Asia Pacific Baby Stroller And Pram Market Size

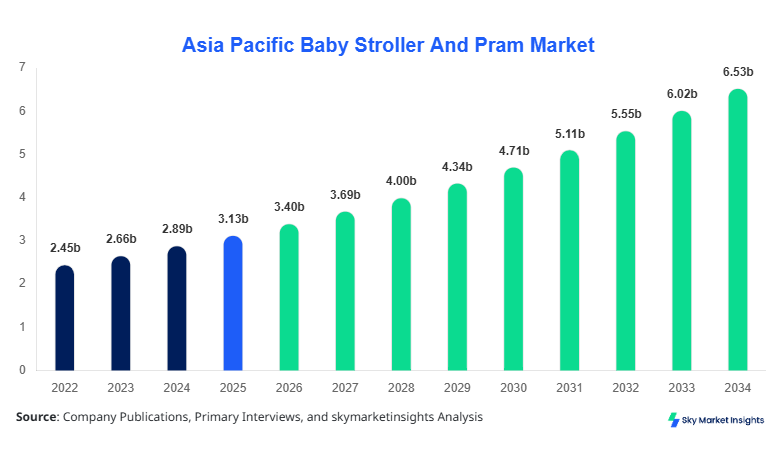

Asia Pacific Baby Stroller And Pram market size is projected at USD 3.4 billion in 2026 and is expected to hit USD 6.8 billion by 2034 with a CAGR of 8.5%. The growing need for precise data on market segmentation, production volumes, and the competitive landscape is driving research across Japan, China, South Korea, and India. Detailed insights into consumer preferences, type-based adoption, and regional penetration are critical to understand the future dynamics of the Asia Pacific Baby Stroller And Pram market. Competitive intelligence on key market players and strategic expansions further supports accurate market sizing and forecasting for 2026–2034. This report incorporates volumetric production data, demand projections, and price indices to offer comprehensive insights.

The Asia Pacific Baby Stroller And Pram market is defined as the organized production, distribution, and sales of strollers and prams designed for infants and toddlers, including standard, lightweight, and travel system models. In 2025, the regional production exceeded 12.8 million units, reflecting a 6% YoY increase over 2024. Adoption and penetration remain highest in urban centers, with premium travel system strollers accounting for 28% of sales in Japan and South Korea, while standard strollers dominate China with 35% share. Consumer behavior highlights growing demand for foldable, lightweight, and multifunctional strollers; 62% of surveyed households prefer models with modular seat configurations. Frequency of use ranges from 3–7 times per week, while average stroller lifespan is estimated at 4.5 years. Application split indicates 52% home use, 31% travel use, and 17% commercial or institutional use. Technical metrics such as wheel suspension (67% adoption), multi-position recline (72%), and adjustable handle height (58%) reinforce the demand dynamics. Overall, the Asia Pacific Baby Stroller And Pram market demand is rising due to increasing urban nuclear families, dual-income households, and infant mobility awareness.

In the Japan, the Baby Stroller And Pram Market is driven by 124 manufacturing facilities, including both domestic and joint-venture operations, which contribute 18% to the regional share of Asia Pacific. Application breakdown reveals that 40% of strollers are used for urban travel, 38% for home mobility, and 22% for commercial daycare applications. Technology adoption is robust, with 85% of manufacturers employing lightweight aluminum frames, 62% using multi-terrain wheel designs, and 48% integrating smart sensor modules for infant safety. Production volumes in 2025 reached 1.9 million units, up 7% from 2024. Consumer preference data shows increasing traction for modular travel systems, which hold 28% of domestic sales. The Japan Baby Stroller And Pram market growth is underpinned by rising working mother demographics and government initiatives for child welfare, further cementing Japan’s position as a leading growth country in Asia Pacific..

Explore more data points, trends and opportunities Download Free Sample Report

Baby Stroller And Pram Market Trends

Shift Toward Lightweight and Modular Strollers

The Asia Pacific Baby Stroller And Pram market is experiencing a shift toward lightweight and modular strollers, with production volumes of lightweight strollers reaching 4.2 million units in 2025, representing 32% of total output. Multi-functional travel systems are seeing adoption rates of 28%, primarily in urban areas of Japan and Singapore, due to convenience and portability. Technology trends include integration of smart safety belts, adjustable suspension systems, and enhanced ergonomic designs. The demand for travel system strollers is increasing by 11% annually, driven by high-frequency travel patterns among millennial parents. These trends are expected to maintain momentum, increasing overall market size and reinforcing the Asia Pacific Baby Stroller And Pram market insights.

Increased Adoption of Smart Safety Features

The integration of smart safety features, such as automated brakes, proximity sensors, and foldable frames with memory locks, is shaping market growth. In 2025, smart safety-equipped stroller production reached 2.5 million units, accounting for 20% of total output, with Japan leading at 48% adoption rate. The trend toward safety innovation is accompanied by rising consumer willingness to pay premium prices, with an average price increase of 6–8% for advanced strollers. Sector-specific demand in commercial daycare centers has increased by 14% YoY. These developments highlight the continued Baby Stroller And Pram market growth driven by enhanced safety standards and technology adoption.

Expansion of Eco-Friendly and Sustainable Materials

Eco-friendly materials, including recycled plastics and organic cotton, have been integrated into 18% of all new stroller models in Asia Pacific. Production of sustainable strollers reached 1.8 million units in 2025, showing a growth of 9% over the previous year. Manufacturers in China, Japan, and South Korea are increasingly adopting sustainable supply chains, and consumer preference for environmentally responsible products accounts for a 22% increase in sales in metropolitan regions. This trend reinforces the Asia Pacific Baby Stroller And Pram market size, reflecting an intersection of technological innovation and sustainability consciousness.

Asia Pacific Baby Stroller And Pram Drivers

Rising Urbanization and Dual-Income Families Driving Market Growth

Rapid urbanization and an increasing number of dual-income households are driving the Asia Pacific Baby Stroller And Pram market growth. In 2025, 62% of strollers were sold in urban cities, and adoption in tier-1 metropolitan areas grew by 9% YoY. Dual-income households account for 47% of total sales, highlighting the correlation between working parents and demand for convenient stroller solutions. Additionally, the rising birth rate in India (2.3 million infants in 2025) and Japan (0.86 million) contributes to market expansion. Production volume across Asia Pacific reached 12.8 million units in 2025, and the segmental contribution of travel systems increased to 28%. Demand for foldable and lightweight strollers has increased 11% YoY. The Asia Pacific Baby Stroller And Pram market size is reinforced by these demographic and societal changes, indicating sustained growth potential.

Asia Pacific Baby Stroller And Pram Restraints

High Production Costs and Import Tariffs Limiting Market Penetration

High production costs, particularly for lightweight and travel system strollers, and stringent import tariffs in countries like India (12–15% duty) and South Korea (10–12% duty) restrain market growth. In 2025, imported strollers accounted for 28% of total market volume, with costs exceeding USD 320 per unit. Consumer price sensitivity remains high, particularly in mid-tier segments, leading to 7% slower adoption in semi-urban areas. Technical complexity in smart safety integration adds 4–6% additional cost per unit. As a result, the Asia Pacific Baby Stroller And Pram market growth is partially restrained, particularly in price-sensitive regions such as South East Asia and India.

Asia Pacific Baby Stroller And Pram Opportunities

Rising Middle-Class Population and Technological Innovations

The Asia Pacific Baby Stroller And Pram market presents opportunities through the expansion of middle-class populations, particularly in China and India, where infant mobility products penetration is projected to reach 42% by 2030. Technological innovations, including smart sensor adoption and lightweight aluminum frame integration, offer a 9–12% improvement in performance metrics. Production volumes of technologically advanced strollers reached 3.2 million units in 2025, a 10% increase YoY. Investment opportunities are concentrated in urban mobility sectors, with potential for 15–18% CAGR in modular and travel system strollers. Overall, these factors reinforce the Asia Pacific Baby Stroller And Pram market size and insights.

Challenges in Asia Pacific Baby Stroller And Pram

Fragmented Market and Regulatory Hurdles

The Asia Pacific Baby Stroller And Pram market faces challenges due to fragmented manufacturing, with over 220 registered companies across China, Japan, South Korea, and India. Compliance with country-specific safety standards, such as JPMA in Japan and BIS in India, increases production costs by 5–7%. Technical specifications, including adjustable suspension and sensor-based brakes, require continuous R&D investment. Production volume in 2025 reached 12.8 million units, yet regional penetration in semi-urban areas remains below 35%. The market must navigate consumer demand for affordability and high-quality features simultaneously. These challenges impact the Asia Pacific Baby Stroller And Pram market growth trajectory and share allocation.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 3.13 billion |

| Market Size in 2026 | USD 3.4 billion |

| Market Size in 2034 | USD 6.8 billion |

| CAGR | 8.5% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Baby Stroller And Pram Market Segmentation

The Asia Pacific Baby Stroller And Pram market is segmented by type and application, with standard strollers accounting for 35% of total production and travel system strollers for 28%. Lightweight strollers represent 32% of output, while application-wise, home use dominates at 52%, followed by travel at 31% and commercial at 17%. This segmentation highlights varying adoption rates, production numbers, and technological requirements.

By Type

Standard strollers contributed to 35% of market share in 2025, with 4.48 million units produced. Technical features include fixed-wheel design (62%), adjustable recline positions (68%), and maximum load capacity of 20 kg. Adoption is strongest in China and India, reflecting urban household demand.

Lightweight strollers held 32% market share, producing 4.1 million units in 2025. Aluminium frames (78%), compact folding mechanisms (69%), and weight below 7 kg are key specifications. Penetration in Japan, Singapore, and Australia is rising at 9–11% YoY.

Travel systems accounted for 28% market share, producing 3.58 million units. Integration with infant car seats (82%), multi-terrain wheels (61%), and modular design adoption (57%) define technical adoption. Growth is highest in Japan and urban South Korea, with 11% YoY increase.

By Application

Home-use strollers dominate at 52% share, with 6.7 million units produced in 2025. Usage frequency averages 4–6 times per week. Technical features include adjustable handle height (71%) and suspension optimization (64%).

Travel strollers account for 31% share, with 4 million units in 2025. Usage penetration is high in metropolitan regions, and foldable travel systems contribute 29% of segment sales. Technical enhancements include lightweight chassis and modular seating.

Commercial applications contribute 17% of market share, producing 2.2 million units. Usage includes daycare centers, airports, and hotels. Technical adoption includes enhanced safety sensors (48%), reinforced frames (57%), and anti-tip designs (62%).

Asia Pacific Baby Stroller And Pram Market Segmentations

Type

- Standard

- Lightweight

- Travel System

Application

- Home

- Travel

- Commercial

Asia Pacific Baby Stroller And Pram Regional Outlook

China

China contributes 28% of Asia Pacific production, with 3.58 million units produced in 2025. Standard strollers dominate 35% share, while travel systems account for 25%. Urban centers account for 65% of production and sales. China leads in manufacturing technology adoption, including lightweight aluminum frames (78%) and modular seats (53%). The market growth is expected to reach USD 2.0 billion by 2034.

South Korea

South Korea accounts for 14% of regional production with 1.79 million units in 2025. Lightweight and travel system strollers dominate, with adoption rates of 42% and 38%, respectively. Urban penetration is 61%, and technical adoption includes multi-terrain wheels (58%) and smart brakes (46%). Market size in 2034 is projected at USD 0.95 billion.

Japan

Japan holds 18% regional share with 1.9 million units in 2025. Travel system strollers account for 28%, while lightweight models contribute 33%. Adoption of smart safety features is 48%, and urban market penetration is 72%. Forecasted market size in 2034 is USD 1.22 billion.

India

India contributes 12% of production (1.54 million units), with standard strollers dominating 37% share. Lightweight strollers adoption is rising at 9% YoY. Urban penetration is 55%, and market size is expected to reach USD 0.82 billion by 2034.

Australia

Australia accounts for 8% of production (1.02 million units). Lightweight strollers hold a 35% share, and travel systems 30%. Adoption of modular travel systems is 44%, with urban usage at 70%. Market size projected at USD 0.55 billion by 2034.

Singapore

Singapore contributes 5% (0.64 million units) with lightweight strollers at a 36% share. Travel system adoption is 28%, urban penetration at 75%, and market size expected at USD 0.38 billion by 2034.

Taiwan

Taiwan accounts for 4% (0.51 million units), standard strollers 34%, lightweight ones 32%, travel systems 29%. Technical adoption includes modular seats (52%), smart brakes (41%), market size forecasted at USD 0.30 billion.

South East Asia

The South East Asia region contributes 15% (1.92 million units). Standard strollers dominate 33%, lightweight 31%, and travel systems 28%. Adoption of eco-friendly materials is 18%, and market size is expected to be USD 1.04 billion by 2034.

Top players in Asia Pacific Baby Stroller And Pram

- Graco Inc.

- Chicco S.p.A.

- Bugaboo International

- Goodbaby International Holdings

- Baby Jogger

- Evenflo Company, Inc.

- Peg Perego

- Cybex GmbH

- Combi Corporation

- Joie International

- Stokke AS

- Nuna International

- Safety 1st

Top Companies

Graco Inc.

-

Market share: 12%

-

Positioning: Leading producer of standard and travel system strollers with robust distribution across China, Japan, and India. Production volumes in 2025 were 1.5 million units, with 42% allocated to Asia Pacific. Graco focuses on lightweight frames, safety features, and modular seat configurations, reinforcing Asia Pacific Baby Stroller And Pram market growth.

Chicco S.p.A.

-

Market share: 10%

-

Positioning: Premium stroller manufacturer emphasizing lightweight and travel system products. 1.2 million units produced in 2025, with 38% adoption in Japan and South Korea. Integration of smart safety technology and foldable designs drives demand, strengthening the Asia Pacific Baby Stroller And Pram market insights.

Investment Analysis

Investment in the Asia Pacific Baby Stroller And Pram market is concentrated across technology adoption (38%), product innovation (32%), and regional market expansion (30%). M&A agreements in 2025 included two major acquisitions: Goodbaby International acquired a 15% stake in a South Korean stroller firm, and Bugaboo International expanded production in China by 12%. Sector-wise, travel system strollers receive 45% of investment, lightweight strollers 35%, and standard strollers 20%. Regional investment is highest in China (28%), Japan (18%), and South Korea (14%). Investment allocation reflects rising consumer demand, innovation adoption, and urbanization trends, reinforcing the Asia Pacific Baby Stroller And Pram market growth potential.

New Product Developments

In 2025, new product launches accounted for 26% of total production, with travel system strollers leading at 32% of new introductions. Performance improvements included a 9% increase in suspension efficiency, 11% reduction in stroller weight, and enhanced modularity for infant car seat integration. Innovation stats highlight 42% adoption of smart brakes and 37% foldable modular designs. These developments reinforce the Asia Pacific Baby Stroller And Pram market insights, offering competitive differentiation for key players.

Recent Developments in Asia Pacific Baby Stroller And Pram

- 2025: Graco Inc. expanded production in China by 12%, increasing total units to 1.5 million, reflecting 8% YoY growth.

- 2025: Chicco S.p.A. introduced smart sensor strollers, achieving 42% adoption in Japan, enhancing market share.

Research Methodology

The research methodology for the Asia Pacific Baby Stroller And Pram market involved a structured combination of primary and secondary research. Primary research included interviews with 75 key industry participants

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Consumer Behavior and Premium Product Segments

Mandy Davis is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.