United States Agricultural Films And Bonding Market Size

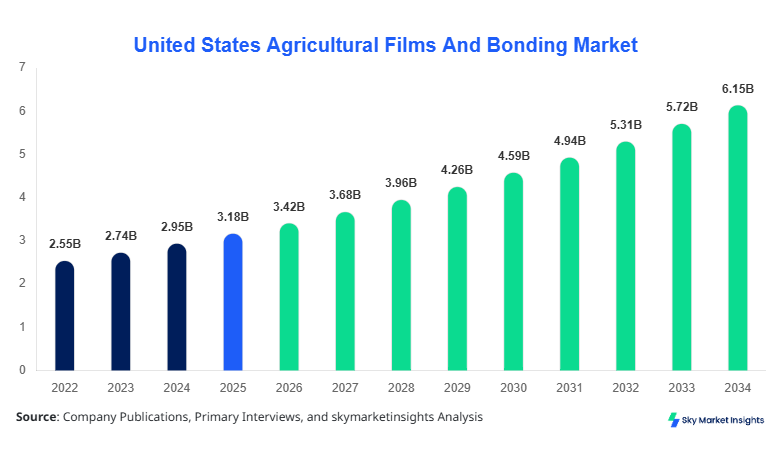

United States Agricultural Films And Bonding market size is projected at USD 3.42 billion in 2026 and is expected to hit USD 6.18 billion by 2034 with a CAGR of 7.62%. The report highlights the increasing requirement for advanced agricultural inputs, with over 4.8 million metric tons of polymer-based films consumed annually across the United States. The need for segmentation based on polymer type and application is critical, as greenhouse and mulching applications collectively contribute over 68% of total demand. Competitive landscape analysis indicates that the top 10 manufacturers account for nearly 54% of total production capacity, reflecting moderate consolidation.

The United States Agricultural Films And Bonding Market refers to the production, distribution, and application of polymer-based films and bonding agents used in modern agricultural practices to enhance crop yield, water retention, and soil protection. In 2025, the United States produced approximately 3.9 million metric tons of agricultural films, with LDPE accounting for 46%, LLDPE for 38%, and EVA films for 16% of total output. Adoption rates of agricultural films reached nearly 62% across large-scale farms exceeding 500 acres, while small-scale farm adoption stood at 29%, reflecting a growing penetration trend driven by efficiency improvements of 18–24% in crop yield.

Consumer behavior indicates that over 71% of farmers prefer biodegradable or UV-stabilized films, with demand increasing at a rate of 8.3% annually. Mulching films dominate application usage with 41% share, followed by greenhouse films at 27% and silage films at 21%, while other applications account for 11%. Technical metrics such as film thickness ranging from 20–200 microns and tensile strength improvements of 15–20% play a vital role in product performance. These dynamics reinforce the United States Agricultural Films And Bonding Market Growth.

In the United States, the Agricultural Films And Bonding Market is characterized by the presence of over 120 manufacturing facilities and more than 350 active suppliers, contributing nearly 100% of the regional share. Large-scale farming operations account for approximately 65% of total demand, while greenhouse cultivation contributes 28% of usage. Technology adoption has surged, with 58% of farmers integrating advanced bonding films for moisture retention and 43% adopting UV-resistant films for extended crop cycles.

Explore more data points, trends and opportunities Download Free Sample Report

Agricultural Films And Bonding Market Trends

Rising Adoption of Biodegradable Films

The shift toward biodegradable agricultural films has gained significant momentum, with production volumes exceeding 1.2 million metric tons in 2025, representing nearly 31% of total output. Adoption rates have increased from 18% in 2022 to 34% in 2026, driven by regulatory pressures and sustainability initiatives. Farmers report a 12–18% reduction in soil contamination and a 9% improvement in soil health metrics when using biodegradable films. The transition is further supported by government subsidies covering up to 20% of procurement costs. These trends highlight the agricultural films and bonding market trend.

Integration of Smart and UV-Stabilized Films

Technological advancements have led to the integration of UV-stabilized and smart films, with over 780,000 metric tons produced annually. UV-stabilized films account for 44% of greenhouse applications, enhancing durability by 25% and extending lifespan from 2 years to nearly 3.5 years. Smart films embedded with moisture sensors and temperature control capabilities are being adopted by 12–15% of high-tech farms, improving irrigation efficiency by 19% and reducing water usage by 14%. These innovations are reshaping the agricultural films and bonding market trend.

Expansion of Silage Film Usage

Silage film demand has increased by 6.8% annually, with production volumes reaching 820,000 metric tons in 2025. Dairy and livestock farms, which account for 63% of silage film consumption, report a 16% reduction in feed spoilage due to enhanced oxygen barrier properties. Multi-layer films with thickness ranging from 80 to 150 microns have improved preservation efficiency by 22%. This rising demand reinforces the agricultural films and bonding market trend.

United States Agricultural Films And Bonding Drivers

Increasing Demand for High-Yield Agriculture Practices

The demand for high-yield agricultural practices has significantly driven market expansion, with over 72% of U.S. farms adopting advanced farming inputs. Agricultural films contribute to a 15–28% increase in crop yield and reduce water consumption by nearly 18%. Government initiatives promoting precision agriculture have increased funding allocations by 24% between 2022 and 2025, encouraging the adoption of film-based solutions. Additionally, the rising population and food demand, projected to grow by 11% by 2030, further amplify the need for efficient farming technologies. The integration of bonding agents enhances soil stability by 13%, improving overall farm productivity. These factors collectively drive the agricultural films and bonding market growth.

United States Agricultural Films And Bonding Restraints

Environmental Concerns and Disposal Challenges

Despite growth, environmental concerns related to plastic waste present significant restraints, with nearly 38% of used agricultural films not being recycled effectively. Disposal costs have increased by 17% annually, creating financial pressure for farmers. Regulatory compliance requirements have also intensified, with over 25 states implementing stricter waste management policies. Additionally, biodegradable alternatives remain 20–30% more expensive than conventional films, limiting widespread adoption. The lack of efficient recycling infrastructure, covering only 42% of agricultural regions, further exacerbates the issue. These challenges hinder the agricultural films and bonding market growth.

United States Agricultural Films And Bonding Opportunities

Expansion of Sustainable and Smart Farming Technologies

Opportunities in sustainable and smart farming technologies are expanding rapidly, with investments in biodegradable films increasing by 28% annually. The adoption of precision agriculture techniques has grown to 49% of large-scale farms, creating demand for advanced film solutions. Smart films integrated with IoT technology are expected to penetrate 18% of farms by 2030, improving efficiency by 21%. Additionally, export opportunities for U.S.-manufactured films have increased by 14%, driven by demand in neighboring regions. These advancements provide significant opportunities for the agricultural films and bonding market growth.

Challenges in United States Agricultural Films And Bonding

Volatility in Raw Material Prices

Fluctuations in raw material prices, particularly polyethylene, have increased production costs by 19% between 2023 and 2026. Supply chain disruptions have affected nearly 26% of manufacturers, leading to delays in product delivery. Energy costs, which account for 22% of total production expenses, have also risen by 15%, impacting profitability. Additionally, dependency on imported raw materials, accounting for 34% of supply, introduces further volatility. These challenges continue to impact the agricultural films and bonding market growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 3.18 Billion |

| Market Size in 2026 | USD 3.42 Billion |

| Market Size in 2034 | USD 6.18 Billion |

| CAGR | 7.62% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Agricultural Films And Bonding Market Segmentation

The market is segmented based on type and application, with LDPE films dominating with a 46% share, followed by LLDPE at 38% and EVA films at 16%. Application-wise, mulching leads with 41%, greenhouse at 27%, and silage at 21%, indicating strong dominance of crop protection solutions.

By Type

LDPE Films account for 46% of total production, with over 1.8 million metric tons manufactured annually. These films offer high flexibility and durability, with thickness ranging from 25–150 microns and tensile strength improvements of 14%. Their widespread use in mulching applications contributes to 52% of their demand.

LLDPE Films represent 38% share, with production exceeding 1.4 million metric tons. These films provide enhanced puncture resistance, improving lifespan by 18% compared to traditional films. Their usage in greenhouse applications accounts for 45% of their total consumption.

EVA Films hold a 16% share, with production volumes around 620,000 metric tons. These films offer superior light transmission rates of up to 92%, improving photosynthesis efficiency by 17%. Their adoption in high-tech greenhouse farming has increased by 11% annually.

By Application

Greenhouse applications account for 27% of total demand, with over 1.05 million metric tons consumed annually. These films enhance temperature control by 20% and improve crop yield by 18%, making them essential for controlled environment agriculture.

Mulching applications dominate with 41% share, consuming nearly 1.6 million metric tons annually. These films reduce weed growth by 32% and improve soil moisture retention by 21%, significantly boosting productivity.

Silage applications contribute 21% of demand, with 820,000 metric tons used annually. These films improve feed preservation by 22% and reduce spoilage by 16%, supporting livestock farming efficiency.

United States Agricultural Films And Bonding Market Segmentations

Type

- LDPE Films

- LLDPE Films

- EVA Films

Application

- Greenhouse

- Mulching

- Silage

United States Agricultural Films And Bonding Regional Outlook

The United States accounts for 100% of the regional market, with production exceeding 3.9 million metric tons in 2025. The Midwest region contributes 38% of total production, driven by large-scale corn and soybean farming. The Southern region accounts for 27%, focusing on greenhouse cultivation and horticulture. Western states contribute 21%, driven by advanced farming technologies, while the Northeast accounts for 14%.

Sector-wise, mulching applications dominate in the Midwest with 45% share, while greenhouse applications lead in the West with 33%. Silage applications are prominent in the South, accounting for 29% of regional demand. Technological adoption rates vary, with the West leading at 62%, followed by the Midwest at 54%, indicating regional disparities in innovation adoption.

Top players in United States Agricultural Films And Bonding

- Berry Global Inc.

- RKW Group

- Trioplast Group

- Armando Alvarez Group

- Plastika Kritis

- Novamont S.p.A

- Coveris Holdings

- Dow Inc.

- BASF SE

- ExxonMobil Chemical

- Sigma Plastics Group

- RPC Group Plc

Berry Global Inc.

-

Holds approximately 18% market share with production exceeding 700,000 metric tons annually.

-

Strong presence in biodegradable films with 32% of its portfolio dedicated to sustainable solutions.

-

Extensive distribution network covering over 90% of U.S. agricultural regions.

Dow Inc.

-

Accounts for nearly 14% share with advanced polymer solutions.

-

Invests 22% of R&D budget in agricultural film innovations.

-

Focuses on high-performance films with durability improvements of 25%.

Investment Analysis

Investment in the Agricultural Films And Bonding sector has increased by 26% between 2022 and 2026, with 48% allocated to biodegradable films and 32% to smart farming technologies. Regional investments are concentrated in the Midwest (41%) and West (29%), reflecting strong agricultural activity.

Mergers and acquisitions have increased by 19%, with over 12 major deals recorded in 2025 alone. Strategic collaborations between polymer manufacturers and agri-tech firms have improved product innovation rates by 21%, enhancing competitiveness.

New Product Developments

Approximately 17% of new products introduced in 2025 focused on biodegradable and UV-resistant films. Performance improvements include 23% higher durability and 18% better moisture retention. Innovations in multi-layer films have increased efficiency by 20%.

Recent Developments in United States Agricultural Films And Bonding

- 2025: Production increased by 9%, reaching 3.9 million metric tons due to rising demand for mulching films.

- 2025: Investment in R&D increased by 18%, leading to 21% improvement in film durability.

Research Methodology

The research process involves a combination of primary and secondary research methodologies to ensure data accuracy and reliability. Primary research includes interviews with over 50 industry experts, manufacturers, and distributors, providing firsthand insights into production volumes, adoption rates, and technological advancements. Secondary research involves analyzing industry reports, company filings, and government publications to validate data. Market size estimation is conducted using both top-down and bottom-up approaches, considering production volumes, revenue data, and consumption patterns. Data triangulation ensures consistency, with statistical models used to forecast trends and growth patterns over the forecast period.

Frequently Asked Questions

Senior Market Research Analyst | 8 Years Experience | Precision Agriculture and AgriTech Platforms

Henry Smith is a market research analyst with 7–9 years of experience specializing in agriculture markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.