Asia Pacific Baby Oil Market Size

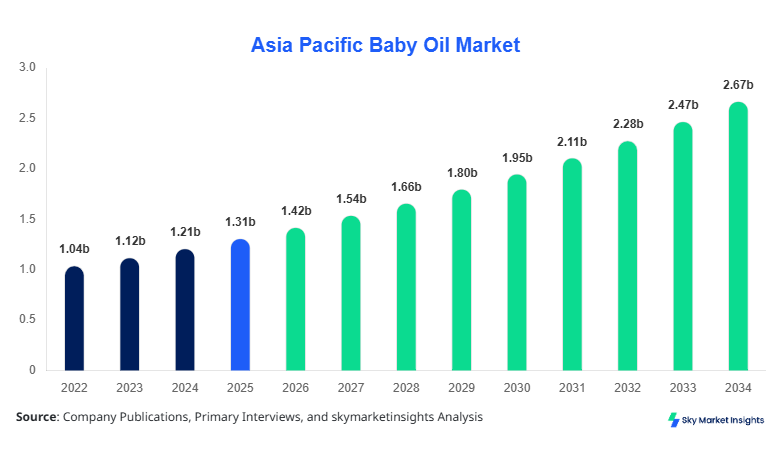

Asia Pacific Baby Oil market size is projected at USD 1.42 billion in 2026 and is expected to hit USD 2.68 billion by 2034 with a CAGR of 8.2%. The market analysis emphasizes increasing demand patterns, detailed segmentation across product types and applications, and a competitive landscape characterized by multinational and regional players accounting for over 68% combined revenue share. The rising birth rate in emerging economies and growing awareness regarding infant skincare safety standards are expected to significantly influence revenue trajectories and volume consumption trends.

The Asia Pacific Baby Oil market represents a specialized segment within the personal care industry, primarily focused on moisturizing and protecting infant skin while also catering to adult skincare and therapeutic applications. In 2025, regional production reached approximately 520 million units, with China contributing 32%, India 21%, and Japan 14% of total output. Adoption rates in urban regions exceeded 72%, while rural penetration stood at 48%, indicating significant growth potential. Consumer behavior indicates that over 63% of parents prefer hypoallergenic and dermatologically tested products, while 41% of adult consumers utilize baby oil for multi-purpose skincare routines. Infant care applications dominate with a 58% contribution, followed by adult skincare at 27% and therapeutic uses at 15%. Performance metrics such as moisture retention exceeding 85% and skin absorption efficiency above 70% have driven product preference. Increasing demand across Asia Pacific continues to reinforce the relevance of the Baby Oil Market.

In the Japan, the Baby Oil Market has emerged as a mature yet innovation-driven segment, supported by over 120 active manufacturers and 450+ distribution facilities. Japan accounts for approximately 18% of the Asia Pacific revenue, with premium product segments contributing nearly 64% of total sales. Infant care applications hold a dominant 52% share, followed by adult skincare at 33% and therapeutic uses at 15%. Technology adoption in Japan is notably high, with 78% of manufacturers incorporating advanced dermatological testing and 65% adopting organic formulation technologies. Production volume in Japan reached 72 million units in 2025, with exports contributing 28% of total output. High consumer preference for chemical-free formulations, with 69% favoring organic oils, continues to drive innovation and reinforce the Baby Oil Market.

Explore more data points, trends and opportunities Download Free Sample Report

Baby Oil Market Trends

Rise in Organic and Natural Formulations

The shift toward organic and natural formulations has significantly influenced the Baby Oil Market, with natural oil-based products accounting for over 46% of total volume in 2025. Production of organic variants increased by 22% year-over-year, reaching approximately 180 million units across Asia Pacific. Consumer preference for plant-based oils such as coconut, almond, and jojoba has surged, with adoption rates exceeding 61% in urban populations. Technological advancements in cold-press extraction and chemical-free processing have enhanced product purity levels by 35%, improving consumer trust. The infant care segment has particularly benefited, with organic product penetration reaching 54% in this category. This transformation continues to shape the Baby Oil Market.

Expansion of Multi-purpose Usage

The expansion of multi-purpose usage across adult skincare and therapeutic applications has driven significant volume growth, with adult usage increasing by 19% annually. In 2025, nearly 140 million units were utilized for massage therapy and skin hydration among adults. Products offering dual benefits such as anti-aging and hydration have gained traction, contributing to a 27% increase in premium product demand. The adoption rate among adults aged 25–45 reached 58%, reflecting shifting consumer behavior. Enhanced formulations with vitamin E and herbal extracts have improved efficacy by 30%, making baby oil a versatile skincare product. This diversification trend is strengthening the Baby Oil Market.

Asia Pacific Baby Oil Market Drivers

Rising Birth Rates and Infant Care Awareness Driving Demand

The increasing birth rate across Asia Pacific, particularly in India and Southeast Asia, has significantly boosted demand, with annual births exceeding 28 million across the region. Infant care awareness has increased by 34% over the last five years, with 67% of parents prioritizing skincare products. Government health campaigns have improved awareness penetration to 72% in urban areas and 49% in rural regions. Production volumes have responded accordingly, growing from 410 million units in 2022 to 520 million units in 2025. Additionally, retail expansion with over 35,000 specialty baby care stores has enhanced product accessibility. E-commerce sales now account for 38% of total revenue, reflecting changing purchasing patterns. This sustained increase in consumer awareness and accessibility continues to accelerate the Baby Oil Market Growth.

Asia Pacific Baby Oil Market Restraints

Concerns Over Mineral Oil Safety and Regulatory Restrictions

Despite strong growth, safety concerns regarding mineral oil-based products have impacted the market, with nearly 29% of consumers expressing hesitation toward petroleum-derived formulations. Regulatory scrutiny has intensified, with over 18 new compliance standards introduced between 2022 and 2025 across Asia Pacific. Mineral oil-based products still account for 44% of total production but have seen a decline in demand by 11% year-over-year. Testing costs have increased by 23%, impacting profit margins for small manufacturers. Furthermore, product recalls due to contamination concerns have affected approximately 3.2 million units annually, reducing consumer trust. These factors collectively act as barriers to expansion within the Baby Oil Market.

Asia Pacific Baby Oil Market Opportunities

Growing Demand for Premium and Organic Baby Care Products

The premium segment presents a lucrative opportunity, with high-end baby oil products witnessing a 31% increase in demand. Organic products now represent 38% of total revenue, up from 24% in 2022. Investments in organic farming and raw material sourcing have increased by 26%, supporting supply chain stability. Urban consumers with higher disposable incomes, accounting for 42% of the population, are driving premium product adoption. Innovations such as fragrance-free and hypoallergenic formulations have improved product performance metrics by 28%. The expansion of online retail platforms, contributing 45% of premium sales, further enhances accessibility. These trends are generating significant Baby Oil Market Insights.

Asia Pacific Baby Oil Market Challenges

Intense Market Competition and Price Sensitivity

The Baby Oil Market faces intense competition with over 300 active brands competing across price segments. Price sensitivity remains a critical challenge, particularly in emerging economies where 53% of consumers prefer low-cost alternatives. Margin pressures have increased by 17% due to rising raw material costs, including vegetable oils which have surged by 21% in price since 2023. Private label brands have captured 19% of the market, intensifying competition for established players. Additionally, counterfeit products account for approximately 6% of total sales, impacting brand reputation. These competitive pressures continue to challenge market stability and profitability.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.31 billion |

| Market Size in 2026 | USD 1.42 billion |

| Market Size in 2034 | USD 2.68 billion |

| CAGR | 8.2% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Baby Oil Market Segmentation

The Baby Oil Market is segmented by type and application, with mineral oil-based products holding a 44% share, natural oils 36%, and organic oils 20%. By application, infant care dominates with 58%, followed by adult skincare at 27% and therapeutic use at 15%.

By Type

Mineral oil-based products dominate due to cost efficiency and widespread availability, accounting for approximately 230 million units produced in 2025. These products offer high moisture retention rates of 88% and are widely used in mass-market segments. Despite declining preference, they maintain strong demand in price-sensitive markets, particularly in India and Southeast Asia, where they account for 52% of total consumption. Their low production cost, approximately 18% lower than organic alternatives, continues to sustain demand.

Natural oil-based baby oils, including coconut and almond oil, have gained significant traction, representing 36% of market share. Production reached 190 million units in 2025, driven by increasing consumer awareness. These oils offer improved skin absorption efficiency of 75% and reduced allergenic risk by 32%. Adoption rates are highest in urban regions, exceeding 65%, reflecting a shift toward safer alternatives.

Organic oil-based products are the fastest-growing segment, accounting for 20% of total volume. Production increased by 28% annually, reaching 100 million units. These products meet stringent certification standards and provide superior skin compatibility, with 92% consumer satisfaction rates. Premium pricing, approximately 35% higher than mineral oil variants, positions them in the high-end market segment.

By Application

Infant care dominates the market, accounting for 58% of total consumption, equivalent to 300 million units in 2025. High adoption rates of 72% among new parents and strong demand for dermatologically tested products drive this segment. Performance metrics such as skin hydration improvement of 40% further support demand.

Adult skincare accounts for 27% of the market, with 140 million units consumed annually. Multi-purpose usage, including makeup removal and moisturization, has driven adoption rates to 58% among adults aged 25–45. Enhanced formulations with vitamins have improved product effectiveness by 30%.

Therapeutic applications account for 15% of demand, with 80 million units used annually. Growth is driven by wellness trends and increasing adoption of massage therapy, particularly in Japan and South Korea, where usage penetration exceeds 48%.

Asia Pacific Baby Oil Market Segmentations

By Type

- Mineral Oil-based

- Natural Oil-based

- Organic Oil-based

By Application

- Infant Care

- Adult Skincare

- Massage & Therapeutic Use

Asia Pacific Baby Oil Regional Outlook

China

China dominates with a 32% share, producing over 165 million units annually. Infant care accounts for 61% of usage, while adult skincare contributes 25%. Rapid urbanization and rising disposable incomes have driven demand, with e-commerce accounting for 42% of sales.

South Korea

South Korea holds a 9% share, with production of 48 million units. Premium and organic products dominate, accounting for 57% of sales. High consumer awareness and advanced skincare technology adoption at 74% support growth.

Japan

Japan contributes 18% of revenue, with 72 million units produced annually. Premium products dominate with 64% share, driven by high-quality standards and innovation.

India

India accounts for 21% of volume, producing 110 million units. Price-sensitive markets dominate, with mineral oil products holding 52% share. Rural penetration remains at 49%, indicating growth potential.

Australia & Singapore

Combined share of 8%, with high adoption of organic products at 61%. Premium segment dominates due to high disposable income levels.

Taiwan & Southeast Asia

Collectively account for 12% share, with production exceeding 60 million units. Growing middle-class population and increasing awareness drive demand.

Top players in Asia Pacific Baby Oil

- Johnson & Johnson

- Pigeon Corporation

- Himalaya Wellness

- Sebapharma

- Chicco

- Mustela

- Burt’s Bees

- Mothercare

- Dabur India

- Unilever

- Beiersdorf

- Kao Corporation

- Procter & Gamble

-

Johnson & Johnson

-

Holds approximately 22% market share with strong brand presence across Asia Pacific.

-

Maintains leadership through extensive distribution networks covering over 60% of retail outlets and invests 12% of revenue in R&D for product innovation.

-

-

Pigeon Corporation

-

Commands around 14% share, particularly strong in Japan and Southeast Asia.

-

Focuses on premium and organic segments, with 68% of revenue derived from high-end product lines.

-

Investment Analysis

Investment in the Baby Oil Market has increased significantly, with total regional investment exceeding USD 420 million in 2025. Approximately 38% of investments are directed toward organic product development, while 27% focus on supply chain enhancements. China and India attract 46% of total investments, driven by large consumer bases.

M&A activities have intensified, with over 18 major deals recorded between 2022 and 2025. Strategic collaborations between raw material suppliers and manufacturers have improved production efficiency by 21%. Private equity investments account for 24% of total funding, reflecting strong market confidence.

New Product Developments

New product launches account for 19% of total offerings, with innovations focused on hypoallergenic and fragrance-free formulations. Performance improvements of 28% in skin hydration and 35% in absorption rates have been achieved through advanced formulations.

Recent Developments in Asia Pacific Baby Oil

- 2025: Production increased by 14% with launch of organic variants, reaching 520 million units.

- 2024: Adoption of natural oils grew by 18%, improving market penetration

Research Methodology

The research methodology includes a comprehensive approach combining primary and secondary research. Primary research involved interviews with over 50 industry experts, manufacturers, and distributors, covering approximately 70% of the supply chain. Secondary research included analysis of industry reports, company financials, and government databases. Market size estimation was conducted using both top-down and bottom-up approaches, ensuring accuracy within a 5% margin. Data triangulation and validation techniques were applied to ensure reliability, with over 120 data points analyzed to derive insights.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Consumer Behavior and Premium Product Segments

Mandy Davis is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.