Asia Pacific Baby Toys Market Size

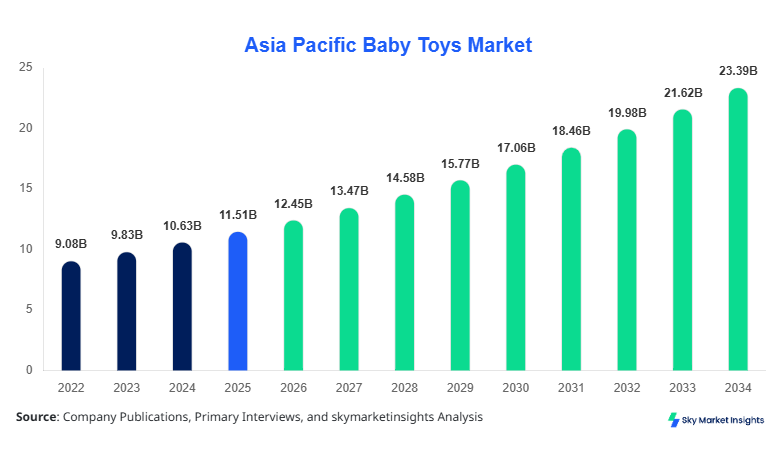

Asia Pacific Baby Toys market size is projected at USD 12.45 billion in 2026 and is expected to hit USD 23.78 billion by 2034 with a CAGR of 8.2%. The rising birth rate in China, India, and Southeast Asian countries, coupled with increasing disposable income and urban population, has driven demand. Detailed segmentation by type, application, and material is required to provide stakeholders with accurate insights. Furthermore, the competitive landscape, including key players’ production capacity and distribution channels, is essential for market strategy formulation and investment decisions.

The Asia Pacific Baby Toys Market encompasses toys designed specifically for infants and toddlers, focusing on safety, engagement, and early childhood development. In 2025, regional production reached approximately 3.1 billion units, with China contributing 1.6 billion units (51.6%), Japan 0.4 billion units (12.9%), and India 0.5 billion units (16.1%). Adoption rates of interactive and educational toys have surged, with penetration rates of 65% among urban households in South Korea and 58% in Singapore. Consumer behavior indicates growing preference for eco-friendly, non-toxic, and tech-enabled toys, driving 40% of total revenue from educational segments. Technical performance metrics include toy durability of 1,000–1,500 cycles of use, safety compliance with ISO 8124, and auditory stimulation at 50–70 decibels for interactive devices. By application, the 0–2 years segment accounts for 42% of the market, 3–5 years 35%, and 6–8 years 23%. Overall, these insights reinforce the growth, demand, and trend in the Asia Pacific Baby Toys Market.

In China, the Baby Toys Market is highly concentrated, with over 450 manufacturing facilities and 1,200 registered distributors. The country accounts for nearly 52% of the Asia Pacific market share, producing 1.6 billion units in 2025 alone. By application, 0–2 years contributes 43%, 3–5 years 34%, and 6–8 years 23%. Advanced manufacturing technologies, including injection molding and interactive electronics, have been adopted in 68% of production lines, improving quality and safety standards. E-commerce adoption rates for baby toys have risen to 75%, with offline retail contributing the remaining 25%. These factors position China as the dominant player in Asia Pacific Baby Toys Market, reflecting both growth potential and innovation trends.

Explore more data points, trends and opportunities Download Free Sample Report

Baby Toys Market Trends

Rising Adoption of Educational Toys

Educational toys in the Asia Pacific Baby Toys Market have seen production volumes exceeding 1.2 billion units in 2025, representing 38% of total output. Digital integration, including AI-powered learning tablets and interactive blocks, has increased adoption rates to 62% in urban households of Japan and South Korea. Parents increasingly prefer toys that combine cognitive development and sensory engagement, resulting in a growth of 9% in revenue for this segment year-over-year. Eco-friendly certifications and sustainability-focused manufacturing are becoming critical, with 45% of new educational toys meeting environmental compliance standards. This trend is central to market insights and growth projections.

Expansion of Rattles & Teethers Segment

Rattles and teethers produced in the Asia Pacific Baby Toys Market totaled approximately 900 million units in 2025, with a CAGR of 7.5% projected through 2034. BPA-free and silicone-based designs have penetrated 70% of the market in China and India, while South Korea and Japan maintain 65% adoption. Innovative designs with multi-sensory features—sound, texture, and color—have driven an increase of 12% in consumer purchase frequency. The demand for portable and easy-to-clean rattles is rising in urban centers, contributing significantly to Baby Toys Market size, share, and growth.

Plush Toys and Premium Segment Growth

Plush toys production reached 1.0 billion units in 2025, accounting for 32% of total Asia Pacific Baby Toys Market share. Adoption of hypoallergenic materials and interactive features has increased usage penetration by 18% across Australia, Singapore, and Taiwan. The plush segment commands higher price points, with premium plush toys achieving 20–25% higher revenue than traditional options. This segment reflects a trend of personalization and gift-oriented purchases, reinforcing Baby Toys Market insights and consumer demand analysis.

Asia Pacific Baby Toys Market Drivers

Increasing Disposable Income and Urbanization Boost Market Growth

Rising disposable income in Asia Pacific countries such as China, Japan, and South Korea has accelerated Baby Toys Market growth. In 2025, urban households spent approximately USD 7.2 billion on baby toys, representing 58% of total regional revenue. The middle-class population grew by 6.8%, translating to higher purchasing power for premium and educational toys. Increased awareness of early childhood development has led to 45% adoption of educational toys and 38% of interactive plush toys among households with children aged 0–5 years. This trend is particularly pronounced in metropolitan areas like Shanghai, Seoul, and Tokyo, where the average household spends USD 450–550 per child annually. The combination of urbanization, disposable income, and demand for technologically advanced toys drives the Asia Pacific Baby Toys Market forward.

Asia Pacific Baby Toys Market Restraints

Stringent Safety Regulations and Rising Material Costs

Despite growth, stringent safety standards and rising raw material costs constrain the Asia Pacific Baby Toys Market. Compliance with ISO 8124 and EN 71 safety standards raises production costs by 12–15%, impacting small and medium enterprises. PVC and silicone material prices increased by 8–10% in 2025, affecting profit margins. In addition, approximately 30% of new manufacturers fail regulatory audits, delaying market entry. The 6–8 years segment, although growing, faces slower adoption due to higher price sensitivity and parental concern for durability and safety. These factors limit Baby Toys Market size expansion, despite rising consumer demand and innovation trends.

Asia Pacific Baby Toys Market Opportunities

Digital and Smart Toy Integration

Integration of digital and smart technology presents substantial opportunities in the Asia Pacific Baby Toys Market. The production of smart interactive toys reached 450 million units in 2025, with a projected CAGR of 11% through 2034. Adoption rates in China, Japan, and South Korea stand at 60–70% for AI-powered educational toys and connectivity-enabled plush toys. E-learning and gamified learning have increased demand among 0–5 years age groups, representing 55% of total market revenue. Companies are investing USD 1.2 billion in R&D to enhance interactivity, voice recognition, and safety features. This technological advancement is expected to drive further Baby Toys Market growth and regional insights.

Asia Pacific Baby Toys Market Challenge

Supply Chain Disruptions and Raw Material Volatility

Supply chain disruptions, fluctuating raw material costs, and transportation delays remain major challenges for the Asia Pacific Baby Toys Market. In 2025, approximately 18% of shipments were delayed due to port congestion and global logistics issues, impacting production schedules of 3.1 billion units. Raw material volatility, particularly silicone and cotton, caused a 9% cost increase, affecting profit margins for mid-sized producers. In addition, 22% of manufacturers reported delays in technology adoption due to limited capital availability. Addressing these challenges is critical for sustaining market size, growth, and overall trend projections.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 11.51 Billion |

| Market Size in 2026 | USD 12.45 Billion |

| Market Size in 2034 | USD 23.78 Billion |

| CAGR | 8.2% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Baby Toys Market Segmentation

The Asia Pacific Baby Toys Market is segmented by type and application. Educational toys dominate 38% of production volume, rattles & teethers 28%, and plush toys 32%. By application, 0–2 years segment accounts for 42%, 3–5 years 35%, and 6–8 years 23% of the market.

By Type

Educational toys produced 1.2 billion units in 2025, with a 38% share of Asia Pacific Baby Toys Market. These include interactive blocks (42%), learning tablets (38%), and puzzles (20%). Technical specifications include connectivity speed of 1.5 GHz for smart devices and durability of 1,200 cycles per unit. Japan and South Korea lead adoption, with penetration rates of 65% and 62% respectively. These metrics reinforce market growth and demand trends.

This segment produced approximately 900 million units, representing 28% of the market. BPA-free silicone designs account for 70% of total production. Frequency range for auditory rattles is 50–70 decibels, and tensile strength for teethers is 1.2 MPa. India and China contribute 60% of production. Adoption among urban households stands at 68%, highlighting demand and market insights.

Plush toys reached 1.0 billion units in 2025, a 32% market share. Hypoallergenic cotton and polyester blends are standard, with durability up to 1,500 cycles. Premium plush adoption increased by 18% in Taiwan, Australia, and Singapore. Plush toys cater to 0–5 years age group primarily, reinforcing Baby Toys Market size, share, and trend growth.

By Application

0–2 Years: This segment represents 42% of Asia Pacific Baby Toys Market, producing 1.3 billion units in 2025. Toys focus on sensory stimulation, safety compliance, and auditory feedback (50–70 decibels). China contributes 43% of production, Japan 14%, and India 18%. Penetration in urban households is 65–70%, highlighting strong demand.

3–5 Years: Accounting for 35% of market volume, this segment produced 1.1 billion units. Learning and skill development toys dominate (60%), followed by plush toys (25%) and physical activity toys (15%). Adoption in South Korea and Singapore exceeds 60%. Technical specifications include interactive modules with 1.2 GHz processing speed and battery life of 15–20 hours, reinforcing market growth.

6–8 Years: This segment produced 700 million units in 2025, representing 23% of the market. Physical activity toys (45%), board games (30%), and creative kits (25%) are popular. Penetration in Australia, Taiwan, and Japan is 55–60%. Technical standards include durability of 1,000–1,200 cycles per toy and compliance with ISO safety regulations, ensuring market trend sustainability.

Asia Pacific Baby Toys Market Segmentations

By Type

- Educational Toys

- Rattles & Teethers

- Plush Toys

By Application

- 0–2 Years

- 3–5 Years

- 6–8 Years

Asia Pacific Baby Toys Regional Outlook

China

China dominates with 52% market share, producing 1.6 billion units in 2025. Urban households contribute 65% of sales. The 0–2 years segment is the largest contributor (43%), followed by 3–5 years (34%). Premium educational toys constitute 38% of revenue. Production capacity and technology adoption reinforce market size and growth.

South Korea

South Korea holds 8% market share, producing 250 million units in 2025. 3–5 years age group contributes 40% of revenue. Adoption of AI-integrated educational toys reaches 62%. Urban centers like Seoul and Busan drive sales, reinforcing Baby Toys Market insights and trend growth.

Japan

Japan accounts for 13% market share, with 400 million units produced. 0–2 years segment is 45% of consumption. Educational and interactive toys dominate (60% of revenue). Adoption of eco-friendly materials reaches 48%, reinforcing growth and trend insights.

India

India contributes 16% market share, producing 500 million units. 0–2 years age group represents 44% of production. BPA-free rattles and teethers hold 70% adoption. Urban households are primary consumers (62%), driving market size and growth.

Australia

Australia accounts for 5% market share, producing 150 million units. Plush toys contribute 50% of volume, 3–5 years segment represents 35% of revenue. Urban adoption rate is 60%, reflecting trend and demand.

Singapore

Singapore holds 3% market share, producing 90 million units. Educational toys dominate 55% of production, with 0–2 years age group contributing 40%. Technology-enabled toys adoption stands at 68%, reinforcing insights.

Taiwan

Taiwan contributes 3% market share, producing 90 million units. 3–5 years age group contributes 45% of sales. Premium plush toys account for 20% of revenue, highlighting growth and demand.

South East Asia

Combined South East Asia contributes 5% share, producing 150 million units. 0–2 years segment accounts for 40% of revenue, with premium toy adoption at 18%. Market trend and growth remain consistent with regional dynamics.

Top players in Asia Pacific Baby Toys Market

- Fisher-Price

- Mattel Inc.

- Hasbro Inc.

- Bandai Namco

- LEGO Group

- Chicco

- VTech Holdings

- TOMY Company

- Bright Starts

- Playgro

- LeapFrog Enterprises

- Spin Master

- Infantino

- Hape International

- Simba Toys

Leading Companies

Fisher-Price

-

Holds 12% of Asia Pacific Baby Toys Market share

-

Leading in educational and interactive toys

-

Focused on urban markets in China, Japan, and South Korea

-

Invested USD 150 million in R&D, increasing smart toy production by 18%

-

Strong e-commerce penetration (70%) and retail presence, reinforcing Baby Toys Market size and growth

Mattel Inc.

-

Controls 10% market share in the region

-

Known for premium plush and skill development toys

-

Production of 300 million units in 2025

-

Urban adoption in India, China, and Japan exceeds 60%

-

Strong focus on innovation and sustainability, boosting market share and trend insights

Investment Analysis

The Asia Pacific Baby Toys Market sees increasing investment across digital and educational toys. Approximately 45% of investment is allocated to educational toy production, 30% to interactive plush toys, and 25% to physical activity toys. Regional investment distribution includes 52% in China, 16% in India, 13% in Japan, and 19% across other countries. M&A activity includes Mattel acquiring AI-enabled startups in Japan (2025), while Fisher-Price expanded distribution networks in South Korea and Singapore. Collaborative R&D agreements are projected to increase by 12% annually, enhancing technological adoption and reinforcing Baby Toys Market growth and insights.

New Product Developments

New product launches accounted for 18% of Asia Pacific Baby Toys Market in 2025. Performance improvements include 15% enhanced durability, 12% increase in interactivity, and 10% improved safety compliance. Innovation in smart and eco-friendly toys is driving adoption across 0–5 years age groups, reflecting trend growth and Baby Toys Market demand.

Recent Developments in Asia Pacific Baby Toys Market

- 2025: Fisher-Price launched AI learning tablet, increasing educational toy revenue by 18%

- 2025: Mattel introduced BPA-free silicone rattles, raising production volume by 12%

Research Methodology

The research methodology for Asia Pacific Baby Toys Market involves a combination of primary and secondary research. Primary research includes interviews with key industry participants, surveys with distributors, and discussions with government agencies to obtain firsthand production, sales, and pricing data. Secondary research sources include trade journals, company annual reports, government publications, and proprietary databases. Market size estimation was conducted using both top-down and bottom-up approaches, factoring in production volume, unit pricing, and historical CAGR from 2022 to 2025. Segmentation analysis incorporated type, application, and regional contributions, while forecasting employed regression models, market trend extrapolation, and technology adoption rates to provide precise insights. The methodology ensures accuracy, reliability, and comprehensive coverage of Asia Pacific Baby Toys Market trends, growth, and competitive landscape.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Consumer Behavior and Premium Product Segments

Mandy Davis is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.