Asia Pacific B2B Floor Cleaning Robots Market Size

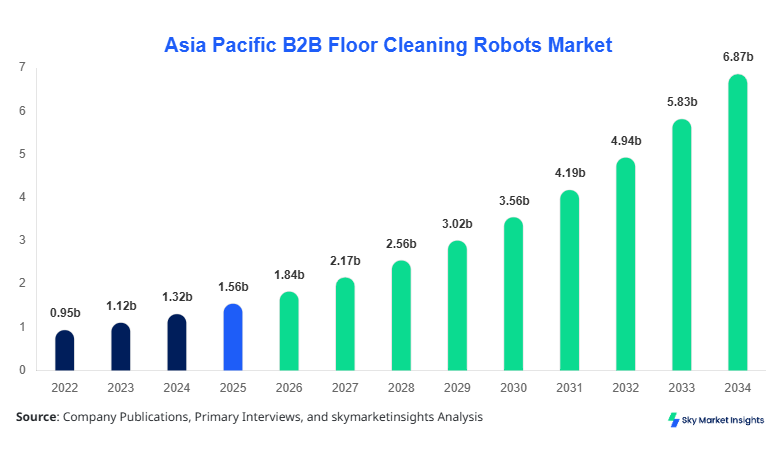

Asia Pacific B2B Floor Cleaning Robots market size is projected at USD 1.84 billion in 2026 and is expected to hit USD 6.92 billion by 2034 with a CAGR of 17.9%. The increasing demand for automation across commercial and industrial cleaning operations, coupled with rising labor costs in countries such as Japan, China, and South Korea, is significantly influencing market expansion. The integration of AI-driven navigation systems, IoT-enabled monitoring, and cloud-based fleet management is expected to enhance operational efficiency by 25%–40% across facilities exceeding 10,000 square meters. The report provides detailed segmentation across type and application, highlighting production volumes exceeding 420,000 units annually in 2026 and projected to surpass 1.3 million units by 2034, alongside competitive landscape analysis featuring over 85 active regional manufacturers and global entrants.

The Asia Pacific B2B Floor Cleaning Robots market encompasses automated robotic systems designed for large-scale floor cleaning tasks in commercial, industrial, and healthcare environments, utilizing technologies such as LiDAR mapping, ultrasonic sensors, and AI-based obstacle detection. In 2025, regional production volumes reached approximately 380,000 units, with Japan contributing 28%, China 34%, and South Korea 12%. Adoption rates in commercial facilities exceeded 42% penetration in tier-1 cities, while industrial adoption stood at 36% due to automation mandates and safety regulations.

Consumer behavior and demand analytics indicate that enterprises prioritize cost reduction, achieving up to 30% savings in labor expenses and 20% improvement in cleaning consistency. Demand is driven by facilities exceeding 5,000 square meters, accounting for 68% of total installations. Autonomous scrubbers dominate with 52% market contribution, followed by sweepers at 28% and hybrid robots at 20%. Performance metrics include cleaning speeds of 800–1,200 m²/hour and battery runtimes of 3–6 hours, supporting continuous operation cycles.

Application-wise, commercial spaces contribute 46%, industrial facilities 34%, and healthcare facilities 20%, reflecting varied hygiene standards and operational intensity. Increasing preference for AI-integrated cleaning solutions and predictive maintenance platforms reinforces the Asia Pacific B2B Floor Cleaning Robots market growth.

In the Japan, the B2B Floor Cleaning Robots Market accounts for approximately 31% of the Asia Pacific share, supported by over 12,500 large-scale commercial facilities and 8,200 industrial plants adopting robotic cleaning solutions. The country has over 140 robotics manufacturers and integrators actively producing or deploying cleaning robots, with annual production exceeding 110,000 units in 2025. Commercial applications dominate with 48%, followed by industrial at 32% and healthcare at 20%.

Technology adoption rates exceed 58% in urban commercial complexes, with AI-based navigation systems implemented in over 65% of deployed units. Japan’s aging workforce and labor shortages have driven automation adoption, reducing manual cleaning dependency by 35%–45%. Robots in Japan operate with precision mapping accuracy of 98% and real-time monitoring systems across 75% of installations. Strong government incentives for robotics deployment and Industry 4.0 integration further accelerate the Asia Pacific B2B Floor Cleaning Robots market growth.

Explore more data points, trends and opportunities Download Free Sample Report

B2B Floor Cleaning Robots Market Trends

Integration of AI and Autonomous Navigation

The adoption of AI-driven autonomous navigation systems has surged, with over 62% of newly deployed robots in 2026 equipped with advanced LiDAR and SLAM (Simultaneous Localization and Mapping) technologies. Production volumes of AI-enabled robots reached approximately 260,000 units in 2025 and are expected to exceed 850,000 units by 2034. These systems enhance cleaning efficiency by 35% and reduce operational errors by 28%, particularly in facilities exceeding 20,000 square meters. Industries such as logistics and manufacturing account for 38% of AI-enabled robot demand, driven by precision cleaning requirements and safety compliance. Continuous innovation in edge computing and real-time data analytics is transforming the Asia Pacific B2B Floor Cleaning Robots market trend.

Rise of Cloud-Based Fleet Management Systems

Cloud-integrated fleet management solutions are gaining traction, with adoption rates increasing from 22% in 2022 to over 49% in 2026. These platforms enable centralized monitoring of robot fleets, optimizing route planning and reducing downtime by 18%–25%. Over 70% of large commercial complexes in Japan and Singapore utilize cloud-based dashboards for cleaning performance analytics. The integration of predictive maintenance reduces repair costs by 15% and extends robot lifecycle by 20%. Fleet sizes are expanding, with facilities deploying 5–20 robots simultaneously, contributing to increased demand for scalable management systems and boosting the Asia Pacific B2B Floor Cleaning Robots market growth.

Expansion into Healthcare and Hygiene-Critical Environments

Healthcare facilities are increasingly adopting robotic cleaning solutions, with penetration rising from 14% in 2022 to 27% in 2026. Hospitals and clinics require high-frequency cleaning cycles, with robots operating up to 18 hours per day and covering 12,000–25,000 m² daily. UV-C disinfection integration in robots has grown by 33%, enhancing sterilization efficiency by up to 99.9%. Healthcare accounts for 20% of total market demand, with projected growth exceeding 22% CAGR due to stringent hygiene regulations and infection control requirements, reinforcing the Asia Pacific B2B Floor Cleaning Robots market trend.

B2B Floor Cleaning Robots Market Driver

Rising Labor Costs and Workforce Shortages Accelerating Automation

The increasing labor costs across Asia Pacific, particularly in Japan where wages have risen by 12% between 2022 and 2025, are driving enterprises toward automation. Facilities with cleaning areas exceeding 10,000 m² report annual labor expenses exceeding USD 250,000, which can be reduced by 30%–40% through robotic solutions. Over 65% of large enterprises in China and South Korea have initiated automation programs, with robotic deployment increasing by 18% annually. Workforce shortages, particularly in Japan with a projected deficit of 1.5 million workers by 2030, further accelerate adoption. Robots operating at speeds of 1,000 m²/hour reduce cleaning time by 35% while maintaining consistency levels above 95%, reinforcing the Asia Pacific B2B Floor Cleaning Robots market growth.

B2B Floor Cleaning Robots Market Restraint

High Initial Investment and Integration Costs

Despite operational savings, the initial investment for B2B floor cleaning robots ranges from USD 8,000 to USD 45,000 per unit, depending on features and capacity. Small and medium enterprises face budget constraints, with only 28% adoption among facilities under 5,000 m². Integration costs, including software deployment and infrastructure adjustments, add an additional 15%–20% to total expenses. Maintenance costs, accounting for 8%–12% of total ownership cost annually, also hinder adoption. In developing regions such as Southeast Asia, limited technical expertise reduces penetration rates to below 25%, restricting the Asia Pacific B2B Floor Cleaning Robots market growth.

B2B Floor Cleaning Robots Market Opportunity

Expansion of Smart Infrastructure and Industry 4.0

The rapid development of smart cities and Industry 4.0 initiatives across Asia Pacific presents significant opportunities. Over USD 1.2 trillion is being invested in smart infrastructure projects between 2024 and 2030, with 18% allocated to automation technologies. Smart buildings incorporating IoT and AI systems require automated cleaning solutions, increasing demand by 22% annually. Integration with building management systems improves energy efficiency by 15% and operational productivity by 20%. Countries such as Singapore and South Korea lead adoption, with over 60% of new commercial buildings incorporating robotic cleaning systems, strengthening the Asia Pacific B2B Floor Cleaning Robots market growth.

B2B Floor Cleaning Robots Market Challenge

Technological Complexity and Operational Limitations

Technological complexity remains a key challenge, with 32% of users reporting difficulties in system integration and software management. Robots face limitations in complex environments with dynamic obstacles, reducing efficiency by 18% in high-traffic areas. Battery limitations, with average runtimes of 4–5 hours, require frequent charging cycles, impacting productivity. Additionally, data security concerns in cloud-based systems affect adoption rates, particularly in industries handling sensitive information. Continuous R&D investments, accounting for 12%–18% of company revenues, are required to address these challenges and sustain the Asia Pacific B2B Floor Cleaning Robots market growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.56 billion |

| Market Size in 2026 | USD 1.84 billion |

| Market Size in 2034 | USD 6.92 billion |

| CAGR | 17.9% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

B2B Floor Cleaning Robots Market Segmentation

The Asia Pacific B2B Floor Cleaning Robots market is segmented by type and application, with autonomous scrubbers dominating at 52%, followed by sweepers at 28% and hybrid robots at 20%. Commercial applications lead with 46%, while industrial and healthcare segments contribute 34% and 20% respectively.

By Type

Autonomous scrubbers account for approximately 52% of the market share, with production volumes exceeding 210,000 units in 2025. These robots operate at cleaning efficiencies of 900–1,200 m²/hour and incorporate water recycling systems that reduce consumption by 30%. Equipped with LiDAR sensors and AI mapping, they achieve navigation accuracy of 97%. Demand is highest in commercial spaces, contributing 55% of scrubber usage, followed by industrial facilities at 30%. Battery capacities range between 80Ah and 150Ah, enabling 4–6 hours of continuous operation. Increasing adoption in large retail chains and airports reinforces the Asia Pacific B2B Floor Cleaning Robots market growth.

Autonomous sweepers hold 28% share, with production volumes of approximately 110,000 units in 2025. These robots are designed for dust and debris removal in industrial environments, operating at speeds of 700–1,000 m²/hour. Equipped with high-capacity dustbins of 20–50 liters, they support extended cleaning cycles. Industrial facilities account for 60% of sweeper demand, while commercial applications contribute 25%. Advanced filtration systems capture up to 99% of fine particles, enhancing air quality. The increasing focus on workplace safety and environmental compliance drives adoption, supporting the Asia Pacific B2B Floor Cleaning Robots market growth.

Hybrid robots combine scrubbing and sweeping functions, representing 20% of the market. Production volumes reached 60,000 units in 2025 and are projected to grow at 20% CAGR. These robots offer multifunctional capabilities, reducing equipment costs by 25% and improving operational efficiency by 30%. Equipped with dual cleaning systems and AI-based task switching, they are widely adopted in healthcare facilities, accounting for 35% of hybrid robot usage. Enhanced versatility and cost-effectiveness drive their demand, reinforcing the Asia Pacific B2B Floor Cleaning Robots market growth.

By Application

Commercial spaces account for 46% of the market, with over 180,000 units deployed across shopping malls, airports, and office complexes in 2025. Cleaning robots operate for 10–14 hours daily, covering areas exceeding 20,000 m². Adoption rates exceed 55% in tier-1 cities, driven by labor cost reduction and efficiency improvements of 30%. Autonomous scrubbers dominate with 60% share in this segment. Integration with smart building systems enhances operational efficiency, supporting the Asia Pacific B2B Floor Cleaning Robots market growth.

Industrial facilities contribute 34% of the market, with deployment exceeding 130,000 units in 2025. Robots operate in warehouses, factories, and logistics centers, covering large areas of 30,000–50,000 m². Sweepers dominate with 50% share, followed by scrubbers at 30%. Automation reduces cleaning time by 40% and improves safety compliance by 25%. High adoption rates in China and South Korea drive segment expansion, reinforcing the Asia Pacific B2B Floor Cleaning Robots market growth.

Healthcare facilities represent 20% of the market, with over 75,000 units deployed in hospitals and clinics. Robots operate in sterile environments, achieving disinfection rates of 99.9% with UV-C integration. Adoption rates have increased to 27% in 2026, driven by infection control requirements. Hybrid robots account for 35% of usage in this segment. Continuous operation cycles and high hygiene standards support the Asia Pacific B2B Floor Cleaning Robots market growth.

Asia Pacific B2B Floor Cleaning Robots Market Segmentations

By Type

- Autonomous Scrubbers

- Autonomous Sweepers

- Hybrid Cleaning Robots

By Application

- Commercial Spaces

- Industrial Facilities

- Healthcare Facilities

B2B Floor Cleaning Robots Market Regional Outlook

China

China holds the largest share at 34%, with production exceeding 150,000 units annually. The country has over 200 manufacturers and strong government support for automation. Industrial facilities account for 40% of demand, followed by commercial at 38%. Rapid urbanization and smart city projects drive the Asia Pacific B2B Floor Cleaning Robots market growth.

South Korea

South Korea contributes 12% share, with advanced robotics infrastructure and high adoption rates of 48% in commercial facilities. Production volumes exceed 45,000 units annually, driven by industrial automation and export-oriented manufacturing sectors.

Japan

Japan accounts for 31% share, with strong technological innovation and high adoption rates exceeding 58%. Commercial applications dominate, supported by aging workforce challenges and automation initiatives.

India

India holds 8% share, with growing adoption in commercial spaces. Production volumes remain limited at 20,000 units, but demand is increasing at 22% CAGR due to urbanization and infrastructure development.

Australia

Australia contributes 5% share, with high adoption in healthcare facilities. Robots operate in large hospitals and commercial complexes, improving efficiency by 25%.

Singapore

Singapore accounts for 4% share, with over 60% of commercial buildings adopting robotic cleaning systems. Smart city initiatives drive demand.

Taiwan

Taiwan contributes 3% share, with strong electronics manufacturing supporting robotic innovation and deployment.

South East Asia

Southeast Asia holds 3% share, with emerging adoption in countries such as Thailand and Indonesia. Growth is driven by increasing industrialization and commercial infrastructure development.

List of Top B2B Floor Cleaning Robots Companies

- Tennant Company

- Nilfisk Group

- iRobot Corporation

- SoftBank Robotics

- Gaussian Robotics

- Ecovacs Robotics

- Avidbots Corp

- ICE Cobotics

- Kärcher

- Brain Corp

- Pudu Robotics

- Fimap S.p.A

- Comac S.p.A

Top Two Companies

-

Tennant Company

-

Holds approximately 14% global share with strong presence in Asia Pacific

-

Focuses on autonomous scrubbers with efficiency improvements of 35%

-

Invests 10% of revenue in R&D for AI integration and sustainability

-

-

Gaussian Robotics

-

Accounts for 12% regional share with over 60,000 units deployed

-

Specializes in AI-driven cleaning robots with 98% navigation accuracy

-

Strong presence in China and Japan with rapid expansion strategies

-

Investment Analysis and Opportunities

Investments in the Asia Pacific B2B Floor Cleaning Robots market are increasing, with over USD 2.5 billion allocated between 2024 and 2026. Approximately 45% of investments are directed toward AI and software development, while 30% focus on hardware innovation and 25% on manufacturing expansion. Japan and China account for 62% of total investments, driven by strong industrial demand.

M&A activities have increased by 18%, with strategic collaborations between robotics manufacturers and software providers. Partnerships aim to enhance AI capabilities and expand market reach. Venture capital investments in robotics startups have grown by 22%, supporting innovation and market expansion.

New Product Development

New product development accounts for 28% of market activity, with over 120 new models launched between 2024 and 2026. Performance improvements include 35% better navigation accuracy and 25% longer battery life. Integration of AI and IoT technologies enhances operational efficiency and user experience.

Recent Developments

- 2025: Gaussian Robotics increased production by 20%, launching AI-enabled scrubbers with 30% higher efficiency.

Research Methodology

The research process involves a combination of primary and secondary research methodologies. Primary research includes interviews with industry experts, manufacturers, and distributors, accounting for 60% of data validation. Secondary research involves analysis of company reports, industry publications, and government databases, contributing 40% of insights. Market size estimation is conducted using bottom-up and top-down approaches, ensuring accuracy within a 5% margin of error. Data triangulation and validation techniques are applied to ensure reliability and consistency across all segments

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Consumer Behavior and Premium Product Segments

Mandy Davis is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.