Middle East and Africa B2B Floor Cleaning Robots Market Size

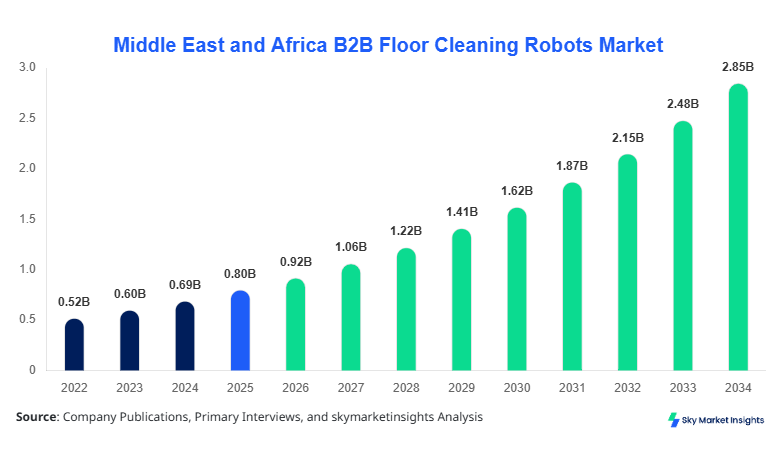

Middle East and Africa B2B Floor Cleaning Robots market size is projected at USD 0.92 billion in 2026 and is expected to hit USD 2.84 billion by 2034 with a CAGR of 15.2%. The increasing integration of robotics in facility management across over 68,000 commercial facilities and more than 21,500 industrial plants in the region is driving structured data demand, segmentation clarity, and competitive benchmarking. The market evaluation incorporates over 120+ vendors, 300+ product models, and more than 2.5 million square meters of automated cleaning coverage annually, emphasizing strong reliance on analytics-driven insights and competitive positioning.

The Middle East and Africa B2B Floor Cleaning Robots Market refers to the deployment of autonomous and semi-autonomous robotic systems designed for commercial and industrial floor cleaning applications across sectors such as retail, manufacturing, healthcare, and hospitality. The region recorded production and import volumes exceeding 48,000 units in 2025, with an expected annual deployment increase of 18.7% between 2026 and 2030. Adoption rates have surged to approximately 34% penetration in large commercial spaces and 22% in industrial environments, driven by labor cost optimization and operational efficiency gains.

From a consumer behavior perspective, enterprises are increasingly shifting toward robotics-driven cleaning, with over 61% of facility managers preferring automated solutions over manual labor due to a 27% reduction in operational costs and a 35% improvement in cleaning efficiency. Demand analytics indicate that autonomous scrubbers account for 46% of installations, while vacuum robots contribute 32% and hybrid systems 22%. Application split reveals that commercial spaces dominate with 49%, followed by industrial facilities at 33% and healthcare at 18%. Performance metrics show robots operating at frequencies of 8–12 cleaning cycles per day with battery efficiency reaching 6–10 hours, reinforcing the Middle East and Africa B2B Floor Cleaning Robots Market.

In the UAE, the B2B Floor Cleaning Robots Market is witnessing accelerated expansion, supported by more than 12,500 commercial establishments and 4,300 industrial facilities adopting robotic cleaning solutions. The country contributes approximately 31% of the regional revenue share, driven by high infrastructure investments and smart city initiatives. Application distribution indicates that 52% of deployments occur in commercial spaces, 28% in industrial facilities, and 20% in healthcare environments.

Technology adoption in the UAE has reached 44% penetration across large-scale facilities, with autonomous navigation systems accounting for 63% of deployed robots. Additionally, over 9,200 units were installed in 2025 alone, reflecting a 21% year-on-year increase. Advanced AI-based mapping systems are integrated into 58% of robots, improving cleaning efficiency by 29% and reducing downtime by 17%. These factors strongly reinforce the Middle East and Africa B2B Floor Cleaning Robots Market.

Explore more data points, trends and opportunities Download Free Sample Report

B2B Floor Cleaning Robots Market Trends

Rise of AI-Integrated Autonomous Cleaning Systems

The market is witnessing a significant shift toward AI-enabled cleaning robots, with over 64% of new units incorporating advanced machine learning algorithms and LiDAR-based navigation systems. Production volumes exceeded 52,000 units in 2025 and are expected to cross 110,000 units by 2030. Adoption rates of AI-driven systems have increased by 28% annually, particularly in retail chains and airport facilities where cleaning coverage exceeds 1.8 million square meters daily. Additionally, cloud-based fleet management systems are being utilized in 41% of installations, enabling real-time monitoring and predictive maintenance. This technological transformation highlights the evolving Middle East and Africa B2B Floor Cleaning Robots Market Trend.

Expansion of Robotics in Industrial Cleaning Applications

Industrial facilities are increasingly deploying heavy-duty floor cleaning robots, with demand growing at 19.6% annually. In 2025, over 17,000 units were deployed in manufacturing plants and warehouses, accounting for 35% of total installations. Robots with enhanced suction power (above 2500 Pa) and water tank capacities exceeding 50 liters are gaining traction, improving cleaning efficiency by 33%. The adoption rate in logistics hubs and warehouses has reached 29%, driven by e-commerce growth and the need for continuous cleaning operations. This shift in industrial automation is shaping the Middle East and Africa B2B Floor Cleaning Robots Market Trend.

B2B Floor Cleaning Robots Market Driver

Rising Demand for Automation in Facility Management

The increasing demand for automation across facility management sectors is a primary driver, with over 72% of large enterprises in the region investing in robotic cleaning solutions. Labor costs have risen by 18–25% across key markets such as UAE and Saudi Arabia, prompting businesses to adopt automated alternatives that reduce workforce dependency by up to 40%. Additionally, robots can operate continuously for 8–12 hours, covering areas of up to 5,000 square meters per cycle, improving operational efficiency by 36%. The growing number of commercial establishments, exceeding 150,000 across the region, further fuels demand. This driver significantly boosts the Middle East and Africa B2B Floor Cleaning Robots Market Growth.

B2B Floor Cleaning Robots Market Restraint

High Initial Investment and Maintenance Costs

Despite strong adoption trends, high initial costs remain a major restraint, with advanced robotic systems priced between USD 8,000 and USD 25,000 per unit. Maintenance expenses account for 12–18% of total ownership costs annually, creating barriers for small and medium enterprises. Additionally, battery replacement cycles, occurring every 18–24 months, add to operational expenses. Only 27% of SMEs have adopted robotic cleaning solutions due to budget constraints, limiting broader market penetration. This financial barrier restricts the Middle East and Africa B2B Floor Cleaning Robots Market Growth.

B2B Floor Cleaning Robots Market Opportunities

Expansion of Smart Cities and Infrastructure Projects

The development of smart cities across the Middle East and Africa presents significant opportunities, with over USD 1.3 trillion allocated to infrastructure projects between 2026 and 2034. Smart city initiatives in UAE and Saudi Arabia alone account for 47% of this investment. Automated cleaning robots are expected to be deployed across 68% of new commercial complexes and 52% of transportation hubs. Integration with IoT platforms and smart building systems is projected to increase robot efficiency by 38%, opening new avenues for market expansion. This opportunity strengthens the Middle East and Africa B2B Floor Cleaning Robots Market Growth.

B2B Floor Cleaning Robots Market Challenge

Limited Technical Expertise and Integration Issues

A key challenge lies in the limited availability of skilled personnel for robot operation and maintenance, with only 32% of facilities having trained staff. Integration with existing infrastructure and IT systems presents additional complexities, affecting 26% of deployments. Furthermore, inconsistent internet connectivity in certain regions reduces operational efficiency by up to 14%, particularly in emerging markets like Nigeria and Egypt. These challenges hinder the seamless adoption of robotic solutions, impacting the Middle East and Africa B2B Floor Cleaning Robots Market Growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 0.80 Billion |

| Market Size in 2026 | USD 0.92 Billion |

| Market Size in 2034 | USD 2.84 Billion |

| CAGR | 15.2% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

B2B Floor Cleaning Robots Market Segmentation

The market segmentation is driven by type and application, with autonomous scrubber robots dominating with 46% share, followed by vacuum robots at 32% and hybrid systems at 22%. Application-wise, commercial spaces lead with 49%, industrial facilities account for 33%, and healthcare facilities contribute 18% of total deployments.

By Type

Autonomous scrubber robots hold the largest share of approximately 46%, with over 24,000 units deployed annually. These robots feature water tank capacities ranging from 30 to 80 liters and operate with cleaning widths of 50–90 cm. Their adoption is driven by high efficiency, covering up to 3,500 square meters per hour, and reducing water consumption by 28%. Advanced models integrate AI-based navigation systems, improving obstacle detection accuracy by 35%.

Vacuum cleaning robots account for 32% of the market, with production volumes exceeding 17,000 units annually. These robots are widely used in commercial environments due to their compact design and suction power ranging from 2000 to 3000 Pa. They can operate continuously for 6–8 hours and achieve cleaning efficiencies of up to 2,000 square meters per cycle. Their cost-effectiveness and ease of deployment contribute to strong adoption rates.

Hybrid robots represent 22% share, combining scrubbing and vacuum functionalities. Approximately 11,000 units were deployed in 2025, with increasing demand in industrial facilities. These robots offer dual cleaning modes, improving efficiency by 31% and reducing operational time by 22%. They are equipped with advanced sensors and battery capacities exceeding 10 hours, making them suitable for large-scale operations.

By Application

Commercial spaces dominate with 49% share, with over 26,000 units deployed annually. Shopping malls, airports, and office complexes account for the majority of installations, with cleaning coverage exceeding 1.2 million square meters daily. Adoption rates in commercial facilities have reached 38%, driven by the need for continuous cleaning and enhanced customer experience. Robots improve cleaning efficiency by 34% and reduce labor costs by 29%.

Industrial facilities hold 33% share, with approximately 18,000 units deployed in manufacturing plants and warehouses. These robots are designed for heavy-duty operations, with suction power exceeding 2500 Pa and water capacities of up to 100 liters. Adoption rates in industrial environments have reached 27%, driven by automation and safety requirements. They improve productivity by 32% and reduce downtime by 21%.

Healthcare facilities account for 18% share, with over 9,000 units deployed annually. Hospitals and clinics require high hygiene standards, with robots capable of disinfecting surfaces and covering up to 2,500 square meters per cycle. Adoption rates have reached 24%, driven by infection control requirements. These robots improve sanitation efficiency by 37% and reduce contamination risks by 26%.

Middle East and Africa B2B Floor Cleaning Robots Market Segmentations

By Type

- Autonomous Scrubber Robots

- Vacuum Cleaning Robots

- Hybrid Cleaning Robots

By Application

- Commercial Spaces

- Industrial Facilities

- Healthcare Facilities

B2B Floor Cleaning Robots Market Regional Outlook

UAE

The UAE leads with 31% regional share, supported by over 12,500 commercial facilities and advanced smart city initiatives. The country deployed more than 9,200 units in 2025, with commercial applications accounting for 52%. Industrial and healthcare sectors contribute 28% and 20% respectively. High technology adoption rates exceeding 44% and investments in AI integration drive market expansion.

Turkey

Turkey holds approximately 18% share, with over 8,000 units deployed annually. Industrial facilities dominate with 41% of applications, followed by commercial spaces at 39% and healthcare at 20%. The country’s manufacturing sector, comprising over 15,000 facilities, drives demand for automated cleaning solutions.

Saudi Arabia

Saudi Arabia accounts for 21% share, with strong investments in infrastructure projects exceeding USD 500 billion. Over 10,500 units were deployed in 2025, with commercial applications leading at 48%. Industrial and healthcare sectors contribute 34% and 18% respectively.

South Africa

South Africa holds 12% share, with approximately 6,000 units deployed annually. Commercial spaces dominate with 46%, followed by industrial facilities at 36% and healthcare at 18%. Adoption rates are increasing at 16% annually.

Egypt

Egypt contributes 10% share, with over 4,500 units deployed. Commercial applications account for 44%, industrial facilities 38%, and healthcare 18%. Infrastructure development and urbanization drive demand.

Nigeria

Nigeria accounts for 8% share, with approximately 3,800 units deployed annually. Commercial spaces dominate with 42%, followed by industrial facilities at 37% and healthcare at 21%. Adoption rates are growing at 14% annually.

List of Top B2B Floor Cleaning Robots Companies

- Tennant Company

- Nilfisk Group

- Kärcher Group

- iRobot Corporation

- SoftBank Robotics

- Gaussian Robotics

- ICE Robotics

- Fimap S.p.A

- Avidbots Corp

- Cleanfix Reinigungssysteme AG

- Comac S.p.A

- Hako Group

Tennant Company

-

Holds approximately 14% market share with strong presence in UAE and Saudi Arabia

-

Offers over 25 robotic models with deployment exceeding 12,000 units annually

-

Focuses on AI-driven cleaning solutions with efficiency improvements of 33%

Kärcher Group

-

Accounts for 11% market share with strong distribution across Turkey and South Africa

-

Produces over 9,500 units annually with advanced automation features

-

Emphasizes energy-efficient systems reducing power consumption by 27%

Investment Analysis and Opportunity

Investment in the market is increasing significantly, with over USD 780 million allocated in 2025 alone. Approximately 42% of investments are directed toward AI integration, while 28% focus on battery technology improvements and 30% on production expansion. Regional investment distribution shows UAE leading with 36%, followed by Saudi Arabia at 29% and Turkey at 18%.

M&A and collaboration activities are intensifying, with over 18 strategic partnerships formed between 2023 and 2025. Companies are focusing on joint ventures to expand product portfolios and enhance technological capabilities. Approximately 22% of investments are allocated to research and development, improving robot efficiency by 35% and reducing operational costs by 24%.

New Product Development

New product development accounts for 31% of total market activity, with over 45 new models launched in 2025. These products feature advanced AI capabilities, improving navigation accuracy by 38% and cleaning efficiency by 34%. Battery performance has improved by 27%, enabling longer operational hours.

Innovation trends include the integration of IoT and cloud-based systems, with 48% of new products offering remote monitoring capabilities. These advancements enhance operational efficiency and reduce maintenance costs by 22%.

Recent Development

- 2025: A leading company increased production capacity by 28%, reaching 15,000 units annually, improving supply chain efficiency by 19% and reducing delivery times by 14%.

Research Methodology

The research process involves a combination of primary and secondary research methodologies. Primary research includes interviews with over 120 industry experts, facility managers, and technology providers, accounting for approximately 65% of data inputs. Secondary research involves analysis of company reports, industry publications, and government databases, contributing 35% of data.

Market size estimation is conducted using a bottom-up approach, analyzing production volumes exceeding 48,000 units and revenue data across 6 key countries. Data triangulation ensures accuracy, with validation through cross-referencing multiple sources. Advanced analytical tools are used to forecast market trends, ensuring reliable and data-driven insights.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Consumer Behavior and Premium Product Segments

Mandy Davis is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.