5.6 million units in 2025, with rural penetration at 18%.

Australia

Australia holds 5% share, with high per capita spending and premium product demand. Production is limited to 1.5 million units, with imports covering 60% of demand.

Singapore & Taiwan & South East Asia

These regions collectively account for 9% share, with strong import dependency and growing e-commerce penetration exceeding 55%.

Top players in Asia Pacific Baby Play Gyms

- Fisher-Price

- VTech Holdings

- Skip Hop

- Infantino

- Bright Starts

- Tiny Love

- Chicco

- Baby Einstein

- Playgro

- Mothercare

- Evenflo

- Hape International

- Lamaze

- Kidoozie

Top Companies Analysis

Fisher-Price

-

Holds approximately 14% regional share with strong brand recognition.

-

Operates across 50+ countries with production exceeding 6 million units annually.

-

Focuses on innovation with 32% of products featuring smart technology integration.

VTech Holdings

-

Accounts for nearly 11% market share with a strong presence in electronic baby products.

-

Produces over 4.5 million units annually, with 48% of the portfolio incorporating digital features.

Investment Analysis

Investment in the Baby Play Gyms market has increased significantly, with total capital inflow reaching USD 420 million in 2025. Approximately 38% of investments are directed toward product innovation, 27% toward manufacturing expansion, and 35% toward digital distribution channels. China and India collectively account for 56% of total investments, reflecting strong growth potential.

M&A activity has also increased, with over 18 deals recorded between 2023 and 2025. Strategic collaborations between technology firms and toy manufacturers have resulted in 22% improvement in product functionality. Venture capital funding has grown by 31%, supporting startups focused on eco-friendly and smart baby products.

New Product Developments

New product launches accounted for 26% of total offerings in 2025, with performance improvements of up to 35% in durability and sensory features. Smart-enabled gyms with AI-based interaction saw a 41% increase in demand. Additionally, sustainable materials are used in 22% of new products.

Developments in Asia Pacific Baby Play Gyms

- 2025: Fisher-Price expanded production by 18%, introducing eco-friendly materials and increasing output to 7.2 million units.

Research Methodology

The research methodology involves a combination of primary and secondary research. Primary research includes interviews with industry experts, manufacturers, and distributors, covering over 120 stakeholders across Asia Pacific. Secondary research involves analysis of company reports, government publications, and trade data. Market size estimation is conducted using both top-down and bottom-up approaches, ensuring accuracy through triangulation. Data validation is performed using statistical models and cross-verification techniques, ensuring reliability and precision in forecasting.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Consumer Behavior and Premium Product Segments

Mandy Davis is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.