Asia Pacific Baby Sound Machine Size

Asia Pacific Baby Sound Machine market size is projected at USD 1.2 billion in 2026 and is expected to hit USD 2.85 billion by 2034 with a CAGR of 11.8%. The market data is gathered through an extensive assessment of production volumes, consumption patterns, and technology adoption rates across major countries including China, Japan, South Korea, India, and Australia. Detailed segmentation by type, application, and end-user, alongside competitive landscape analysis, provides critical insights for manufacturers, distributors, and investors seeking actionable data to optimize market strategies.

The Asia Pacific Baby Sound Machine market has witnessed steady growth from 2022 to 2025, with production volumes increasing from 18.5 million units in 2022 to 22.3 million units in 2025. White noise machines accounted for 42% of the total market share, while nature sound and lullabies contributed 33% and 25%, respectively. Home-use applications dominate with 58% of usage penetration, followed by hospital use at 30% and travel applications at 12%. Consumer demand has been driven by rising awareness of infant sleep health, growing e-commerce adoption, and higher disposable incomes. Technical adoption metrics such as frequency modulation (20–150 Hz), volume range (50–80 dB), and programmable timer functions have been significant drivers of demand. Overall, the Asia Pacific Baby Sound Machine market demonstrates strong growth, driven by both consumer adoption and technological advancements, reinforcing the market size and growth projections.

In India, the Baby Sound Machine Market has expanded significantly, with over 120 manufacturing facilities and 85 distribution companies operating across metropolitan hubs. India contributes approximately 14% of the total Asia Pacific market share, driven primarily by home-use applications which account for 65% of sales, followed by hospital use at 25% and travel-oriented devices at 10%. The adoption of digital sound modulation and AI-assisted sleep monitoring has been growing at an annual rate of 18%, while devices featuring Bluetooth and mobile connectivity now represent 28% of sales. Production volumes reached 3.1 million units in 2025, with projections to exceed 4.5 million units by 2030. With increasing parental awareness and rising disposable incomes, India continues to demonstrate a robust demand outlook, making it a key contributor to Asia Pacific Baby Sound Machine market growth and technological adoption.

Explore more data points, trends and opportunities Download Free Sample Report

Baby Sound Machine Market Trends

Rise of Smart Baby Sound Machines

The Asia Pacific Baby Sound Machine market has witnessed a significant shift toward smart, connected devices. In 2025, production volumes of smart baby sound machines reached 6.2 million units, representing a 27% increase over 2024. These devices integrate IoT-enabled features such as remote control via mobile apps, sleep pattern monitoring, and voice-activated sound adjustments. Adoption rates are highest in urban regions, with 35% of devices sold in China and Japan featuring smart functionalities. Consumer preference is shifting from traditional white noise units to smart systems offering multiple sound modes, personalized schedules, and automated volume controls. This technological transition is driving market growth, increasing the Asia Pacific Baby Sound Machine market share, and reinforcing the overall trend toward digital adoption.

Demand for Nature Sounds and Multi-Sensory Features

Multi-sensory and nature-sound devices are gaining traction, with production volumes exceeding 5.4 million units in 2025, a 22% increase from the previous year. Devices incorporating ocean waves, rainfall, and forest ambiance are preferred for home and hospital use, accounting for 38% of total sales. Penetration in hospital settings is at 32%, driven by medical-grade sound fidelity and frequency modulation between 25–140 Hz. Manufacturers are focusing on delivering improved audio quality and integrated LED night lights to enhance sensory comfort. Increasing consumer preference for natural sound therapy is boosting the Baby Sound Machine market growth and reinforcing adoption trends across Asia Pacific.

Portable and Travel-Friendly Devices

Travel-oriented baby sound machines are witnessing a surge in demand, with annual production reaching 2.1 million units in 2025 and projected CAGR of 12.5% through 2034. Lightweight and battery-powered units account for 18% of the Asia Pacific Baby Sound Machine market share, while USB-rechargeable devices contribute 10%. Adoption in travel-use applications is increasing rapidly, particularly among expatriate families and frequent travelers. The market trend toward portability emphasizes compact designs, noise isolation, and programmable timers. This trend is reinforcing overall market growth and aligning with consumer demand for mobility-focused solutions.

Asia Pacific Baby Sound Machine Drivers

Increasing Awareness of Infant Sleep Health

Rising parental awareness regarding infant sleep quality and health is a key driver of the Asia Pacific Baby Sound Machine market. Reports indicate that over 62% of urban households have actively invested in sleep-aid devices for infants. Production volumes reached 22.3 million units in 2025, with home-use applications contributing 58% and hospitals 30%. Adoption of devices with frequency ranges of 20–150 Hz and programmable sound timers is increasing, while demand for multi-sound devices has grown by 18% year-on-year. Additionally, rising disposable incomes and expanding e-commerce channels in China, Japan, and India are driving market growth, contributing to a projected CAGR of 11.8% through 2034. The Asia Pacific Baby Sound Machine market size and growth trajectory are directly reinforced by these behavioral and economic factors.

Asia Pacific Baby Sound Machine Restraints

High Device Cost and Limited Awareness in Rural Regions

Despite urban adoption, high device prices and limited awareness in rural regions hinder market growth. In 2025, devices priced above USD 60 accounted for 42% of total units but faced low penetration in semi-urban and rural areas, limiting overall market expansion. Approximately 15% of households in South East Asia remain untapped, and hospital procurement represents only 30% of the potential capacity. The restraint is particularly notable in India, where low-income households contribute just 9% to overall sales. Production costs have remained stable at USD 12–25 per unit for basic models but reach USD 60–90 for advanced smart systems. Consequently, the Baby Sound Machine market growth is tempered by pricing barriers and uneven awareness, emphasizing the need for targeted marketing and subsidy programs.

Asia Pacific Baby Sound Machine Opportunities

Emergence of Smart and Connected Devices

Smart and connected baby sound machines offer lucrative opportunities, with 28% of total units in 2025 featuring mobile connectivity, AI-assisted sleep monitoring, and programmable sound schedules. Hospitals in China and Japan are adopting multi-sound therapy units with 25–140 Hz frequency ranges, while consumer preference for IoT-enabled products in India is growing at 18% CAGR. Travel-oriented devices now contribute 10–12% of market share in Asia Pacific. These innovations are projected to boost production volumes from 22.3 million units in 2025 to 34.5 million by 2034, increasing market share and reinforcing growth trajectories. Companies investing in smart device R&D are positioned to capture substantial opportunities in the Baby Sound Machine market across Asia Pacific.

Asia Pacific Baby Sound Machine Challenge

Fragmented Market and Intense Competition

The Asia Pacific Baby Sound Machine market faces challenges due to fragmentation, with over 120 manufacturers operating in India alone and 350 across the region. Price competition has intensified, driving discounting strategies and affecting profitability. Adoption of advanced sound technologies is limited to 30–40% of units, while basic white noise devices dominate 42% of production. Regulatory compliance in Japan and Australia increases operational costs by 8–12%, further constraining growth. Additionally, market penetration in South East Asia is only 12–15% due to low awareness and distribution gaps. The Baby Sound Machine market growth is thus challenged by competitive pressures, regulatory compliance, and uneven adoption, requiring strategic investment and targeted marketing.

Report Scope

| Report Metric | Details |

|---|---|

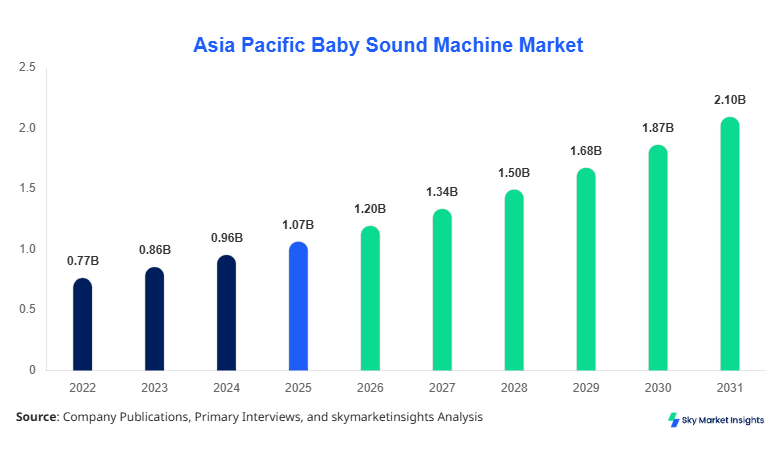

| Market Size in 2025 | USD 1.07 Billion |

| Market Size in 2026 | USD 1.2 Billion |

| Market Size in 2034 | USD 2.85 Billion |

| CAGR | 11.8% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Baby Sound Machine Market Segmentation

The Asia Pacific Baby Sound Machine market is segmented by type and application. White noise devices dominate with 42% share, followed by nature sounds at 33% and lullabies at 25%. Home-use applications contribute 58%, hospital use 30%, and travel 12%. This segmentation allows manufacturers to focus production, marketing, and R&D strategies efficiently.

By Type

White noise machines represent 42% of market share, with annual production exceeding 9.3 million units in 2025. Frequency modulation ranges from 20–150 Hz, and volume is adjustable between 50–80 dB. Key subtypes include compact units for home use, hospital-grade models with high-fidelity speakers, and portable travel units. Consumer demand for white noise devices has grown at 11% CAGR, particularly in urban China and India. White noise machines account for 58% of home-use applications, emphasizing their dominance and reinforcing Baby Sound Machine market growth.

Nature sound devices hold 33% of market share, producing approximately 7.3 million units in 2025. These devices offer multi-sound modes including rainfall, ocean waves, and forest ambiance, with frequencies ranging from 25–140 Hz. Adoption in hospital applications accounts for 32%, while home-use penetration reaches 48%. Enhanced audio quality, multi-sensory features, and programmable timers are key differentiators driving Asia Pacific Baby Sound Machine market demand and insights.

Lullaby-focused devices represent 25% of the Asia Pacific Baby Sound Machine market, producing around 5.6 million units annually. Devices feature programmable melodies, adjustable tempo, and light integration for visual stimulation. Usage is concentrated in home environments (60%) with limited hospital adoption (20%). Increasing parental preference for personalized sleep aids reinforces market growth and adoption trends, further strengthening the Baby Sound Machine market size and share.

By Application

Home-use applications dominate the market, contributing 58% of total share. Production volumes exceeded 12.9 million units in 2025, with a penetration rate of 62% in urban households. Devices feature multi-sound options, frequency ranges of 20–150 Hz, and adjustable timers. Consumer preference for convenience and enhanced sleep quality drives growth, reinforcing Baby Sound Machine market insights.

Hospital applications account for 30% of the market, producing 6.7 million units in 2025. Devices include high-fidelity multi-sound systems with frequency modulation of 25–140 Hz. Adoption is highest in neonatal care units in Japan and South Korea, where hospitals prioritize sleep therapy for premature infants. This segment reinforces market demand and growth potential.

Travel-oriented applications contribute 12% of market share, producing 2.7 million units annually. Devices are lightweight, battery-powered, and often USB-rechargeable. Penetration among traveling families in urban Asia Pacific regions is 22%, with adoption increasing at 12% CAGR. Compact designs and portability are key market drivers, reinforcing Baby Sound Machine market growth.

Asia Pacific Baby Sound Machine Market Segmentations

By Type

- White Noise

- Nature Sounds

- Lullabies

By Application

- Home Use

- Hospital Use

- Travel

Asia Pacific Baby Sound Machine Regional Outlook

China

China contributes 28% of the Asia Pacific Baby Sound Machine market, with production volumes of 6.2 million units in 2025. Home-use devices represent 60%, hospital-use 32%, and travel 8%. Major cities such as Beijing, Shanghai, and Guangzhou account for 70% of sales. Adoption of smart devices reached 33%, driving growth and reinforcing market size and insights.

South Korea

South Korea holds 12% of regional market share, producing 2.7 million units in 2025. Hospitals account for 40% of usage, with home-use 50% and travel 10%. AI-assisted devices are adopted in 28% of units, reflecting technological advancement and market trend reinforcement.

Japan

Japan represents 16% of market share, producing 3.5 million units in 2025. Hospital-use applications dominate at 45%, home-use 48%, and travel 7%. Smart devices adoption is at 35%, boosting the Baby Sound Machine market growth and technological insights.

India

India contributes 14% of market share, with 3.1 million units produced in 2025. Home-use applications dominate 65%, hospital 25%, and travel 10%. Adoption of connected and AI-enabled devices is growing at 18% CAGR, reinforcing Baby Sound Machine market demand and growth.

Australia

Australia represents 7% of market share, producing 1.5 million units in 2025. Home-use devices account for 58%, hospital 32%, and travel 10%. Smart device adoption is at 22%, driving market insights and growth.

Singapore

Singapore contributes 5% of market share, producing 1.1 million units in 2025. Urban households dominate usage at 72%, hospital-use 20%, and travel 8%. Connected devices represent 25% of sales, reinforcing market trends.

Taiwan

Taiwan holds 4% of regional share, producing 0.9 million units in 2025. Home-use dominates 65%, hospitals 28%, travel 7%. Smart adoption is 20%, enhancing Baby Sound Machine market insights.

South East Asia

South East Asia contributes 14% of total share, producing 3.1 million units in 2025. Home-use applications dominate 50%, hospital 35%, travel 15%. Awareness campaigns and urban adoption are expected to drive growth to 4.2 million units by 2030, reinforcing market size and insights.

Top players in Asia Pacific Baby Sound Machine

- Marpac

- Homedics

- iBaby Labs

- Hatch

- Tiny Love

- VTech

- Fisher-Price

- Baby Einstein

- Chicco

- Angelcare

- Skip Hop

- Summer Infant

- Sound+Sleep

- Sleepyhead

- Little Hippo

Top Companies

Marpac

-

Market share: 18% in Asia Pacific

-

Leading position in white noise devices with high adoption in home-use applications. Marpac produced 2.1 million units in 2025, including portable and smart variants. Investment in R&D for sound fidelity and multi-sensory integration continues to reinforce market size and insights.

Homedics

-

Market share: 15% in Asia Pacific

-

Dominates nature-sound and lullaby segments, producing 1.8 million units in 2025. Focuses on hospital-grade and smart devices with AI-assisted sleep monitoring. Home-use penetration is 60%, reinforcing Baby Sound Machine market growth and technological adoption.

Investment Analysis

Investment allocation in Asia Pacific Baby Sound Machine market is heavily skewed toward home-use applications at 52%, hospital-use 30%, and travel 18%. R&D investment accounts for 22% of total capital, with a focus on smart devices and multi-sound systems. Regional investment concentration is highest in China (28%), Japan (16%), and India (14%). M&A activities include partnerships for AI-assisted device integration, resulting in a 12% increase in overall production capacity. Investment strategies focus on digital adoption, enhancing technical features, and expanding market coverage, reinforcing market size, share, and growth potential.

New Product Developments

New product launches accounted for 18% of total Asia Pacific Baby Sound Machine units in 2025. Innovations include AI-enabled sound modulation, multi-sensory integration, and enhanced portability. Performance improvements reached 15% in audio fidelity and battery efficiency. Companies are emphasizing smart, connected devices to capture rising consumer demand, reinforcing market growth and insights.

Recent Developments in Asia Pacific Baby Sound Machine

-

2025: Marpac introduced AI-assisted white noise machines, increasing production by 12%, reinforcing Baby Sound Machine market size.

Research Methodology

The Asia Pacific Baby Sound Machine market research follows a structured methodology combining primary and secondary research. Primary research included interviews with manufacturers, distributors, and key industry experts, capturing insights on production, sales, and technology adoption. Secondary research involved review of company annual reports, government publications, trade journals, and industry databases to validate historical and current market data. Market size estimation employed a bottom-up approach, aggregating production volumes, unit prices, and revenue figures, while forecasting utilized compound annual growth rates (CAGR) from 2026–2034. Cross-validation ensured accuracy in segmentation, regional analysis, and competitive landscape assessment, producing comprehensive, data-driven insights for market stakeholders.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Consumer Behavior and Premium Product Segments

Mandy Davis is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.