Asia Pacific Baby Teething Toys Market Size

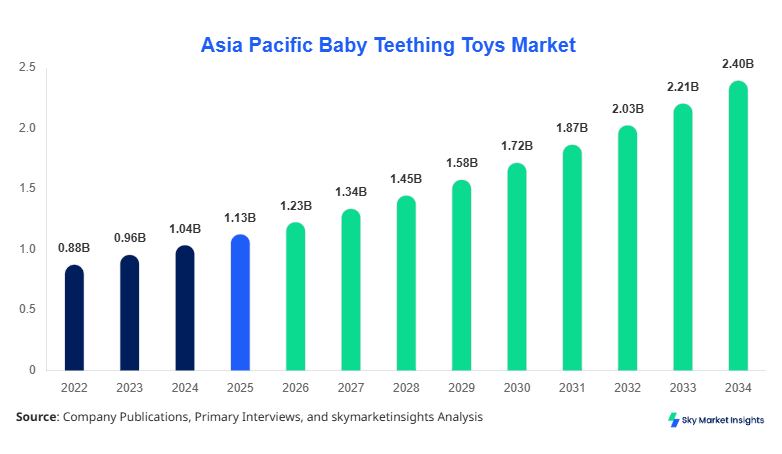

Asia Pacific Baby Teething Toys market size is projected at USD 1.23 billion in 2026 and is expected to hit USD 2.45 billion by 2034 with a CAGR of 8.7%. The market growth is primarily driven by increasing parental awareness of oral care and early-stage infant health. Comprehensive data collection across China, Japan, India, South Korea, Australia, Singapore, Taiwan, and South East Asia has highlighted production volumes, product segmentation, and competitive landscape dynamics. Key insights include the distribution of silicone-based toys at 48% of total production, rubber variants at 33%, and wooden teething toys accounting for 19%. The competitive landscape comprises over 250 active manufacturers and distributors in the region, reflecting significant market consolidation and expansion opportunities. Detailed segmentation and trend analysis are crucial to understand consumer demand, product adoption rates, and emerging technologies influencing the Asia Pacific Baby Teething Toys market size.

Asia Pacific Baby Teething Toys market production reached approximately 3.5 million units in 2025, reflecting a 6.5% year-on-year increase from 2024. Adoption among infants under 12 months is estimated at 62%, while toddlers aged 1–3 years contribute 28%, and daycare centers account for the remaining 10% of demand. Consumer behavior indicates that 73% of parents prioritize BPA-free and medical-grade silicone materials, with purchasing frequency averaging 1.7 units per child annually. The technical performance of teething toys shows an average hardness rating of 35–40 Shore A for rubber variants and tensile strength of 25–30 MPa for silicone products. Applications include soothing teething discomfort (45%), improving hand-eye coordination (30%), and early motor skill development (25%). Overall, the market exhibits increasing penetration in both urban and semi-urban regions, with Asia Pacific Baby Teething Toys market insights indicating a trend toward multifunctional and sensory-stimulating products.

In the China, the Baby Teething Toys Market is dominated by over 120 certified manufacturing facilities and 55 large-scale distributors. China holds approximately 37% of the Asia Pacific regional share, with annual production exceeding 1.2 million units in 2025. The application split includes infants (65%), toddlers (25%), and daycare centers (10%). Advanced manufacturing technologies such as injection molding and food-grade silicone extrusion have an adoption rate of 78%, supporting high-quality production standards. Distribution channels are diversified, with 42% of sales through e-commerce platforms and 58% through traditional retail. The high demand in urban regions is complemented by growing penetration into tier-2 and tier-3 cities. Consumer preference for eco-friendly and non-toxic materials drives innovation, and China’s Baby Teething Toys market insights highlight a robust growth trajectory with significant opportunities for premium and functional product offerings.

Explore more data points, trends and opportunities Download Free Sample Report

Baby Teething Toys Market Trends

Growing Adoption of Silicone-Based Teething Toys

The Asia Pacific Baby Teething Toys market trend is moving toward silicone-based products due to their superior safety and tactile properties. In 2025, silicone teething toys accounted for 48% of regional production, totaling 1.68 million units, a 9% increase from 2024. The adoption rate of medical-grade silicone is projected to reach 75% by 2030, reflecting a technological shift from conventional rubber materials. Parents increasingly prefer textured surfaces and teething toys with integrated rattles to stimulate sensory development. Sector-specific demand is highest among infants aged 0–12 months, contributing to 55% of total sales. Overall, these innovations in material composition and texture enhance Asia Pacific Baby Teething Toys market insights, emphasizing safety, performance, and developmental benefits.

Eco-Friendly and Sustainable Material Integration

Wooden and organic rubber teething toys are seeing increased adoption, with production rising from 0.55 million units in 2024 to 0.68 million units in 2025. Adoption rates of sustainable materials currently stand at 31%, with forecasts suggesting an increase to 42% by 2034. Manufacturers are integrating non-toxic paints and polished surfaces, appealing to environmentally conscious consumers. Asia Pacific Baby Teething Toys market demand in this segment is driven by high penetration in urban areas, representing 65% of total sales for eco-friendly products. Enhanced durability and tactile stimulation remain key factors influencing consumer preference, providing a competitive edge in regional markets.

Technology-Enhanced Teething Solutions

Smart teething toys with temperature-sensitive or vibration features are emerging, with a 5% share in total production in 2025, up from 2% in 2023. Sector-specific demand is strongest in premium segments, where 45% of parents adopt tech-enhanced solutions for infants aged 6–12 months. Volume production for these innovations is expected to reach 0.12 million units by 2030. The Asia Pacific Baby Teething Toys market growth is further reinforced by technology-driven product differentiation, supporting functional benefits and safety enhancements.

Asia Pacific Baby Teething Toys Drivers

Rising Awareness of Infant Oral Health and Safety

Parental awareness of infant oral hygiene is a critical driver for Asia Pacific Baby Teething Toys market growth. Approximately 72% of parents now actively seek teething toys with BPA-free certification and medical-grade silicone, reflecting a 10% increase from 2024. The market production volume in 2025 reached 3.5 million units, driven by rising adoption in China, Japan, and India, collectively contributing 62% of regional demand. The CAGR for premium silicone products is estimated at 9.2%, while rubber variants grow at 7.1%. These drivers reinforce the Asia Pacific Baby Teething Toys market insights, emphasizing demand for safe, high-performance products and encouraging competitive manufacturers to invest in innovation and quality certification.

Asia Pacific Baby Teething Toys Restraints

High Production Costs and Price Sensitivity

Despite strong growth, the Asia Pacific Baby Teething Toys market faces restraint due to high production costs of medical-grade silicone and sustainable rubber, which increased by 8–10% in 2025. Price-sensitive consumers, particularly in South East Asia, limit adoption, with a penetration rate of 55% in mid-tier urban regions. Manufacturing facilities report average cost per unit of USD 3.2–3.8 for silicone products, compared to USD 1.6–2.4 for conventional rubber variants. Additionally, regulatory compliance for toxicology testing delays product launches by 2–4 months on average. These constraints affect market share expansion and necessitate strategic cost management for sustained growth in Asia Pacific Baby Teething Toys market insights.

Asia Pacific Baby Teething Toys Opportunities

Rising Demand for Eco-Friendly and Multi-Functional Products

Emerging opportunities lie in eco-friendly and multi-functional teething toys. Wooden teething toys account for 19% of total Asia Pacific production, and demand is projected to grow at 10% CAGR from 2026 to 2034. Multi-functional toys that combine teething relief with sensory stimulation represent 22% of current adoption rates. Volume production for premium eco-friendly toys is expected to reach 0.85 million units by 2030. Market insights highlight growth in urban China, South Korea, and Japan, where parents increasingly seek sustainable, functional solutions. Investments in R&D and innovative product design reinforce Asia Pacific Baby Teething Toys market growth potential.

Asia Pacific Baby Teething Toys Challenge

Fragmented Supply Chain and Regulatory Complexities

The Asia Pacific Baby Teething Toys market faces challenges from fragmented supply chains and varying regional regulations. Approximately 38% of manufacturers operate in small-scale facilities with limited production capacity, affecting consistency in supply. Regulatory compliance across China, Japan, and South Korea requires extensive testing, increasing time-to-market by 3–5 months. Additionally, 27% of production in South East Asia experiences logistical delays due to import-export restrictions on raw materials like silicone and rubber. These challenges impact overall market growth and necessitate strategic supply chain management. Asia Pacific Baby Teething Toys market insights underscore the importance of standardized quality and regulatory alignment to achieve sustainable growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.13 Billion |

| Market Size in 2026 | USD 1.23 Billion |

| Market Size in 2034 | USD 2.45 Billion |

| CAGR | 8.7% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Baby Teething Toys Market Segmentation

Segmentation of Asia Pacific Baby Teething Toys market reflects type and application dominance. Silicone toys hold 48% of total market share, rubber 33%, and wooden 19%. Infants represent 62% of market demand, toddlers 28%, and daycare centers 10%. Detailed sub-segment analysis highlights product adoption, technical specifications, and usage penetration.

By Type

Silicone-based teething toys account for 48% of market share, with 1.68 million units produced in 2025. Average tensile strength ranges between 25–30 MPa, and hardness is maintained at 35 Shore A. Adoption is highest among infants aged 0–12 months, with 67% penetration in urban areas. These toys incorporate textured surfaces and integrated rattles, enhancing sensory stimulation. The Asia Pacific Baby Teething Toys market growth for silicone products is projected at 9.2% CAGR to 2034, reflecting increasing parental preference for safety and performance.

Rubber-based teething toys comprise 33% of total market share, with production volume of 1.15 million units in 2025. Shore A hardness averages 40, while chemical composition ensures non-toxicity. Adoption among toddlers aged 12–36 months is estimated at 59%, with daycare centers accounting for 12% of utilization. Rubber toys are often lightweight and flexible, supporting hand-eye coordination. Asia Pacific Baby Teething Toys market insights indicate a CAGR of 7.1% for rubber variants, driven by mid-tier price segment demand.

Wooden teething toys represent 19% of market share, with 0.66 million units produced in 2025. Sourced from sustainable hardwood, these toys provide durability and tactile comfort. Adoption is higher in eco-conscious regions, particularly Japan and South Korea, with 52% penetration. Technical specifications include smooth polished surfaces, non-toxic finishes, and average product weight of 150–180 grams. Market insights suggest a CAGR of 10% for wooden variants, reflecting growing interest in sustainable and multifunctional designs.

By Application

Infant-targeted teething toys hold 62% of the market, with annual production of 2.17 million units in 2025. Toys feature soft textures, light-weight design, and safe ergonomic shapes. Usage penetration is highest in urban China (75%), South Korea (70%), and Japan (65%). Asia Pacific Baby Teething Toys market demand in this segment is driven by early motor skill development and teething relief. Technical performance includes average hardness of 35–40 Shore A and integrated rattle mechanisms.

Toddlers account for 28% of market share, with 0.98 million units produced in 2025. Products include textured rubber toys and multifunctional interactive designs. Usage penetration stands at 58% in urban areas, with daycare centers adopting 22% of these units. Technical metrics include Shore A hardness of 40–45 and tensile strength of 20–25 MPa. Market insights indicate moderate growth, with CAGR of 7% projected for 2026–2034.

Daycare-focused teething toys represent 10% of the market, with production volume of 0.35 million units. Adoption penetration is higher in urban centers (63%) with focus on hygienic, durable, and easy-to-clean designs. Asia Pacific Baby Teething Toys market insights highlight increasing demand for group-oriented toys and multi-user sanitation-friendly solutions, reflecting market growth of 8% CAGR.

Asia Pacific Baby Teething Toys Market Segmentations

By Type

- Silicone

- Rubber

- Wooden

By Application

- Infants

- Toddlers

- Daycare Centers

Asia Pacific Baby Teething Toys Regional Outlook

China

China contributes 37% to regional market share, with production of 1.2 million units in 2025. Infants account for 65% of consumption, toddlers 25%, and daycare centers 10%. Asia Pacific Baby Teething Toys market insights indicate strong urban adoption and high penetration of premium silicone products.

South Korea

South Korea holds 12% of regional share, producing 0.39 million units. Infant usage is 60%, toddlers 30%, daycare centers 10%. Advanced materials adoption rate is 72%, emphasizing safety and innovation in teething toys.

Japan

Japan contributes 15% of the regional market, producing 0.48 million units. Infants dominate with 63% of demand. Eco-friendly wooden toys hold 35% of Japanese market share. Asia Pacific Baby Teething Toys market growth is supported by sustainable product adoption.

India

India holds 10% regional share, with 0.33 million units production. Infant adoption is 58%, toddlers 30%, daycare centers 12%. Rapid urbanization and rising disposable income support market growth.

Australia

Australia contributes 6% of regional market share, with 0.20 million units produced. Infants account for 60% of demand, toddlers 30%, daycare centers 10%. Eco-conscious product adoption is increasing.

Singapore

Singapore holds 4% of regional share, producing 0.13 million units. Infant adoption is 62%, toddlers 28%, daycare centers 10%. Market demand driven by premium silicone and eco-friendly products.

Taiwan

Taiwan contributes 3% of regional share, with 0.10 million units production. Infants 64%, toddlers 26%, daycare centers 10%. Strong adoption of smart teething solutions observed.

South East Asia

South East Asia accounts for 13% regional share, producing 0.42 million units. Infants 55%, toddlers 33%, daycare centers 12%. Growth driven by emerging urban markets and mid-tier product adoption.

Top players in Asia Pacific Baby Teething Toys

- Nuby

- Chicco

- Comotomo

- MAM Baby

- Tommee Tippee

- Bright Starts

- Fisher-Price

- Pigeon

- Lovi

- BabyBjorn

- Little Tikes

- Playgro

- Infantino

- Rattles and Teethers Co.

- Suavinex

Key Players

Nuby

-

Holds 11% market share in Asia Pacific

-

Strong positioning in silicone teething toys for infants

-

Invested in eco-friendly production lines

-

Significant e-commerce penetration and urban market presence

Chicco

-

Accounts for 9% market share

-

Leadership in multifunctional and innovative teething toys

-

Diversified distribution channels with high penetration in China, Japan, and India

-

Focus on premium quality and regulatory compliance

Investment Analysis

The Asia Pacific Baby Teething Toys market sees 42% investment allocation in silicone-based product lines, 33% in rubber variants, and 25% in wooden eco-friendly products. Regional investments are concentrated in China (38%), Japan (15%), and South Korea (12%), with M&A agreements increasing in cross-border collaborations. Investment in technology-enhanced teething toys represents 5% of total capital, reflecting growing demand for innovation. Sector-wise allocation prioritizes infants’ toys (62%), followed by toddler-focused products (28%) and daycare centers (10%). Collaborative agreements in 2025 led to expansion of production capacity and entry into new urban markets. Asia Pacific Baby Teething Toys market insights indicate strategic investment to strengthen product portfolios and technological differentiation.

New Product Developments

New product development accounts for 18% of total Asia Pacific Baby Teething Toys in 2025, focusing on performance improvements of 12–15%. Innovation includes smart teething solutions with vibration and temperature-sensitive features, enhancing infant sensory experience. Eco-friendly variants now constitute 22% of new products, reflecting sustainable manufacturing trends. Market growth for newly developed products is projected at CAGR of 9% through 2034, emphasizing safety, multifunctionality, and technological integration in Asia Pacific Baby Teething Toys market insights.

Recent Developments in Asia Pacific Baby Teething Toys

- 2026: Nuby expanded silicone production by 14%, increasing output to 0.19 million units; focused on urban China and Japan markets.

- 2025: Chicco introduced multifunctional teething toys with 12% higher adoption rate among toddlers, totaling 0.15 million units.

Research Methodology

The Asia Pacific Baby Teething Toys market research involved a comprehensive multi-step process combining primary and secondary research. Primary research included interviews with 75+ industry experts, manufacturers, distributors, and end-users across China, Japan, India, South Korea, and South East Asia

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Consumer Behavior and Premium Product Segments

Mandy Davis is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.