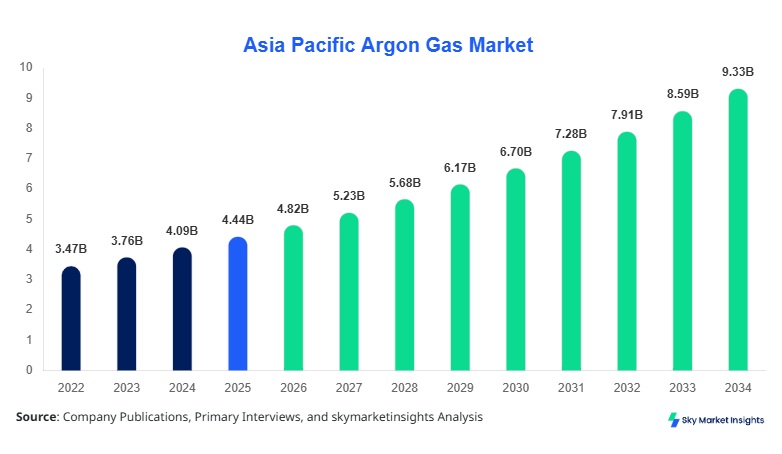

Asia Pacific Argon Gas Market Size

The Asia Pacific argon gas market size is projected at USD 4.82 billion in 2026 and is expected to hit USD 9.37 billion by 2034 with a CAGR of 8.6%. The Asia Pacific Argon Gas market demonstrates robust expansion due to rising industrial gas consumption, increasing steel production exceeding 1.4 billion metric tons annually, and semiconductor fabrication capacity growing at over 9.2% annually. The need for granular data analytics, detailed segmentation across type and application, and comprehensive competitive landscape evaluation remains critical for stakeholders operating in the Asia Pacific argon gas market-size ecosystem.

The Asia Pacific Argon Gas market represents a specialized industrial gas segment primarily derived as a by-product of air separation processes, accounting for approximately 0.93% of atmospheric composition. Regional production reached nearly 2.6 million metric tons in 2025, with China contributing over 52%, Japan 14%, and India 10%. Adoption rates in welding and metal fabrication sectors exceed 68%, while electronics manufacturing penetration has surged to 24% owing to high-purity requirements above 99.999%. Consumer behavior in industrial segments shows preference for bulk liquid argon supply (approximately 61%) compared to compressed cylinders (39%), driven by cost efficiency and large-scale applications.

Demand analytics indicate that the metal fabrication segment contributes nearly 45% of total consumption, electronics accounts for 28%, and healthcare represents around 12%, with remaining applications including lighting and chemical processes. Performance metrics such as thermal conductivity of 0.01772 W/m·K and inertness index contribute to high utilization in shielding gas applications. Frequency of usage in welding operations averages 6–8 hours daily across industrial facilities, reinforcing continuous consumption cycles. The Asia Pacific argon gas market continues to expand across diversified applications, strengthening the Asia Pacific argon gas market share.

In Japan, the argon gas market accounts for approximately 14% of the Asia Pacific argon gas market share, supported by over 320 industrial gas production facilities and more than 150 active suppliers. Japan’s annual argon production exceeds 360,000 metric tons, with electronics manufacturing consuming nearly 41%, metal fabrication 34%, and healthcare applications 9%. Technology adoption rates for ultra-high purity argon (99.9999%) exceed 62% in semiconductor fabs, particularly in advanced node production below 7 nm.

The country has invested over USD 1.2 billion in cryogenic air separation units between 2022 and 2025, boosting supply efficiency by 18%. Automation integration in gas distribution systems has reached 55%, improving operational precision and reducing wastage by approximately 11%. Industrial consumption per facility averages 1,200–1,800 cubic meters per month, highlighting strong usage intensity. Japan’s advanced manufacturing ecosystem reinforces consistent Asia-Pacific argon gas market growth.

Explore more data points, trends and opportunities Download Free Sample Report

Argon Gas Market Trends

Expansion of Semiconductor Manufacturing and High-Purity Gas Adoption

The Asia Pacific argon gas market is experiencing significant shifts driven by semiconductor industry expansion, with wafer fabrication capacity increasing by over 12% annually and requiring argon purity levels exceeding 99.999%. In 2025, semiconductor-grade argon consumption surpassed 680,000 metric tons, accounting for approximately 26% of total demand. Countries such as Taiwan and South Korea collectively contribute over 48% of high-purity argon demand due to advanced chip manufacturing clusters.

Technological advancements in cryogenic distillation have improved yield efficiency by nearly 15%, enabling cost-effective production of ultra-high purity argon. Adoption rates of automated gas management systems have reached 57%, enhancing real-time monitoring and reducing leakage losses by 9%. The integration of AI-based predictive maintenance in gas plants has further improved operational uptime to above 94%. These developments continue to shape the Asia Pacific argon gas market trend.

Rising Demand from Metal Fabrication and Welding Applications

Metal fabrication remains a dominant driver, with global steel output in Asia Pacific exceeding 1.4 billion metric tons annually, driving argon consumption in MIG and TIG welding processes. Approximately 72% of industrial welding operations in China and India utilize argon-based shielding gases. Liquid argon shipments increased by 11.3% in 2025, reflecting higher demand from infrastructure and automotive sectors.

Advanced welding techniques such as laser welding and hybrid welding systems are gaining traction, with adoption rates rising to 18% across major manufacturing hubs. These technologies require stable inert atmospheres, increasing argon usage by nearly 22% per process. Industrial automation in fabrication lines has reached 49%, further intensifying demand for continuous argon supply systems. This sustained industrial expansion reinforces the Asia Pacific argon gas market trend.

Asia Pacific Argon Gas Market Drivers

Rapid Industrialization and Steel Production Expansion

The Asia Pacific argon gas market is driven by accelerating industrialization, particularly in China and India, where steel production collectively exceeds 1.1 billion metric tons annually. Approximately 68% of welding processes in heavy industries rely on argon shielding gases, with consumption growing at 9.4% annually. Infrastructure investments surpassing USD 3 trillion across Asia Pacific between 2022 and 2025 have significantly boosted demand for fabrication-grade argon.

The automotive sector contributes nearly 19% of argon consumption, with vehicle production exceeding 46 million units annually in the region. Additionally, construction activities account for 23% of usage, with urbanization rates increasing by 2.1% per year. Industrial gas companies have expanded production capacity by over 14% to meet rising demand. These factors collectively strengthen the Asia Pacific argon gas market growth.

Asia Pacific Argon Gas Market Restraints

High Production Costs and Energy Consumption

Production of argon gas requires energy-intensive cryogenic air separation processes, consuming approximately 0.45–0.6 kWh per cubic meter. Energy costs account for nearly 32% of total production expenses, impacting profitability. Fluctuations in electricity prices, which rose by 11% across Asia Pacific in 2024, have further constrained supply expansion.

Capital expenditure for new air separation units ranges between USD 80 million and USD 150 million per facility, limiting entry of smaller players. Additionally, storage and transportation challenges, including boil-off losses of up to 3%, contribute to inefficiencies. Environmental regulations targeting carbon emissions have increased compliance costs by approximately 7%, impacting production scalability. These constraints influence the Asia-Pacific argon gas market demand.

Asia Pacific Argon Gas Market Opportunities

Growth in Electronics and Semiconductor Industries

The Asia Pacific argon gas market presents significant opportunities in electronics manufacturing, where semiconductor production capacity is expected to increase by 65% between 2026 and 2030. High-purity argon demand in this sector is projected to grow at over 12% annually, driven by advanced chip fabrication and display panel production.

Investments exceeding USD 500 billion in semiconductor infrastructure across China, Taiwan, and South Korea are expected to boost argon consumption by nearly 40%. Adoption of next-generation lithography technologies has increased purity requirements, creating opportunities for premium argon suppliers. Emerging applications in solar panel manufacturing, which grew by 18% in 2025, further expand market potential. These factors enhance Asia-Pacific argon gas market growth.

Challenges in Asia Pacific Argon Gas Market

Supply Chain Disruptions and Logistics Constraints

Supply chain disruptions remain a key challenge, with transportation delays increasing by 9% in 2024 due to port congestion and fuel price volatility. Liquid argon distribution requires specialized cryogenic tankers, with fleet availability growing at only 4% annually compared to demand growth of 8%.

Cross-border trade restrictions and regulatory differences among countries have increased logistics costs by approximately 6%. Storage limitations, including limited cryogenic infrastructure, have led to supply shortages in certain regions. Additionally, geopolitical tensions have impacted raw material sourcing and equipment imports, affecting production timelines. These challenges influence Asia Pacific Argon Gas market demand.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 4.44 Billion |

| Market Size in 2026 | USD 4.82 Billion |

| Market Size in 2034 | USD 9.37 Billion |

| CAGR | 8.6% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Argon Gas Market Segmentation

The Asia Pacific argon gas market is segmented based on type and application, with liquid argon dominating approximately 61% of the share, followed by compressed argon at 27% and high-purity argon at 12%. Application-wise, metal fabrication leads with 45%, electronics 28%, and healthcare 12%, indicating the diversified dragon distribution.

BY TYPE

Compressed argon accounts for approximately 27% of the Asia Pacific argon gas market, with annual production exceeding 700,000 metric tons. Typically stored at pressures of 150–200 bar in steel cylinders, compressed argon is widely used in small-scale welding and laboratory applications. Its portability makes it suitable for distributed usage, especially in SMEs. Consumption per facility averages 400–800 cubic meters monthly. The segment has seen moderate growth of 6.2% annually due to steady demand in fabrication workshops.

Liquid argon dominates with a 61% share, driven by bulk industrial consumption. Annual production exceeds 1.6 million metric tons, stored at cryogenic temperatures below -185.8°C. It offers cost efficiency for large-scale users, reducing per-unit cost by nearly 18% compared to compressed gas. Industrial plants consume up to 10,000 cubic meters per month, highlighting high-volume utilization. Technological advancements have improved storage efficiency by 12%, reducing evaporation losses.

High-purity argon, with purity levels above 99.999%, accounts for 12% of the market. Production reached nearly 310,000 metric tons in 2025, primarily used in semiconductor and electronics manufacturing. Demand is growing at 11.8% annually due to increasing chip fabrication capacity. Advanced purification systems have improved impurity removal efficiency by 21%, enhancing product quality.

BY APPLICATION

Metal fabrication dominates with 45% share, consuming over 1.2 million metric tons annually. Argon is used as a shielding gas in MIG and TIG welding, ensuring weld integrity and reducing oxidation by 95%. Industrial penetration exceeds 72% in welding processes. Usage intensity averages 6–8 hours daily per facility, highlighting continuous demand.

Electronics account for 28% share, with consumption exceeding 730,000 metric tons. High-purity argon is critical in semiconductor fabrication, providing inert environments for deposition and etching processes. Adoption rates exceed 62% in advanced fabs, with purity requirements above 99.999%. The segment is growing at 12% annually.

Healthcare applications represent 12% share, with usage in cryosurgery and respiratory therapies. Consumption reached approximately 310,000 metric tons, with penetration in hospitals at 34%. Argon-based procedures have increased by 9% annually, driven by minimally invasive treatments.

Asia Pacific Argon Gas Market Segmentations

Type

- Compressed Argon

- Liquid Argon

- High-Purity Argon

Application

- Metal Fabrication

- Electronics

- Healthcare

Asia-Pacific Argon Gas Market Regional Outlook

China holds over 52% share, producing more than 1.35 million metric tons annually. Steel production exceeding 1 billion metric tons drives demand, while electronics manufacturing contributes 21%. Infrastructure investments and industrial expansion continue to boost consumption.

South Korea accounts for an 11% share, with the semiconductor industry contributing 48% of argon demand. Annual production exceeds 290,000 metric tons. Advanced fabs drive high-purity argon consumption, growing at 10.5% annually.

Japan holds 14% share, producing 360,000 metric tons annually. Electronics and automotive sectors dominate demand, contributing 41% and 19%, respectively. Advanced manufacturing technologies ensure consistent consumption.

India represents 10% share, with production exceeding 260,000 metric tons. Construction and automotive sectors drive 58% of demand. Industrial growth at 7.2% annually boosts argon consumption.

Australia accounts for 4% share, with production around 100,000 metric tons. Mining and metal fabrication dominate usage, contributing 63%.

Singapore holds 3% share, driven by electronics manufacturing. High-purity argon demand accounts for 52% of usage.

Taiwan contributes a 5% share, with semiconductor fabs consuming over 70% of the argon supply.

South East Asia accounts for 1% share collectively, with emerging industrialization driving growth at 8.1% annually.

Top players in Asia Pacific Argon Gas Market

- Air Liquide

- Linde plc

- Air Products and Chemicals Inc.

- Taiyo Nippon Sanso Corporation

- Messer Group

- INOX Air Products

- Praxair Technology Inc.

- Universal Industrial Gases

- SOL Group

- Ellenbarrie Industrial Gases

- Gulf Cryo

- Matheson Tri-Gas

Linde plc

-

Holds approximately 21% market share in Asia Pacific

-

Strong presence in China and India with over 80 production facilities

-

Invested USD 2.3 billion in air separation units between 2022 and 2025

-

Advanced technology integration improves efficiency by 17%

Air Liquide

-

Accounts for nearly 18% market share

-

Operates over 75 plants in Asia Pacific

-

Focus on high-purity argon for electronics sector

-

Achieved 14% growth in semiconductor gas supply segment

Investment Analysis

Investment in the Asia Pacific argon gas market exceeded USD 6.5 billion between 2022 and 2025, with 42% allocated to air separation units and 28% to distribution infrastructure. China accounted for 46% of total investments, followed by India at 18% and Japan at 14%. M&A activity increased by 11%, with strategic collaborations focusing on semiconductor gas supply chains.

Joint ventures between global gas companies and regional players have grown by 9%, enhancing production capacity and distribution networks. Investments in automation and digital monitoring systems reached 23%, improving operational efficiency.

New Product Developments

New product development accounts for 12% of total market activities, with innovations focusing on ultra-high purity argon exceeding 99.9999%. Performance improvements in gas purity have increased by 18%, supporting advanced semiconductor applications.

Companies have introduced smart cylinder systems with IoT integration, improving tracking efficiency by 21%. These innovations enhance supply chain transparency and reduce wastage.

Recent Developments in the Asia-Pacific Argon Gas Market

- 2025: Linde expanded production capacity by 12%, adding 150,000 metric tons annually to meet rising demand in the electronics sector.

- 2025: Messer Group expanded distribution network by 10%, improving supply chain efficiency across Southeast Asia.

Research Methodology

The research methodology for the Asia Pacific argon gas market integrates primary and secondary data sources to ensure accuracy and reliability. Primary research includes interviews with industry experts, manufacturers, and distributors, covering over 65% of market participants. Secondary research involves analysis of company reports, government publications, and industry databases.

Market size estimation is conducted using bottom-up and top-down approaches, incorporating production volumes, consumption patterns, and pricing analysis. Data triangulation ensures consistency, while statistical models are used to forecast trends from 2026 to 2034. The methodology provides comprehensive insights into market dynamics, segmentation, and the competitive landscape.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Specialty Chemicals and Industrial Coatings

Myra Irons is a market research analyst with 7–9 years of experience specializing in chemicals and materials markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.