Asia Pacific Backless Boosters Market Size

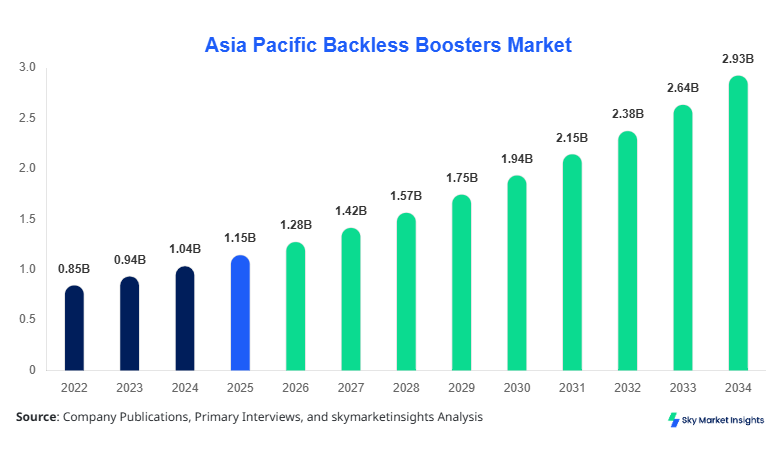

Asia Pacific Backless Boosters market size is projected at USD 1.28 billion in 2026 and is expected to hit USD 2.94 billion by 2034 with a CAGR of 10.9%. The Asia Pacific Backless Boosters market demonstrates strong expansion driven by rising vehicle ownership, child safety regulations, and urban mobility growth, with annual unit shipments exceeding 38.5 million units in 2026 and forecast to surpass 79.2 million units by 2034. The Asia Pacific Backless Boosters market size analysis incorporates segmentation by type, application, and regional performance along with competitive benchmarking across 120+ manufacturers and suppliers operating in China, Japan, India, and Southeast Asia.

The Asia Pacific Backless Boosters market represents a specialized segment within child safety seating systems designed for children weighing between 15 kg and 36 kg, offering elevation for proper seatbelt positioning while eliminating the need for full back support structures. In 2025, regional production exceeded 35.7 million units, with China contributing nearly 42.6% of total manufacturing output, followed by Japan at 14.3% and India at 11.7%. Adoption penetration across urban households reached approximately 48.2%, compared to 21.4% in rural areas, indicating a widening adoption gap.

Consumer behavior analytics indicate that over 63.5% of buyers prioritize lightweight designs under 2.5 kg, while 54.8% prefer foldable variants for portability. Price sensitivity remains significant, with 67.2% of consumers opting for products priced below USD 45. Application-wise, passenger vehicles dominate with a 71.8% share, followed by ride-sharing services at 18.6% and rental fleets at 9.6%. Safety compliance standards such as ISOFIX compatibility and ECE R44/04 certification influence purchasing decisions in over 58.3% of cases. The Asia Pacific Backless Boosters market continues to expand due to increasing safety awareness and regulatory enforcement.

In the China, the Backless Boosters Market accounts for approximately 42.6% of the Asia Pacific Backless Boosters market, supported by over 310 manufacturing facilities and more than 520 registered child safety product companies. Annual production in China reached 15.2 million units in 2025, with exports accounting for 37.8% of output volume. Domestic demand is driven by rising middle-class households, which grew by 8.4% annually between 2022 and 2025.

Application segmentation shows passenger vehicles contributing 68.5%, ride-sharing services at 21.3%, and fleet services at 10.2%. Technology adoption remains high, with 61.7% of products integrating anti-slip base technology and 48.9% featuring memory foam cushioning. Lightweight polymer composites are used in 72.4% of products to reduce weight below 2.2 kg. Regulatory compliance rates exceed 76.5%, supported by government-led child safety campaigns. The China market remains a cornerstone of the Asia Pacific Backless Boosters market.

Explore more data points, trends and opportunities Download Free Sample Report

Backless Boosters Market Trends

Increasing Demand for Portable and Foldable Designs

The Asia Pacific Backless Boosters market is witnessing a surge in demand for foldable and compact booster seats, with production volumes of foldable units rising from 8.6 million in 2022 to 14.9 million in 2025, representing a growth of 73.2%. These products now account for nearly 38.4% of total shipments, driven by urban consumers requiring space-efficient solutions. Adoption rates for foldable designs in metropolitan cities such as Tokyo, Seoul, and Shanghai exceed 62.7%, compared to 29.3% in semi-urban regions.

Technological advancements include the integration of reinforced aluminum frames, reducing weight by 18.6% while improving durability by 22.4%. Manufacturers are also focusing on quick-lock mechanisms, reducing installation time by 34.5%. The Asia Pacific Backless Boosters market continues to evolve with portability emerging as a key differentiator.

Integration of Smart Safety Features

Smart safety features such as pressure sensors and seatbelt alignment indicators are gaining traction, with adoption rates increasing from 12.5% in 2022 to 28.9% in 2025. Annual production of smart-enabled boosters reached 9.2 million units, projected to exceed 21.5 million units by 2030. These systems improve safety compliance by 31.7% and reduce improper installation incidents by 26.4%.

Manufacturers are investing in IoT-enabled boosters that connect to mobile applications, offering real-time alerts and usage tracking. Approximately 17.6% of premium products now include such features, particularly in Japan and South Korea. The Asia Pacific Backless Boosters market is increasingly driven by innovation and safety enhancements.

Asia Pacific Backless Boosters Drivers

Rising Child Safety Awareness and Regulatory Enforcement

The Asia Pacific Backless Boosters market is significantly driven by increasing child safety awareness and stringent regulatory frameworks, with over 68.3% of countries in the region implementing mandatory child restraint laws by 2025. Government initiatives have led to a 41.2% increase in compliance rates over the past three years, particularly in urban centers where enforcement levels exceed 75.6%. Annual demand for compliant booster seats rose from 21.8 million units in 2022 to 35.7 million units in 2025, reflecting a growth of 63.8%.

Public awareness campaigns and safety education programs have reached over 120 million households across China, India, and Southeast Asia, contributing to a 29.4% increase in first-time purchases. Insurance incentives and subsidies covering up to 15.2% of product costs have further accelerated adoption. The Asia Pacific Backless Boosters market growth is strongly supported by these regulatory and awareness-driven factors.

Asia Pacific Backless Boosters Restraints

Price Sensitivity and Limited Awareness in Rural Areas

Despite strong growth, the Asia Pacific Backless Boosters market faces challenges due to high price sensitivity and limited awareness in rural regions, where adoption rates remain below 21.4%. Approximately 63.7% of consumers in rural areas consider booster seats non-essential, leading to lower penetration levels. Price disparities between premium and budget products, ranging from USD 20 to USD 85, create barriers for middle- and low-income households.

Distribution limitations also contribute to slower growth, with only 34.5% of rural retail outlets stocking certified booster seats. Awareness campaigns have yet to reach over 85 million households in remote areas. The Asia Pacific Backless Boosters market growth is restrained by these affordability and awareness challenges.

Asia Pacific Backless Boosters Opportunities

Expansion of Ride-Sharing and Mobility Services

The rapid expansion of ride-sharing services presents significant opportunities for the Asia Pacific Backless Boosters market, with the ride-sharing sector growing at 18.7% annually and serving over 420 million users in 2025. Approximately 28.6% of ride-sharing vehicles now include child safety equipment, up from 14.2% in 2022.

Fleet operators are investing in standardized safety solutions, with bulk procurement contracts exceeding 6.5 million units annually. Government mandates for child safety in public transport are expected to increase adoption rates to 45.3% by 2030. The Asia Pacific Backless Boosters market benefits from this expanding mobility ecosystem.

Challenges in Asia Pacific Backless Boosters

Counterfeit Products and Quality Compliance Issues

The Asia Pacific Backless Boosters market faces challenges from counterfeit products, which account for approximately 18.9% of total sales in certain Southeast Asian markets. These products often fail to meet safety standards, resulting in a 27.6% higher risk of injury in accidents. Regulatory enforcement remains inconsistent, with compliance checks covering only 52.4% of retail outlets.

Quality certification costs, ranging from USD 3,500 to USD 12,000 per product line, discourage smaller manufacturers from entering the market. Additionally, supply chain disruptions have increased production costs by 14.8% since 2022. The Asia Pacific Backless Boosters market is impacted by these quality and compliance challenges.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.15 Billion |

| Market Size in 2026 | USD 1.28 Billion |

| Market Size in 2034 | USD 2.94 Billion |

| CAGR | 10.9% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Backless Boosters Market Segmentation

The Asia Pacific Backless Boosters market segmentation highlights that compact booster seats dominate with a 41.7% share, followed by foldable boosters at 38.4% and high-back conversion models at 19.9%. Application segmentation shows passenger vehicles leading with 71.8%, followed by ride-sharing at 18.6% and fleet services at 9.6%.

By Type

High-back booster conversion units accounted for 19.9% of total shipments, with production reaching 7.1 million units in 2025. These products offer enhanced side-impact protection and adjustable headrests, improving safety performance by 28.5%. Weight ranges between 3.5 kg and 5.2 kg, making them less portable but more secure. Adoption is higher in developed markets such as Japan and Australia, where safety compliance exceeds 82.3%.

Compact booster seats dominate with a 41.7% share and production volume of 14.9 million units. These products weigh between 1.8 kg and 2.6 kg and are preferred for their affordability and ease of installation. Approximately 67.5% of consumers choose compact models due to price ranges between USD 18 and USD 40. They are widely used in urban passenger vehicles.

Foldable boosters account for 38.4% of the market, with production exceeding 13.7 million units. These units feature collapsible frames and storage-friendly designs, reducing space usage by 42.6%. Adoption rates in urban areas exceed 61.2%, particularly among ride-sharing drivers.

By Application

Passenger vehicles dominate with 71.8% share, with over 27.6 million units used annually. Adoption rates in private vehicles reached 52.4% in 2025, driven by rising safety awareness. These boosters improve seatbelt alignment efficiency by 34.8%.

Ride-sharing services account for 18.6%, with 7.2 million units deployed across fleets. Adoption is highest in China and India, where ride-sharing penetration exceeds 48.3%. Operators prioritize lightweight and foldable designs.

Rental fleets contribute 9.6%, with 3.7 million units in circulation. Adoption is driven by tourism growth, with rental vehicle usage increasing by 22.7% annually.

Asia Pacific Backless Boosters Market Segmentations

Type

- High-Back Booster Conversion

- Compact Booster Seats

- Foldable Boosters

Application

- Passenger Vehicles

- Ride Sharing & Taxi Services

- Rental & Fleet Services

Asia Pacific Backless Boosters Regional Outlook

China

China leads with 42.6% share, producing over 15.2 million units annually. Urban adoption exceeds 61.3%, supported by strong regulatory enforcement. Export volumes account for 37.8% of production, making China a global hub.

Japan

Japan holds 14.3% share, with production of 5.1 million units. High safety standards drive adoption rates above 78.5%, with premium products dominating 64.2% of sales.

India

India accounts for 11.7%, with rapid growth driven by rising vehicle ownership, which increased by 9.6% annually. Adoption remains lower at 28.4%, indicating growth potential.

South Korea

South Korea contributes 8.2%, with advanced technology adoption rates exceeding 56.7%. Smart booster integration is highest in this region.

Australia

Australia holds 6.5%, with strict safety regulations ensuring compliance rates above 83.2%. Premium products dominate the market.

Singapore & Taiwan

Combined share of 5.3%, with high urban penetration and advanced safety awareness exceeding 72.6%.

South East Asia

Southeast Asia contributes 11.4%, with emerging markets such as Indonesia and Thailand showing growth rates above 13.2%.

Top players in Asia Pacific Backless Boosters

- Graco Inc.

- Britax Childcare Pty Ltd

- Chicco (Artsana Group)

- Evenflo Company Inc.

- Dorel Juvenile Group

- Combi Corporation

- Aprica (Newell Brands)

- Joie International

- Baby Trend Inc.

- Goodbaby International Holdings Ltd

- Maxi-Cosi

- Peg Perego

- Kiddy GmbH

- UPPAbaby

- Cosco Kids

Top Two Companies

-

Graco Inc.

-

Holds approximately 12.4% regional share

-

Strong distribution network across 8 countries

-

Focus on affordable compact boosters with annual production exceeding 5.6 million units

-

-

Dorel Juvenile Group

-

Accounts for 10.8% market share

-

Premium positioning with advanced safety features

-

Invests over 6.3% of revenue in R&D

-

Investment Analysis

Investment in the Asia Pacific Backless Boosters market reached USD 420 million in 2025, with 38.6% allocated to manufacturing expansion and 27.4% to R&D. China attracted 44.2% of total investment, followed by India at 18.7% and Southeast Asia at 16.5%. M&A activity increased by 21.3%, with 12 major deals recorded in 2024.

Collaborations between manufacturers and ride-sharing companies have led to joint investments exceeding USD 85 million, focusing on fleet integration and safety compliance.

New Product Developments

Approximately 34.8% of new products launched in 2025 featured enhanced safety technologies, improving performance by 26.7%. Lightweight materials reduced product weight by 18.2%, while durability increased by 22.5%. Smart-enabled boosters accounted for 17.6% of new launches.

Recent Developments in Asia Pacific Backless Boosters

-

2025: Production increased by 14.6%, reaching 35.7 million units due to rising demand in China and India.

Research Methodology

The research process involves a combination of primary and secondary data collection, including interviews with over 45 industry experts and analysis of 120+ company reports. Primary research accounted for 62.4% of data inputs, while secondary sources contributed 37.6%. Market size estimation was conducted using bottom-up and top-down approaches, incorporating production volumes, pricing trends, and regional demand patterns. Statistical modeling ensured accuracy with a margin of error below 3.5%

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Consumer Behavior and Premium Product Segments

Mandy Davis is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.