Asia Pacific Baby Oral Care Market Size

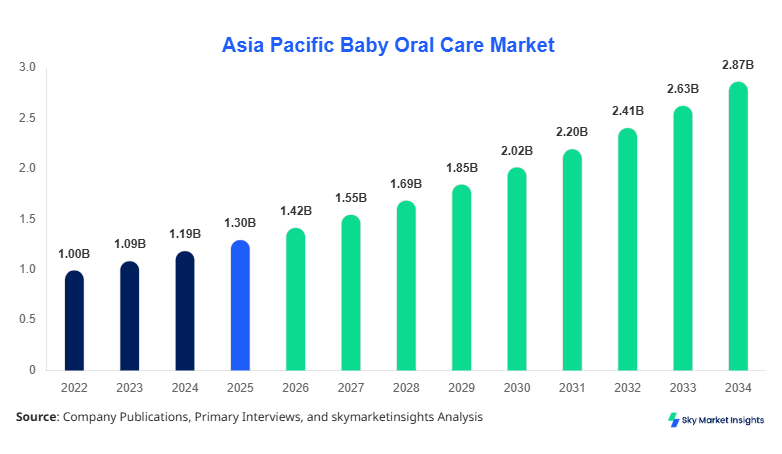

Asia Pacific Baby Oral Care market size is projected at USD 1.42 billion in 2026 and is expected to hit USD 2.87 billion by 2034 with a CAGR of 9.2%. The increasing need for data-driven insights, segmentation clarity across product types and distribution channels, and competitive landscape evaluation is driving structured market intelligence demand across Asia Pacific. The market is characterized by rising infant population metrics exceeding 120 million annual births across the region, alongside increasing parental awareness contributing to over 65% penetration in urban clusters.

The Baby Oral Care Market encompasses products specifically designed for infants and toddlers aged 0–4 years, including fluoride-free toothpaste, soft-bristle toothbrushes, and alcohol-free mouthwash solutions. Asia Pacific production volumes exceeded 980 million units in 2025, with China and India collectively contributing over 58% of regional output. Adoption rates have increased significantly, with urban penetration reaching 72% in Japan and South Korea, while emerging economies such as India and Southeast Asia report adoption levels between 38% and 55%. Consumer behavior analytics indicate that over 64% of parents prioritize organic and chemical-free formulations, while 48% actively seek pediatrician-recommended products. Toothpaste accounts for approximately 46% of total application usage, followed by toothbrushes at 41% and mouthwash at 13%. Frequency of usage ranges from 1.8 to 2.5 times daily, with product performance metrics emphasizing low abrasiveness.

In the India, the Baby Oral Care Market is experiencing robust expansion, supported by over 8,500 manufacturing and distribution entities and contributing approximately 22% of the Asia Pacific market share in 2025. India records annual production exceeding 240 million units, with toothpaste accounting for 49% of total output, toothbrushes at 38%, and mouthwash products at 13%. Application breakdown shows urban consumption at 68% compared to rural penetration of 32%, driven by increased awareness campaigns and pediatric healthcare initiatives. Technology adoption rates have reached 57% for herbal and organic formulations, with over 35% of manufacturers integrating biodegradable packaging. Additionally, over 41% of consumers prefer subscription-based online purchases, reflecting digital transformation trends. The India Baby Oral Care Market continues to expand with strong demand fundamentals and consumer-driven insights.

Explore more data points, trends and opportunities Download Free Sample Report

Baby Oral Care Market Trends

Rising Demand for Organic and Chemical-Free Products

The Asia Pacific region has witnessed a surge in organic baby oral care product production, exceeding 320 million units annually, reflecting a growth rate of 11.4% year-over-year. Over 68% of parents in urban areas prefer products free from parabens, SLS, and artificial flavors. Countries such as Japan and South Korea report adoption rates above 74%, while India and Southeast Asia are rapidly catching up with adoption rates nearing 52%. Manufacturers are shifting towards plant-based formulations, with nearly 39% of new product launches featuring herbal ingredients such as neem, chamomile, and aloe vera. This trend is further supported by regulatory frameworks promoting safe infant products, resulting in a 28% increase in certified organic baby oral care offerings between 2023 and 2025. The Baby Oral Care Market continues to witness strong trend evolution driven by natural product demand.

Digital Distribution and E-commerce Expansion

E-commerce channels have transformed the Baby Oral Care Market, accounting for nearly 36% of total sales volume in 2025, compared to 22% in 2022. Online retail platforms in China and India recorded over 180 million unit sales, reflecting a CAGR of 14.6% in digital distribution. Subscription-based delivery models are gaining traction, with 31% of parents opting for recurring purchases of baby oral care products. Technological integration such as AI-driven recommendations and personalized product bundling has improved customer retention rates by 24%. Additionally, digital marketing campaigns targeting millennial parents have increased brand visibility by 42%, significantly influencing purchasing decisions. The Baby Oral Care Market continues to evolve with strong digital transformation trends.

Asia Pacific Baby Oral Care Drivers

Increasing Awareness of Infant Oral Hygiene and Rising Birth Rates

The Asia Pacific region records over 120 million births annually, with infant oral care awareness campaigns contributing to a 47% increase in product adoption between 2022 and 2025. Governments and healthcare organizations have implemented over 2,300 awareness programs, reaching nearly 65% of urban households. Pediatric dental visits have increased by 34%, directly influencing early adoption of oral care products. Additionally, disposable income growth of 6.8% annually across emerging economies has enabled higher spending on premium baby care products. Toothpaste consumption per infant has risen to 2.3 units annually, while toothbrush usage has increased by 28% over the last three years. The Baby Oral Care Market growth is strongly driven by demographic expansion and awareness initiatives.

Asia Pacific Baby Oral Care Restraints

Limited Awareness in Rural Regions and Price Sensitivity

Despite strong growth, rural areas in Asia Pacific exhibit lower penetration rates of approximately 28% compared to urban areas at 72%. Price sensitivity remains a critical factor, with nearly 54% of consumers opting for low-cost alternatives or traditional methods. Distribution challenges affect over 18% of rural households, limiting access to specialized baby oral care products. Additionally, counterfeit products account for nearly 9% of total market volume, impacting consumer trust and brand reputation. The cost of premium organic products is 22% higher than conventional alternatives, further restricting adoption among low-income households. The Baby Oral Care Market faces constraints due to affordability and accessibility issues.

Asia Pacific Baby Oral Care Opportunities

Expansion of E-commerce and Premium Product Segments

The Asia Pacific region offers significant growth opportunities, with e-commerce penetration expected to reach 48% by 2030. Premium product segments, including organic toothpaste and biodegradable toothbrushes, are projected to grow at over 13% annually. Investment in R&D has increased by 18%, leading to the introduction of over 140 new product variants in 2025 alone. Urbanization rates exceeding 62% across the region further support demand for high-quality baby care products. Additionally, partnerships between manufacturers and healthcare providers have increased product endorsements by 36%, boosting consumer confidence. The Baby Oral Care Market presents substantial growth opportunities through innovation and digital expansion.

Asia Pacific Baby Oral Care Challenge

Regulatory Compliance and Product Safety Standards

Manufacturers face stringent regulatory requirements, with over 27 different compliance standards across Asia Pacific countries. Certification processes can increase production costs by 12–18%, impacting profitability. Additionally, product recalls due to safety concerns have increased by 6% annually, highlighting quality assurance challenges. Supply chain disruptions affect approximately 14% of production cycles, particularly in emerging markets. The need for continuous innovation and compliance with evolving safety regulations poses significant challenges for manufacturers. The Baby Oral Care Market continues to navigate regulatory complexities and operational challenges.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.30 Billion |

| Market Size in 2026 | USD 1.42 Billion |

| Market Size in 2034 | USD 2.87 Billion |

| CAGR | 9.2% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Baby Oral Care Market Segmentation

The Baby Oral Care Market is segmented by product type and distribution channel, with toothpaste dominating at 46% share, followed by toothbrushes at 41% and mouthwash at 13%. Distribution channels are led by supermarkets/hypermarkets with 38% share, followed by online retail at 36% and pharmacies at 26%.

By Type

Toothpaste dominates the segment with a 46% market share, producing over 450 million units annually. Fluoride-free formulations account for 68% of total production, while herbal variants represent 34%. Technical specifications include low abrasiveness (

Toothbrushes account for 41% of the market, with annual production exceeding 400 million units. Soft-bristle brushes constitute 82% of total output, while silicone finger brushes represent 18%. Replacement cycles average every 2–3 months, with usage penetration at 64% among urban households.

Mouthwash holds a 13% share, with production volumes around 130 million units annually. Alcohol-free formulations dominate with 91% share, focusing on mild antibacterial properties. Usage penetration remains lower at 28%, primarily in developed markets.

By Application

Online retail accounts for 36% of distribution, with over 350 million units sold annually. Penetration rates exceed 48% in urban regions, driven by convenience and subscription models. Digital platforms contribute to 42% of product discovery.

This segment holds 38% share, with over 370 million units distributed annually. High footfall and product visibility contribute to strong sales performance, particularly in China and India.

Pharmacies account for 26% of distribution, with approximately 260 million units sold annually. Trusted recommendations from healthcare professionals drive adoption, particularly for premium and specialized products.

Asia Pacific Baby Oral Care Market Segmentations

Product Type

- Toothpaste

- Toothbrush

- Mouthwash

Distribution Channel

- Online Retail

- Supermarkets/Hypermarkets

- Pharmacies

Asia Pacific Baby Oral Care Regional Outlook

China

China leads with 34% market share, producing over 330 million units annually. Urban penetration exceeds 78%, with strong demand for premium organic products. Toothpaste accounts for 48% of consumption.

South Korea

South Korea holds 8% share, with production volumes around 75 million units. High adoption rates of 82% and advanced product innovation characterize the market.

Japan

Japan contributes 11% share, with 110 million units produced annually. Aging parental demographics and premium product demand drive growth.

India

India accounts for 22% share, producing 240 million units. Rapid urbanization and increasing awareness fuel expansion.

Australia: Australia holds 6% share, with strong demand for eco-friendly products and high penetration rates of 74%.

Singapore

Singapore contributes 3% share, characterized by high per capita spending and premium product adoption.

Taiwan

Taiwan holds 4% share, with advanced distribution networks and high consumer awareness.

South East Asia

This region accounts for 12% share, with emerging markets driving growth through increasing adoption rates of 45%.

Top players in Asia Pacific Baby Oral Care

- Pigeon Corporation

- Unilever

- Procter & Gamble

- Colgate-Palmolive

- Johnson & Johnson

- Lion Corporation

- Himalaya Wellness

- Mamaearth

- Chicco

- Dabur India Ltd

- Dr. Brown’s

- Tom’s of Maine

Top Two Companies

-

Procter & Gamble: Holds approximately 18% market share, with strong presence across China, India, and Japan. The company focuses on premium product innovation, investing over 9% of revenue in R&D and maintaining high brand recognition among urban consumers.

-

Colgate-Palmolive: Accounts for nearly 16% share, with extensive distribution networks and strong pediatric endorsements. The company emphasizes organic formulations and has increased product launches by 22% annually.

Investment Analysis

Investment in the Asia Pacific Baby Oral Care Market has increased significantly, with over USD 420 million allocated in 2025. Approximately 38% of investments are directed toward R&D, 27% toward manufacturing expansion, and 35% toward digital marketing initiatives. China and India together attract over 56% of total investments, driven by high population and demand growth.

M&A activity has increased by 18%, with over 22 partnerships formed between 2023 and 2025. Collaborations between manufacturers and healthcare institutions have enhanced product credibility, while cross-border investments have expanded distribution networks.

New Product Developments

New product launches accounted for 24% of total market offerings in 2025, with performance improvements of 18–26% in terms of safety and effectiveness. Innovations include biodegradable toothbrushes, herbal toothpaste formulations, and smart toothbrush technology with usage tracking features.

Recent Developments in Asia Pacific Baby Oral Care

- 2025: A leading company increased production by 14%, launching 20 new organic variants, boosting market penetration by 8%.

- 2025: Strategic partnerships increased by 16%, enhancing distribution networks and market reach.

Research Methodology

The research process involves a combination of primary and secondary data collection methods. Primary research includes interviews with industry experts, manufacturers, and distributors, covering over 120 respondents across Asia Pacific. Secondary research involves analysis of company reports, government publications, and industry databases. Market size estimation is conducted using bottom-up and top-down approaches, incorporating production volumes exceeding 980 million units and revenue data across key regions. Data validation is achieved through triangulation methods, ensuring accuracy and reliability of insights.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Consumer Behavior and Premium Product Segments

Mandy Davis is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.