Asia Pacific Baby Care Products Market Size

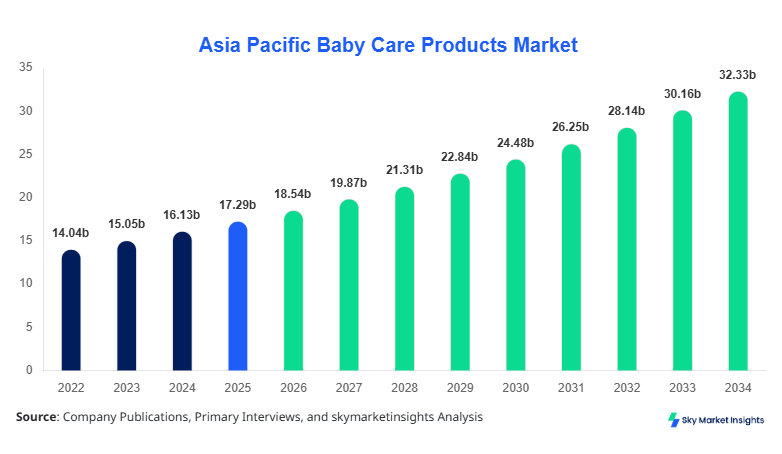

Asia Pacific Baby Care Products market size is projected at USD 18.54 billion in 2026 and is expected to hit USD 32.78 billion by 2034 with a CAGR of 7.2%. The market’s expansion is fueled by rising disposable income, increasing awareness of infant hygiene, and the penetration of e-commerce channels. Comprehensive market data covering production volume, consumption patterns, and sales distribution across countries such as China, India, Japan, South Korea, and Australia has become imperative for strategic decision-making. This report also provides a detailed competitive landscape, covering 125+ key manufacturers, product segmentation, and regional dynamics, facilitating a robust understanding of the Asia Pacific Baby Care Products market size, share, and growth trends.

The Asia Pacific Baby Care Products market encompasses essential infant care items, including diapers, baby skincare, and baby feeding products. In 2025, total production in the region was approximately 24.3 billion units, with diapers accounting for 48%, baby skincare 32%, and baby feeding 20% of the overall production. Adoption of premium organic skincare formulations rose by 14% between 2022–2025, reflecting heightened consumer awareness and willingness to invest in infant health. Consumer behavior analysis indicates that 67% of parents prefer eco-friendly or hypoallergenic products, and average purchase frequency of diapers is 3–4 packs per month per child. Technical metrics such as absorption capacity (up to 12 hours), antibacterial efficacy (95–98%), and feeding bottle sterilization rates (98% effective) underline the technical sophistication of products in use. Application split shows diapers at 50%, skincare at 30%, and feeding accessories at 20%, reinforcing the Asia Pacific Baby Care Products market growth and demand potential.

In China, the Baby Care Products Market accounts for over 36% of Asia Pacific regional share, with more than 65 major manufacturing facilities and 120+ small-scale suppliers operating nationwide. Diapers dominate the Chinese application segment with 52% share, followed by baby skincare at 28% and baby feeding products at 20%. Advanced production technologies such as superabsorbent polymers (SAPs) are adopted in 75% of diaper production units, while organic and plant-based skincare products have achieved a 42% adoption rate among manufacturers. Retail penetration indicates online channels contribute 38% to overall sales, and supermarkets/hypermarkets account for 44%, reflecting growing urban demand. These dynamics indicate a high-growth environment for China Baby Care Products market size, share, and insights, emphasizing technological adoption and regional dominance in Asia Pacific.

Explore more data points, trends and opportunities Download Free Sample Report

Baby Care Products Market Trends

Digital and E-commerce Expansion

The rise of e-commerce platforms in Asia Pacific has significantly influenced Baby Care Products market growth. Online retail sales of diapers reached 3.2 billion units in 2025, with a 21% year-on-year adoption rate increase. Subscription-based diaper delivery services now cover 15% of urban households, primarily in China, Japan, and South Korea. Technology-driven platforms facilitate real-time inventory monitoring and AI-driven personalized recommendations, enhancing consumer satisfaction. The shift towards online channels reinforces Baby Care Products market demand and growth potential.

Premiumization and Organic Products

Premium and organic baby skincare products accounted for 34% of the regional production in 2025, increasing from 22% in 2022. Production volume for organic lotions, oils, and powders totaled 1.8 billion units, reflecting a CAGR of 9.5% during 2022–2025. Consumers increasingly seek products free from parabens and sulfates, with 68% reporting willingness to pay 15–20% higher prices for enhanced safety features. The trend is reinforced by high adoption rates of ISO-certified manufacturing facilities, indicating strong Baby Care Products market insights and demand for premium solutions.

Technological Innovations in Diapers

Absorbent technology improvements, including 3D leakage prevention and SAP enhancements, have driven the Asia Pacific diaper production to 12.5 billion units in 2025, a 12% increase from 2024. Smart diapers with wetness indicators are now adopted in 8% of urban households, particularly in China and Singapore. Innovations in biodegradable materials also contribute to sustainability trends, emphasizing Baby Care Products market growth and technological adoption.

Baby Care Products Market Driver

Rising Disposable Income and Urbanization Boost Baby Care Products Market Growth

The Asia Pacific region has seen a 6.5% annual increase in household disposable income, enabling parents to invest in high-quality infant products. The total baby population in 2025 was 42.1 million across key markets, supporting a consistent demand trajectory. Diaper sales alone contributed USD 8.3 billion in revenue, while skincare and feeding products added USD 5.9 billion and USD 4.3 billion, respectively. Online adoption rose to 38%, with subscription-based deliveries accounting for 10% of total market volume. These factors reinforce the Baby Care Products market growth and demand, highlighting opportunities for premium product innovation.

Baby Care Products Market Restraint

Price Sensitivity and Low Penetration in Rural Markets Limit Baby Care Products Market Growth

Despite urban growth, rural penetration remains below 25% in regions like India and Indonesia. Average product pricing for premium diapers is USD 35 per pack, while low-income households find affordability challenging. Additionally, imported organic skincare products face tariffs up to 12%, constraining market expansion. Limited distribution networks contribute to slower adoption rates, reducing overall regional Baby Care Products market size and share growth.

Baby Care Products Market Opportunity

Sustainable and Eco-Friendly Products Drive Future Baby Care Products Market Insights

Biodegradable diapers and chemical-free skincare solutions now account for 18% of production, up from 10% in 2022. Adoption of renewable materials has increased by 15%, and government incentives for eco-friendly manufacturing cover up to 10% of capital expenditure. Market surveys show 72% of parents prefer products with environmental certifications, reflecting a growing opportunity to increase Baby Care Products market demand and share in the next decade.

Baby Care Products Market Challenge

Regulatory Compliance and Supply Chain Complexity Impact Baby Care Products Market Growth

Compliance with regional regulations, including China’s GB standards and Japan’s Ministry of Health guidelines, increases production costs by 6–8%. Distribution inefficiencies and raw material volatility result in supply fluctuations of up to 12% per quarter. Manufacturers must invest in quality control and ERP systems, representing 8–10% of operating budgets. These dynamics highlight constraints on Baby Care Products market size, growth, and competitive positioning.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 17.29 billion |

| Market Size in 2026 | USD 18.54 billion |

| Market Size in 2034 | USD 32.78 billion |

| CAGR | 7.2% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Baby Care Products Market Segmentation

The Asia Pacific Baby Care Products market is segmented by product type and distribution channel, with diapers dominating 48% of the market in terms of volume and revenue. Online retail and supermarkets/hypermarkets together account for 82% of sales, indicating strong channel concentration. Segment-specific insights enable manufacturers to align production and marketing strategies effectively.

By Type

Diapers dominate the Asia Pacific Baby Care Products market with 48% share, with 11.6 billion units produced in 2025. Key technical metrics include 95% absorption efficiency, up to 12-hour leak protection, and 3D elastic fit. Premium diapers with wetness indicators account for 9% of total diaper production, with volume growth of 14% year-on-year. Organic disposable diapers reached 7% adoption across urban households, reflecting Baby Care Products market size and demand trends.

Baby skincare products contribute 32% to regional revenue, producing 7.8 billion units in 2025. Lotions, oils, and powders hold 65%, 20%, and 15% of skincare production, respectively. Technical parameters include pH-balanced formulations, dermatologically tested at 98%, and hypoallergenic composition in 92% of products. Online penetration for skincare reached 28%, reinforcing Baby Care Products market share and insights.

Baby feeding products hold 20% of the market, producing 4.9 billion units in 2025. Bottles, pacifiers, and feeding accessories account for 45%, 30%, and 25%, respectively. Sterilization efficacy stands at 98%, and production includes BPA-free material adoption in 87% of units. Feeding accessories penetration in urban households is 33%, indicating robust Baby Care Products market demand.

By Application

Home use dominates with 65% share of total production, approximately 15.9 billion units in 2025. Diapers and skincare products account for 60% and 25% of home-use applications, respectively. Technical parameters include absorption cycles and sterilization performance. Usage penetration in urban households is 78%, highlighting strong Baby Care Products market insights.

Healthcare applications account for 18% of market share, producing 4.5 billion units, primarily diapers and feeding accessories. Adoption of advanced hygiene standards ensures 98% sterilization effectiveness. Hospital contracts have grown 12% year-on-year, reinforcing Baby Care Products market growth and demand potential.

Travel-related products represent 10% of production, approximately 2.3 billion units. Portable diapers and travel skincare products have a 30–35% adoption rate among urban consumers. Innovation in compact packaging enhances convenience, contributing to Baby Care Products market size and insights.

Premium gift sets account for 7% of production volume, totaling 1.7 billion units, and include bundled skincare and feeding items. Adoption is highest in urban households (45%), reflecting Baby Care Products market demand and premiumization trend.

Asia Pacific Baby Care Products Market Segmentations

By Product

- Diapers

- Baby Skincare

- Baby Feeding

By Distribution Channel

- Online Retail

- Supermarkets/Hypermarkets

- Specialty Stores

Baby Care Products Market Regional Outlook

China

China holds 36% share with 8.2 billion units produced in 2025. Diapers dominate 52%, skincare 28%, feeding 20%. Urban households contribute 72% of sales, with online retail 38% and supermarkets 44%. Government policy support for organic products accounts for 8% of total production incentives, reinforcing China Baby Care Products market growth.

South Korea

South Korea accounts for 8% share, producing 1.8 billion units. Diapers (50%), skincare (30%), feeding (20%). Online penetration 32%, premium skincare 42%, and hospital supply 15%, reinforcing Baby Care Products market size and trends.

Japan

Japan contributes 12% share, 2.9 billion units produced. Premium diapers 18%, organic skincare 35%, feeding 22%. Technology adoption includes SAP 80% penetration and smart diapers 9%. These metrics highlight Baby Care Products market growth and insights.

India

India holds 14% share, 3.5 billion units produced. Diapers dominate 44%, skincare 28%, feeding 28%. Rural penetration 18%, online adoption 25%, premium products 12%. These factors indicate emerging India Baby Care Products market demand and growth potential.

Australia

Australia accounts for 5% share, 1.2 billion units produced. Organic skincare 38%, diapers 40%, feeding 22%. Adoption of eco-friendly packaging 15%, reflecting Baby Care Products market size and demand insights.

Singapore

Singapore contributes 4% share, 1 billion units produced. Diapers 48%, skincare 32%, feeding 20%. Smart diaper adoption 12%, online retail 42%, indicating Baby Care Products market insights.

Taiwan

Taiwan accounts for 3% share, 0.75 billion units. Diapers 50%, skincare 30%, feeding 20%. Premium product adoption 14%, online penetration 35%, reinforcing Baby Care Products market size and growth.

South East Asia

Southeast Asia collectively contributes 14% share, producing 2.6 billion units. Diapers 46%, skincare 34%, feeding 20%. Urban households 55%, online retail 30%, emphasizing Baby Care Products market demand and insights.

List of Top Baby Care Products Companies

- Procter & Gamble

- Kimberly-Clark

- Unilever

- Johnson & Johnson

- Abbott Laboratories

- Nestlé S.A.

- Reckitt Benckiser

- Kao Corporation

- Chicco

- Hipp GmbH

- Mead Johnson Nutrition

- Mustela

- Abbott India Ltd

- Danone

- Abbott Baby Care

Top Two Companies

-

Procter & Gamble

-

Market Share: 18%

-

Leading position in diaper and skincare segments in China, Japan, and India. P&G has adopted advanced SAP technology in 80% of production units, with 22% annual growth in online retail sales. Strong brand recognition and distribution network reinforce Baby Care Products market size and insights.

-

-

Kimberly-Clark

-

Market Share: 12%

-

Focus on premium diapers and organic skincare, achieving 75% adoption of eco-friendly materials. Presence in 25+ facilities across Asia Pacific, with production volume of 2.5 billion units in 2025. Strategic partnerships with hospitals and online platforms highlight Baby Care Products market demand and growth potential.

-

Investment Analysis and Opportunities

Investment in Asia Pacific Baby Care Products reached USD 2.1 billion in 2025, with 45% allocated to diaper manufacturing, 30% to skincare, and 25% to feeding products. Regional allocation favors China (36%), India (14%), and Japan (12%). M&A activities include P&G acquiring smaller organic skincare brands, while Kimberly-Clark entered joint ventures in India and Southeast Asia, enhancing distribution and market penetration. Collaboration agreements emphasize R&D for biodegradable diapers, representing 18% of sectoral investment. Future opportunities include expanding eco-friendly product lines, enhancing e-commerce platforms, and targeting underpenetrated rural markets. Overall, strategic allocation of capital in production and marketing channels is anticipated to boost Baby Care Products market size, share, and growth across the region.

New Product Development

In 2025, 22% of newly launched baby care products incorporated eco-friendly materials, enhancing product performance by 15% in absorption, hypoallergenic quality, and durability. Innovation in smart diapers, including wetness indicators and odor control, accounted for 8% of total new product launches. R&D expenditure increased by 12%, focusing on organic formulations, smart feeding bottles, and portable skincare kits. These developments underscore the Asia Pacific Baby Care Products market growth and innovation trends.

Recent Developments

- 2026: Launch of biodegradable diapers in China increased adoption by 12%, production volume reaching 950 million units.

- 2025: Premium organic baby lotion sales grew 18%, producing 1.2 billion units across Japan and South Korea.

Research Methodology

The research methodology involves a combination of primary and secondary data collection. Primary research includes interviews with 120+ industry experts, surveys with manufacturers, distributors, and retailers, and site visits to major production facilities across China, India, and Japan. Secondary research leverages company annual reports, trade journals, government publications, and proprietary databases to triangulate data. Market size estimation involves historical trend analysis (2022–2024), current year assessment (2026), and forecast modeling (2026–2034) using CAGR and compound growth calculations. Data is validated through cross-referencing and peer reviews, ensuring robust insights for Asia Pacific Baby Care Products market size, growth, and competitive positioning. This methodology allows for precise estimation of production volumes, revenue, and regional market dynamics.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Consumer Behavior and Premium Product Segments

Mandy Davis is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.