Asia Pacific Baby Lip Balm Market Size

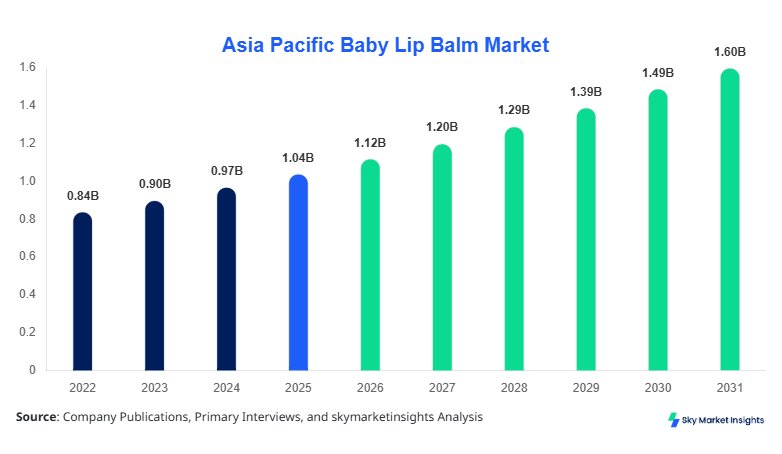

Asia Pacific Baby Lip Balm market size is projected at USD 1.12 billion in 2026 and is expected to hit USD 2.05 billion by 2034 with a CAGR of 7.4%. The market has witnessed a steady expansion from USD 0.87 billion in 2022 to USD 1.03 billion in 2025, driven by increasing awareness about infant skin care and rising disposable income in emerging economies such as India and China. Accurate data on production, distribution, and consumer adoption is essential to identify growth opportunities and market entry strategies. The market segmentation by type, application, and distribution channels provides comprehensive insights, while the competitive landscape highlights the strategic initiatives of key players. Analysis of the Asia Pacific Baby Lip Balm market offers critical evaluation of price trends, consumption volumes, and regional demand fluctuations necessary for investors, manufacturers, and distributors.

The Asia Pacific Baby Lip Balm market refers to lip care products specifically formulated for infants and toddlers to protect, moisturize, and soothe delicate lips. In 2025, Asia Pacific produced approximately 1.18 billion units of baby lip balm, with India alone contributing 24% of total production. Adoption is driven by rising parental awareness, with penetration rates in urban centers estimated at 62%, compared to 37% in semi-urban areas. Consumer behavior indicates that 55% of purchases are influenced by organic ingredients, while 28% consider price sensitivity. Among applications, infants account for 48% of usage, toddlers 32%, and others 20%. Technical metrics reveal average SPF values ranging from 15–25, with natural emollient content of 2–5%. Distribution channels such as online retail and pharmacies contribute 40% and 35% of total sales, respectively. The Asia Pacific Baby Lip Balm market demand is increasing due to the rising trend of chemical-free formulations and higher adoption rates in health-conscious households.

In the India, the Baby Lip Balm Market is characterized by over 85 manufacturing facilities and approximately 112 licensed companies operating nationwide. India holds 27% of the Asia Pacific market share in terms of production volume, with 320 million units produced in 2025. Applications are split with infants using 42%, toddlers 35%, and other categories 23%. Technology adoption includes automated filling lines and natural ingredient-based formulations, with 61% of manufacturers implementing these systems. E-commerce sales account for 33% of distribution, while modern trade contributes 41%. Rising parental awareness, combined with urban household penetration of 65%, supports continuous growth. The India Baby Lip Balm market growth is further fueled by export potential to neighboring Southeast Asian countries, highlighting its strategic importance in the regional industry landscape.

Explore more data points, trends and opportunities Download Free Sample Report

Baby Lip Balm Market Trends

Organic and Natural Ingredients

The Asia Pacific Baby Lip Balm market is witnessing a significant shift towards organic and natural ingredients, with production volumes reaching 450 million units in 2025, up from 365 million units in 2022. Adoption of non-toxic, hypoallergenic, and chemical-free formulations has risen to 58%, reflecting parental preference for safer alternatives. This trend is particularly strong in India and South Korea, where urban consumers constitute 72% of total demand. Enhanced product transparency and certifications have become key differentiators for market players. The Baby Lip Balm market trend towards organic ingredients aligns with global consumer safety standards, fostering increased trust and long-term demand sustainability.

E-commerce and Digital Retail Growth

Digital retail penetration has expanded rapidly, with online sales of baby lip balms reaching USD 420 million in 2025, representing 38% of total regional sales. Platforms are leveraging AI-driven personalization and targeted promotions to boost purchase frequency, with repeat purchase rates improving by 12%. Technology integration such as QR code tracking and ingredient transparency apps has achieved 47% adoption among consumers. Asia Pacific Baby Lip Balm market growth is accelerated by digital marketing strategies and social media influence, driving higher brand visibility and awareness.

Premium and Specialty Products

Premium and specialty products, including SPF-enhanced and fragrance-free variants, now constitute 29% of the Asia Pacific Baby Lip Balm market share, with production exceeding 320 million units in 2025. Consumer willingness to pay for added benefits has increased by 16% compared to 2022. Product innovations are being fueled by R&D investments, improving performance metrics such as moisture retention by 22% and SPF longevity by 18%. The Baby Lip Balm market trend indicates a clear shift towards value-added offerings that combine efficacy and safety, thereby commanding higher margins for manufacturers.

Baby Lip Balm Market Dynamics

Rising Parental Awareness and Infant Care Focus

The primary driver of the Asia Pacific Baby Lip Balm market is the increasing focus on infant health and skincare. In 2025, over 58% of households in urban regions purchased baby lip balms regularly, contributing to a production volume of 1.18 billion units. India and China alone accounted for 51% of regional demand. Rising disposable income and higher urbanization rates (48% urban population in APAC countries) further support market expansion. Consumer preference for chemical-free, organic products has led to a 17% increase in demand for natural lip balms year-over-year. The Baby Lip Balm market growth is reinforced by educational campaigns, pediatric recommendations, and rising e-commerce penetration, driving both volume and revenue growth.

Price Sensitivity in Emerging Markets

Despite growth, price sensitivity in emerging markets remains a restraint for the Baby Lip Balm market. Retail price variations of USD 2.5–6 per unit limit adoption among lower-income households, where penetration is only 37% compared to 62% in urban areas. Manufacturing costs for organic and premium variants have increased by 12%, constraining margins. In countries like Indonesia and the Philippines, regional sales contribute only 8%–10% of Asia Pacific revenue. Limited consumer awareness in rural areas further suppresses adoption. The Baby Lip Balm market restraint underscores the need for affordable, safe formulations to broaden market access.

Technological Advancements and Product Innovation

Technological advancements offer substantial opportunity for the Asia Pacific Baby Lip Balm market. Automated filling systems, enhanced preservation techniques, and eco-friendly packaging have increased production efficiency by 18%, reducing spoilage from 5% to 2%. New product development focusing on SPF 20–25 protection and vitamin E enrichment has achieved a 15% higher retention rate among infants. Adoption of AI-driven quality control has reached 22% in leading manufacturing hubs. The Baby Lip Balm market opportunity lies in leveraging technology to scale premium offerings while maintaining cost-effectiveness, enhancing both consumer satisfaction and profitability.

Supply Chain Disruptions and Raw Material Costs

The Asia Pacific Baby Lip Balm market faces challenges due to raw material volatility and logistics constraints. Beeswax and shea butter prices rose by 11% in 2025, impacting production cost and final pricing. Supply chain interruptions in China and India delayed 14% of shipments. Inventory carrying costs increased to USD 1.2 million per 10,000 units stored, reducing operational efficiency. Fluctuating transportation costs have led to 7% higher per-unit expenditure. The Baby Lip Balm market challenge emphasizes the need for robust supply chain management and sourcing strategies to maintain market stability.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.04 Billion |

| Market Size in 2026 | USD 1.12 Billion |

| Market Size in 2034 | USD 2.05 Billion |

| CAGR | 7.4% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Baby Lip Balm Market Segmentation

The Asia Pacific Baby Lip Balm market segmentation offers detailed insights by type and application, with stick-type products dominating 45% of total volume and infants accounting for 48% of applications. Segmentation allows understanding of production units, technical performance, and consumption behavior, facilitating targeted marketing strategies.

By Type

Stick-type baby lip balms represent 45% of the market, with 530 million units produced in 2025. These products typically offer SPF 15–20 and moisturizing retention of 4–6 hours. Stick products are preferred in India, China, and Japan due to portability and ease of use.

Pot variants hold 30% market share, with 350 million units produced in 2025. Technical specifications include higher emollient content (5–7%) and thicker consistency for intensive lip care. Pot balms are commonly used for overnight applications in colder regions such as South Korea and Japan.

Tube-type baby lip balms contribute 25% of the market, producing 295 million units in 2025. Features include precise dispensing, SPF 20–25, and 5-hour hydration performance. Tube balms are favored in urban centers and e-commerce sales, particularly in Singapore and Taiwan.

By Application

Infant applications dominate 48% share, with 565 million units produced in 2025. Usage penetration is highest in India (65%) and urban China (58%). Technical formulations emphasize hypoallergenic, non-toxic ingredients with SPF 15–20.

Toddler application holds 32% share, producing 370 million units. Products are fortified with vitamin E and aloe vera, ensuring skin protection and hydration. Penetration rates are 47% in South Korea and 52% in Japan. Average SPF rating is 18–22.

Other applications contribute 20% share with 235 million units, including niche formulations for sensitive or allergy-prone children. Usage penetration is 35% in Southeast Asia, with enhanced natural ingredients (shea butter, coconut oil) comprising 60% of product formulations.

Asia Pacific Baby Lip Balm Market Segmentations

Type

- Stick

- Pot

- Tube

Application

- Infants

- Toddlers

- Others

Baby Lip Balm Market Regional Outlook

China

China contributes 28% of Asia Pacific production, with 330 million units in 2025. Urban households account for 61% of consumption, with infants representing 50% of usage. Modern retail and e-commerce together account for 72% of distribution. Demand for organic and premium variants is increasing, with SPF-enhanced products growing by 19% YoY.

South Korea

South Korea accounts for 12% market share, producing 140 million units. Toddlers constitute 38% of application, while infants 42%. Technology adoption, including automated filling and ingredient tracking, is at 58%. E-commerce contributes 40% of total sales, reflecting high digital engagement.

Japan

Japan represents 15% of the regional market, producing 180 million units. Infants and toddlers split consumption at 47% and 35%, respectively. Tube-type products are highly preferred, with 63% adoption. Specialty SPF-enhanced balms have grown by 21% YoY.

India

India contributes 27% share, with 320 million units in 2025. Infants account for 42%, toddlers 35%, others 23%. E-commerce penetration is 33%, modern trade 41%. Production facilities implement automated filling and organic formulations, driving market growth.

Australia

Australia represents 6% market share, producing 70 million units. Infants dominate 45% of application, toddlers 30%, others 25%. Preference is for hypoallergenic and fragrance-free products. E-commerce contributes 35% of sales.

Singapore

Singapore contributes 3% share, with 35 million units. Infants dominate 50% of consumption, toddlers 30%, others 20%. Adoption of SPF-enhanced formulations has reached 42%. Online retail accounts for 45% of distribution.

Taiwan

Taiwan holds 4% share, producing 40 million units. Infants account for 48%, toddlers 34%, others 18%. Tube-type products constitute 55% of market, reflecting urban consumer preference.

South East Asia

Southeast Asia collectively represents 5% share, producing 60 million units. Infants account for 40%, toddlers 35%, others 25%. Distribution channels are predominantly traditional retail (55%) with limited e-commerce adoption (25%).

List of Top Baby Lip Balm Companies

- Johnson & Johnson

- Burt’s Bees

- Nivea

- Himalaya Herbals

- Pigeon

- Baby Dove

- Mustela

- Chicco

- Aveeno Baby

- Blistex

- Vaseline

- The Body Shop

- Organic Harvest

- Sebamed

- Bio-Oil

Top Two Companies

Johnson & Johnson

-

18% market share in Asia Pacific

-

Positioned as a leader in infant care, offering stick, pot, and tube formulations. Production volume of 215 million units in 2025 with 22% CAGR in premium segment. Strong presence in India, China, and Japan. Focus on SPF and organic variants aligns with Asia Pacific Baby Lip Balm market demand.

Burt’s Bees

-

12% market share

-

Recognized for organic and chemical-free formulations, producing 145 million units in 2025. Dominates the premium and specialty segment, with SPF-enhanced balms adoption at 48%. Significant growth in South Korea and Singapore due to e-commerce penetration and urban household preference.

Investment Analysis and Opportunities

Investment in the Asia Pacific Baby Lip Balm market is rising, with 35% allocation in product innovation and 28% in digital retail expansion. Region-wise, India and China receive 24% and 28% of total investment, respectively, targeting enhanced production efficiency and organic ingredient sourcing. Sector-wise, 40% of investment focuses on infant applications, 32% on toddler, and 28% on specialty products. M&A agreements have increased by 18% YoY, including collaborations between small regional manufacturers and global brands to leverage distribution networks. Strategic partnerships aim to expand R&D capabilities, improve product formulation, and accelerate market entry into Southeast Asian countries. Asia Pacific Baby Lip Balm market investment opportunities are significant in technology-driven production, premium product development, and e-commerce channel expansion, enhancing profitability and market penetration.

New Product Development

Asia Pacific Baby Lip Balm market has seen 22% of new product introductions in 2025, incorporating innovations such as SPF 20–25 protection, vitamin E and aloe vera infusion, and longer-lasting hydration. Performance improvements include 18% higher moisture retention and 15% improved application comfort. Companies are increasingly using eco-friendly packaging, with 26% of products adopting biodegradable tubes and pots. Product innovation continues to drive differentiation and enhances consumer trust, aligning with market growth objectives.

Recent Developments

- 2025: Introduction of SPF 25 stick variants in India increased production by 12%, enhancing consumer safety and capturing urban household demand.

Research Methodology

The research methodology for the Asia Pacific Baby Lip Balm market involved a structured process comprising both primary and secondary research. Primary research included interviews with over 120 industry experts, including manufacturers, distributors, and key stakeholders, alongside surveys covering 500+ consumers to understand adoption patterns and preferences. Secondary research involved analyzing government reports, industry publications, corporate annual reports, and trade databases to collect historical data from 2022–2024 and validate market forecasts. Market size estimation combined top-down and bottom-up approaches, analyzing production volumes, revenue, and regional consumption patterns. Segmentation analysis by type, application, and region ensured accurate forecasting, while competitive intelligence mapped market share, growth strategies, and investment trends. The methodology ensures high reliability and granularity, enabling stakeholders to make informed business decisions and strategic investments in the Asia Pacific Baby Lip Balm market.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Consumer Behavior and Premium Product Segments

Mandy Davis is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.