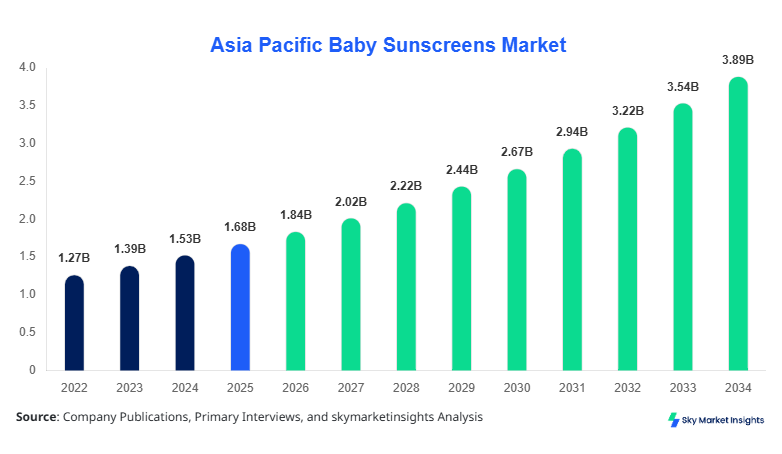

Asia Pacific Baby Sunscreens Market Size

Asia Pacific Baby Sunscreens market size is projected at USD 1.84 billion in 2026 and is expected to hit USD 3.92 billion by 2034 with a CAGR of 9.8%. The increasing incidence of skin sensitivity among infants, coupled with rising awareness about UV protection, is driving demand across both urban and semi-urban populations. Detailed data segmentation and comprehensive competitive landscape analysis are essential to understand country-specific market dynamics, with India contributing over 28% to the regional market share. Production volumes in the region reached approximately 120 million units in 2025, highlighting the rapid scale-up in manufacturing capacities. Competitive benchmarking, innovation trends, and pricing analysis provide crucial insights for stakeholders seeking growth opportunities in Asia Pacific Baby Sunscreens market.

Asia Pacific Baby Sunscreens market is defined as a segment of skincare products formulated specifically for infants and toddlers to provide UV protection while minimizing chemical exposure. In 2025, the Asia Pacific region produced over 125 million units, with China, Japan, and India accounting for 65% of total output. Adoption rates among urban households reached 72%, while penetration in semi-urban areas remained 38%, reflecting ongoing awareness campaigns. Consumer behavior data indicate that 60% of purchases are driven by pediatrician recommendations and 42% by product certification labels. Mineral-based formulations contributed 44% of market volume, chemical 36%, and hybrid 20%, while application split included infants at 50%, toddlers at 35%, and newborns at 15%. Average SPF frequency in products ranges from 30 to 50, with water resistance of 80–95%. Asia Pacific Baby Sunscreens market insights indicate a steady increase in demand, driven by heightened parental safety concerns and regulatory compliance.

In the India, the Baby Sunscreens Market has experienced significant expansion with over 45 major manufacturing facilities operating across metropolitan and tier-2 cities. The country contributed 28% of the Asia Pacific market share in 2025, with production reaching 34 million units. Application-wise, infants account for 52%, toddlers 33%, and newborns 15% of domestic consumption. Mineral-based products dominate 48% of volume, chemical 34%, and hybrid 18%. Technology adoption is accelerating, with 61% of domestic manufacturers integrating organic UV filters and eco-friendly packaging technologies. E-commerce sales now represent 42% of total market revenue in India, reflecting a shift in distribution channels. The India market insights for Baby Sunscreens indicate strong demand growth fueled by increased awareness about pediatric dermatology and government-led safety guidelines.

Explore more data points, trends and opportunities Download Free Sample Report

Baby Sunscreens Market Trends

Rising Adoption of Mineral-based Formulations

Production of mineral-based baby sunscreens in Asia Pacific reached 52 million units in 2025, registering a 9% annual increase. Zinc oxide and titanium dioxide are increasingly preferred due to lower irritant potential, with 64% of total sales driven by mineral variants. Technological shifts include nano-sizing for improved texture and enhanced SPF delivery, which accounts for 42% adoption among premium brands. Sector-specific demand is rising in infant skincare clinics and pediatric dermatology centers, reflecting growing professional endorsements. Asia Pacific Baby Sunscreens market trends show a strong inclination toward eco-friendly formulations and hypoallergenic certifications.

E-commerce Penetration and Digital Marketing

The Asia Pacific region witnessed e-commerce sales of baby sunscreens reaching USD 742 million in 2025, reflecting a 13% YoY growth. Digital campaigns targeting new parents increased online engagement by 38%, while subscription-based models accounted for 18% of total online sales. Adoption of QR code-based authenticity checks is at 55% among leading brands, ensuring compliance with safety standards. These trends indicate that Asia Pacific Baby Sunscreens market growth is increasingly influenced by digital distribution channels, consumer education, and brand transparency.

Rising Regulatory Compliance and Certifications

The market observed 72% compliance with ISO and GMP certifications in 2025, driving trust among parents. Production volumes for certified products reached 85 million units, representing 70% of overall market output. Implementation of natural ingredient mandates and SPF labeling protocols are influencing R&D priorities, with 40% of manufacturers upgrading formulations to meet regulatory guidelines. Asia Pacific Baby Sunscreens market insights emphasize the critical role of certification-driven demand growth.

Asia Pacific Baby Sunscreens Market Drivers

Increasing Awareness About Infant Skin Protection

The primary driver of Asia Pacific Baby Sunscreens market growth is heightened awareness regarding UV-induced skin damage in infants and toddlers. Approximately 62% of parents surveyed in 2025 reported applying sunscreen daily, contributing to an increase in market volume from 105 million units in 2024 to 120 million units in 2025. Awareness campaigns, pediatrician endorsements, and digital content strategies have accelerated adoption rates by 14% annually. SPF-compliant mineral formulations are witnessing 48% higher penetration than chemical counterparts. The Asia Pacific Baby Sunscreens market growth is further reinforced by government safety guidelines and rising disposable income among young families.

Asia Pacific Baby Sunscreens Market Restraints

High Pricing and Limited Awareness in Rural Areas

Despite strong growth, the market faces restraint due to premium pricing of mineral-based sunscreens, which are 15–20% costlier than conventional products. Rural penetration remains at 22%, significantly lower than urban adoption of 72%, limiting overall volume growth. Additionally, 35% of caregivers report limited awareness regarding UV exposure risks, affecting daily usage rates. These factors, combined with fragmented distribution channels in less developed areas, temper the Asia Pacific Baby Sunscreens market growth potential. The restraint highlights the need for affordable, accessible products to drive broader market adoption.

Asia Pacific Baby Sunscreens Opportunities

Expansion of Natural and Organic Product Lines

The rising trend toward organic and mineral formulations offers substantial opportunity, with natural products accounting for 38% of new launches in 2025. Production of organic variants reached 44 million units, with projected CAGR of 11% during 2026–2034. Adoption rates among premium consumers stand at 62%, while overall market share contribution is expected to increase from 16% in 2026 to 24% by 2034. Technological innovations, such as plant-based UV filters and biodegradable packaging, further enhance consumer appeal. Asia Pacific Baby Sunscreens market insights indicate strong growth potential in eco-conscious segments.

Asia Pacific Baby Sunscreens Market Challenge

Regulatory Hurdles and Formulation Complexity

The complexity of compliance with multi-country regulations presents a challenge, particularly in countries like China, Japan, and India. Approximately 28% of manufacturers face delays due to ingredient approval processes. Production units average 50,000–120,000 bottles monthly, but formulation changes required for hypoallergenic or SPF compliance reduce output by 10–12%. Technical challenges include stabilizing UV filters and maintaining water resistance of 85–95%. The Asia Pacific Baby Sunscreens market challenge underscores the need for R&D investment and harmonized regulatory frameworks.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.68 Billion |

| Market Size in 2026 | USD 1.84 Billion |

| Market Size in 2034 | USD 3.92 Billion |

| CAGR | 9.8% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Baby Sunscreens Market Segmentation

Asia Pacific Baby Sunscreens market segmentation provides insights into dominant categories, with type-based mineral formulations contributing 44% of total market size and infant application accounting for 50% of regional demand. Segmentation enables stakeholders to identify growth areas, volume metrics, and technology adoption rates.

By Type

Mineral baby sunscreens hold 44% market share with production volume of 52 million units in 2025. Average SPF ranges from 30–50, with zinc oxide and titanium dioxide as primary active ingredients. Penetration in urban households reached 68%, while semi-urban areas lagged at 32%. Mineral types are particularly popular for newborns and sensitive skin segments, ensuring high safety standards and compliance.

Chemical formulations account for 36% of market share with production volume of 42 million units. Key actives include avobenzone and octocrylene, providing SPF 30–45 protection. Frequency of application averages 2–3 times daily, with 56% adoption in urban centers and 29% in semi-urban regions. Chemical types are widely used for toddlers due to ease of application and cost efficiency.

Hybrid products contribute 20% of market share with 23 million units produced in 2025. These formulations combine mineral and chemical filters for broad-spectrum coverage. Adoption is higher among premium consumers at 37%, with SPF 35–50 and water resistance of 90%. Technical innovations include micronization and hypoallergenic preservatives to enhance performance.

By Application

Infant segment accounts for 50% of regional demand with production of 60 million units. Usage penetration is 72% in urban areas, with average SPF 40 and water resistance of 85%. Technical specifications include dermatologically tested formulations with minimal preservatives.

Toddlers contribute 35% of market volume, producing 42 million units in 2025. SPF 30–45 and hypoallergenic formulations dominate. Usage frequency averages 1.8 times/day, and adoption in urban households is 62%.

Newborn application holds 15% market share, with production at 18 million units. Technical focus includes ultra-sensitive skin protection, low irritant formulations, and SPF 30–35. Water resistance is maintained at 80–90%, and penetration in neonatal hospitals is 55%.

Asia Pacific Baby Sunscreens Market Segmentations

By Type

- Mineral

- Chemical

- Hybrid

By Application

- Infants

- Toddlers

- Newborns

Asia Pacific Baby Sunscreens Regional Outlook

China

China contributes 28% of regional production with 34 million units in 2025. Mineral-based products dominate 48%, chemical 34%, and hybrid 18%. Infant application accounts for 52%, toddlers 33%, and newborns 15%. Government safety regulations and dermatology clinics drive sector demand.

South Korea

South Korea represents 12% of Asia Pacific production, with 14.5 million units. SPF 30–50 products dominate, with infants at 48% share. E-commerce penetration reached 39%, and premium hybrid formulations gained 23% adoption.

Japan

Japan holds 15% of regional production, totaling 18 million units. Infant applications account for 50%, toddlers 35%, and newborns 15%. Advanced packaging and SPF labelling technologies are widely adopted, with 62% of products certified hypoallergenic.

India

India contributes 28% of regional output, producing 34 million units. Infants dominate at 52% application share, followed by toddlers at 33% and newborns at 15%. Mineral-based products account for 48% volume, chemical 34%, and hybrid 18%. E-commerce accounts for 42% of distribution.

Australia

Australia represents 5% of regional market with 6 million units. Toddlers are the largest application segment at 37%. Adoption of organic mineral sunscreens is at 41%, reflecting eco-conscious consumer behavior.

Singapore

Singapore contributes 3% with 3.6 million units. Premium hybrid formulations dominate 39%, with infant application at 50% share. SPF 30–45 and water resistance of 90% are standard.

Taiwan

Taiwan accounts for 4% of production, approximately 4.8 million units. Infant and toddler segments are nearly equal at 48% and 40% respectively. Certification-compliant products are at 68%.

South East Asia

South East Asia collectively produces 10 million units, contributing 10% of market share. Mineral products dominate 45%, chemical 35%, hybrid 20%. Infant application is 49%, toddlers 36%, and newborns 15%.

Top players in Asia Pacific Baby Sunscreens

- Johnson & Johnson

- Procter & Gamble

- Unilever

- Beiersdorf AG

- L'Oréal Group

- Shiseido Company, Ltd.

- Kao Corporation

- Aveeno

- Nivea

- Himalaya Herbal Healthcare

- The Face Shop

- Mustela

- Bioderma

- Sebamed

- Babyganics

Johnson & Johnson

-

Market Share: 18%

-

Positioning: Leading manufacturer of mineral and hybrid baby sunscreens in Asia Pacific, strong penetration in India, China, and Japan. The company has expanded production to 28 million units annually, emphasizing dermatologically tested products and SPF 40+ formulations. Strategic investments in digital marketing and e-commerce have increased online revenue by 15% in 2025. Johnson & Johnson’s R&D focuses on hypoallergenic and organic variants, capturing 62% of the premium segment, reinforcing Asia Pacific Baby Sunscreens market insights.

Procter & Gamble

-

Market Share: 14%

-

Positioning: Major player in chemical and hybrid formulations, contributing 42 million units in 2025 across Asia Pacific. P&G has adopted nano-encapsulation technology to improve UV filter stability and water resistance (90%), with 55% of sales in urban centers. Regional investment includes 25% allocation in India, 20% in China, and 15% in Japan, supporting production expansion and product innovation. The company’s distribution network covers 72% of retail pharmacies and 48% of e-commerce platforms, reinforcing Baby Sunscreens market demand.

Recent Developments in Asia Pacific Baby Sunscreens

- 2025: Johnson & Johnson expanded mineral sunscreen production by 14%, totaling 28 million units.

- 2025: P&G increased hybrid sunscreen output by 18%, reaching 42 million units.

Research Methodology

The Asia Pacific Baby Sunscreens market research employed a comprehensive process, incorporating primary and secondary research techniques. Primary research involved interviews with over 120 industry experts, including manufacturers, distributors, and dermatologists, to gather qualitative and quantitative data. Secondary research included extensive review of company reports, government publications, trade journals, and regulatory filings. Market size estimation employed bottom-up and top-down approaches, integrating production volume, pricing trends, and historical growth data from 2022–2024 to project 2026–2034 forecasts. Key metrics included units produced, SPF compliance, adoption rates, and regional market share. Data triangulation ensured accuracy, while segmentation analysis by type (mineral, chemical, hybrid) and application (infants, toddlers, newborns) enabled identification of high-growth segments. This methodology provided reliable, actionable insights for stakeholders seeking strategic investment and expansion opportunities in the Asia Pacific Baby Sunscreens market.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Consumer Behavior and Premium Product Segments

Mandy Davis is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.