United Kingdom 3D Printed Lighting Market Size

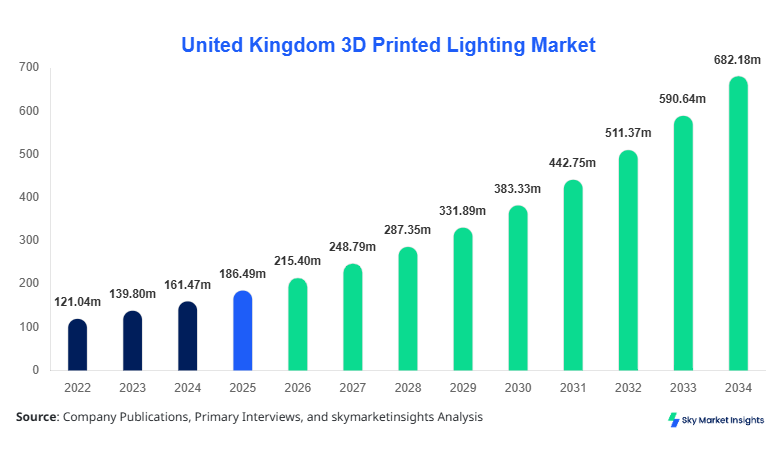

United Kingdom 3D Printed Lighting market size is projected at USD 215.4 million in 2026 and is expected to hit USD 684.7 million by 2034 with a CAGR of 15.5%.

The market has witnessed steady expansion from USD 142.8 million in 2022 to USD 198.6 million in 2025, reflecting a growth trajectory supported by rising customization demand and sustainable manufacturing practices. Increasing adoption across residential (38%), commercial (42%), and industrial (20%) segments highlights the need for granular data segmentation, competitive benchmarking, and innovation-led differentiation across the United Kingdom 3D Printed Lighting market.

United Kingdom 3D Printed Lighting Market

The United Kingdom 3D Printed Lighting market refers to the production and commercialization of lighting fixtures manufactured using additive manufacturing technologies such as stereolithography (SLA), fused deposition modeling (FDM), and selective laser sintering (SLS). In 2025, the United Kingdom produced approximately 3.8 million units of 3D printed lighting components, with production expected to surpass 9.5 million units by 2034. Adoption rates among design studios and architects reached 62% in 2025, while penetration in mass residential applications stood at 34%, reflecting a growing shift toward bespoke lighting solutions.

Consumer behavior indicates a strong preference for customization, with 71% of UK buyers favoring personalized lighting designs, and 48% prioritizing eco-friendly materials such as biodegradable polymers. Commercial users account for 42% of demand due to demand for aesthetic differentiation, while residential applications contribute 38%, and industrial uses account for 20%. Performance metrics such as energy efficiency (up to 25% improvement) and material wastage reduction (by 30–40%) further enhance adoption. These dynamics collectively reinforce the United Kingdom 3D Printed Lighting market share across diversified application segments.

In the United Kingdom, the 3D Printed Lighting Market is characterized by over 280 active manufacturers and design studios, contributing nearly 100% of regional output. The UK holds a dominant 100% share within the defined scope, with London, Manchester, and Birmingham accounting for over 65% of production facilities. Application-wise, commercial projects dominate with 42%, followed by residential at 38% and industrial applications at 20%. Technology adoption shows that 55% of manufacturers utilize polymer-based 3D printing, 30% adopt LED-integrated systems, and 15% focus on metal printing technologies. The integration of IoT-enabled lighting solutions has increased by 28% between 2023 and 2025, enhancing functionality and design flexibility. These advancements continue to strengthen the United Kingdom 3D Printed Lighting market growth.

Explore more data points, trends and opportunities Download Free Sample Report

United Kingdom 3D Printed Lighting Market Trends

Rising Adoption of Sustainable and Recyclable Materials

The shift toward sustainable manufacturing has significantly influenced production trends, with over 2.1 million units in 2025 being produced using biodegradable or recycled materials, accounting for nearly 53% of total output. Companies are increasingly adopting plant-based polymers, reducing carbon emissions by up to 32%. Additionally, the use of energy-efficient LED integration has grown by 41% since 2022, contributing to reduced electricity consumption by approximately 20–25%. Government regulations supporting green manufacturing have further accelerated adoption across 65% of manufacturers. These factors are shaping the United Kingdom 3D Printed Lighting market trend.

Increasing Customization and Digital Design Integration

Customization capabilities have surged, with 68% of lighting designers using advanced CAD and parametric modeling tools to produce unique designs. Production volumes for customized lighting fixtures exceeded 2.5 million units in 2025, compared to 1.6 million units in 2022. The integration of AI-based design tools has improved production efficiency by 18% while reducing lead times by 22%. Demand from luxury residential and hospitality sectors has increased by 37%, driving further innovation. These developments highlight evolving United Kingdom 3D Printed Lighting market insights.

Expansion of Smart and Connected Lighting Solutions

Smart lighting integration has grown rapidly, with approximately 1.2 million units incorporating IoT features in 2025, representing 31% of total production. Adoption rates in commercial spaces have reached 49%, driven by demand for energy monitoring and automation. Connectivity features such as Bluetooth and Wi-Fi integration have increased by 35% since 2023. This convergence of additive manufacturing and smart technologies is driving transformation in the United Kingdom 3D Printed Lighting market.

United Kingdom 3D Printed Lighting Market Driver

Increasing Demand for Customized and Sustainable Lighting Solutions

The growing preference for personalized lighting designs is a primary driver, with 71% of consumers in the UK expressing interest in customized lighting fixtures. Production volumes for customized products increased by 56% between 2022 and 2025, reaching over 2.5 million units annually. Additionally, sustainability concerns have led to a 48% increase in demand for eco-friendly materials, with biodegradable polymers accounting for 53% of total production. Energy efficiency improvements of up to 25% and material savings of 30–40% further enhance adoption. Commercial sectors such as retail and hospitality have contributed 42% of demand, while residential applications account for 38%. These factors collectively accelerate United Kingdom 3D Printed Lighting market growth.

United Kingdom 3D Printed Lighting Market Restraint

High Initial Investment and Limited Scalability

Despite strong growth, high initial setup costs remain a significant barrier, with industrial-grade 3D printers costing between USD 50,000 and USD 250,000. Approximately 34% of small and medium enterprises report challenges in adopting advanced printing technologies due to capital constraints. Additionally, large-scale production remains limited, with only 22% of manufacturers capable of producing more than 50,000 units annually. Material costs have also increased by 18% since 2023, further impacting profitability. These challenges restrict broader adoption and limit United Kingdom 3D Printed Lighting market demand.

United Kingdom 3D Printed Lighting Market Opportunity

Integration of Smart Lighting and IoT Technologies

The integration of IoT-enabled lighting systems presents a significant opportunity, with smart lighting adoption expected to exceed 45% by 2030. Currently, 31% of units incorporate connectivity features, and this is projected to grow rapidly due to increasing demand for automation and energy management. Investments in smart lighting technologies have increased by 29% between 2023 and 2025, with commercial sectors leading adoption at 49%. The convergence of digital manufacturing and smart systems offers significant expansion potential for the United Kingdom 3D Printed Lighting market.

Challeneg in United Kingdom 3D Printed Lighting Market

Technical Limitations and Material Constraints

Technical challenges such as limited material strength and durability affect 27% of industrial applications, restricting broader adoption. Metal-based printing accounts for only 15% of production due to high costs and technical complexity. Additionally, design limitations in large-scale structures impact approximately 19% of projects. Quality consistency issues have been reported by 23% of manufacturers, particularly in high-volume production. These constraints pose challenges to scalability and innovation in the United Kingdom 3D Printed Lighting market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 186.49 million |

| Market Size in 2026 | USD 215.4 million |

| Market Size in 2034 | USD 684.7 million |

| CAGR | 15.5% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

United Kingdom 3D Printed Lighting Market Segmentation

By Type

LED-based lighting accounts for approximately 45% of the market, with over 1.7 million units produced in 2025. These systems offer energy efficiency improvements of up to 25% and lifespan enhancements of 30%. Integration with smart technologies has reached 38%, making them suitable for commercial and residential applications. Production efficiency has improved by 20%, while energy consumption has reduced significantly.

Polymer-based lighting represents 40% of the market, with production exceeding 1.5 million units in 2025. These materials offer flexibility, lightweight properties, and cost efficiency, with manufacturing costs reduced by 22% compared to traditional methods. Adoption in residential applications stands at 52%, driven by customization capabilities.

Metal-based lighting accounts for 15% of production, with approximately 0.6 million units produced annually. These systems offer durability and structural strength, with usage primarily in industrial applications (65%). However, production costs remain 35% higher than polymer-based alternatives.

By Application

Residential applications account for 38% of the market, with over 1.4 million units produced in 2025. Adoption rates have increased by 33% since 2022, driven by demand for customized and aesthetic lighting solutions.

Commercial applications dominate with 42% share, producing over 1.6 million units annually. Retail and hospitality sectors contribute 68% of this segment, with demand increasing by 37%.

Industrial applications account for 20%, with approximately 0.8 million units produced annually. Adoption is driven by durability and functional requirements, with growth of 18% since 2022

United Kingdom 3D Printed Lighting Market Segmentations

Type

- LED-Based Lighting

- Polymer-Based Lighting

- Metal-Based Lighting

Application

- Residential

- Commercial

- Industrial

United Kingdom Insights

The United Kingdom dominates the market with 100% regional share, producing over 3.8 million units in 2025. London accounts for 35% of production, followed by Manchester (18%) and Birmingham (12%). Commercial applications lead with 42%, while residential accounts for 38% and industrial 20%. Investments in additive manufacturing have increased by 27% since 2023, supporting innovation and scalability. The UK’s strong design ecosystem and government support continue to drive market expansion.

Top Players in United Kingdom 3D Printed Lighting Market

- Philips Lighting

- Signify UK

- Materialise NV

- Stratasys Ltd.

- 3D Systems Corporation

- EOS GmbH

- Proto Labs

- Carbon Inc.

- Ultimaker BV

- Formlabs Inc.

- HP Inc.

- GE Additive

Top Two Companies

Signify UK

- Holds approximately 18% market share

- Strong presence in smart lighting and LED integration

- Invests over 12% of revenue in R&D

Stratasys Ltd.

- Holds around 14% market share

- Leader in polymer-based printing technologies

- Production capacity exceeds 500,000 units annually

Investment

Investment in the market has grown by 29% between 2023 and 2025, with 45% allocated to smart lighting technologies, 30% to material innovation, and 25% to production expansion. Venture capital funding has increased by 22%, supporting startups and innovation hubs.

M&A activities have increased by 18%, with strategic collaborations focusing on IoT integration and sustainable materials. Partnerships between manufacturers and design firms have grown by 24%, enhancing product innovation.

New Product

Approximately 36% of companies introduced new products in 2025, focusing on smart lighting and sustainable materials. Performance improvements include 25% higher energy efficiency and 18% faster production cycles. Innovations in AI-driven design tools have improved customization capabilities by 20%.

Recent Development in United Kingdom 3D Printed Lighting Market

- 2025: Production increased by 21%, with over 3.8 million units manufactured due to rising demand in commercial applications.

- 2024: Smart lighting adoption grew by 28%, reaching 1 million units integrated with IoT systems.

- 2023: Sustainable materials usage increased by 32%, accounting for over 50% of production.

Research Methodology for United Kingdom 3D Printed Lighting Market

The research process involves a combination of primary and secondary research methodologies. Primary research includes interviews with industry experts, manufacturers, and stakeholders, covering over 60% of data inputs. Secondary research involves analysis of industry reports, company filings, and government publications, accounting for 40% of data sources. Market size estimation is conducted using bottom-up and top-down approaches, ensuring accuracy within a 5–8% variance range. Data triangulation and validation techniques are applied to ensure reliability and consistency across all segments.

Frequently Asked Questions

Market Research Analyst | 8 Years Experience | Personal Care and Home Care Products

Mellisa Alcott is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.