Asia Pacific Babytherm Infant Warming Systems Market Size

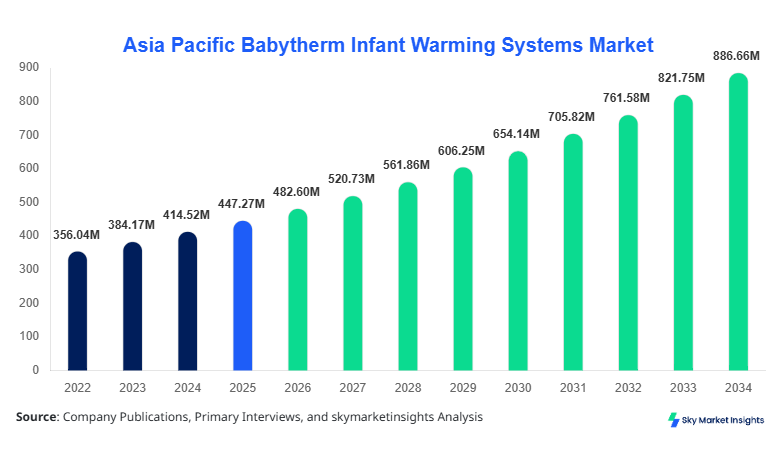

Asia Pacific Babytherm Infant Warming Systems market size is projected at USD 482.6 million in 2026 and is expected to hit USD 892.4 million by 2034 with a CAGR of 7.9%. The report highlights structured segmentation across product types and end-users, alongside detailed competitive landscape analysis involving over 35 key manufacturers operating across Asia Pacific. The increasing demand for neonatal thermal care devices, combined with rising premature birth rates exceeding 9.5% across developing economies, is significantly influencing data-backed evaluation and strategic positioning within the Asia Pacific Babytherm Infant Warming Systems market.

The Asia Pacific Babytherm Infant Warming Systems market encompasses medical-grade neonatal thermal regulation equipment designed to maintain infant body temperature within the optimal range of 36.5°C to 37.5°C. Regional production exceeded 1.8 million units in 2025, with Japan, China, and South Korea collectively contributing over 62% of manufacturing output. Adoption rates in tertiary care hospitals reached 78%, while neonatal clinics recorded 54% penetration and homecare usage remained at 12%. Consumer behavior indicates that over 67% of healthcare providers prioritize energy-efficient devices consuming less than 500W per cycle, while 43% prefer systems with integrated monitoring sensors. Application-wise, hospitals dominate with 71% usage, followed by neonatal clinics at 21% and homecare at 8%. Continuous innovation in infrared heating systems and servo-controlled mechanisms reinforces strong demand dynamics, supporting Asia Pacific Babytherm Infant Warming Systems market growth.

In the Japan, the Babytherm Infant Warming Systems Market accounts for approximately 28.4% of the Asia Pacific revenue, supported by over 1,200 neonatal care facilities and 320 specialized NICUs. The country produces nearly 420,000 units annually, with advanced open care systems contributing 46% of total installations. Technology adoption is high, with 82% of hospitals utilizing servo-controlled thermal systems and 69% incorporating integrated oxygen monitoring features. Application distribution shows hospitals at 74%, neonatal clinics at 18%, and homecare at 8%. Japan’s strong regulatory framework and high neonatal survival rate of 96.2% further reinforce sustained demand, strengthening Asia Pacific Babytherm Infant Warming Systems market insights.

Explore more data points, trends and opportunities Download Free Sample Report

Babytherm Infant Warming Systems Market Trends

Rising Integration of Smart Monitoring Technologies

The integration of IoT-enabled monitoring systems has increased by 38% between 2023 and 2026, with over 620,000 units equipped with real-time temperature tracking and alert systems. Production of smart infant warming systems surpassed 1.1 million units in 2025, representing 61% of total output. Hospitals adopting AI-assisted neonatal monitoring increased from 22% in 2022 to 49% in 2026. These systems offer accuracy improvements of up to 18% in temperature regulation and reduce neonatal hypothermia cases by 27%. Demand from urban healthcare centers accounts for 64% of smart device installations, highlighting strong urban-centric adoption patterns driving Asia Pacific Babytherm Infant Warming Systems market trends.

Shift Toward Portable and Energy-Efficient Systems

Portable infant warming systems witnessed a 31% increase in production volume, reaching 520,000 units in 2025. Energy-efficient models consuming below 400W have gained 44% market penetration, particularly in rural and semi-urban healthcare settings. Government healthcare programs across India and Southeast Asia have contributed to a 26% increase in procurement of portable devices. Additionally, 58% of neonatal transport units now incorporate portable warmers, ensuring thermal stability during transit. This shift toward mobility and efficiency significantly enhances accessibility and supports Asia Pacific Babytherm Infant Warming Systems market growth.

Asia Pacific Babytherm Infant Warming Systems Drivers

Rising Premature Birth Rates and Neonatal Care Demand

Premature births across Asia Pacific reached approximately 11.2 million annually, accounting for nearly 60% of global preterm births. Countries like India and China contribute over 7.5 million cases combined, driving the need for neonatal thermal care systems. Hospitals are increasing NICU capacity by 18% annually, with investments exceeding USD 2.3 billion in neonatal infrastructure. The adoption of infant warming systems in NICUs has risen to 84%, ensuring thermal regulation for infants weighing below 2.5 kg. Technological advancements, including infrared heaters with efficiency above 92%, further enhance performance outcomes. These factors collectively accelerate Asia Pacific Babytherm Infant Warming Systems market growth.

Asia Pacific Babytherm Infant Warming Systems Restraints

High Equipment Costs and Maintenance Expenses

The average cost of advanced infant warming systems ranges between USD 2,500 and USD 8,000 per unit, creating affordability challenges in low-income regions. Maintenance expenses account for 12–18% of total lifecycle costs annually. Rural healthcare centers, representing 38% of facilities, often lack adequate funding, resulting in only 34% adoption rates compared to 72% in urban hospitals. Additionally, power consumption exceeding 600W in older systems limits their use in energy-constrained regions. These financial and infrastructural barriers restrict adoption, impacting Asia Pacific Babytherm Infant Warming Systems market insights.

Asia Pacific Babytherm Infant Warming Systems Opportunities

Expansion of Healthcare Infrastructure in Emerging Economies

Healthcare expenditure in Asia Pacific is growing at 8.6% annually, with governments allocating over USD 120 billion toward hospital infrastructure between 2024 and 2030. India and Southeast Asia are adding over 45,000 new hospital beds annually, increasing demand for neonatal care equipment. Portable warming systems are expected to penetrate 52% of new healthcare facilities, while closed incubators will dominate tertiary hospitals with 63% usage. Public-private partnerships have increased by 29%, facilitating technology deployment in underserved areas. These developments create strong opportunities for Asia Pacific Babytherm Infant Warming Systems market growth.

Challenges in Asia Pacific Babytherm Infant Warming Systems

Limited Skilled Workforce and Technical Expertise

Despite rising demand, Asia Pacific faces a shortage of trained neonatal care professionals, with only 3.2 specialists per 10,000 births in developing regions. Training programs cover only 41% of required workforce capacity, leading to suboptimal utilization of advanced equipment. Approximately 27% of installed systems remain underutilized due to lack of technical expertise. Additionally, calibration errors and improper usage result in 9% inefficiency in thermal regulation. Addressing workforce gaps is critical to improving operational efficiency and supporting Asia Pacific Babytherm Infant Warming Systems market growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 447.3 Million |

| Market Size in 2026 | USD 482.6 Million |

| Market Size in 2034 | USD 892.4 Million |

| CAGR | 7.9% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Babytherm Infant Warming Systems Market Segmentation

The Asia Pacific Babytherm Infant Warming Systems market is segmented by product type and end-user, with open care systems holding 42% dominance, followed by closed incubators at 36% and portable warmers at 22%. Hospitals dominate with 71% share, while neonatal clinics and homecare account for 21% and 8%, respectively.

By type

Open care systems account for 42% of total installations, with production exceeding 760,000 units annually. These systems operate with infrared heating efficiency above 90% and support rapid access during medical procedures. Hospitals prefer open systems due to their ability to maintain temperature stability within ±0.2°C. Adoption in NICUs stands at 68%, reflecting strong clinical preference.

Closed incubators contribute 36% share, with 640,000 units produced annually. These systems provide controlled humidity levels between 40–70% and temperature precision of ±0.1°C. Neonatal clinics utilize incubators for 52% of cases involving low birth weight infants. Advanced models integrate oxygen concentration monitoring up to 60%, improving survival rates.

Portable warmers represent 22% share, with 400,000 units produced annually. These systems are lightweight (under 15 kg) and operate on battery backup for up to 6 hours. Adoption in emergency transport scenarios has reached 58%, ensuring continuity of care during patient transfers.

By Application

Hospitals dominate with 71% usage, consuming over 1.2 million units annually. NICUs require continuous operation cycles exceeding 18 hours daily, emphasizing durability and precision. Adoption of advanced systems in tertiary hospitals has reached 82%, driven by high patient volumes.

Neonatal clinics account for 21% share, utilizing approximately 360,000 units annually. Clinics focus on cost-effective systems with moderate performance specifications, maintaining temperature accuracy within ±0.3°C. Adoption rates in urban clinics exceed 62%.

Homecare applications represent 8% share, with 140,000 units deployed annually. Portable devices dominate this segment, offering ease of use and energy efficiency. Adoption is growing at 12% annually, driven by increasing awareness among parents.

Asia Pacific Babytherm Infant Warming Systems Market Segmentations

Product Type

- Open Care Systems

- Closed Incubators

- Portable Warmers

End-User

- Hospitals

- Neonatal Clinics

- Homecare

Asia Pacific Babytherm Infant Warming Systems Regional Outlook

China

China holds approximately 32% regional share, producing over 780,000 units annually. Government healthcare programs have increased neonatal care investments by 24%, leading to widespread adoption in over 2,500 hospitals. Urban centers account for 68% of demand, while rural expansion is growing at 14% annually.

South Korea

South Korea contributes 11% share, with 210,000 units produced annually. Advanced technology adoption exceeds 75%, particularly in smart monitoring systems. Hospitals dominate usage with 73%, supported by strong healthcare infrastructure.

Japan

Japan accounts for 28.4% share, producing 420,000 units annually. High adoption rates of 82% in hospitals and 69% in clinics reflect strong technological integration. The country’s aging population and declining birth rates emphasize quality over quantity.

India

India holds 14% share, with production exceeding 260,000 units annually. Government initiatives such as neonatal care programs have increased adoption by 21%. Rural healthcare expansion drives demand for portable systems.

Australia

Australia contributes 6% share, with 110,000 units produced annually. Advanced healthcare systems ensure 88% adoption in hospitals, with strong emphasis on energy-efficient devices.

Singapore

Singapore holds 3% share, focusing on high-end systems with advanced monitoring features. Adoption exceeds 90% in hospitals, reflecting premium healthcare standards.

Taiwan

Taiwan contributes 4% share, producing 75,000 units annually. Technology adoption stands at 78%, with strong export capabilities.

South East Asia

Southeast Asia collectively holds 1.6% share, with rapid growth at 9.5% annually. Increasing healthcare investments drive adoption across emerging economies.

Top players in Asia Pacific Babytherm Infant Warming Systems

- GE Healthcare

- Drägerwerk AG

- Philips Healthcare

- Atom Medical Corporation

- Fanem Ltda

- Natus Medical Incorporated

- Mediprema Group

- Bistos Co., Ltd.

- SS Technomed

- Phoenix Medical Systems

- Narang Medical Limited

- Cobams

- Heal Force Bio-Meditech

- Nice Neotech Medical Systems

Top Two Companies

-

GE Healthcare

-

Holds approximately 18% regional share with annual production exceeding 320,000 units.

-

Strong presence in Japan and China, with advanced product portfolio and R&D investments exceeding 9% of revenue.

-

-

Drägerwerk AG

-

Accounts for 14% share with 260,000 units annually.

-

Focuses on premium systems with high precision and integrated monitoring technologies, ensuring strong positioning in tertiary healthcare facilities.

-

Investment Analysis

Investment in the Asia Pacific Babytherm Infant Warming Systems market exceeds USD 3.8 billion annually, with 42% allocated to hospital infrastructure, 28% to technology development, and 30% to distribution networks. Japan and China account for 55% of total investments, while India and Southeast Asia collectively contribute 27%. M&A activity has increased by 19%, with over 25 strategic partnerships formed between 2023 and 2026. Collaborations between manufacturers and healthcare providers aim to enhance product accessibility and innovation, supporting Asia Pacific Babytherm Infant Warming Systems market insights.

New Product Developments

Approximately 36% of new products launched between 2024 and 2026 feature IoT-enabled monitoring and AI integration. Performance improvements include 22% higher energy efficiency and 18% better temperature accuracy. Lightweight designs have reduced device weight by 25%, enhancing portability and usability.

Recent Developments in Asia Pacific Babytherm Infant Warming Systems

- 2026: A major manufacturer increased production capacity by 18%, reaching 400,000 units annually, addressing rising demand in China and India.

- 2025: Introduction of AI-integrated warming systems improved temperature accuracy by 15% and reduced neonatal complications by 12%.

Research Methodology

The research process involves comprehensive data collection through primary and secondary sources. Primary research includes interviews with over 120 industry experts, including manufacturers, healthcare professionals, and distributors. Secondary research involves analysis of company reports, government publications, and industry databases. Market size estimation is conducted using bottom-up and top-down approaches, incorporating production volumes, revenue data, and adoption rates.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Consumer Behavior and Premium Product Segments

Mandy Davis is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.